| Study Period | 2019 - 2030 |

| Market Volume (2025) | 174.31 Million units |

| Market Volume (2030) | 257.78 Million units |

| CAGR | 8.14 % |

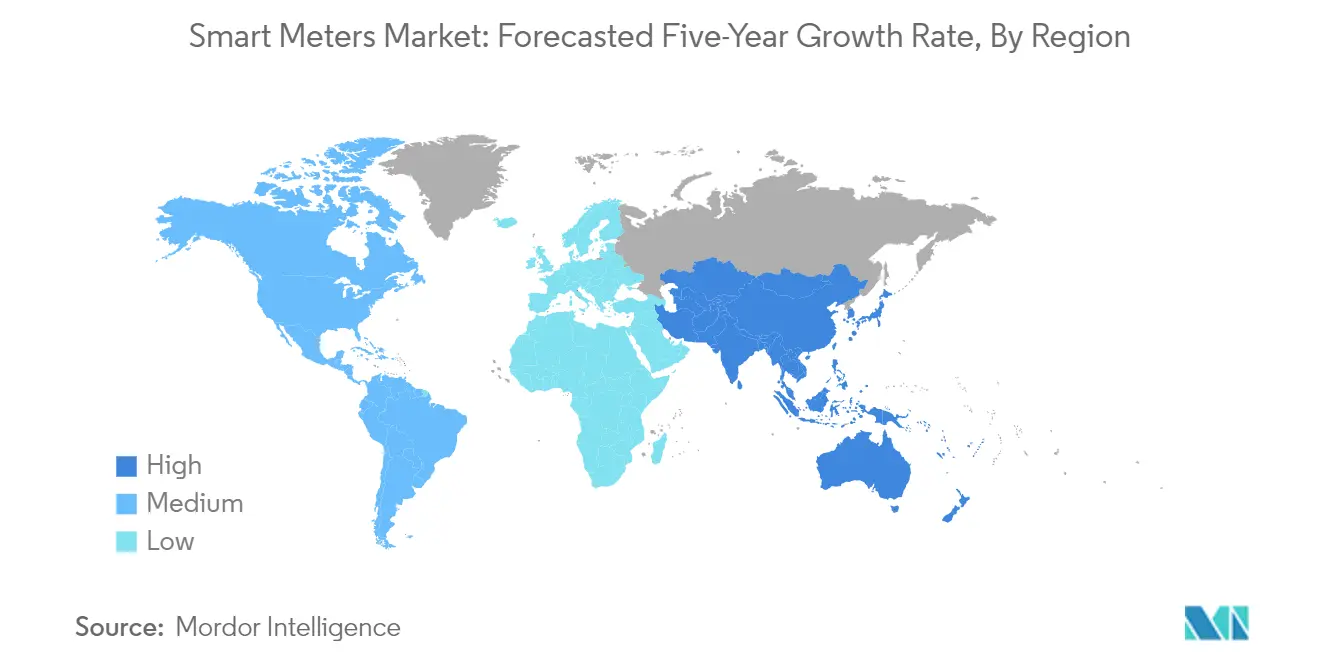

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players Market Major Players")

*Disclaimer: Major Players sorted in no particular order |

Market Size")

Smart Meters (AMI) Market Analysis

The Smart Meters Market size in terms of shipment volume is expected to grow from 174.31 million units in 2025 to 257.78 million units by 2030, at a CAGR of 8.14% during the forecast period (2025-2030).

The smart meters market is experiencing a significant transformation driven by the increasing digitalization of energy infrastructure and evolving consumer demands. According to GSMA projections, North America alone is expected to have approximately 1.4 billion smart buildings and 700 million smart homes by 2025, highlighting the massive scale of potential smart metering implementations. This digital revolution is reshaping how utilities and consumers interact with energy systems, leading to more sophisticated demand-response programs and enhanced smart grid management capabilities. The integration of advanced technologies like IoT, machine learning, and big data analytics is enabling unprecedented levels of data collection and analysis, allowing utilities to make more informed decisions about energy distribution and consumption patterns.

