| Study Period | 2019 - 2030 |

| Market Volume (2025) | 0.45 Million tons |

| Market Volume (2030) | 2.12 Million tons |

| CAGR | 36.35 % |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Green Hydrogen Market Analysis

The Green Hydrogen Market size is estimated at 0.45 million tons in 2025, and is expected to reach 2.12 million tons by 2030, at a CAGR of 36.35% during the forecast period (2025-2030).

The green hydrogen industry is witnessing an unprecedented transformation as industrial sectors accelerate their decarbonization efforts. According to the World Steel Association, as of April 2024, over 200 low-carbon steel projects have been announced across various shades of 'green,' marking a significant shift in industrial practices. Major steel manufacturers are increasingly integrating green hydrogen into their production processes, with companies like Baowu and Ansteel Group pioneering breakthrough hydrogen technology in hydrogen-based steel production. This industrial evolution is complemented by rapid technological advancements in electrolyzer efficiency and capacity scaling, enabling more cost-effective green hydrogen production.

Infrastructure development for green hydrogen production and distribution is gaining momentum globally, with significant investments in production facilities and transportation networks. The World Economic Forum reports that approximately 98% of ammonia value chain emissions stem from the hydrogen production stage, driving urgent infrastructure modernization initiatives. Companies are developing innovative solutions for hydrogen infrastructure, including compression technologies, liquefaction facilities, and conversion to carriers like ammonia or methanol. These infrastructure developments are crucial in establishing a robust supply chain capable of supporting the growing demand across various industries.

The market is experiencing a significant shift in production technologies and efficiency improvements. According to IRENA, global ammonia demand is projected to grow to 600 million tons by 2050, necessitating rapid scaling of green hydrogen production capabilities. Leading manufacturers are investing in advanced hydrogen technology, with innovations in both alkaline and PEM (Proton Exchange Membrane) systems driving improved efficiency and reduced production costs. The industry is witnessing a trend toward larger-scale projects, with multiple gigawatt-scale facilities under development worldwide.

Policy frameworks and investment landscapes are evolving to support market growth, with governments worldwide implementing supportive regulations and funding mechanisms. Major economies are introducing production tax credits, contracts for difference (CfD) schemes, and renewable hydrogen mandates to accelerate market development. The European Union's comprehensive hydrogen strategy, targeting 40 GW of electrolyzer capacity by 2030, exemplifies the policy-driven approach to market development. This regulatory support is complemented by substantial private sector investments, with numerous companies forming strategic partnerships and joint ventures to advance green hydrogen projects and technologies.

Green Hydrogen Market Trends

Realizing the Potential in the Chemical Industry

The chemical industry stands as one of the largest consumers of industrial hydrogen, with the sector being the primary user of energy across all industrial segments. This is particularly evident in ammonia production, where global output reached approximately 150 million metric tons in 2022, with significant applications in fertilizer manufacturing and household cleaning products. The industry's massive scale is further demonstrated by China's substantial chemical fertilizer consumption of 51.9 million metric tons in 2021, while the United States recorded an impressive ammonia production of 13 million metric tons in 2022, marking a 50% increase over eight years.

The integration of green hydrogen in chemical manufacturing processes represents a transformative opportunity for sustainable hydrogen production. Currently, the European Union alone utilizes about 10 million tons of hydrogen annually, primarily as feedstock for ammonia production and in the refining sector. This significant consumption pattern is driving major investments in renewable hydrogen production infrastructure, as exemplified by Yara International's partnership with Linde Engineering in January 2022 for constructing a green hydrogen demonstration plant at their ammonia production facility in Norway. The industry's commitment to clean hydrogen production is further evidenced by numerous fertilizer manufacturing companies announcing plans to expand commercial production of green ammonia, with projects like Iberdrola's EUR 750 million plant designed specifically for green ammonia production in June 2023.

