Market Size of Vendor-Neutral Archive (VNA) And PACS Industry

| Study Period | 2019 - 2029 |

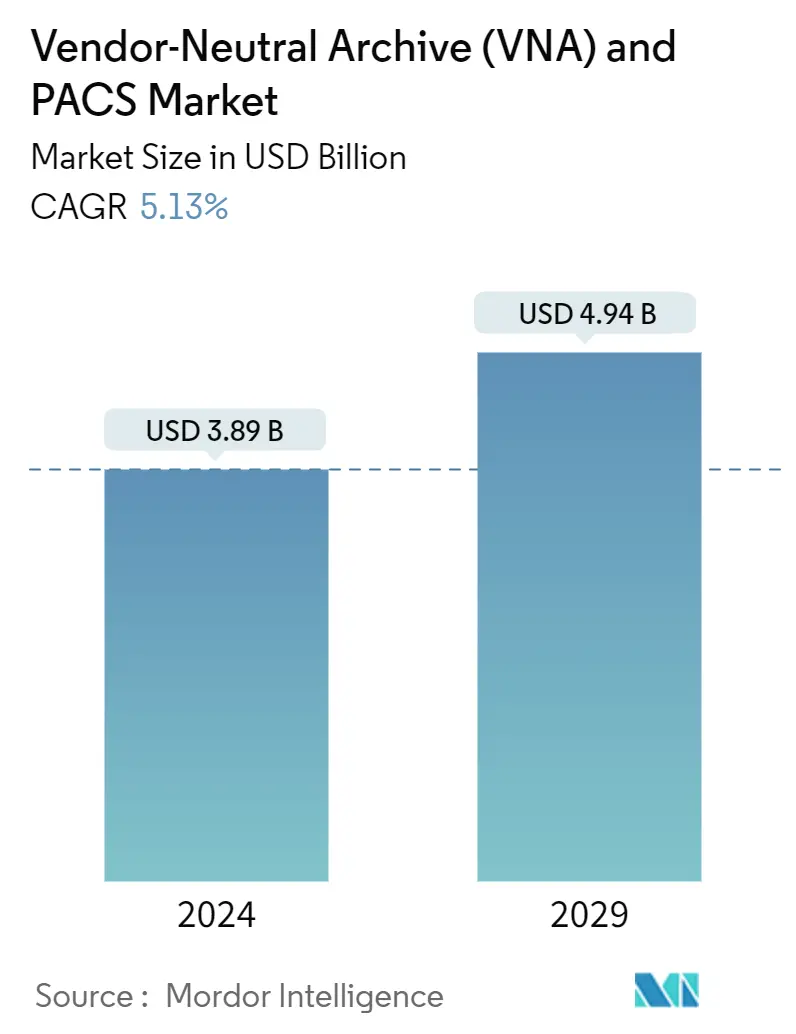

| Market Size (2024) | USD 3.89 Billion |

| Market Size (2029) | USD 4.94 Billion |

| CAGR (2024 - 2029) | 5.13 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players_and_PACS_Market_player.webp)

*Disclaimer: Major Players sorted in no particular order |

VNA & PACS Market Analysis

The Vendor-Neutral Archive And PACS Market size is estimated at USD 3.89 billion in 2024, and is expected to reach USD 4.94 billion by 2029, growing at a CAGR of 5.13% during the forecast period (2024-2029).

The COVID-19 pandemic showed a significant impact on the studied market. The increase in COVID-19 patients and the surge in diagnostics requirements in diagnostic centers, clinics, hospitals, and mobile clinics increased during the pandemic. It fuelled the demand for integrating VNAs into hospital systems for easy diagnosis and access to patient records. According to an article published in the Journal of Digital Imaging in April 2021, the study was conducted to evaluate the disaster planning process during the COVID-19 pandemic phase, and it showed that researchers enabled their picture archiving and communication system (PACS) workstation for home use and evaluate system performance. After that, various guidelines were made, and several research centers allowed wireless adapters for the PACS workstations for use at home. It positively impacted the growth of the market studied. Thus, COVID-19 showed a considerable impact on the market studied. This is further anticipated to continue its growth trend during the analysis period.