The industry is witnessing a notable shift towards sustainable energy management practices, with particular emphasis on reducing unnecessary power consumption. Studies indicate that consumer electronics and office equipment consume approximately 15-20% of total residential and commercial electricity while not in primary mode, mostly during low-power operations. This revelation has sparked increased interest in advanced metering infrastructure systems that can track and optimize energy usage patterns. The trend towards energy efficiency is further supported by the growing adoption of renewable energy sources and the need for more sophisticated smart grid management systems.

The global electricity landscape is undergoing a dramatic expansion, with the Energy Information Administration (EIA) forecasting that worldwide electricity generation capacity will more than double in the next three decades, reaching approximately 14.7 terawatts by 2050. This substantial growth is driving utilities to seek more efficient ways to manage and optimize their distribution networks. The integration of smart metering with advanced analytics capabilities is becoming increasingly crucial for utilities to handle this growing capacity while maintaining grid stability and reliability.

Technological innovation continues to drive market evolution, particularly in the development of next-generation smart metering solutions. In Japan, industry projections suggest the installation of up to 80 million smart meters nationwide by 2024, supported by a significant government investment of JPY 20 trillion (USD 155 billion) in new power grid technology and energy-saving initiatives. These advancements are not limited to basic metering functions but extend to sophisticated features such as real-time data analytics, predictive maintenance capabilities, and integration with other smart home technologies. The industry is seeing an increased focus on developing interoperable solutions that can seamlessly connect with various advanced metering infrastructure components and energy management systems.