Understand The Key Trends Shaping This Market

Download PDF

Growing Environmental Concerns Regarding Carbon Emissions

The urgency to address carbon emissions has positioned clean energy hydrogen as a crucial solution in the global fight against climate change. According to the International Energy Agency, the implementation of green hydrogen production methods could prevent the emission of 830 million tonnes of CO2 that are currently released annually through fossil fuel-based hydrogen production. This potential for emission reduction is particularly significant given the IEA's projection that global energy demand will rise by 25-30% by 2040, necessitating immediate action to develop sustainable energy alternatives.

The industrial sector's transition to hydrogen energy is gaining momentum through substantial government support and corporate commitments. Germany's ambitious targets exemplify this trend, with projected hydrogen production demand expected to reach 90-110 TWh by 2030 and exceed 600 TWh by 2050. Similarly, the United Arab Emirates has set forth an aggressive hydrogen strategy, aiming to capture a quarter of the global low-carbon hydrogen market by 2030. Japan's recent announcement of a USD 3.4 billion investment from its green innovation fund to accelerate hydrogen generation, research, development, and promotion over the next decade further demonstrates the global commitment to addressing environmental concerns through hydrogen energy adoption. These initiatives are complemented by corporate actions, such as Linde's efforts to establish a hydrogen energy storage economy in Greece and Iberdrola's commitment to produce 350,000 tonnes of green hydrogen annually by 2030, with a portfolio of projects totaling 2,400 MW.

