Graft Versus Host Disease Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

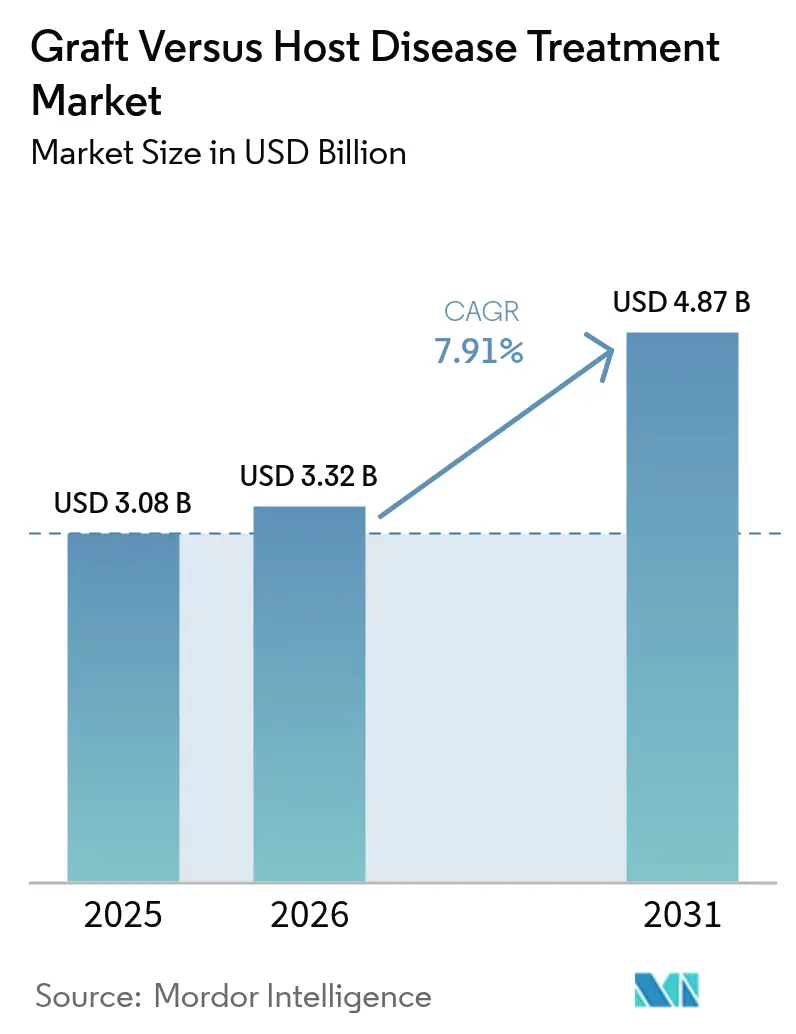

| Market Size (2026) | USD 3.32 Billion |

| Market Size (2031) | USD 4.87 Billion |

| Growth Rate (2026 - 2031) | 7.91% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Graft Versus Host Disease Treatment Market Analysis by Mordor Intelligence

GVHD treatment market size in 2026 is estimated at USD 3.32 billion, growing from 2025 value of USD 3.08 billion with 2031 projections showing USD 4.87 billion, growing at 7.91% CAGR over 2026-2031. Transplant-center volumes continue to expand as broader eligibility criteria allow older and comorbid patients to receive allogeneic HSCT, while a steady cadence of FDA approvals validates next-generation biologics and cell therapies. Post-transplant cyclophosphamide protocols have removed many donor-matching constraints, further lifting procedure numbers. Increasing use of biomarkers is guiding steroid-sparing regimens that balance efficacy with infection risk, and digital health tools are enabling closer outpatient monitoring. Although manufacturing capacity for mesenchymal stem cells (MSC) and viral vectors remains tight, industry investment in closed-system bioreactors is beginning to ease supply bottlenecks.

Key Report Takeaways

- By disease type, acute GVHD led with 61.12% GVHD treatment market share in 2025; chronic GVHD is projected to grow the fastest at an 11.17% CAGR to 2031.

- By product category, corticosteroids held 38.12% revenue share in 2025, whereas JAK inhibitors are expected to post a 12.44% CAGR through 2031.

- By therapeutic modality, small-molecule drugs captured 43.98% of the GVHD treatment market size in 2025, while cell and gene therapies are poised to expand at an 11.66% CAGR.

- By treatment line, first-line regimens accounted for 68.15% of spending in 2025; second-line therapies exhibit the highest growth at 11.34% through 2031.