Segment Analysis: By Smart Gas Meter

Europe Segment in Smart Gas Meter Market

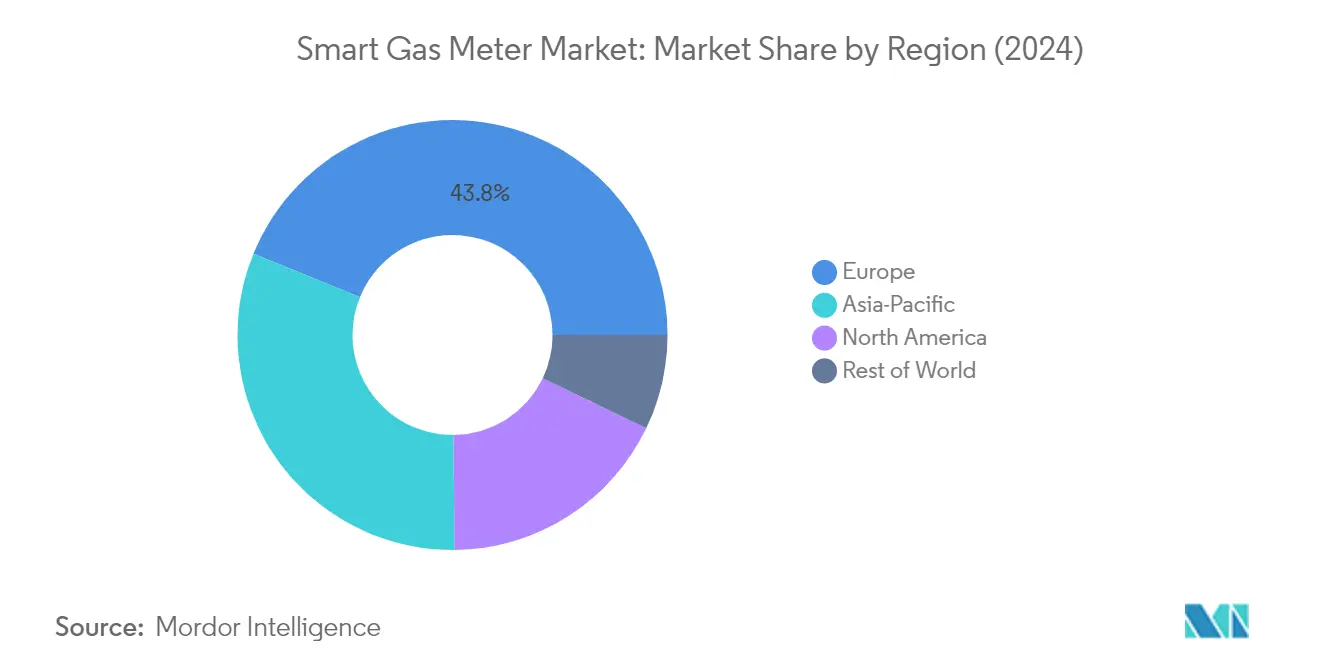

Europe dominates the global smart gas meter market, commanding approximately 44% market share in 2024. The region's leadership position is primarily driven by strong governmental support and regulatory frameworks promoting smart meter adoption. Countries like the United Kingdom, France, and Italy are at the forefront of smart gas meter deployment, with significant rollout programs underway. The European Union's energy efficiency directives and climate targets have created a favorable environment for smart gas meter adoption, while the region's focus on reducing carbon emissions and modernizing gas infrastructure continues to drive market growth. The presence of major smart meter suppliers and advanced technological infrastructure further strengthens Europe's position in the global market.

Asia-Pacific Segment in Smart Gas Meter Market

The Asia-Pacific region is emerging as the fastest-growing segment in the smart gas meter market, with an expected growth rate of approximately 10% during 2024-2029. This remarkable growth is fueled by rapid urbanization, increasing natural gas consumption, and ambitious smart city initiatives across countries like China and Japan. Government initiatives promoting energy efficiency and the modernization of utility infrastructure are driving widespread adoption. The region's focus on reducing non-revenue gas losses and improving billing accuracy has led to increased investments in smart metering systems solutions. Additionally, the growing emphasis on environmental sustainability and the need for better energy management systems in developing economies is expected to maintain this strong growth momentum.

Remaining Segments in Smart Gas Meter Market

North America and Rest of World regions represent significant opportunities in the smart gas meter market, each bringing unique dynamics to the industry. North America's market is characterized by advanced technological adoption and strong utility modernization programs, particularly in the United States and Canada. The region's focus on grid modernization and energy efficiency initiatives continues to drive smart meter adoption. Meanwhile, the Rest of World region, encompassing Latin America, the Middle East, and Africa, shows growing potential driven by increasing urbanization and utility infrastructure development. These regions are increasingly recognizing the benefits of smart gas metering in reducing losses and improving operational efficiency, though adoption rates vary significantly based on local regulatory environments and infrastructure readiness.

Segment Analysis: By Smart Water Meter

Asia-Pacific Segment in Smart Water Meter Market

The Asia-Pacific region dominates the smart water meter market, commanding approximately 42% market share in 2024. This significant market position is primarily driven by China's extensive deployment of smart water meters, accounting for over 52% of the region's installations. The region's leadership is further strengthened by Japan's substantial contribution of about 25% to the regional market, followed by other rapidly developing economies. Major initiatives such as India's smart city developments, Singapore's comprehensive water management programs, and Australia's growing focus on water conservation have significantly contributed to this dominance. The region's large population base, rapid urbanization, and increasing government support for smart water infrastructure have created a robust market environment for smart water meters.

European Segment in Smart Water Meter Market

Europe is emerging as the fastest-growing segment in the smart water meter market, with a projected growth rate of approximately 12% during 2024-2029. This accelerated growth is driven by stringent water conservation regulations, increasing focus on reducing non-revenue water losses, and substantial investments in water infrastructure modernization. Countries like France, the United Kingdom, and Italy are leading this growth through aggressive smart meter deployment programs. The European Union's strong push towards digitalization of utilities, coupled with increasing environmental concerns and water scarcity issues, particularly in Southern European countries, is accelerating the adoption of smart water meters. The region's emphasis on sustainable water management practices and the integration of advanced IoT technologies in water infrastructure are creating favorable conditions for market expansion.

Remaining Segments in Smart Water Meter Market

North America and Rest of the World segments play crucial roles in shaping the global smart water meter market landscape. North America's market is characterized by advanced infrastructure and high technology adoption rates, with utilities focusing on modernizing their water management systems. The region's emphasis on reducing water wastage and improving billing accuracy continues to drive smart meter adoption. Meanwhile, the Rest of the World segment, encompassing Latin America, the Middle East, and Africa, is witnessing growing interest in smart water metering solutions, particularly in urban areas and developing economies. These regions are increasingly recognizing the importance of efficient water management systems, with several countries implementing pilot projects and regulatory frameworks to support smart meter deployment.