Segment Analysis: End-User Industry

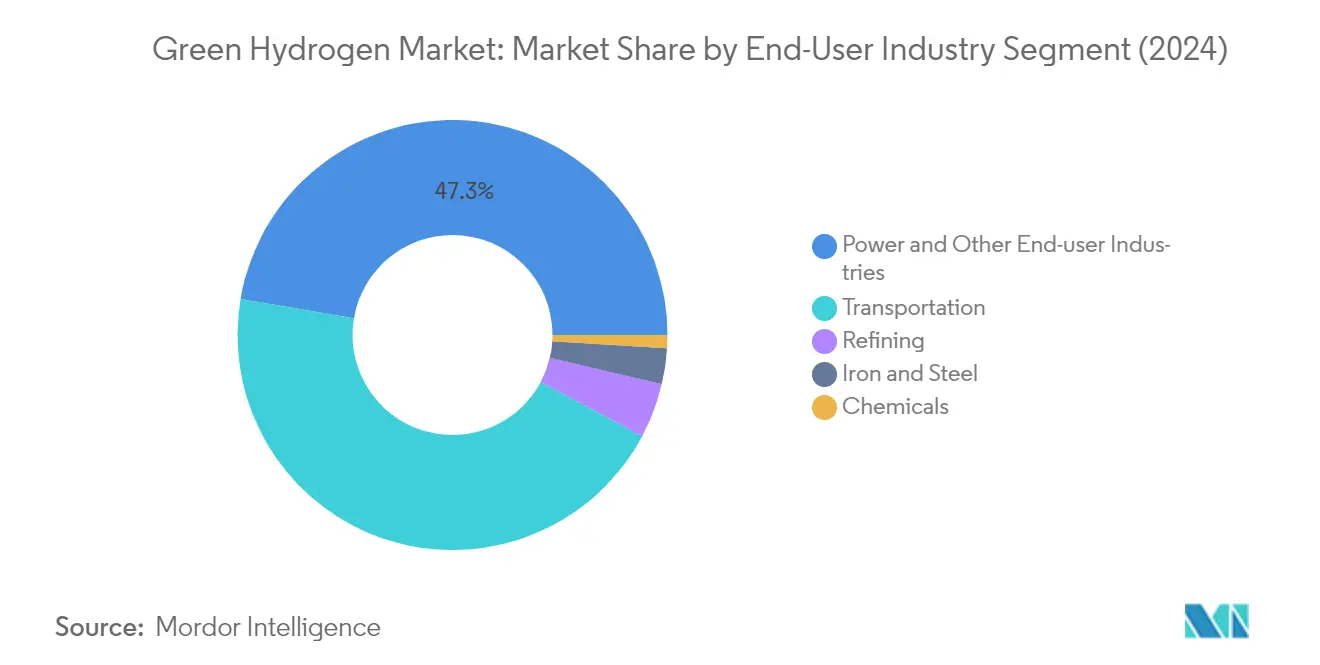

Power and Other End-user Industries Segment in Green Hydrogen Market

The Power and Other End-user Industries segment dominates the global green hydrogen market, commanding approximately 47% of the market share in 2024. This significant market position is driven by the increasing adoption of hydrogen energy storage in power generation facilities worldwide. The segment's growth is particularly evident in major economies like China, India, and the United States, where numerous power generation facilities are integrating green hydrogen storage solutions. The rising demand for round-the-clock power using hydrogen energy storage, exemplified by projects like India's 100 MW demonstration initiative, showcases the segment's robust market presence. Furthermore, the building sector's transition toward eco-friendly solutions, coupled with directives like the EU's Energy Performance of Buildings Directive and the US Inflation Reduction Act, has strengthened this segment's market leadership.

Chemicals Segment in Green Hydrogen Market

The Chemicals segment is emerging as the fastest-growing segment in the green hydrogen market, with a projected growth rate of approximately 47% during 2024-2029. This exceptional growth is fueled by the increasing adoption of industrial hydrogen in chemical manufacturing processes, particularly in green ammonia and methanol production. Major chemical manufacturers worldwide are investing heavily in hydrogen production facilities, as evidenced by projects like Iberdrola's EUR 750 million green ammonia plant and NEOM's large-scale production facility. The segment's growth is further accelerated by government initiatives supporting green chemical production, such as India's National Green Hydrogen Mission and the European Commission's approval of substantial subsidies for clean hydrogen production in industrial applications. The trend toward sustainable chemical production and the growing demand for green ammonia in agriculture and industrial applications continue to drive this segment's rapid expansion.

Remaining Segments in End-User Industry

The remaining segments in the green hydrogen market include Transportation, Refining, and Iron & Steel, each playing crucial roles in market development. The Transportation segment is witnessing significant growth through the increasing adoption of hydrogen fuel cell vehicles and infrastructure development across major economies. The Refining segment is experiencing transformation as major refineries worldwide integrate hydrogen generation to reduce their carbon footprint and meet stringent environmental regulations. The Iron & Steel segment is gaining momentum through various decarbonization initiatives, with major steel manufacturers implementing hydrogen fuel technologies in their production processes. These segments collectively contribute to the market's diversification and demonstrate the versatile applications of hydrogen energy across different industrial sectors.

Green Hydrogen Market Geography Segment Analysis

Green Hydrogen Market in Asia-Pacific

The Asia-Pacific region has emerged as a powerhouse in the global green hydrogen market, driven by ambitious national strategies and substantial investments in renewable energy infrastructure. China leads the regional market with its massive electrolyzer capacity and comprehensive hydrogen strategy, while India has launched its National Green Hydrogen Mission with significant funding allocations. Japan and South Korea have also demonstrated strong commitment through their respective hydrogen roadmaps and industrial applications, particularly in the mobility and power generation sectors. The region's competitive advantage stems from its robust manufacturing capabilities, favorable renewable energy conditions, and strong government support for decarbonization initiatives.

Green Hydrogen Market in China

China dominates the Asia-Pacific green hydrogen market through its comprehensive approach to developing the hydrogen economy. The country has unveiled its inaugural long-term hydrogen plan spanning 2021-2035, emphasizing domestic hydrogen industry development through technological advancements and enhanced manufacturing capabilities. With approximately 95% share of the Asia-Pacific market in 2024, China's leadership is reinforced by major projects like Sinopec's Xinjiang Kuqa Green Hydrogen Project and significant investments in electrolyzer manufacturing. The country's strategy focuses on integrating green hydrogen across various sectors, including industrial applications, transportation, and power generation, supported by provincial initiatives and strong policy frameworks.