- By route of administration, intravenous products dominated with 53.72% share in 2025, yet oral formulations are rising at a 10.33% CAGR.

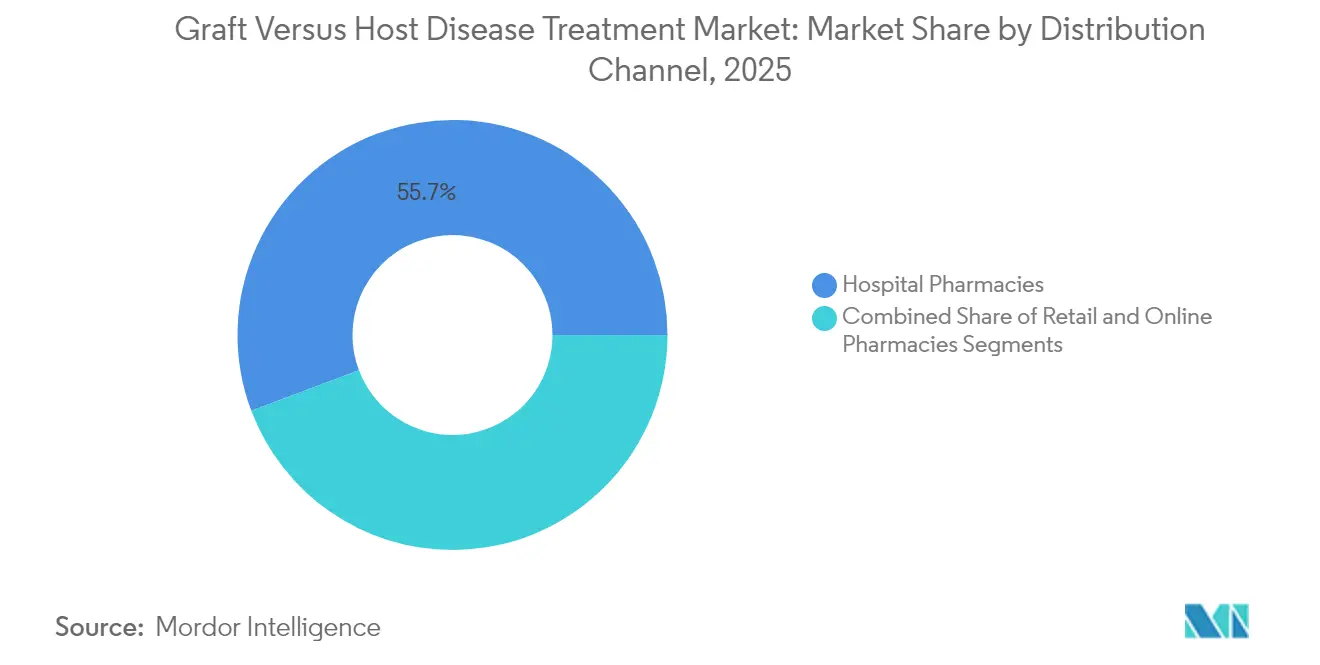

- By distribution channel, hospital pharmacies managed 55.74% of distribution in 2025; online pharmacies are on track for a 12.09% CAGR.

- By patient age group, adults represented 60.91% of demand in 2025, while the pediatric cohort is increasing at a 10.55% CAGR.

- By geography, North America commanded 41.82% of 2025 revenue; Asia-Pacific is the fastest-growing region at 10.54% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Graft Versus Host Disease Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Broader Eligibility Driving Allogeneic HSCT Volumes | 1.2% | Global, with early gains in North America & Europe | Medium term (2-4 years) |

| Wave Of FDA Approvals | 1.8% | North America core, spill-over to EU & APAC | Short term (≤ 2 years) |

| Expanding Pipeline Of Biologics & Cell Therapies | 1.5% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Growing Incidence Of Hematologic Malignancies | 1.3% | Global, with aging population impact in developed regions | Long term (≥ 4 years) |

| Microbiome-Modulation Therapeutics Opening New Niches | 0.9% | North America & EU early adoption, APAC following | Medium term (2-4 years) |

| Post-Transplant Cyclophosphamide Enabling Haplo-Identical HSCT | 1.1% | Global, with rapid adoption in resource-constrained settings | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Broader Eligibility Driving Allogeneic HSCT Volumes

CMS expanded Medicare coverage for allogeneic HSCT in myelodysplastic syndrome during March 2024, permitting transplants in older or comorbid patients and directly enlarging the pool that may experience GVHD.[1]Centers for Medicare & Medicaid Services, “NCA – Allogeneic Hematopoietic Stem Cell Transplantation for Myelodysplastic Syndromes,” cms.gov Hospitals now treat candidates once deemed ineligible, and mixed-chimerism data from non-myeloablative regimens reinforce this inclusive approach. Growing procedure counts translate into higher prophylaxis usage and recurring therapy needs, sustaining GVHD treatment market momentum.