Segment Analysis: By Smart Electricity Meter

Asia-Pacific Segment in Smart Electricity Meter Market

The Asia-Pacific region dominates the global smart electricity meter market, accounting for approximately 55% of the total market share in 2024. This significant market position is primarily driven by China's extensive smart meter deployment initiatives and Japan's aggressive adoption of smart metering technologies. The region's leadership is further strengthened by substantial government investments in grid modernization projects, particularly in countries like India, Australia, and South Korea. The increasing focus on renewable energy integration, rising urbanization, and growing energy demand across the region have created a robust ecosystem for smart electricity meter adoption. Additionally, the implementation of favorable policies supporting smart grid development and the presence of major manufacturing hubs have contributed to the region's market dominance.

Latin America Segment in Smart Electricity Meter Market

Latin America has emerged as the fastest-growing segment in the smart electricity meter market, with Brazil leading the regional growth trajectory. The region's rapid expansion is driven by increasing government initiatives for grid modernization, rising energy consumption, and growing awareness about energy efficiency. Countries like Mexico, Colombia, and Chile are implementing ambitious smart meter rollout programs to improve their utility infrastructure and reduce power losses. The region's utilities are increasingly adopting smart utility meter solutions to address challenges such as electricity theft, improve billing accuracy, and enhance customer service. Furthermore, the growing investments in renewable energy projects and the need for better energy management systems are creating substantial opportunities for smart meter deployments across Latin American countries.

Remaining Segments in Smart Electricity Meter Market

The European market maintains a strong position in the smart electricity meter landscape, driven by stringent regulatory frameworks and ambitious clean energy targets. North America continues to demonstrate steady growth through advanced infrastructure development and increasing focus on grid modernization initiatives. The Middle East and Africa region, while smaller in market size, shows promising growth potential due to increasing urbanization and smart city initiatives. These regions are characterized by different adoption rates and implementation strategies, influenced by factors such as existing infrastructure, regulatory environment, and technological readiness. The varying pace of smart meter rollouts across these regions reflects the diverse challenges and opportunities in different geographical markets.

Smart Meters Market Geography Segment Analysis

Smart Meters Market in North America

North America represents a mature smart meters market, with the United States and Canada leading the adoption across gas, water, and electricity segments. The region's growth is primarily driven by government initiatives promoting energy efficiency, modernization of aging infrastructure, and an increasing focus on reducing non-revenue losses. Both countries have made significant investments in smart grid technologies and advanced metering infrastructure, supported by favorable regulatory frameworks and utility companies' commitment to digital transformation.

Smart Meters Market in United States

The United States dominates the North American smart meters market landscape with approximately 89% smart meter market share in 2024. The country's leadership position is attributed to extensive smart grid projects, strong utility participation, and comprehensive government support for grid modernization initiatives. The US market benefits from advanced technological infrastructure, increasing adoption of renewable energy sources, and growing awareness about energy conservation. Several major utilities are actively expanding their smart meter deployments while leveraging smart meters data and IoT capabilities to enhance grid efficiency and customer service.

Smart Meters Market in Canada

Canada exhibits the highest growth potential in North America, with a projected growth rate of approximately 14% during 2024-2029. The country's smart meter market is experiencing rapid expansion driven by provincial mandates for smart meter installation, an increasing focus on water conservation, and a growing emphasis on renewable energy integration. Canadian utilities are particularly focused on implementing advanced metering infrastructure to improve operational efficiency and customer service. The country's commitment to reducing greenhouse gas emissions and modernizing its energy infrastructure continues to create favorable conditions for smart meter adoption.

Smart Meters Market in Europe

Europe maintains a strong position in the global smart meter market, with significant deployments across the United Kingdom, France, Spain, and Italy. The region's market is characterized by stringent regulatory frameworks, ambitious environmental targets, and widespread utility modernization programs. The European Union's energy efficiency directives and sustainability goals have been instrumental in driving smart meter adoption across member states.

Smart Meters Market in France

France leads the European smart meters market with approximately 23% smart meter market share in 2024. The country has established itself as a pioneer in smart meter deployment through comprehensive national programs and utility-driven initiatives. French utilities have successfully implemented large-scale smart meter rollouts, supported by strong government backing and technological innovation in the energy sector.

