| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 6.45 Billion |

| Market Size (2030) | USD 8.90 Billion |

| CAGR (2025 - 2030) | 6.64 % |

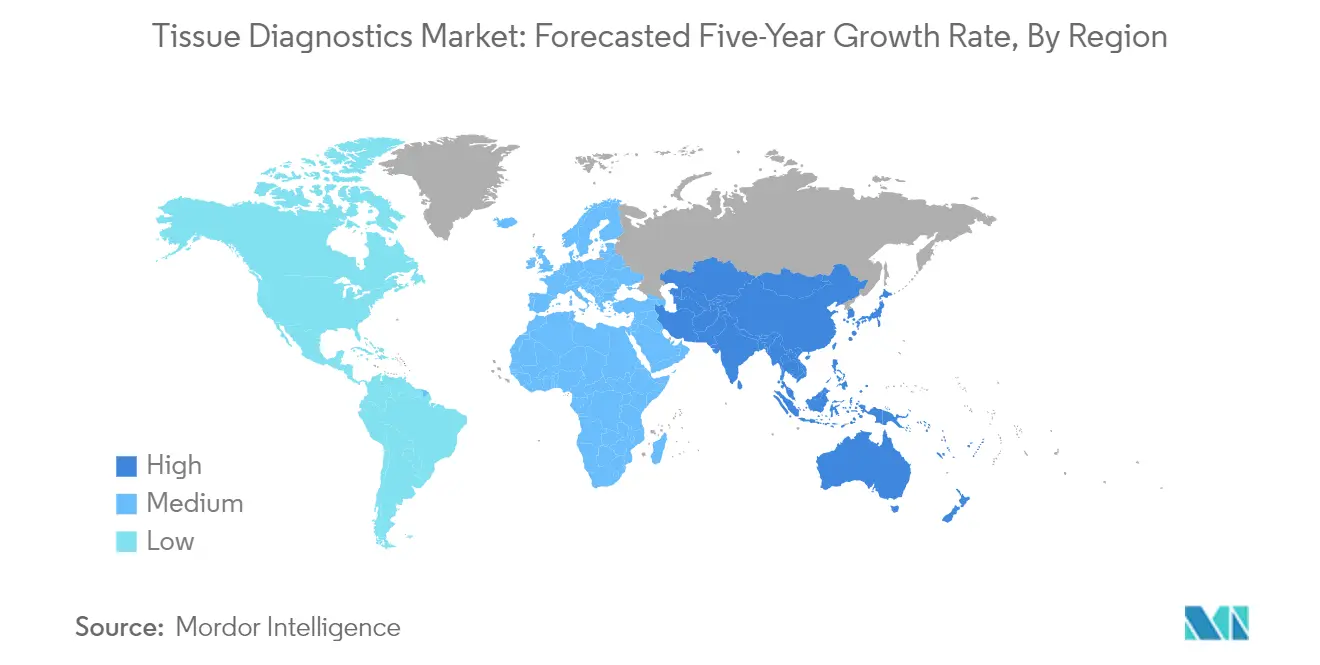

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

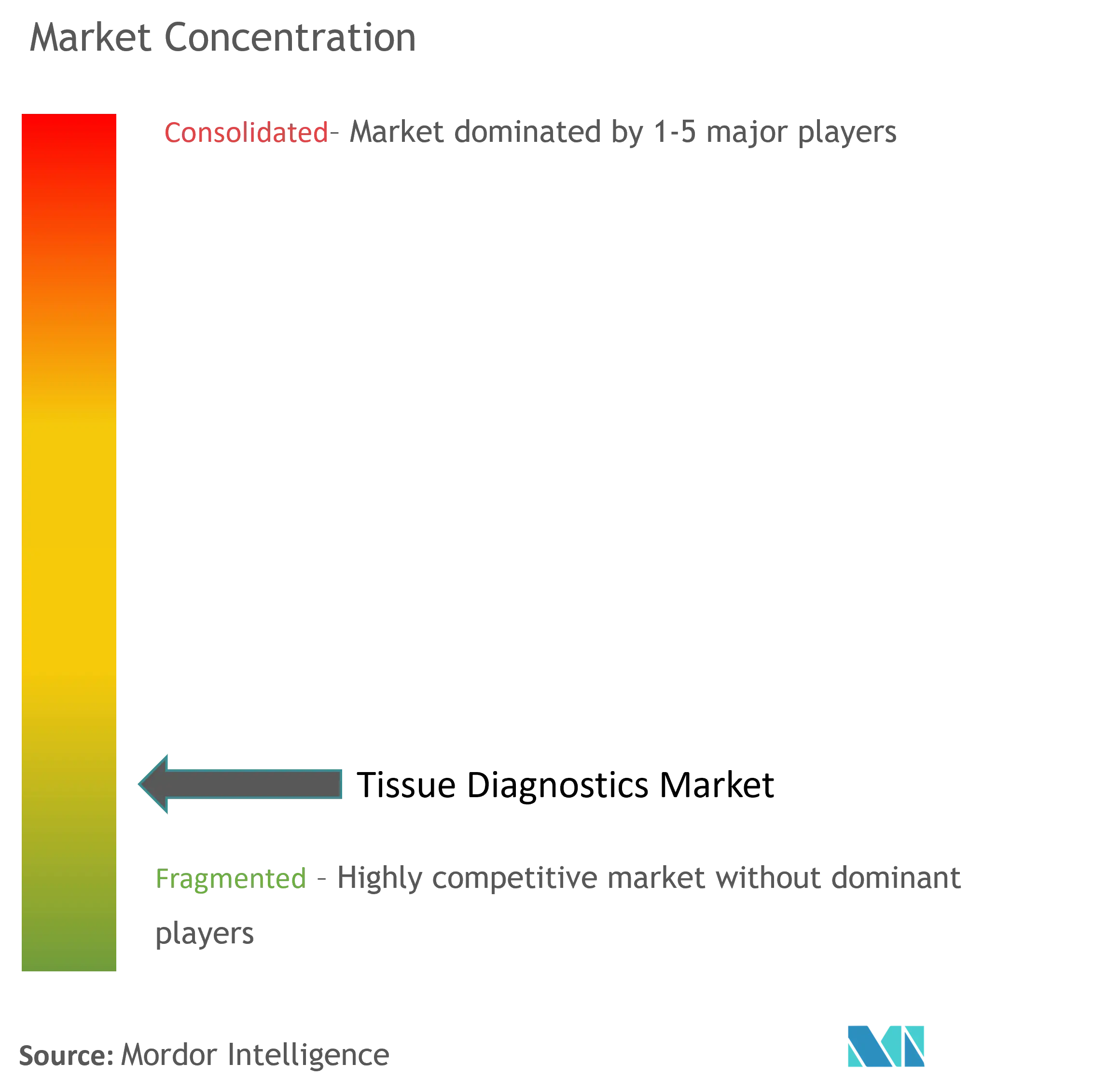

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Tissue Diagnostics Market Analysis

The Tissue Diagnostics Market size is estimated at USD 6.45 billion in 2025, and is expected to reach USD 8.90 billion by 2030, at a CAGR of 6.64% during the forecast period (2025-2030).

The tissue diagnostics market is experiencing significant transformation driven by increasing demand for early disease detection and precision medicine approaches. This evolution is particularly evident in oncology applications, where tissue testing serves as a crucial tool for accurate cancer diagnosis and treatment planning. The market's expansion is further supported by demographic shifts, with an aging global population requiring more sophisticated diagnostic solutions. According to recent estimates from the American Cancer Society, new cancer cases in the United States are projected to increase from 1.9 million in 2023 to 2.0 million in 2024, highlighting the growing need for advanced diagnostic capabilities.

Strategic partnerships and consolidation activities are reshaping the competitive landscape of the tissue diagnostics market. Companies are increasingly focusing on collaborative approaches to enhance their technological capabilities and market presence. A notable example is the July 2023 partnership between Quest Diagnostics