Wave of FDA Approvals

FDA endorsements for remestemcel-L in pediatric steroid-refractory acute GVHD and axatilimab in chronic GVHD provide new therapeutic angles and premium pricing opportunities.[2]U.S. Food and Drug Administration, “FDA Approves Remestemcel-L-rknd for Steroid-Refractory Acute Graft-Versus-Host Disease in Pediatric Patients,” fda.gov Each approval encourages investment in analogous mechanisms, accelerates trial enrollment, and underscores regulatory commitment to address unmet need. Rapid commercialization of these assets heightens competition and enriches the product mix within the GVHD treatment market.

Expanding Pipeline of Biologics & Cell Therapies

Companies such as Orca Bio, Atara Biotherapeutics, and Kyverna Therapeutics are advancing CAR-T, MSC, and engineered-T-cell candidates aimed at both acute and chronic disease phases. Many candidates leverage off-the-shelf manufacturing, which promises shorter lead times and broader access. A steady influx of biologics diversifies treatment choices, supports precision medicine strategies, and lifts the GVHD treatment market over the long term.

Growing Incidence of Hematologic Malignancies

An aging global population means higher leukemia, lymphoma, and MDS incidence, all major indications for HSCT. Earlier diagnosis, coupled with reduced-intensity conditioning, increases transplant candidacy among elderly patients. Rising transplant numbers translate directly into heightened prophylactic and therapeutic demand, reinforcing the GVHD treatment market’s steady expansion.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost Of Biologics & Cell Therapies | -0.8% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Infection Risk From Profound Immunosuppression | -1.2% | Global, with higher impact in resource-limited settings | Medium term (2-4 years) |

| Supply Constraints For MSC & Viral-Vector Manufacturing | -0.7% | Global, concentrated in regions with limited manufacturing | Long term (≥ 4 years) |

| Reimbursement Gaps For Off-Label Regimens In EMS | -0.9% | Emerging markets, with spillover to developed regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Biologics & Cell Therapies

Remestemcel-L and axatilimab list prices strain payer budgets, especially where health-technology-assessment frameworks emphasize cost-effectiveness. Emerging markets face particular hurdles, delaying uptake despite clear clinical benefit. Prior authorization rules and step-therapy protocols sometimes deter clinicians from adopting next-generation agents, tempering growth potential in the near term.

Infection Risk from Profound Immunosuppression

Layered immunosuppressive regimens elevate susceptibility to viral reactivation, bacterial sepsis, and invasive fungal infections. Clinicians often dial back doses or defer combination therapy because of safety fears, potentially compromising efficacy. Hospitals in resource-constrained regions—with limited infectious-disease support—may avoid aggressive regimens altogether, constraining the GVHD treatment market’s addressable segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Disease: Chronic GVHD Growth Outpaces Acute Cases

Acute GVHD retained 61.12% of 2025 GVHD treatment market share, reflecting the still-greater clinical frequency of early post-transplant inflammation. Chronic GVHD, however, is on track for an 11.17% CAGR to 2031, the fastest among disease segments. This acceleration stems from longer post-transplant survival that enlarges the chronic-phase patient pool and from fresh options such as JAK inhibitors and monoclonal antibodies that specifically target fibrosis, B-cell activation, or ROCK2 signaling. Lower-GI prophylaxis with vedolizumab has already lifted day-180 survival to 85.5%, which decreases acute events yet leaves more patients alive to develop chronic manifestations.

Multidisciplinary clinics are now treating chronic GVHD more like systemic autoimmune disease, adding pulmonary rehab, ocular lubricants, and topical ruxolitinib to standard immunosuppression. Teduglutide’s 64.7% overall response in severe intestinal cases underlines how organ-directed biologics can lift remission rates. As a result, chronic therapies are expected to raise their portion of GVHD treatment market size each year through 2031, creating a sustained addressable base for innovators.