Smart Meters Market in United Kingdom

The United Kingdom demonstrates remarkable growth potential with an expected growth rate of approximately 8% during 2024-2029. The country's smart meter market benefits from ambitious government targets, strong regulatory support, and increasing consumer awareness about energy efficiency. British utilities are actively investing in next-generation smart meter technologies and advanced communication networks to enhance grid reliability and consumer engagement.

Smart Meters Market in Asia-Pacific

The Asia-Pacific region represents a dynamic smart meters market, encompassing diverse economies like China, Japan, and New Zealand. The region's market is driven by rapid urbanization, increasing energy demand, and a growing focus on water conservation. China leads the regional market in terms of deployment scale, while Japan shows the strongest growth potential. The region's utilities are increasingly adopting smart metering solutions to address challenges related to resource management, operational efficiency, and customer service improvement.

Smart Meters Market in China

China maintains its position as the largest smart meter market in Asia-Pacific, driven by extensive government support, rapid urban development, and ambitious smart city initiatives. The country's utilities are implementing comprehensive smart metering programs as part of broader grid modernization efforts. Chinese manufacturers are also playing a crucial role in developing cost-effective smart meter solutions for both domestic and international markets.

Smart Meters Market in Japan

Japan emerges as the fastest-growing market in Asia-Pacific, supported by advanced technological infrastructure and strong utility commitment to grid modernization. The country's utilities are focusing on implementing next-generation smart meters with enhanced communication capabilities and advanced features. Japan's smart meter market benefits from strong government support, technological innovation, and an increasing focus on energy efficiency.

Smart Meters Market in Latin America

Latin America represents an emerging smart meters market, with Brazil and Mexico leading regional adoption. The market is characterized by increasing utility modernization initiatives, a growing focus on reducing non-technical losses, and rising energy demand. Brazil emerges as both the largest and fastest-growing market in the region, driven by extensive utility modernization programs and government support for smart grid initiatives.

Smart Meters Market in Middle East and Africa

The Middle East and Africa region shows promising growth potential in the smart meters market, with significant developments in GCC countries and South Africa. The market is driven by increasing urbanization, smart city initiatives, and a growing focus on resource conservation. The United Arab Emirates leads the regional market, while Saudi Arabia shows the fastest growth potential, supported by ambitious smart city projects and utility modernization programs.

Get Analysis on Important Geographic Markets

Download PDF

Smart Meters (AMI) Market Overview

Top Companies in Smart Meters Market

The smart meters companies market features a mix of established multinational corporations and specialized metering solution providers competing through continuous innovation and strategic expansion. Companies are increasingly focusing on developing comprehensive end-to-end solutions that integrate advanced communication protocols, data analytics capabilities, and enhanced security features. The industry witnesses substantial investment in research and development to create more efficient, reliable, and cost-effective smart metering solutions. Market leaders are expanding their geographical presence through strategic partnerships, joint ventures, and distributor networks while simultaneously diversifying their product portfolios to include electricity, gas, and water metering solutions. There is a growing emphasis on developing interoperable solutions that can seamlessly integrate with existing infrastructure while providing enhanced functionality for utility providers and end-users.