and Envision Sciences, which led to the launch of a novel prostate cancer biomarker test through AmeriPath. Similarly, CŌRE Diagnostics' strategic alliance with PredOmix Technologies in July 2023 resulted in the introduction of OncoVeryx-F, a revolutionary multi-cancer detection test specifically designed for women's cancer risk assessment.

The industry is witnessing a significant shift toward personalized healthcare solutions, with tissue diagnostics playing a crucial role in enabling tailored treatment approaches. This trend is particularly evident in Brazil, where healthcare authorities anticipate approximately 704,000 new cancer cases between 2023 and 2025, driving the demand for more precise diagnostic tools. The integration of advanced technologies, including artificial intelligence and digital pathology, is revolutionizing traditional diagnostic methods, enabling more accurate and efficient tissue analysis of samples.

Market dynamics are being influenced by the increasing focus on comprehensive diagnostic solutions that can simultaneously assess multiple parameters. Healthcare providers are demanding more sophisticated tools that can provide detailed molecular and genetic information from tissue samples, enabling better treatment decisions. The industry is responding to these needs through continuous innovation in diagnostic technologies, although challenges remain in terms of standardization and accessibility. The trend toward integrated diagnostic platforms is expected to continue, with an emphasis on solutions that can provide both accuracy and efficiency in tissue analysis.