Green Hydrogen Market Growth Dynamics in China

China's green hydrogen market is projected to grow at approximately 39% annually from 2024 to 2029, driven by aggressive capacity expansion plans and technological innovations. The country's growth trajectory is supported by initiatives like the China Hydrogen Alliance's "Renewable Hydrogen 100" program, which targets significant increases in electrolyzer capacity. Major energy companies are investing heavily in large-scale projects, such as Sinopec's developments in Inner Mongolia and CEEC's comprehensive hydrogen energy industrial parks. The nation's commitment to achieving carbon neutrality by 2060 continues to drive investments in green hydrogen infrastructure and technology development.

Green Hydrogen Market in North America

North America's green hydrogen market is characterized by strong policy support, technological innovation, and increasing private sector investments. The United States leads the regional market with substantial federal funding and incentives through the Inflation Reduction Act and Infrastructure Investment and Jobs Act. Canada has established itself as a key player with its national hydrogen strategy and provincial initiatives, while Mexico is developing its regulatory framework to promote green hydrogen adoption. The region's market is particularly driven by applications in industrial decarbonization, transportation, and power generation sectors.

Green Hydrogen Market in United States

The United States has established itself as the dominant force in North America's green hydrogen market, holding approximately 75% of the regional market share in 2024. The country's leadership is supported by significant federal investments, including a $750 million allocation for clean hydrogen projects across 24 states. The U.S. Department of Energy's comprehensive hydrogen program and strategic roadmap have created a robust framework for market growth, particularly in sectors like heavy industry, transportation, and energy storage.

Green Hydrogen Market Growth Dynamics in United States

The United States is set to maintain its regional leadership with a projected growth rate of approximately 24% annually from 2024 to 2029. This growth is driven by major initiatives like Plug Power's expansion plans to achieve 500 tons/day production capacity by 2025, and ambitious projects such as Green Hydrogen International's 60 GW renewable hydrogen project. The country's growth is further supported by strong policy frameworks, tax incentives, and increasing private sector investments in hydrogen infrastructure and technology development.