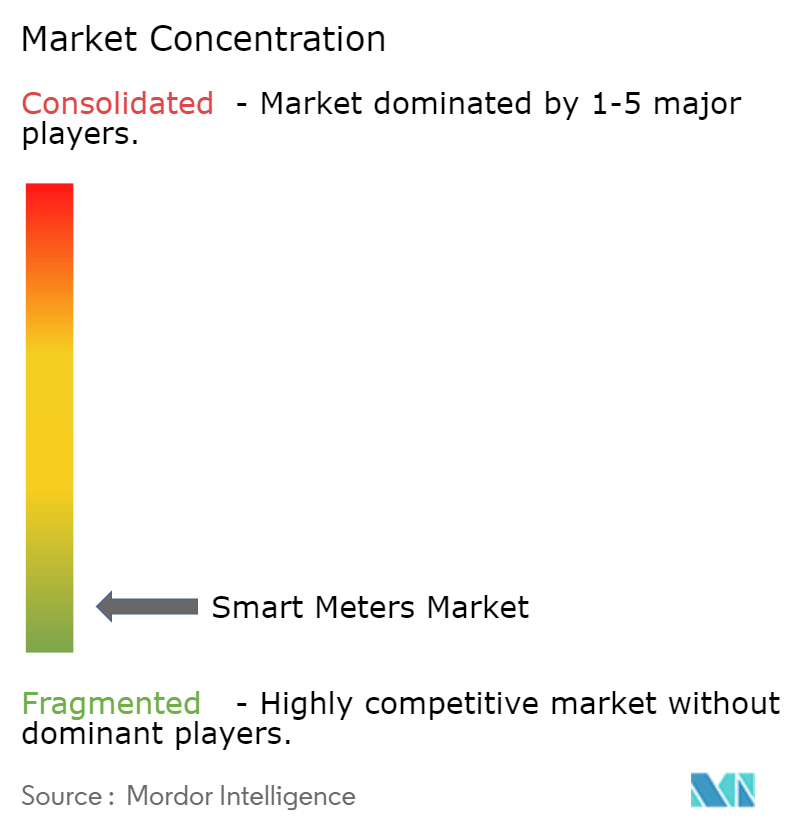

Consolidated Market with Strong Regional Players

The smart meters market exhibits a relatively consolidated structure dominated by large multinational corporations with significant manufacturing capabilities and extensive distribution networks. These major players leverage their technological expertise, financial resources, and established relationships with utility providers to maintain their market positions. Regional specialists have carved out strong positions in their respective markets by offering customized solutions that address local requirements and regulations. The industry has witnessed significant merger and acquisition activity as larger companies seek to acquire innovative technology startups and regional players to expand their capabilities and market reach.

The competitive landscape is characterized by the presence of both diversified industrial conglomerates that offer smart metering as part of their broader energy management solutions, and specialized manufacturers focused exclusively on metering technologies. Market consolidation continues as companies seek to achieve economies of scale and expand their technological capabilities through strategic acquisitions. Local players maintain competitive advantages in certain regions due to their understanding of specific market requirements, established relationships with utility providers, and ability to provide customized solutions for regional needs.

Innovation and Adaptability Drive Market Success

Success in the smart meters market increasingly depends on companies' ability to develop innovative solutions that address evolving utility requirements while maintaining cost competitiveness. Incumbent players must focus on continuous product innovation, enhanced communication capabilities, and improved data analytics features to maintain their market positions. Companies need to invest in developing comprehensive solutions that integrate seamlessly with smart grid infrastructure while ensuring robust cybersecurity measures. The ability to provide excellent after-sales support, maintenance services, and software updates has become crucial for maintaining long-term customer relationships and securing large-scale deployment contracts.

Market contenders can gain ground by focusing on niche applications, developing specialized solutions for specific industry segments, or targeting underserved regional markets. Success factors include the ability to offer competitive pricing while maintaining product quality, establishing strong partnerships with utility providers, and developing innovative financing models for large-scale deployments. Companies must also navigate complex regulatory environments, address growing cybersecurity concerns, and ensure their solutions comply with evolving industry standards and environmental regulations. The increasing focus on sustainability and energy efficiency creates opportunities for companies that can demonstrate the environmental benefits of their smart metering industry solutions.

Smart Meters (AMI) Market Leaders

-

AEM

-

Aichi Tokei Denki Co., Ltd.

-

Apator SA

-

Arad Group

-

Azbil Kimmon Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Smart Meters (AMI) Market News

- September 2024: Metron, a global frontrunner in cellular-based smart metering and water intelligence, unveiled two groundbreaking products: WaterScope Utility, an analytics app designed to optimize frontline operations in intricate municipal water systems, and the Metron Spectrum Wave, a state-of-the-art ultrasonic smart meter that marries versatility and durability with top-tier data capture capabilities.

- July 2024: Genus Power Infrastructures Limited (Genus), a frontrunner in smart meter technology boasting a vast installation base of smart electricity meters, has achieved a significant milestone by successfully shipping its Smart Ultrasonic Water Meters DN20 to Australia. This shipment underscores Genus's strategic expansion into water management solutions. The advanced meters, featuring LoRa communication technology, facilitate remote monitoring and management, heralding a significant leap forward in smart water distribution.