Tissue Diagnostics Market Trends

Rising Burden of Cancer

The escalating prevalence of cancer worldwide has emerged as a critical driver for the tissue diagnostics market, with various cancer types showing concerning growth trends. For instance, according to the American Cancer Society's 2024 statistics, breast cancer cases in the United States have increased significantly from 300,590 in 2023 to 313,510 in 2024, highlighting the growing need for accurate diagnostic solutions. The rising cancer burden is particularly evident in various forms, including leukemia, which saw an increase from 59,610 cases in 2023 to 62,770 cases in 2024 in the United States, emphasizing the critical need for advanced molecular diagnostics capabilities across multiple cancer types.

The burden of cancer is also rising significantly in other regions, creating a substantial demand for tissue diagnostics solutions. For example, according to the Global Cancer Observatory's 2023 data, Argentina reported 21,631 new breast cancer cases in 2022, with projections indicating further increases in the coming years. This growing cancer burden has led to increased emphasis on early detection and accurate diagnosis, driving healthcare providers and institutions to invest in advanced tissue biomarker technologies and solutions. The rising prevalence of cancer has also prompted healthcare organizations to focus on improving diagnostic accuracy and efficiency, particularly in identifying specific biomarkers and genetic mutations that can inform treatment decisions.

Understand The Key Trends Shaping This Market

Download PDF

Growing Healthcare Expenditure

The substantial increase in healthcare spending across developed and developing nations has become a significant driver for the tissue diagnostics market, enabling greater investment in advanced diagnostic technologies and infrastructure. According to the National Health Spending 2023 Edition by the California Healthcare Foundation, the national healthcare spending in the United States totaled USD 4.3 trillion, or USD 12,914 per person, with the federal government investing the largest share, accounting for one in three dollars. This significant healthcare expenditure has enabled healthcare institutions to invest in sophisticated in vitro diagnostics equipment and technologies, improving their diagnostic capabilities.

In other regions, healthcare spending continues to show positive growth trends, supporting the expansion of diagnostic capabilities. For instance, the Australian Government allocated AUD 105.8 billion for health in 2022-23, representing 16.8% of the total government expenditure, including USD 893.5 million specifically for services aimed at improving health outcomes and survival rates from various cancers. Similarly, developing countries like India have shown commitment to healthcare investment, with the Ministry of Health and Family Welfare allocating INR 89,155 crore in the 2023-2024 Union Budget, marking a 13% increase over the previous year's revised estimates. This growing healthcare expenditure has enabled healthcare providers to adopt advanced tissue diagnostics solutions and improve their diagnostic infrastructure.

Technological Advancements in Tissue Diagnostics

The continuous evolution of tissue diagnostics technologies has significantly enhanced the capability to detect and characterize various types of cancers, driving market growth through improved accuracy and efficiency. Recent technological breakthroughs include the integration of artificial intelligence and digital pathology solutions, as exemplified by the September 2023 launch of Ibex Medical Analytics' Galen Breast HER2, an AI-powered solution that helps pathologists achieve higher standards of accuracy in HER2 scoring for breast cancer patients. These advancements have revolutionized traditional diagnostic approaches by enabling more precise and reproducible results while reducing the time required for diagnosis.

The industry has also witnessed significant progress through strategic collaborations and innovative product developments aimed at enhancing diagnostic capabilities. For instance, in December 2023, AstraZeneca Pharma India Ltd's partnership with Roche Diagnostics India to improve the breast cancer diagnostic landscape demonstrates the industry's commitment to technological advancement. This collaboration focuses on streamlining HER2 diagnostics for early-stage breast cancer detection, representing a significant step forward in diagnostic technology. Additionally, the integration of digital pathology solutions and automated workflows has improved the efficiency of pathology laboratory processes, enabling healthcare providers to handle increasing patient volumes while maintaining high diagnostic standards.