Factors such as increasing demand for the universalization of medical image archiving, reducing data storage costs, and high-level integration with the Electronic Health Records (EHR) industry are some of the major factors expected to drive the market studied. In addition, the universal demand for digitization of healthcare systems has increased the demand for medical archiving. The research article published in the Diagnostics Journal in July 2021 stated that large amounts of imaging data are generated in daily clinical practice constantly, leading to continuously expanding archives, and new progressive efforts are being made worldwide to build large-scale medical imaging repositories. Thus, the research and studies show demand for medical imaging archives, which may drive the growth of the overall market studied.

Additionally, studies have been conducted recently to clarify the pros and cons of PACS and VNAs and suggest that organizations can use PACS successfully, but to save money in the long run and quickly associated with data storage and effectively use medical images, VNAs should be considered as a promising option for reducing long-term costs and allowing greater interoperability around critical imaging data. Moreover, the compatibility of VNA with older data archival systems is another major driving factor for the studied market.

For instance, an article published by RamSoft Inc. in March 2022 stated that VNAs could assist healthcare providers in optimizing their medical imaging operations and increase business growth with specific advantages, enhanced interoperability, and data exchange. Also, the article highlighted that some commercially available powerful VNAs offer the prominent advantage of acting as a single integration point for data stored by diverting the burden of integration from every separate clinical system connected to the organization's network. Thus, the market studied is expected to grow due to the abovementioned factors.

Moreover, the engagement of major companies worldwide in advancing enterprise imaging is another driving factor for the market studied. For instance, in November 2021, GE Healthcare developed a next-generation, cloud-based picture archiving and communication system (PACS) to help healthcare organizations keep current with rapidly evolving technology. The subscription-based diagnostic imaging solution called Edison True PACS encompasses diagnostic reading, exam workflow, AI Applications, 3D post-processing, enterprise visualization, and archiving in a single platform. Thus, the studied market growth is attributed to the abovementioned factors, and the market is expected to grow significantly over the forecast period. However, the availability of long-term data affecting the decisions of service providers and the long product life cycle are some factors that are predicted to hinder market growth.

VNA & PACS Industry Segmentation

As per the scope of this report, VNA is a technology in which images and documents are stored in a standard format. PACS is a technology that provides economical storage and convenient access to images from multiple modalities. The Vendor-Neutral Archive (VNA) and PACS Market are Segmented by Imaging Modality (Angiography, Mammography, Computed Tomography, Magnetic Resonance Imaging, Ultrasound, and Other Imaging Modalities), Type (PACS and VNA Software), Mode of Delivery (On-Site (Premise), Hybrid and Cloud-hosted), Usage Model (Single Department, Multiple Departments, and Multiple Sites), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD) for the above segments.

| By Imaging Modality | |

| Angiography | |

| Mammography | |

| Computed Tomography | |

| Magnetic Resonance Imaging | |

| Ultrasound | |

| Other Imaging Modalities |

| By Type | |

| PACS | |

| VNA Software |

| By Mode of Delivery | |

| On-Site (Premise) | |

| Hybrid | |

| Cloud-hosted |

| By Usage Model | |

| Single Department | |

| Multiple Departments | |

| Multiple Sites |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Vendor-Neutral Archive (VNA) And PACS Market Size Summary

The Vendor-Neutral Archive (VNA) and PACS market is poised for significant growth, driven by the increasing demand for universal medical image archiving and the need for cost-effective data storage solutions. The COVID-19 pandemic has accelerated the adoption of these technologies, as healthcare facilities sought to integrate VNAs into their systems for improved diagnostic capabilities and easier access to patient records. The push for digitization in healthcare systems has further fueled the demand for medical archiving solutions, with ongoing efforts to build large-scale medical imaging repositories. The compatibility of VNAs with older data archival systems and their ability to reduce long-term costs while enhancing interoperability are key factors propelling market expansion. Major companies are actively engaging in advancing enterprise imaging, with new product launches and innovations contributing to the market's growth trajectory.