Green Hydrogen Market in Europe

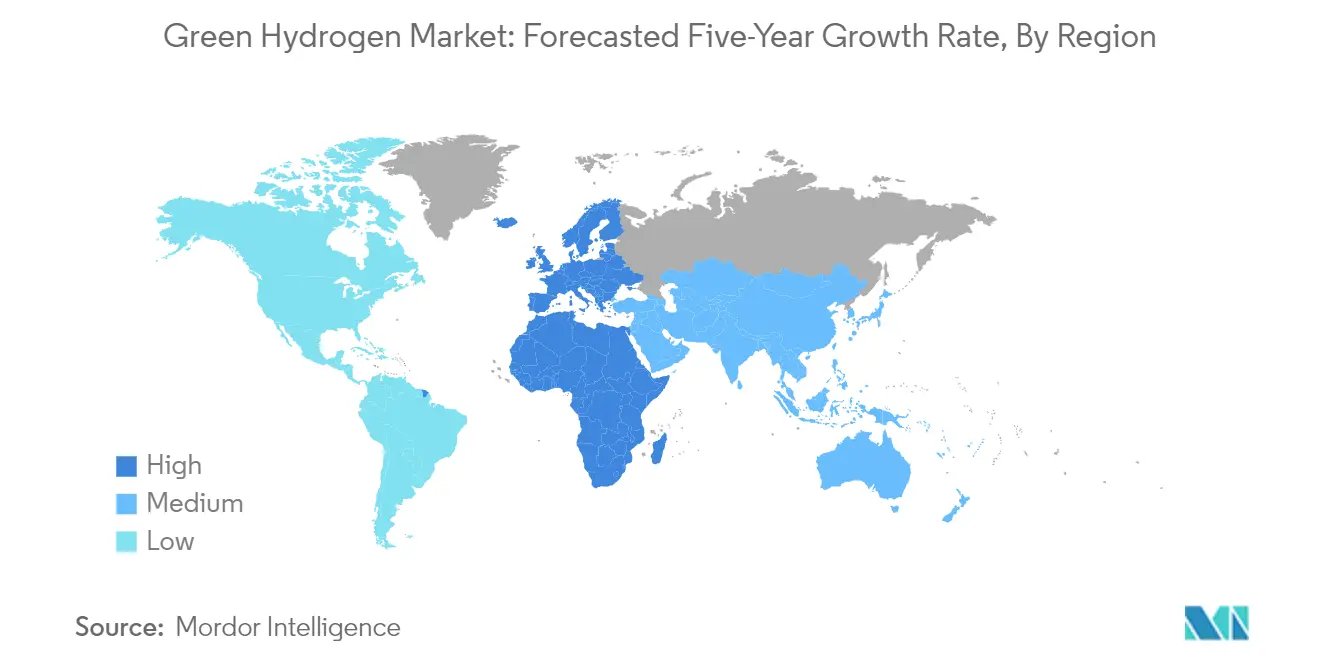

Europe's green hydrogen market is characterized by a strong regulatory framework and collaborative cross-border initiatives. Germany leads the region with its comprehensive National Hydrogen Strategy and ambitious production targets, while France, the United Kingdom, and Italy have developed their respective hydrogen roadmaps. The region's market is particularly driven by the European Union's comprehensive hydrogen strategy and significant investments in large-scale projects. The market benefits from strong public-private partnerships and a clear focus on industrial decarbonization and sustainable mobility solutions.

Green Hydrogen Market in Germany

Germany has positioned itself as the leader in Europe's green hydrogen market through its comprehensive approach to market development. The country's leadership is demonstrated through its ambitious production targets, doubling its national target for green hydrogen production to 10 GW by 2030. Germany's market dominance is supported by significant investments in research and development, strong industrial partnerships, and a robust infrastructure development plan.

Green Hydrogen Market Growth Dynamics in France

France has emerged as the fastest-growing market in Europe's green hydrogen sector, driven by its strategic focus on developing green hydrogen production capabilities and applications. The country's growth is supported by significant government backing, including substantial investments in electrolyzer capacity and green hydrogen projects. France's commitment to becoming a leader in green hydrogen technology is demonstrated through various initiatives and partnerships across industrial, mobility, and energy sectors.

Green Hydrogen Market in Rest of the World

The Rest of the World region, encompassing South America and the Middle East & Africa, shows significant potential in the green hydrogen market. In South America, countries like Chile, Brazil, and Argentina are developing comprehensive hydrogen strategies and attracting significant investments. The Middle East & Africa region is leveraging its renewable energy potential and strategic location to establish itself as a future green hydrogen export hub. Saudi Arabia leads the market size in this region, while South Africa demonstrates the fastest growth potential, supported by its Hydrogen Society Roadmap and significant investments in green hydrogen infrastructure.

Get Analysis on Important Geographic Markets

Download PDF

Green Hydrogen Industry Overview

Top Companies in Green Hydrogen Market

The green hydrogen market is witnessing significant strategic developments driven by major energy and chemical companies. Industry leaders are focusing on developing innovative hydrogen technology and scaling up production capacities through large-scale facilities and demonstration projects. Companies are actively pursuing vertical integration strategies, from renewable energy generation to end-user applications, while establishing strategic partnerships across the value chain. Operational excellence is being achieved through investments in advanced manufacturing capabilities and digitalization initiatives. Geographic expansion is primarily targeted at regions with favorable renewable energy resources and supportive regulatory frameworks, with particular emphasis on Europe, Asia-Pacific, and North America. The industry is also seeing increased collaboration between technology providers and industrial users to develop customized solutions for specific applications.