Segment Analysis: By Product

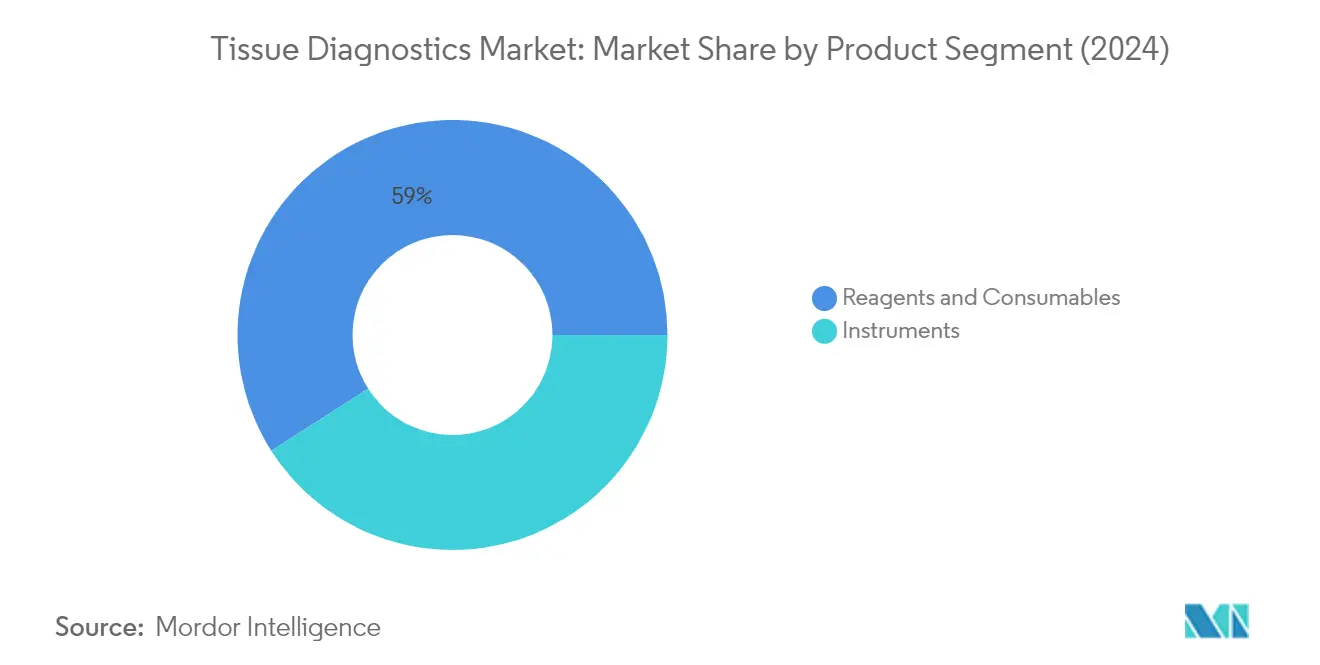

Reagents and Consumables Segment in Tissue Diagnostics Market

The reagents and consumables segment continues to dominate the tissue diagnostics market, holding approximately 59% of the market share in 2024. This segment's leadership position is primarily driven by the increasing adoption of tissue staining and tissue processing procedures in cancer detection and diagnosis worldwide. The segment encompasses a wide range of products, including fixatives, embedding mediums, various stains, antibodies and probes, enzymes and proteases, media, buffer solutions, and disposable lab wear. The high consumption rate and recurring nature of these products contribute significantly to their market dominance. Major market players like Roche, Abbott, and Thermo Fisher Scientific have been expanding their reagents and consumables portfolio through new product launches and innovations, particularly in immunohistochemistry and in-situ hybridization applications. The segment is also benefiting from the growing trend toward automated tissue diagnostic systems, which require specialized reagents and consumables for optimal performance. Additionally, the increasing focus on personalized medicine and tissue biomarker testing has created a sustained demand for high-quality reagents and consumables in tissue diagnostics laboratories.

Instruments Segment in Tissue Diagnostics Market

The instruments segment plays a crucial role in the tissue diagnostics market, encompassing automated staining systems, microscopes, digital imaging systems, flow cytometers, and tissue processors. This segment is experiencing significant technological advancements, particularly in the areas of digital pathology and automated tissue processing systems. The integration of artificial intelligence and machine learning capabilities in tissue diagnostic instruments is revolutionizing the way pathologists analyze and interpret tissue samples. Major manufacturers are focusing on developing more sophisticated and efficient instruments that can handle higher throughput while maintaining accuracy and precision. The demand for these instruments is being driven by the increasing need for standardization in tissue diagnostic procedures, reduction in manual errors, and improved workflow efficiency in pathology laboratories. Furthermore, the growing adoption of digital pathology solutions and the trend toward laboratory automation are creating new opportunities for instrument manufacturers to innovate and expand their product offerings.

Segment Analysis: By Technology

Immunohistochemistry Segment in Tissue Diagnostics Market

Immunohistochemistry (IHC) continues to dominate the tissue diagnostics market, commanding approximately 36% of the total market share in 2024. This significant market position is attributed to its widespread adoption in cancer detection and diagnosis, particularly in identifying specific proteins and biomarkers in tissue samples. The technology's ability to provide accurate visualization of antigens in tissue sections, coupled with its established reliability in clinical settings, has made it an indispensable tool in pathology laboratories worldwide. The segment's prominence is further reinforced by ongoing technological advancements in automated staining platforms and the development of novel antibodies for more precise diagnostic capabilities.