In North America, the VNA and PACS market is expected to experience robust growth due to well-developed healthcare IT infrastructure, the presence of major industry players, and strategic initiatives in countries like the United States, Canada, and Mexico. The region's market growth is supported by the introduction of new products and partnerships among market players, which are enhancing digital diagnostics and improving patient care workflows. The on-premises mode of delivery remains popular due to its security and integration capabilities, further driving segment growth. Despite challenges such as long product life cycles and the need for long-term data availability, the market is anticipated to grow significantly, with major players like Agfa Healthcare, GE Healthcare, and Siemens Healthineers holding substantial market shares and continuously innovating to meet evolving healthcare demands.

Vendor-Neutral Archive (VNA) And PACS Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Increasing Demand for the Universalization of Medical Image Archiving

-

1.2.2 Reducing Data Storage Costs

-

1.2.3 High-level Integration with Electronic Health Records (EHR) Industry

-

1.2.4 Compatibility of VNA with Older Data Archival Systems

-

-

1.3 Market Restraints

-

1.3.1 Availability of Long-Term Data Affecting the Decisions of Service Providers

-

1.3.2 Long Product Life Cycle Affecting New Sales

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Bargaining Power of Buyers/Consumers

-

1.4.2 Bargaining Power of Suppliers

-

1.4.3 Threat of New Entrants

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD)

-

2.1 By Imaging Modality

-

2.1.1 Angiography

-

2.1.2 Mammography

-

2.1.3 Computed Tomography

-

2.1.4 Magnetic Resonance Imaging

-

2.1.5 Ultrasound

-

2.1.6 Other Imaging Modalities

-

-

2.2 By Type

-

2.2.1 PACS

-

2.2.2 VNA Software

-

-

2.3 By Mode of Delivery

-

2.3.1 On-Site (Premise)

-

2.3.2 Hybrid

-

2.3.3 Cloud-hosted

-

-

2.4 By Usage Model

-

2.4.1 Single Department

-

2.4.2 Multiple Departments

-

2.4.3 Multiple Sites

-

-

2.5 Geography

-

2.5.1 North America

-

2.5.1.1 United States

-

2.5.1.2 Canada

-

2.5.1.3 Mexico

-

-

2.5.2 Europe

-

2.5.2.1 Germany

-

2.5.2.2 United Kingdom

-

2.5.2.3 France

-

2.5.2.4 Italy

-

2.5.2.5 Spain

-

2.5.2.6 Rest of Europe

-

-

2.5.3 Asia-Pacific

-

2.5.3.1 China

-

2.5.3.2 Japan

-

2.5.3.3 India

-

2.5.3.4 Australia

-

2.5.3.5 South Korea

-

2.5.3.6 Rest of Asia-Pacific

-

-

2.5.4 Middle East and Africa

-

2.5.4.1 GCC

-

2.5.4.2 South Africa

-

2.5.4.3 Rest of Middle East and Africa

-

-

2.5.5 South America

-

2.5.5.1 Brazil

-

2.5.5.2 Argentina

-

2.5.5.3 Rest of South America

-

-

-

Vendor-Neutral Archive (VNA) And PACS Market Size FAQs

How big is the Vendor-Neutral Archive And PACS Market?

The Vendor-Neutral Archive And PACS Market size is expected to reach USD 3.89 billion in 2024 and grow at a CAGR of 5.13% to reach USD 4.94 billion by 2029.

What is the current Vendor-Neutral Archive And PACS Market size?

In 2024, the Vendor-Neutral Archive And PACS Market size is expected to reach USD 3.89 billion.