- May 2024: Oakter unveiled its latest innovation, the OAKMETER, a state-of-the-art smart energy meter. Leveraging advanced technologies like Advanced Metering Infrastructure, real-time data analytics, and Internet of Things (IoT) capabilities, Oakter’s Smart Meter establishes a two-way communication link with utility servers through internet connectivity. This sophisticated setup detects tampering and ensures real-time data transmission every 15 to 30 minutes. Additionally, it identifies outages and allows users to monitor their energy consumption directly from mobile devices.

Smart Meters (AMI) Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 mpact of Macroeconomic Factors on the Global Smart Meter Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increased Investments in Smart Grid Projects

- 5.1.2 Need for Improvement in Utility Efficiency

- 5.1.3 Supportive Government Regulations

- 5.1.4 Growth in Smart City Deployment

- 5.1.5 Demand for Sustainable Utility Supply for All End Users

-

5.2 Market Challenges

- 5.2.1 High Costs and Security Concerns

- 5.2.2 Integration Difficulties with Smart Meters

- 5.2.3 Lack of Capital Investment for Infrastructure Installation and Lack of ROI

- 5.2.4 Utility Supplier Switching Costs

6. MARKET SEGMENTATION

-

6.1 By Geography - Smart Gas Meter***

- 6.1.1 North America

- 6.1.1.1 United States

- 6.1.1.2 Canada and Central America

- 6.1.2 Europe

- 6.1.2.1 United Kingdom

- 6.1.2.2 France

- 6.1.2.3 Italy

- 6.1.3 Asia

- 6.1.3.1 China

- 6.1.3.2 Japan

- 6.1.4 Australia and New Zealand

- 6.1.5 Latin America

- 6.1.6 Middle East and Africa

-

6.2 By Geography - Smart Water Meter***

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada and Central America

- 6.2.2 Europe

- 6.2.2.1 United Kingdom

- 6.2.2.2 France

- 6.2.2.3 Italy

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 Japan

- 6.2.4 Australia and New Zealand

- 6.2.5 Latin America

- 6.2.6 Middle East and Africa

-

6.3 By Geography - Smart Electricity Meter***

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada and Central America

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 France

- 6.3.2.3 Italy

- 6.3.3 Asia

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.4 Australia and New Zealand

- 6.3.5 Latin America

- 6.3.6 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 AEM

- 7.1.2 Aichi Tokei Denki Co.Ltd.

- 7.1.3 Apator SA

- 7.1.4 Arad Group

- 7.1.5 Azbil Kimmon Co. Ltd.

- 7.1.6 Badger Meter Inc.

- 7.1.7 Diehl Stiftung & Co. KG

- 7.1.8 Elster Group GmbH (Honeywell International Inc.)

- 7.1.9 General Electric Company

- 7.1.10 Hexing Electric company Ltd.

- 7.1.11 Holley Technology Ltd.

- 7.1.12 Itron Inc.

- 7.1.13 Jiangsu Linyang Energy Co. Ltd.

- 7.1.14 Kamstrup A/S

- 7.1.15 Landis+ GYR Group AG

- 7.1.16 Mueller Systems LLC (Muller Water Products Inc.)

- 7.1.17 EDMI Limited (OSAKI ELECTRIC CO. LTD.)

- 7.1.18 Neptune Technology Group Inc. (Roper Technologies, Inc.)

- 7.1.19 Ningbo Sanxing Medical Electric Co., Ltd

- 7.1.20 Pietro Fiorentini SpA

- 7.1.21 Sagemcom SAS

- 7.1.22 Sensus USA Inc. (Xylem Inc.)

- 7.1.23 Aclara Technologies LLC (Hubbell Inc.)

- 7.1.24 Wasion Holdings Limited

- 7.1.25 Yazaki Corporation

- 7.1.26 Zenner International GmbH & Co. KG

- *List Not Exhaustive

-

7.2 Market Rankings Analysis

- 7.2.1 Smart Electricity Meter Market

- 7.2.2 Smart Gas Meter Market

- 7.2.3 Smart Water Meter Market

8. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 8.1 Future of the Market - Smart Electricity Meter

- 8.2 Future of the Market - Smart Gas Meter

- 8.3 Future of the Market - Smart Water Meter

**Subject to Availability

***In the Final Report Asia, Australia and New Zealand will be Studied Together as 'Asia Pacific'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Smart Meters (AMI) Market Industry Segmentation

Smart meters, a groundbreaking innovation in the utility industry, facilitate enhanced communication between consumers and suppliers. These advanced devices not only showcase real-time energy consumption but also offer deeper insights into energy patterns. Leveraging a secure smart data network, smart meters automatically transmit readings to energy suppliers, ensuring precise billing.

The smart meters market is segmented by smart gas meters (North America (United States, Canada & Central America), Europe (United Kingdom, France, Italy, and the Rest of Europe), Asia Pacific (China, Japan, and the Rest of Asia Pacific), Rest of the World), by smart water meters (North America (United States, Canada & Central America), Europe (United Kingdom, France, Italy, and the Rest of Europe), Asia Pacific (China, Japan, and the Rest of Asia Pacific), Rest of the World), by smart electricity meters (North America (United States, Canada & Central America), Europe (United Kingdom, France, Italy, and the Rest of Europe), Asia Pacific (China, Japan, and the Rest of Asia Pacific), Rest of the World). The market sizes and forecasts are provided in terms of volume (shipment units) for all the segments.

| By Geography - Smart Gas Meter*** | North America | United States | |

| Canada and Central America | |||

| Europe | United Kingdom | ||

| France | |||

| Italy | |||

| Asia | China | ||

| Japan | |||

| Australia and New Zealand | |||

| Latin America | |||

| Middle East and Africa | |||

| By Geography - Smart Water Meter*** | North America | United States | |

| Canada and Central America | |||

| Europe | United Kingdom | ||

| France | |||

| Italy | |||

| Asia | China | ||

| Japan | |||

| Australia and New Zealand | |||

| Latin America | |||

| Middle East and Africa | |||

| By Geography - Smart Electricity Meter*** | North America | United States | |

| Canada and Central America | |||

| Europe | United Kingdom | ||

| France | |||

| Italy | |||

| Asia | China | ||

| Japan | |||

| Australia and New Zealand | |||

| Latin America | |||

| Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Smart Meters (AMI) Market Research FAQs

How big is the Smart Meters Market?

The Smart Meters Market size is expected to reach 174.31 million units in 2025 and grow at a CAGR of 8.14% to reach 257.78 million units by 2030.

What is the current Smart Meters Market size?

In 2025, the Smart Meters Market size is expected to reach 174.31 million units.

Who are the key players in Smart Meters Market?

AEM, Aichi Tokei Denki Co., Ltd., Apator SA, Arad Group and Azbil Kimmon Co. Ltd are the major companies operating in the Smart Meters Market.

Which is the fastest growing region in Smart Meters Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Smart Meters Market?

In 2025, the Asia Pacific accounts for the largest market share in Smart Meters Market.

What years does this Smart Meters Market cover, and what was the market size in 2024?

In 2024, the Smart Meters Market size was estimated at 160.12 million units. The report covers the Smart Meters Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Smart Meters Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Smart Meters (AMI) Market Research

Mordor Intelligence provides comprehensive industry analysis and market insights for the smart meters market, covering crucial aspects like smart grid implementation, advanced metering infrastructure adoption, and evolving smart utilities landscape. Our industry research encompasses detailed market segmentation, technology trends, and competitive intelligence about leading smart meters companies. The report pdf includes in-depth market forecasts, growth drivers, and strategic analysis of key segments including residential smart meter, commercial smart meter, and industrial smart meter applications, helping stakeholders make informed decisions in this rapidly evolving industry.

Our consulting expertise extends beyond traditional market research to provide actionable intelligence for the smart metering ecosystem. We assist clients with technology scouting for next-generation smart energy meter solutions, regulatory assessment for various global markets, and comprehensive competition assessment of smart meter manufacturers. Our capabilities include detailed analysis of customer behavior patterns in smart meter adoption, assessment of emerging communication protocols, and evaluation of integration challenges with existing grid infrastructure. Through B2B surveys and advanced data analytics, we help clients understand market dynamics, optimize their go-to-market strategies, and identify potential partnership opportunities in the advanced metering infrastructure industry.