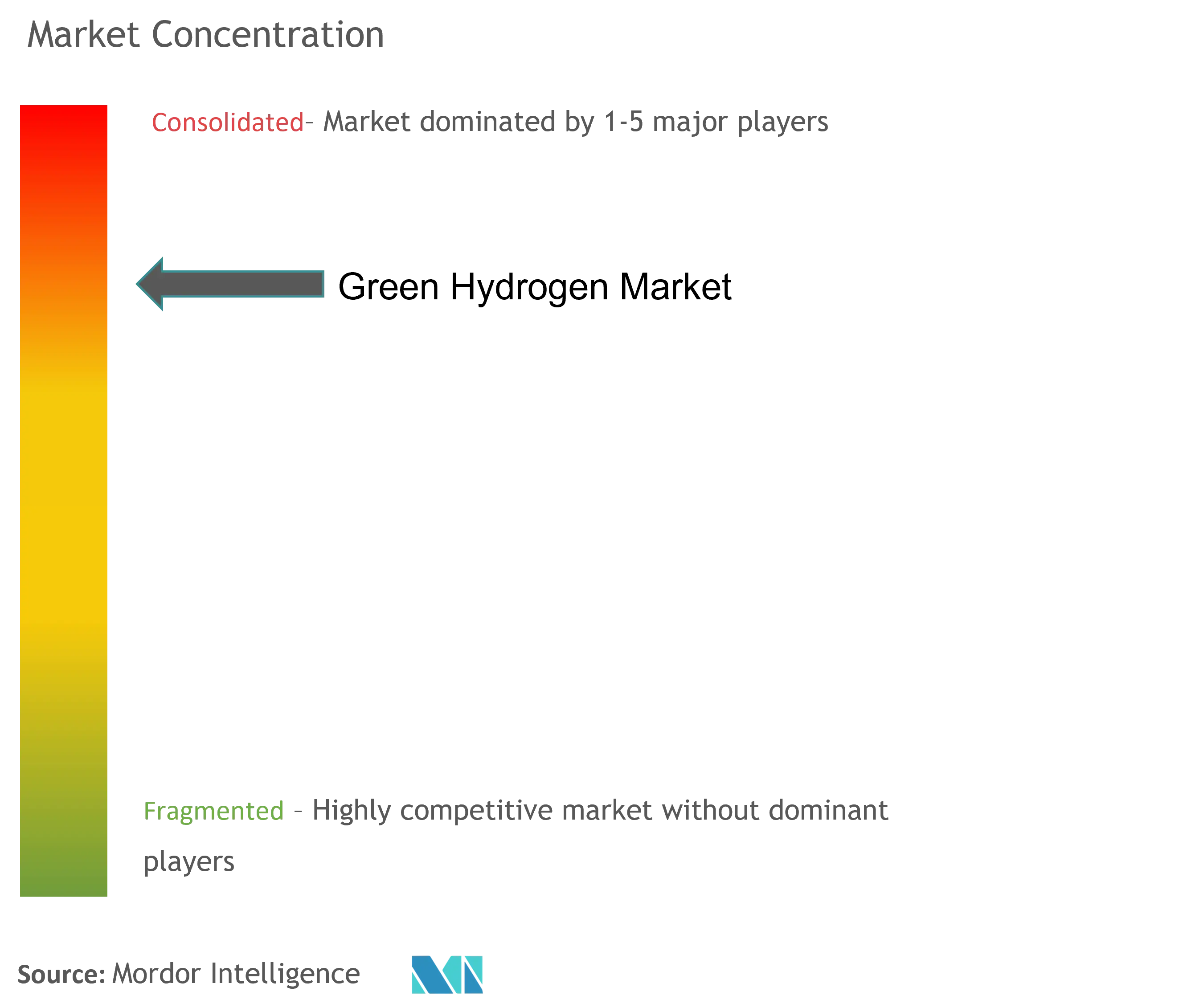

Consolidated Market Led By Energy Giants

The green hydrogen industry structure is characterized by the dominance of large energy conglomerates and established chemical companies, with the top five players holding a significant market share. These industry leaders leverage their extensive infrastructure, technical expertise, and financial resources to maintain their competitive positions. The market is partially consolidated, with major players like China Petroleum & Chemical Corporation, Ningxia Baofeng Energy Group, and Plug Power Inc. leading the space. The competitive landscape is evolving through strategic partnerships, joint ventures, and technology licensing agreements, particularly in emerging markets.