Digital Pathology & Workflow Management Segment in Tissue Diagnostics Market

Digital Pathology & Workflow Management is emerging as the most dynamic segment in the tissue diagnostics market, projected to grow at approximately 8% during 2024-2029. This remarkable growth is driven by the increasing adoption of digital solutions in pathology laboratories, enhanced by artificial intelligence and machine learning capabilities. The segment is witnessing substantial innovation through the integration of advanced imaging technologies, automated analysis tools, and cloud-based platforms that streamline diagnostic workflows. The shift towards digital pathology solutions is particularly accelerated by their ability to facilitate remote consultations, improve diagnostic accuracy, and enhance laboratory efficiency through automated image analysis and data management.

Remaining Segments in Technology Market Segmentation

The tissue diagnostics market's technology landscape is further shaped by In Situ Hybridization (ISH) and other specialized technologies. ISH technology maintains its crucial role in molecular diagnostics, particularly in detecting specific DNA or RNA sequences in tissue samples, making it invaluable for both research and clinical applications. Other technologies in the market include next-generation sequencing (NGS) and mass spectrometry, which contribute to the expanding capabilities of tissue-based diagnostics. These segments continue to evolve with new innovations in probe design, detection methods, and automation capabilities, providing pathologists with a comprehensive toolkit for accurate disease diagnosis and research applications.

Segment Analysis: By Application

Breast Cancer Segment in Tissue Diagnostics Market

The breast cancer segment has emerged as the dominant force in the tissue diagnostics market, commanding approximately 29% of the total market share in 2024. This substantial market position is primarily driven by the increasing global burden of breast cancer and the critical role of tissue diagnostics in early detection and treatment planning. The segment's leadership is further strengthened by the extensive adoption of advanced diagnostic technologies like immunohistochemistry and in-situ hybridization specifically designed for breast cancer detection. According to recent statistics from the American Cancer Society, breast cancer remains one of the most diagnosed cancers among women, necessitating robust diagnostic capabilities. The segment's growth is also supported by ongoing technological advancements, such as the launch of Ibex Medical Analytics' Galen Breast HER2 in 2023, which has enhanced the accuracy and efficiency of breast cancer diagnostics through AI-powered solutions.

Prostate Cancer Segment in Tissue Diagnostics Market

The prostate cancer segment demonstrates significant growth potential in the tissue diagnostics market, driven by increasing awareness and technological innovations in diagnostic procedures. The segment's expansion is supported by breakthrough developments such as Quest Diagnostics' launch of a novel prostate cancer biomarker test in 2023, which has revolutionized the approach to identifying and differentiating potentially aggressive cases of prostate cancer in biopsy samples. The introduction of advanced AI-powered diagnostic tools, exemplified by Oritive's QAi Prostate launch in 2023, has further enhanced the segment's growth trajectory by improving the accuracy and efficiency of prostate cancer diagnosis. The segment's development is also bolstered by increasing research activities and strategic collaborations between diagnostic companies and healthcare institutions, focusing on developing more precise and reliable tissue diagnostic solutions for prostate cancer detection.

Remaining Segments in Application Market

The gastric cancer segment represents a significant portion of the tissue diagnostics market, particularly in regions with high prevalence rates such as Asia-Pacific. This segment's importance is underscored by the continuous development of specialized diagnostic tools and techniques specifically designed for gastric cancer detection. The advancement in tissue imaging solutions, particularly in gastric cancer diagnosis, has led to improved accuracy and efficiency in tissue analysis. The segment has benefited from recent technological innovations, including the development of automated tissue diagnostic systems and AI-powered analysis tools. These developments, combined with increasing awareness about early cancer detection and growing healthcare infrastructure in developing regions, continue to drive the segment's significance in the overall tissue diagnostics market landscape.

Tissue Diagnostics Market Geography Segment Analysis

Tissue Diagnostics Market in North America

North America represents a dominant force in the global tissue diagnostics market, driven by advanced healthcare infrastructure, high healthcare expenditure, and a strong presence of key market players. The region encompasses the United States, Canada, and Mexico, with each country contributing uniquely to the market landscape. The presence of sophisticated diagnostic facilities, increased adoption of digital pathology solutions, and a growing focus on early cancer detection have positioned North America at the forefront of tissue diagnostic innovations. The region's market is further strengthened by robust reimbursement policies, extensive research activities, and increasing collaborations between diagnostic companies and healthcare providers.

Tissue Diagnostics Market in the United States

The United States leads the North American tissue diagnostics market with approximately 85% market share in 2024. The country's dominance is attributed to its extensive network of pathology laboratories, high cancer screening rates, and substantial healthcare spending. The presence of major market players, coupled with continuous technological advancements in tissue testing techniques, has created a robust market environment. The US market is characterized by strong adoption of automated tissue diagnostic systems, increasing focus on personalized medicine, and growing demand for advanced cancer diagnostic solutions. The country's well-established healthcare infrastructure and favorable reimbursement policies continue to drive market growth, while increasing research activities and clinical trials further strengthen its position.