By Product Category: JAK Inhibitors Erode Steroid Leadership

Corticosteroids commanded 38.12% GVHD treatment market share in 2025, largely because guideline writers still endorse methylprednisolone as first-line therapy for acute episodes. Yet JAK inhibitors are expanding at a 12.44% CAGR, buoyed by ruxolitinib’s 94.1% overall effectiveness in children and by growing adult experience in steroid-refractory disease. Mini-dose methotrexate now combines with steroids to push 1-year failure-free survival to 69% versus 41% for steroids alone, highlighting incremental innovations that maintain steroid relevance.

Beyond JAK blockade, monoclonal antibodies such as axatilimab are taking share in chronic GVHD, and BTK inhibitors are being repurposed from oncology programs. Cell and gene therapies, while still holding a modest slice today, carry premium pricing and deliver durable responses that can displace prolonged drug courses. Collectively, these dynamics are expected to chip away at the steroid portion of GVHD treatment market size while broadening therapeutic diversity.

By Therapeutic Modality: Cell Therapies Scale Up

Small-molecule drugs—corticosteroids, JAK inhibitors, calcineurin-sparing agents—held 43.98% of 2025 GVHD treatment market size. Cell and gene therapies are the fastest movers at an 11.66% CAGR, lifted by FDA endorsement of remestemcel-L for pediatric acute GVHD and late-stage programs such as tabelecleucel. Biologics remain a steady middle ground, with antibodies against CSF-1R, CD38, and α4β7 integrin incrementally widening indications.

The manufacturing gap for mesenchymal stem cells and viral vectors is narrowing as closed-system bioreactors and in-house plasmid suites come online, letting sponsors meet commercial demand. Platform advances also allow allogeneic “off-the-shelf” products that avoid patient-specific lead times. Looking ahead, the modality mix will keep shifting toward cell-based solutions that promise sustained, possibly curative, control of GVHD and thereby lift cell therapy share of GVHD treatment market size.

By Treatment Line: Second-Line Therapies Expand Rapidly

First-line regimens captured 68.15% of spending in 2025, a figure rooted in universal steroid initiation across transplant centers. Second-line options, though smaller today, are forecast to climb at an 11.34% CAGR as formal approvals replace historic off-label practice. Belumosudil is evaluating earlier intervention, and axatilimab’s label for patients who have failed at least two systemic therapies offers a validated next step.

Longer transplant survival amplifies the number of steroid-refractory or dependent cases, boosting demand for second-line agents. Step-wise escalation algorithms that layer a JAK inhibitor, ROCK2 blocker, or MSC infusion onto tapering steroids are now common in academic centers. Such sequencing keeps late-line utilization contained but drives compound annual growth for the second-line slice of GVHD treatment market share through 2031.

By Route of Administration: Oral Delivery Picks Up Speed

Intravenous formulations held 53.72% share in 2025, reflecting hospital-based exigencies for biologics, MSC infusions, and high-dose steroids. Oral agents, however, are expanding at a 10.33% CAGR as ruxolitinib, belumosudil, and new BTK inhibitors gain traction in outpatient settings. Subcutaneous options are also emerging, offering flexibility for clinics that lack infusion bays.

Medicare’s separate payment for home IVIG exemplifies a shift toward community-based care. As payers push site-of-care optimization and patients favor convenience, sponsors are reformulating IV drugs into tablets or softgels. These trends suggest oral and subcutaneous forms will erode some hospital-centric share while growing total GVHD treatment market size by improving adherence.

By Distribution Channel: Online Channels Capture Momentum

Hospital pharmacies controlled 55.74% of distribution in 2025 given the inpatient nature of acute GVHD management. Online pharmacies are rising at a 12.09% CAGR as chronic GVHD patients refill oral JAK inhibitors or topical agents remotely. Retail outlets handle stable long-term prescriptions, whereas specialty clinics coordinate complex infusion schedules and lab monitoring.

Supply-chain vulnerabilities—including recent IV fluid shortages—have encouraged decentralization of dispensing. Digital platforms linked to transplant centers now deliver compliance reminders, dose titration alerts, and cold-chain monitoring, making e-commerce increasingly feasible. The result is a gradual share shift toward online vendors, yet hospital pharmacies will keep controlling acute therapy in the GVHD treatment market.

By Patient Age Group: Pediatric Cohort Rises

Adults made up 60.91% of 2025 demand, mirroring the higher incidence of hematologic malignancies among middle-aged and older populations. Pediatric cases are slated for a 10.55% CAGR as broader indications and remestemcel-L’s dedicated label invite earlier, more aggressive transplant strategies. Meanwhile, reduced-intensity conditioning has prompted some centers to transplant infants previously deemed too frail, further lifting pediatric numbers.