The market is experiencing active merger and acquisition activity, primarily focused on technology acquisition and market expansion. Large energy companies are acquiring innovative startups and technology providers to strengthen their positions in the hydrogen production market. Regional players are forming alliances with global leaders to access advanced technologies and expand their market presence. The industry is also witnessing increased participation from renewable energy companies and industrial gas suppliers, adding to the competitive dynamics. New entrants are primarily focusing on niche applications and specific geographic markets, while established players are expanding their presence across multiple end-user segments.

Innovation and Scale Drive Market Success

Success in the hydrogen energy market increasingly depends on technological innovation, cost competitiveness, and operational scale. Incumbent players are focusing on reducing production costs through improved electrolyzer efficiency and integration with renewable energy sources. Companies are investing in research and development to enhance system performance and develop proprietary technologies. Strategic partnerships with end-users in key industries like refining, chemicals, and transportation are becoming crucial for securing long-term demand. Market leaders are also emphasizing sustainability credentials and carbon reduction capabilities to align with global environmental goals.

For new entrants and challenger companies, success factors include developing specialized solutions for specific applications, establishing a strong regional presence, and forming strategic alliances. The ability to navigate regulatory frameworks and secure government support remains critical for both established players and new entrants. Companies must also address infrastructure challenges and develop efficient distribution networks. The market's future competitive dynamics will be shaped by factors such as technology advancement, regulatory support, and the ability to achieve economies of scale. Players must also consider the evolving needs of end-users and potential substitution risks from alternative clean energy solutions.

Green Hydrogen Market Leaders

-

China Petroleum & Chemical Corporation

-

Ningxia Baofeng Energy Group Co. LTD

-

Plug Power Inc.

-

China Three Gorges Corporation (CTG)

-

Tidewater Renewables Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Green Hydrogen Market News

- June 2024: TotalEnergies and Air Products and Chemicals Inc. signed a 15-year agreement to supply 70,000 tons of green hydrogen annually in Europe starting in 2030. Under this agreement, Air Products and Chemicals Inc. plans to deliver green hydrogen to TotalEnergies’ Northern European refineries. This green hydrogen can avoid around 700,000 tons of CO₂ each year.

- June 2024: ExxonMobil and Air Liquide announced an agreement to support the production of low-carbon hydrogen and low-carbon ammonia at ExxonMobil’s Baytown, Texas facility. The agreement will enable the transportation of low-carbon hydrogen through Air Liquide’s existing pipeline network.

- September 2023: TotalEnergies and Air Liquide signed an agreement for the long-term supply of green and low-carbon hydrogen to the TotalEnergies refining and petrochemical platform in Normandy. The project contributes to the decarbonization of the Gonfreville site, reducing its CO2 emissions by up to 150,000 tons a year.

Green Hydrogen Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

-

4.1 Market Drivers

- 4.1.1 Realizing the Potential in the Chemical Industry

- 4.1.2 Growing Environmental Concerns Regarding Carbon Emissions

-

4.2 Market Restraints

- 4.2.1 High Investment Cost of Green Hydrogen

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

- 4.5 Technological Snapshot

5. MARKET SEGMENTATION (Market Size in Volume)

-

5.1 End-user Industry

- 5.1.1 Refining

- 5.1.2 Chemicals

- 5.1.3 Iron and Steel

- 5.1.4 Transportation

- 5.1.5 Power and Other End-user Industries

-

5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Rest of Europe

- 5.2.4 Rest of the World

- 5.2.4.1 South America

- 5.2.4.2 Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

-

6.4 Company Profiles

- 6.4.1 Air Products and Chemicals Inc.