Tissue Diagnostics Market Growth Trajectory in the United States

The United States is projected to maintain its position as the fastest-growing market in North America, with an expected CAGR of approximately 7% during 2024-2029. This growth is fueled by increasing cancer prevalence, rising adoption of digital pathology solutions, and growing demand for precision medicine. The country's commitment to healthcare innovation, substantial investments in research and development, and increasing focus on early disease detection contribute to this growth trajectory. The expansion of diagnostic facilities, integration of artificial intelligence in tissue diagnostics, and growing emphasis on companion diagnostics are expected to further accelerate market growth. Additionally, the rising geriatric population and increasing healthcare awareness continue to drive demand for advanced tissue diagnostic solutions.

Tissue Diagnostics Market in Europe

Europe represents a significant market for tissue diagnostics, characterized by sophisticated healthcare systems, strong research infrastructure, and increasing adoption of advanced diagnostic technologies. The region encompasses key markets including Germany, the United Kingdom, France, Italy, and Spain, each contributing significantly to the overall market landscape. The European market benefits from well-established healthcare policies, increasing cancer screening programs, and growing investments in diagnostic infrastructure. The region's focus on precision medicine and personalized healthcare approaches has driven the adoption of advanced tissue diagnostic solutions.

Tissue Diagnostics Market in Germany

Germany maintains its position as the largest tissue diagnostics market in Europe, holding approximately 23% market share in 2024. The country's market leadership is supported by its advanced healthcare infrastructure, substantial research and development activities, and high adoption rate of innovative diagnostic technologies. Germany's strong focus on cancer research, presence of leading diagnostic companies, and well-established reimbursement framework contribute to its market dominance. The country's healthcare system emphasizes early disease detection and precision medicine, driving the demand for advanced tissue diagnostic solutions. Additionally, the growing aging population and increasing cancer prevalence continue to fuel market growth.

Tissue Diagnostics Market Growth Trajectory in France

France emerges as the fastest-growing market in Europe, with an anticipated CAGR of approximately 8% during 2024-2029. The country's robust growth is driven by increasing investments in healthcare infrastructure, rising adoption of digital pathology solutions, and growing focus on personalized medicine. France's strong emphasis on cancer research and treatment, coupled with favorable government initiatives supporting diagnostic technologies, contributes to this growth trajectory. The country's healthcare system's focus on preventive care and early disease detection, along with increasing awareness about cancer screening, continues to drive market expansion. Additionally, the presence of leading research institutions and growing collaborations between healthcare providers and diagnostic companies support market growth.

Tissue Diagnostics Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market for tissue diagnostics, characterized by improving healthcare infrastructure, increasing healthcare expenditure, and growing awareness about early disease detection. The region encompasses key markets including China, Japan, India, Australia, and South Korea, each contributing uniquely to the market dynamics. The market is driven by the large patient population, rising prevalence of cancer, and increasing adoption of advanced diagnostic technologies. Government initiatives supporting healthcare infrastructure development and growing investments in research and development further strengthen the market landscape.

Tissue Diagnostics Market in China

China emerges as the dominant force in the Asia-Pacific tissue diagnostics market, driven by its large population base, expanding healthcare infrastructure, and increasing government focus on improving cancer diagnosis and treatment facilities. The country's market leadership is supported by rising healthcare expenditure, growing adoption of advanced diagnostic technologies, and increasing awareness about early disease detection. China's robust research and development activities, coupled with growing investments in healthcare infrastructure, contribute to its market dominance. The country's focus on modernizing its healthcare system and increasing access to advanced diagnostic services continues to drive market growth.

Tissue Diagnostics Market Growth Trajectory in China

China maintains its position as the fastest-growing market in the Asia-Pacific region, driven by rapid healthcare infrastructure development, increasing adoption of advanced diagnostic technologies, and growing focus on precision medicine. The country's commitment to improving healthcare access, coupled with rising investments in research and development, supports this growth trajectory. China's expanding middle class, increasing healthcare awareness, and growing demand for quality diagnostic services contribute to market expansion. Additionally, government initiatives supporting healthcare modernization and increasing collaborations with international diagnostic companies continue to drive market growth.