Clinicians note that children tolerate MSC infusions and JAK inhibitors better than older adults, allowing fuller dosing and faster tapering of steroids. Long life expectancy also justifies adoption of premium therapies that may limit chronic complications. Together, these drivers will raise the pediatric portion of GVHD treatment market share throughout the forecast, although adult patients will continue to dominate headline revenue.

Geography Analysis

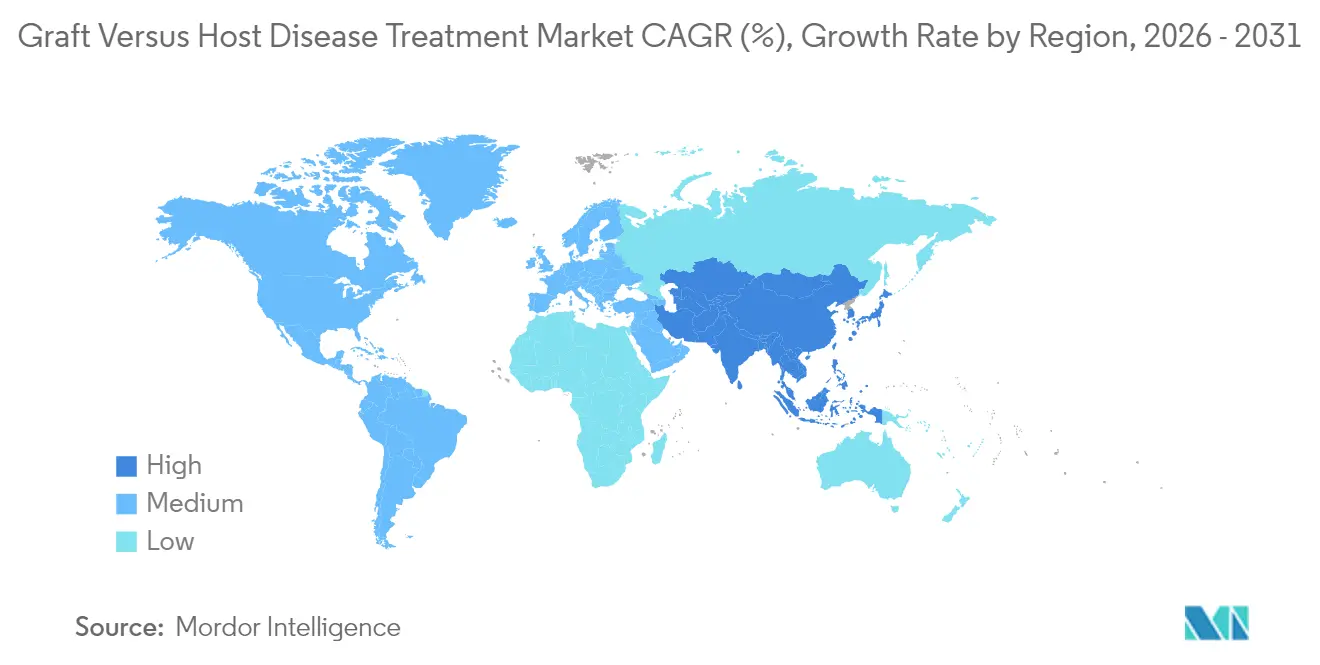

North America captured 41.82% of 2025 revenue, buoyed by an FDA environment that expedites novel approvals and by insurer willingness to reimburse high-cost agents. Medicare’s 2024 decision to fund broader transplant indications further enlarges domestic patient pools. Transplant centers in the United States integrate telehealth follow-up and home-infusion services, limiting inpatient stays and supporting outpatient adoption of oral agents.

Asia-Pacific is projecting a 10.54% CAGR, the fastest worldwide, as China and Japan expand transplant capacity and approve new anti-viral and GVHD therapies. Public-private investment in cell-processing facilities reduces reliance on imported vectors, improving supply security. Rising incidence of hematologic malignancies, coupled with broader insurance schemes, positions the region as a prime contributor to global GVHD treatment market growth.

Europe remains stable and well-penetrated, but tight budget controls moderate uptake of premium therapies. Collaborative trial networks hasten evidence generation, yet payer scrutiny delays reimbursement for frontier products. South America, the Middle East, and Africa remain nascent; technology-transfer deals and donor-registry collaborations are necessary to unlock their long-term GVHD treatment market potential.