- 6.4.2 Air Liquide

- 6.4.3 BP PLC

- 6.4.4 China Petroleum & Chemical Corporation

- 6.4.5 China Three Gorges Corporation

- 6.4.6 Engie

- 6.4.7 Fortescue Future Industries

- 6.4.8 Green Hydrogen International Corp.

- 6.4.9 Iberdrola SA

- 6.4.10 Intercontinental Energy

- 6.4.11 LHYFE

- 6.4.12 Linde PLC

- 6.4.13 Ningxia Baofeng Energy Group Co. Ltd

- 6.4.14 Plug Power Inc.

- 6.4.15 Reliance Industries Limited

- 6.4.16 Tidewater Renewables Ltd

- 6.4.17 Uniper SE

- 6.4.18 Yara

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Favorable Policies and Regulations Promoting the Usage of Green Hydrogen

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Green Hydrogen Industry Segmentation

Green hydrogen is generated through an electrolysis process using renewable electricity, splitting water into hydrogen and oxygen. It does not emit polluting gases during combustion or production. Green hydrogen has applications in transportation, power generation, and refining industries.

The green hydrogen market is segmented by end-user industry and geography. By end-user industry, the market is divided into refining, chemicals, iron and steel, transportation, and power and other end-user industries. The report also covers the market size and forecasts for the green hydrogen market in 11 countries across major regions. For each segment, the market size and forecasts are based on volume (tons).

| End-user Industry | Refining | ||

| Chemicals | |||

| Iron and Steel | |||

| Transportation | |||

| Power and Other End-user Industries | |||

| Geography | Asia-Pacific | China | |

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Rest of the World | South America | ||

| Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Green Hydrogen Market Research FAQs

How big is the Green Hydrogen Market?

The Green Hydrogen Market size is expected to reach 0.45 million tons in 2025 and grow at a CAGR of 36.35% to reach 2.12 million tons by 2030.

What is the current Green Hydrogen Market size?

In 2025, the Green Hydrogen Market size is expected to reach 0.45 million tons.

Who are the key players in Green Hydrogen Market?

China Petroleum & Chemical Corporation, Ningxia Baofeng Energy Group Co. LTD, Plug Power Inc., China Three Gorges Corporation (CTG) and Tidewater Renewables Ltd are the major companies operating in the Green Hydrogen Market.

Which is the fastest growing region in Green Hydrogen Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Green Hydrogen Market?

In 2025, the Asia Pacific accounts for the largest market share in Green Hydrogen Market.

What years does this Green Hydrogen Market cover, and what was the market size in 2024?

In 2024, the Green Hydrogen Market size was estimated at 0.29 million tons. The report covers the Green Hydrogen Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Green Hydrogen Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Green Hydrogen Market Research

Mordor Intelligence provides a comprehensive analysis of the green hydrogen industry. We leverage our extensive expertise in clean hydrogen and renewable hydrogen market dynamics. Our detailed research covers the entire value chain, including hydrogen production and electrolysis hydrogen processes, as well as hydrogen infrastructure development. The report offers an in-depth analysis of electrolyzer technologies, hydrogen fuel cell applications, and hydrogen energy storage solutions. It is available in an easy-to-read report PDF format for immediate download. Our research methodology incorporates a thorough examination of hydrogen generation trends and sustainable fuel developments across global markets.

The report provides stakeholders with crucial insights into hydrogen technology advancements and clean hydrogen production methodologies. This enables informed decision-making in the rapidly evolving green hydrogen industry. Our analysis includes renewable energy hydrogen initiatives, industrial hydrogen applications, and emerging hydrogen fuel technologies. The comprehensive market forecast examines electrolyzer market dynamics, hydrogen energy developments, and sustainable hydrogen implementation strategies. The report delivers valuable insights into market growth patterns, market trends, and strategic opportunities within the hydrogen generation market. This is supported by robust data and expert analysis of the hydrogen energy industry.