Tissue Diagnostics Market in Middle East & Africa

The Middle East & Africa region presents a growing market for tissue diagnostics, characterized by improving healthcare infrastructure and increasing investments in diagnostic facilities. The region encompasses the GCC countries and South Africa as key markets, with varying levels of healthcare development and market maturity. The market is driven by government initiatives to improve healthcare services, increasing awareness about early disease detection, and growing medical tourism. Within the region, GCC countries represent the largest market, while South Africa emerges as the fastest-growing market, supported by improving healthcare infrastructure and increasing adoption of advanced diagnostic technologies.

Tissue Diagnostics Market in South America

The South American tissue diagnostics market demonstrates steady growth potential, supported by improving healthcare infrastructure and increasing focus on cancer diagnosis and treatment. The region includes Brazil and Argentina as key markets, each contributing to the overall market development. The market is characterized by growing awareness about early disease detection, increasing healthcare expenditure, and rising adoption of advanced diagnostic technologies. Brazil emerges as both the largest and fastest-growing market in the region, driven by its large population base, expanding healthcare infrastructure, and increasing investments in diagnostic facilities.

Get Analysis on Important Geographic Markets

Download PDF

Tissue Diagnostics Industry Overview

Top Companies in Tissue Diagnostics Market

The tissue diagnostics market features prominent players like Abbott Laboratories, Roche, Danaher Corporation, Thermo Fisher Scientific, and Qiagen, leading the industry through continuous innovation and strategic expansion. These tissue diagnostics companies are heavily investing in research and development to advance their digital pathology capabilities, particularly in areas of artificial intelligence and machine learning integration for improved diagnostic accuracy. The market is characterized by strategic collaborations between diagnostic companies and healthcare providers to enhance product accessibility and service delivery. Companies are focusing on developing automated solutions and integrated workflow systems to improve laboratory efficiency and reduce diagnostic turnaround times. Geographic expansion, particularly in emerging markets, remains a key strategy, with companies establishing regional centers of excellence and strengthening their distribution networks to capture growing demand in developing economies.

Consolidated Market with Strong Regional Players

The tissue diagnostics market demonstrates a moderately consolidated structure, dominated by large multinational corporations with diverse healthcare portfolios alongside specialized diagnostic companies. These major players leverage their extensive research capabilities, global distribution networks, and comprehensive product portfolios to maintain their market positions. The market witnesses a mix of global conglomerates that offer end-to-end diagnostic solutions and regional specialists focusing on specific geographic markets or technological niches. The presence of strong regional players, particularly in developed healthcare markets, adds a competitive dynamic through their deep understanding of local healthcare systems and regulatory requirements. The competitive landscape is further shaped by the increasing presence of Asian manufacturers who are gradually expanding their international footprint through cost-effective solutions and improving technological capabilities.

Merger and acquisition activities in the tissue diagnostics sector remain robust, driven by the need to acquire innovative technologies, expand geographic presence, and strengthen product portfolios. Large companies actively pursue acquisitions of smaller, innovative firms to gain access to novel diagnostic technologies and complement their existing product lines. Strategic partnerships and collaborations between diagnostic companies and research institutions are becoming increasingly common, fostering innovation and accelerating product development cycles. The market also sees vertical integration attempts, with companies acquiring suppliers or distributors to gain better control over their supply chain and distribution channels.

Innovation and Integration Drive Market Success

Success in the tissue diagnostics market increasingly depends on companies' ability to develop integrated diagnostic solutions that combine traditional tissue analysis with digital pathology and artificial intelligence capabilities. Market leaders are focusing on developing comprehensive platforms that offer end-to-end solutions, from sample preparation to result analysis and interpretation. Companies are investing in user-friendly interfaces and automated systems to address the growing demand for efficient workflow solutions in pathology laboratories. The ability to provide reliable after-sales support, technical training, and continuous system upgrades has become crucial for maintaining customer relationships and market share. Companies are also emphasizing the development of companion diagnostics and personalized medicine solutions to align with the broader trends in healthcare delivery.

For new entrants and smaller players, success lies in identifying and focusing on specific market niches or underserved geographic regions. The increasing adoption of digital pathology solutions presents opportunities for technology-focused companies to enter the market with innovative software solutions or specialized diagnostic tools. Regulatory compliance remains a critical factor, with companies needing to navigate complex approval processes across different regions while maintaining high quality standards. The market's future will be significantly influenced by the ability to adapt to changing healthcare delivery models, including the integration of remote diagnostic capabilities and cloud-based solutions. Companies that can effectively address the growing demand for standardization in diagnostic procedures while offering cost-effective solutions will likely gain competitive advantages.

Tissue Diagnostics Market Leaders

-

Agilent Technologies, Inc.

-

F. Hoffmann-La Roche Ltd

-

Merck KGaA

-

Thermo Fisher Scientific

-

Abbott

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Tissue Diagnostics Market News

- June 2024: F. Hoffmann-La Roche Ltd received a 510(k) clearance from the United States Food and Drug Administration (US FDA) for its Roche Digital Pathology Dx. The newly cleared system helps pathologists interpret digital images for accurate diagnosis.

- March 2023: Aptamer Group developed a new reagent, Optimer-Fc, for automated immunohistochemistry (IHC) workflows to detect if cells have cancer or other disease markers.

Tissue Diagnostics Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Rising Burden of Cancer

- 4.2.2 Growing Healthcare Expenditure

- 4.2.3 Technological Advancements in Tissue Diagnostics

-

4.3 Market Restraints

- 4.3.1 High Cost of Diagnosis and Reimbursement Issues

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value in USD)

-

5.1 By Product

- 5.1.1 Instruments

- 5.1.2 Reagents and Consumables

-

5.2 By Technology

- 5.2.1 Immunohistochemistry

- 5.2.2 In-situ Hybridization

- 5.2.3 Digital Pathology and Workflow Management

- 5.2.4 Other Technologies

-

5.3 By Application

- 5.3.1 Breast Cancer

- 5.3.2 Prostate Cancer

- 5.3.3 Gastric Cancer

- 5.3.4 Other Cancers

-

5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Abbott

- 6.1.2 Agilent Technologies Inc.

- 6.1.3 BioGenex Laboratories

- 6.1.4 Illumina Inc.

- 6.1.5 Danaher

- 6.1.6 F. Hoffmann-La Roche Ltd

- 6.1.7 QIAGEN

- 6.1.8 Merck KGaA

- 6.1.9 Thermo Fisher Scientific Inc.

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape covers- Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Tissue Diagnostics Industry Segmentation

As per the scope of the report, tissue diagnostics involves monitoring and diagnosis of different stages of cancer. The tissue diagnostics market is segmented by product, technology, application, and geography.

The tissue diagnostics market is segmented by product, technology, application, and geography. By product, the market is segmented into instruments, reagents, and consumables. By technology, the market is segmented as immunohistochemistry, in-situ hybridizations, digital pathology and workflow management, and other technologies. By application, the market is segmented into breast cancer, prostate cancer, gastric cancer, and other cancers. The report also covers the market sizes and forecasts for tissue diagnostics in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| By Product | Instruments | ||

| Reagents and Consumables | |||

| By Technology | Immunohistochemistry | ||

| In-situ Hybridization | |||

| Digital Pathology and Workflow Management | |||

| Other Technologies | |||

| By Application | Breast Cancer | ||

| Prostate Cancer | |||

| Gastric Cancer | |||

| Other Cancers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Tissue Diagnostics Market Research FAQs

How big is the Tissue Diagnostics Market?

The Tissue Diagnostics Market size is expected to reach USD 6.45 billion in 2025 and grow at a CAGR of 6.64% to reach USD 8.90 billion by 2030.

What is the current Tissue Diagnostics Market size?

In 2025, the Tissue Diagnostics Market size is expected to reach USD 6.45 billion.

Who are the key players in Tissue Diagnostics Market?

Agilent Technologies, Inc., F. Hoffmann-La Roche Ltd, Merck KGaA, Thermo Fisher Scientific and Abbott are the major companies operating in the Tissue Diagnostics Market.

Which is the fastest growing region in Tissue Diagnostics Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Tissue Diagnostics Market?

In 2025, the North America accounts for the largest market share in Tissue Diagnostics Market.

What years does this Tissue Diagnostics Market cover, and what was the market size in 2024?

In 2024, the Tissue Diagnostics Market size was estimated at USD 6.02 billion. The report covers the Tissue Diagnostics Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Tissue Diagnostics Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Tissue Diagnostics Market Research

Mordor Intelligence provides comprehensive insights into the rapidly evolving tissue diagnostics market. We leverage our extensive experience in the in vitro diagnostics (IVD) industry to deliver detailed analysis. Our expert research team covers tissue testing methodologies such as immunohistochemistry, molecular diagnostics, and digital pathology applications. The report, available as an easy-to-read PDF download, thoroughly examines tissue analysis procedures performed in modern pathology laboratory settings. This includes both anatomical pathology and cellular pathology practices.

Our in-depth analysis addresses crucial aspects of tissue processing, tissue staining, and tissue biopsy procedures. We also explore advanced technologies like tissue imaging and the development of tissue biomarkers. The report examines key market segments, including surgical pathology, cytology testing, and emerging tissue screening methodologies. Stakeholders gain valuable insights into histology equipment trends, tissue diagnostics companies, and technological innovations in digital pathology market developments. The comprehensive coverage extends to the dynamics of the immunohistochemistry market and trends in the molecular diagnostics industry. This provides actionable intelligence for strategic decision-making in the expanding in vitro diagnostics industry.