Competitive Landscape

The competitive field is moderately fragmented. Incyte’s axatilimab added to its GVHD portfolio while Mesoblast secured first-in-class MSC approval, validating cell-therapy economics. Large pharma focuses on combo strategies that pair antibodies with kinase inhibitors, whereas specialist firms refine microbiome modulators and off-the-shelf cell products. Artificial-intelligence-guided patient stratification, advanced bioreactors, and value-based agreements are becoming key differentiators.

Biogen’s move for Human Immunology Biosciences illustrates interest in leveraging immune-modulating antibodies beyond oncology. Meanwhile, Orca Bio’s precision-engineered graft demonstrates 82% one-year GVHD relapse-free survival without post-transplant cyclophosphamide, showing that platform innovation can rival drug-based prophylaxis. Partnerships for viral-vector manufacturing and digital patient-support services are proliferating, as firms aim to secure supply and enhance adherence within the GVHD treatment market.

Graft Versus Host Disease Treatment Industry Leaders

Abbvie Inc.

Sanofi

Bristol Myers Squibb Company

Pfizer Inc.

Incyte Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: MaaT Pharma submits a marketing authorization application to the EMA for Xervyteg (MaaT013) in acute GVHD

- February 2025: Sanofi launches Rezurock for chronic GVHD in India.

- January 2025: Incyte and Syndax receive FDA approval for Niktimvo (axatilimab-csfr); U.S. launch scheduled for early February.

Global Graft Versus Host Disease Treatment Market Report Scope

As per the scope of this report, Graft Versus Host Disease is a complication of the hematopoietic stem cell transplant where the donor's graft stem cells or the bone marrow attack the recipient's body. The Graft Versus Host Disease Treatment Market is Segmented by Disease (Acute Graft Versus Host Disease and Chronic Graft Versus Host Disease), Product (Corticosteroids, Monoclonal Antibodies, Tyrosine Kinase Inhibitors, and Other Products), End User (Hospital Pharmacies, Online Pharmacies, and Retail Pharmacies), and Geography (North America, Europe, Asia-Pacific, and the Rest of the World). The report offers the value (in USD million) for the above segments.

| Acute GVHD |

| Chronic GVHD |

| Corticosteroids |

| Monoclonal Antibodies |

| JAK Inhibitors |

| BTK Inhibitors |

| Tyrosine Kinase Inhibitors (non-JAK/BTK) |

| mTOR Inhibitors |

| Cell & Gene Therapies |

| Other Products |

| Small-Molecule Drugs |

| Biologics |

| Cell & Gene Therapies |

| First-Line (Steroid Sensitive) |

| Second-Line (Steroid-Refractory) |

| Late-Line / Salvage |

| Oral |

| Intravenous |

| Sub-cutaneous |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| Paediatric |

| Adult |

| Geriatric |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Disease | Acute GVHD | |

| Chronic GVHD | ||

| By Product Category | Corticosteroids | |

| Monoclonal Antibodies | ||

| JAK Inhibitors | ||

| BTK Inhibitors | ||

| Tyrosine Kinase Inhibitors (non-JAK/BTK) | ||

| mTOR Inhibitors | ||

| Cell & Gene Therapies | ||

| Other Products | ||

| By Therapeutic Modality | Small-Molecule Drugs | |

| Biologics | ||

| Cell & Gene Therapies | ||

| By Treatment Line | First-Line (Steroid Sensitive) | |

| Second-Line (Steroid-Refractory) | ||

| Late-Line / Salvage | ||

| By Route of Administration | Oral | |

| Intravenous | ||

| Sub-cutaneous | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

| By Patient Age Group | Paediatric | |

| Adult | ||

| Geriatric | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the GVHD treatment market?

The GVHD treatment market reached USD 3.32 billion in 2026 and is projected to hit USD 4.87 billion by 2031.

Which segment will grow the fastest through 2031?

Chronic GVHD therapies are expected to post the highest CAGR at 11.17%, outpacing acute-phase treatments.

How are JAK inhibitors reshaping standard care?

JAK inhibitors, led by ruxolitinib, deliver high response rates in steroid-refractory patients and are forecast to grow at a 12.44% CAGR, challenging corticosteroid dominance.

Why is Asia-Pacific the fastest-growing region?

Rapid expansion of transplant centers in China and Japan, coupled with improving reimbursement, drives a projected 10.54% regional CAGR.

What are the main barriers to wider cell-therapy adoption?

High manufacturing costs, limited viral-vector capacity, and payer budget constraints continue to slow large-scale uptake despite strong clinical demand.

Page last updated on: