| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 7.38 % |

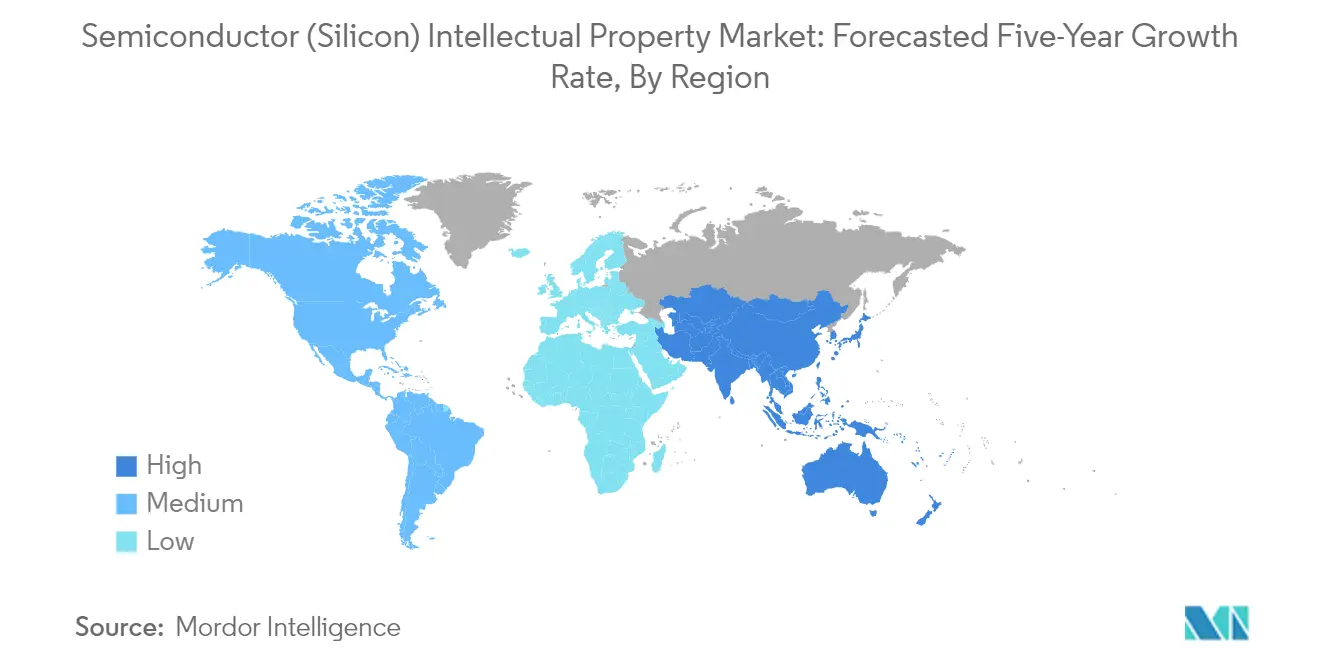

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Intellectual Property Market Size")

Semiconductor Silicon Intellectual Property (IP) Market Analysis

The Semiconductor Intellectual Property Market is expected to register a CAGR of 7.38% during the forecast period.

The Semiconductor Intellectual Property industry is experiencing unprecedented investment and expansion across global markets. According to SEMI's latest quarterly World Fab Forecast report, the semiconductor industry is set to invest more than USD 500 billion between 2021 and 2023 in establishing 84 large-scale chip manufacturing facilities worldwide. This massive investment surge reflects the industry's response to increasing demand across automotive and high-performance computing sectors. The global semiconductor materials market has shown remarkable strength, generating revenues of USD 72.69 billion in 2022, demonstrating the robust foundation of the industry's supply chain. Major industry players are making strategic moves to strengthen their positions, as evidenced by Applied Materials' establishment of a collaborative engineering center in Bangalore in 2023, focusing on developing and commercializing technologies for semiconductor manufacturing equipment.

The industry is witnessing a significant transformation in data center infrastructure and capabilities. According to CBRE Group, the power supply of data centers under construction in the United States reached 1.9 gigawatts in 2022, indicating substantial growth in computing infrastructure development. This expansion is driven by the increasing demands of artificial intelligence, machine learning, and advanced computing applications. The Semiconductor IP landscape is evolving to address these needs, with companies developing specialized solutions for high-performance computing and data center applications. This evolution is particularly evident in the development of advanced process nodes and the integration of artificial intelligence accelerators in semiconductor designs.

The market is experiencing a notable shift toward advanced packaging technologies and heterogeneous integration. Companies are increasingly focusing on developing innovative solutions that combine different types of Semiconductor IPs to create more efficient and powerful systems. This trend is supported by significant investments in research and development, as demonstrated by Intel's announcement of a EUR 33 billion investment in European chip development and manufacturing facilities in March 2023. The industry is also witnessing a growing emphasis on developing specialized IPs for specific applications, particularly in areas such as automotive electronics and industrial automation.

The Internet of Things (IoT) continues to be a major force shaping the Semiconductor IP Market. According to Ericsson, the number of short-range IoT devices reached 10.3 billion worldwide in 2022, highlighting the massive scale of IoT adoption. This proliferation of connected devices has led to increased demand for specialized Semiconductor IPs that can address specific requirements such as low power consumption, enhanced security, and improved connectivity. The industry is responding with innovative IP solutions that enable more efficient integration of multiple functions while maintaining optimal performance and power consumption levels. This trend is particularly evident in the development of new IP cores that combine processing capabilities with specialized functions for IoT applications.

Semiconductor Silicon Intellectual Property (IP) Market Trends

Growing Demand for Connected Devices

The proliferation of connected devices across consumer electronics, industrial applications, and communication systems is driving substantial demand for semiconductor IP. According to Ericsson, smartphone mobile network subscriptions worldwide are projected to grow from 6.42 billion in 2022 to 7.74 billion by 2028, highlighting the massive scale of connected device adoption. This expansion is further amplified by the emergence of 5G technology, with GSMA forecasting that 5G networks will cover approximately 34% of the global population by 2025, enabling more sophisticated and demanding applications that require advanced silicon IP solutions.

The Internet of Things (IoT) ecosystem represents another major growth catalyst, with Ericsson reporting that short-range IoT devices are expected to reach 25 billion by 2027. This trend is particularly evident in the wearables segment, where Cisco data shows connected wearable devices increased from 929 million in 2021 to 1,105 million in 2022. The growing complexity of these devices, which require error-free operation, higher data speeds, device miniaturization, and support for multiple wireless technologies while maintaining extended battery life, is creating sustained demand for sophisticated semiconductor intellectual property solutions that can address these challenging requirements.

Understand The Key Trends Shaping This Market

Download PDF

Growing Demand for Modern SoC Designs

Modern System-on-Chip (SoC) designs are becoming increasingly critical as data centers, artificial intelligence applications, and edge computing solutions demand more control over peak performance while optimizing power consumption and scalability. The development of purpose-built SoC designs is being driven by the need for specialized processing functions, particularly in emerging applications such as autonomous driving systems, AI accelerators, and high-performance computing platforms. These applications require custom processing elements and application-specific instruction-set processors (ASIPs) to address complex processing requirements efficiently.

The evolution of SoC complexity is further evidenced by the integration of multiple specialized functions, including power management, hardware voice activity detection (VAD), Graphics Processing Units (GPU), and various connectivity protocols into single-chip solutions. For instance, in June 2022, Renesas Electronics Corporation introduced the SmartBond DA1470x Family, integrating power management, VAD, GPU, and Bluetooth connectivity in a single SoC, demonstrating the industry's push toward more integrated and sophisticated designs. This trend is particularly prominent in automotive applications, where modern SoCs must support advanced driver-assistance systems (ADAS), in-vehicle infotainment, and autonomous driving capabilities, requiring extensive integration of sensors, processors, and connectivity solutions.

The semiconductor IP industry is poised to benefit significantly from these advancements, as the demand for custom and integrated solutions continues to grow. The IP market size is expected to expand as more companies seek to leverage silicon IP to meet the demands of modern technology applications, further driving the growth of the SIP market.

Segment Analysis: Revenue Type

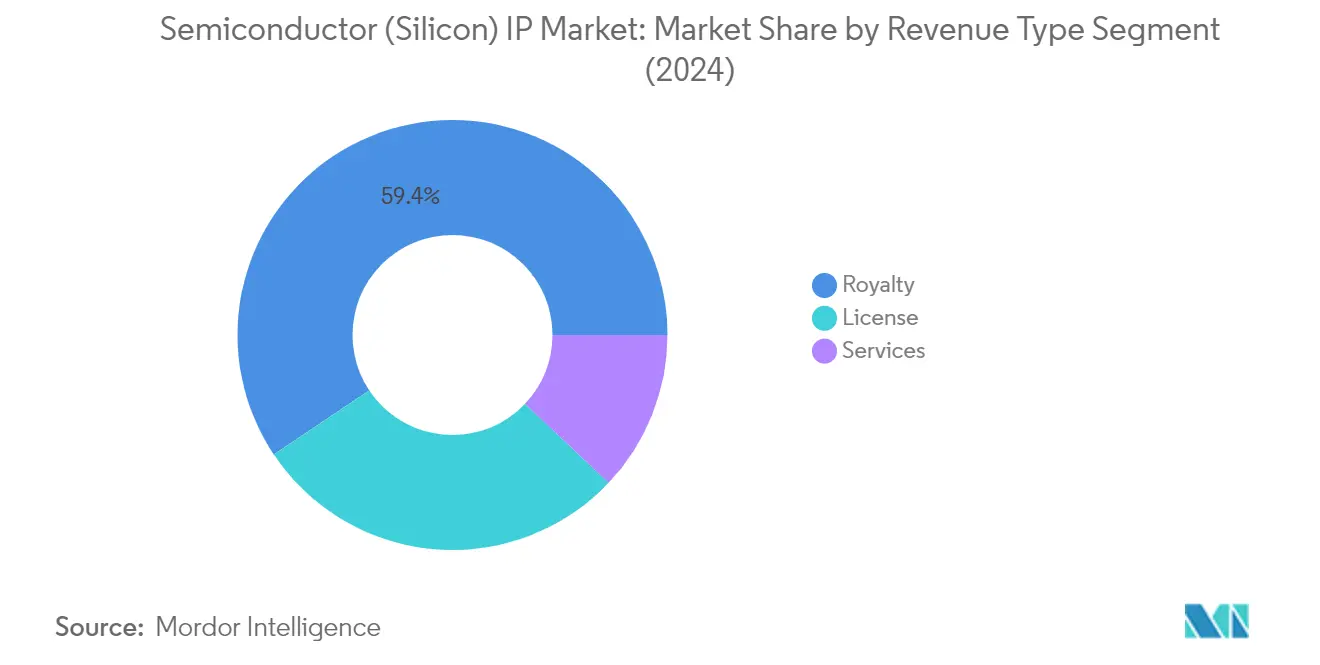

Royalty Segment in Semiconductor (Silicon) Intellectual Property Market

The royalty segment continues to dominate the semiconductor intellectual property market, commanding approximately 59% of the total SIP market share in 2024. This significant market position is attributed to the segment's business model, where providers and buyers share risks and rewards through ongoing royalty payments based on product success. The royalty revenue model has gained particular traction in licensing highly differentiated SIP products, often involving multiple stakeholders, including foundries for foundation semiconductor IP products and end-users for processor and specialty memory SIP. The segment's strength is further reinforced by the rapid technological changes in 5G smartphones, new processors, servers, and IoT applications, where manufacturers can produce various products and pay royalties only for those that achieve market success.

Services Segment in Semiconductor (Silicon) Intellectual Property Market

The services segment is projected to experience the highest growth rate of approximately 8% during the forecast period 2024-2029. This accelerated growth is driven by the increasing complexity of semiconductor designs and the growing demand for specialized design, testing, and consultation services. The segment's expansion is particularly notable in areas such as edge computing, 5G infrastructure, and advanced package test markets. Major industry players are actively expanding their service offerings through strategic partnerships and acquisitions, focusing on areas like automated solutions for semiconductor design verification and testing. The growth is further supported by the rising demand for customized solutions in emerging technologies like artificial intelligence and machine learning applications.

Remaining Segments in Revenue Type

The license segment represents a crucial component of the semiconductor IP market, offering semiconductor companies the flexibility to integrate specific processor architectures into their custom-designed system-on-chips. This segment encompasses various licensing models, including single-use licensing, multiple-use licensing, and subscription-based options, catering to different customer needs. The licensing model is particularly vital for complex chip development projects requiring multiple inputs and specialized features, especially in emerging applications like IoT devices, automotive systems, and advanced computing platforms. The segment's importance is underscored by its role in enabling faster time-to-market and reduced development costs for semiconductor companies.

Segment Analysis: By IP Type

Processor IP Segment in Semiconductor (Silicon) Intellectual Property Market

The Processor IP segment continues to dominate the semiconductor intellectual property market, commanding approximately 50% of the total market share in 2024. This significant market position is driven by the increasing complexity of modern computing requirements and the growing demand for specialized processors in various applications. The segment's strength is particularly evident in emerging technologies like artificial intelligence, machine learning, and edge computing applications. Major technology companies are actively investing in processor IP development, especially for applications in data centers, automotive systems, and consumer electronics. The rise in adoption of System-on-Chip (SoC) designs and the growing need for energy-efficient processing solutions have further solidified the segment's market leadership.

Wired and Wireless Interface IP Segment in Semiconductor (Silicon) Intellectual Property Market

The Wired and Wireless Interface IP segment is experiencing the highest growth trajectory in the market, with an expected growth rate of approximately 7% during the forecast period 2024-2029. This accelerated growth is primarily driven by the rapid expansion of 5G infrastructure, increasing demand for high-speed data transfer capabilities, and the proliferation of IoT devices. The segment is witnessing substantial innovation in areas such as high-speed SerDes technology, PCIe interfaces, and wireless connectivity solutions. The growing adoption of advanced networking technologies in data centers, automotive electronics, and consumer devices is further fueling the segment's growth. Additionally, the increasing focus on developing efficient and reliable communication interfaces for next-generation electronic devices is creating new opportunities for market expansion.

Remaining Segments in IP Type Segmentation

The Other IP Types segment encompasses various specialized intellectual property solutions, including verification IP, analog IP, and mixed-signal IP cores. These components play a crucial role in enabling comprehensive semiconductor solutions for diverse applications. The segment's significance is particularly evident in areas such as power management, sensor interfaces, and signal processing applications. The increasing complexity of modern electronic systems has led to greater demand for specialized IP cores that can address specific functional requirements. The segment continues to evolve with new developments in areas such as security IP, memory controllers, and custom interface solutions, supporting the broader semiconductor ecosystem's growth and innovation.

Segment Analysis: By End-User Vertical

Consumer Electronics Segment in Semiconductor (Silicon) Intellectual Property Market

The Consumer Electronics segment continues to dominate the semiconductor (silicon) intellectual property market, commanding approximately 37% of the total market share in 2024. This significant market position is driven by the increasing integration of advanced semiconductor IP in smartphones, smartwatches, gaming consoles, and other consumer electronic devices. The segment's growth is particularly fueled by the rising demand for connected devices and the implementation of advanced technologies like 5G, AI, and IoT in consumer electronics. The expansion of smart home ecosystems, wearable technologies, and the continuous evolution of mobile devices has created a robust demand for sophisticated semiconductor IP solutions. Additionally, the increasing focus on power efficiency, miniaturization, and enhanced performance in consumer electronics has led to greater adoption of specialized IP cores and architectures designed specifically for these applications.

Automobile Segment in Semiconductor (Silicon) Intellectual Property Market

The Automobile segment is emerging as the fastest-growing segment in the semiconductor (silicon) IP market, with a projected growth rate of approximately 7% during 2024-2029. This remarkable growth is primarily driven by the increasing integration of advanced driver-assistance systems (ADAS), autonomous driving capabilities, and electric vehicle technologies. The automotive industry's rapid transition towards connected and autonomous vehicles has created an unprecedented demand for specialized semiconductor IP solutions. The segment's growth is further accelerated by the increasing complexity of in-vehicle infotainment systems, the adoption of advanced sensor technologies, and the growing emphasis on vehicle electrification. The integration of AI and machine learning capabilities in vehicles, combined with the need for high-performance computing solutions, continues to drive innovation in automotive-specific semiconductor IP designs.

Remaining Segments in End-User Vertical

The remaining segments in the market include Computers and Peripherals, Industrial, and Other End-user Verticals, each playing crucial roles in shaping the overall market landscape. The Computers and Peripherals segment continues to be driven by the growing demand for high-performance computing solutions, data centers, and cloud computing infrastructure. The Industrial segment is experiencing significant transformation with the adoption of Industry 4.0 technologies, industrial IoT, and smart manufacturing solutions. The Other End-user Verticals segment encompasses diverse applications across telecommunications, aerospace, defense, and healthcare sectors, contributing to the market's overall growth through specialized IP requirements for various applications. These segments collectively represent the diverse application landscape of semiconductor IP, each requiring unique solutions tailored to their specific needs and performance requirements.

Semiconductor (Silicon) Intellectual Property Market Geography Segment Analysis

Semiconductor (Silicon) Intellectual Property Market in North America

North America stands as a pivotal region in the global semiconductor IP market, driven by significant technological advancements and robust research and development activities. The United States and Canada form the core markets in this region, with both countries demonstrating strong capabilities in semiconductor IP development and implementation. The region's dominance is supported by the presence of major semiconductor IP vendors, advanced technological infrastructure, and substantial investments in emerging technologies like artificial intelligence, machine learning, and 5G communications.

Semiconductor (Silicon) Intellectual Property Market in the United States

The United States emerges as the dominant force in the North American semiconductor IP market, spearheading innovation and development across various applications. The country's semiconductor intellectual property ecosystem is characterized by robust research facilities, leading technology companies, and supportive government initiatives. The market's strength is evidenced by its approximately 50% share of the global semiconductor IP market in 2024. The country's leadership is further reinforced by the presence of major semiconductor IP companies and research institutions, particularly concentrated in technology hubs like Silicon Valley, which continue to drive innovation in areas such as artificial intelligence, data centers, and advanced computing applications.

Semiconductor (Silicon) Intellectual Property Market in Canada

Canada represents a rapidly evolving market within the North American semiconductor IP landscape, with a projected growth rate of approximately 5% during 2024-2029. The country's semiconductor IP sector is characterized by increasing investments in research and development, particularly in areas such as artificial intelligence and machine learning applications. Canada's market growth is supported by strong collaboration between academic institutions and industry players, creating an environment conducive to innovation and technological advancement. The country's focus on developing specialized semiconductor IP solutions for emerging technologies and its strategic initiatives to strengthen domestic semiconductor capabilities position it as a significant player in the North American market.

Semiconductor (Silicon) Intellectual Property Market in Europe

The European semiconductor IP market demonstrates a strong focus on innovation and technological advancement, with key contributions from the United Kingdom, Germany, France, and other European nations. The region's market is characterized by robust research and development activities, particularly in areas such as automotive electronics, industrial automation, and communications technology. European countries have shown significant commitment to strengthening their semiconductor capabilities through various initiatives and investments, fostering a competitive environment for semiconductor intellectual property development.

Semiconductor (Silicon) Intellectual Property Market in Germany

Germany stands as the largest semiconductor IP market in Europe, commanding approximately 12% of the regional market share in 2024. The country's strength lies in its advanced automotive sector, industrial automation capabilities, and strong research infrastructure. German semiconductor IP development is particularly focused on applications in automotive electronics, Industry 4.0, and industrial automation, supported by collaboration between research institutions and industry leaders. The country's robust manufacturing base and technological expertise continue to drive innovation in semiconductor IP development.

Semiconductor (Silicon) Intellectual Property Market in France

France emerges as the fastest-growing market in the European region, with a projected growth rate of approximately 6% during 2024-2029. The country's semiconductor IP sector is characterized by significant investments in research and development, particularly in areas such as artificial intelligence and telecommunications. France's market growth is driven by strong government support for technological innovation, the presence of leading research institutions, and an increasing focus on developing advanced semiconductor IP solutions. The country's strategic initiatives in semiconductor IP development and its growing ecosystem of technology companies position it as a key player in the European market.

Semiconductor (Silicon) Intellectual Property Market in Asia-Pacific

The Asia-Pacific region represents a dynamic and rapidly evolving market in the global semiconductor IP landscape, encompassing key markets such as China, Taiwan, Japan, South Korea, and India. The region's semiconductor IP ecosystem is characterized by strong manufacturing capabilities, increasing technological innovation, and growing domestic demand. The presence of major semiconductor foundries, particularly in Taiwan and South Korea, coupled with China's ambitious semiconductor development plans and India's emerging technology sector, creates a diverse and competitive semiconductor IP market environment.

Semiconductor (Silicon) Intellectual Property Market in China

China emerges as the largest semiconductor IP market in the Asia-Pacific region, driven by substantial investments in semiconductor technology and strong government support for domestic IP development. The country's semiconductor IP ecosystem is characterized by rapid technological advancement, particularly in areas such as 5G technology, artificial intelligence, and Internet of Things applications. China's market position is strengthened by its large domestic market, growing technological capabilities, and strategic focus on semiconductor independence.

Semiconductor (Silicon) Intellectual Property Market in India

India represents the fastest-growing market in the Asia-Pacific region, characterized by rapid expansion in semiconductor IP development and implementation. The country's growth is driven by increasing domestic demand, government initiatives supporting semiconductor development, and a strong focus on digital transformation. India's semiconductor IP sector benefits from its robust software expertise, growing electronics manufacturing ecosystem, and strategic partnerships with global technology leaders. The country's emergence as a key player in the semiconductor IP market is supported by initiatives to develop domestic semiconductor capabilities and attract international investments.

Semiconductor (Silicon) Intellectual Property Market in Rest of the World

The Rest of the World market, encompassing regions outside North America, Europe, and Asia-Pacific, demonstrates growing potential in the semiconductor IP sector. This market is characterized by increasing adoption of semiconductor technologies across various industries, particularly in emerging economies. The region shows particular strength in areas such as telecommunications infrastructure development and industrial automation applications. While the semiconductor IP market size remains smaller compared to other major regions, it presents significant opportunities for growth, particularly in countries focusing on digital transformation and technological advancement. The region's development is supported by increasing investments in semiconductor technologies and growing awareness of the importance of intellectual property in technological development.

Get Analysis on Important Geographic Markets

Download PDF

Semiconductor Silicon Intellectual Property (IP) Industry Overview

Top Companies in Semiconductor (Silicon) Intellectual Property Market

The semiconductor IP market is led by prominent players including ARM Holdings, Synopsys, Cadence Design Systems, Imagination Technologies, and CEVA Inc., who have established strong market positions through continuous innovation and strategic partnerships. These semiconductor IP companies are actively investing in research and development to expand their IP portfolios, particularly focusing on emerging technologies like artificial intelligence, 5G, automotive applications, and the Internet of Things (IoT). The industry witnesses frequent collaborations between semiconductor IP vendors and semiconductor manufacturers to optimize process nodes and develop comprehensive solutions. Companies are increasingly adopting platform-based approaches and automated IP customization services to accelerate time-to-market for their customers. Strategic acquisitions and licensing agreements have become common as companies seek to enhance their technological capabilities and expand their geographic presence. Market leaders are also focusing on developing specialized IP solutions for specific applications while maintaining flexibility in their business models to accommodate both license fees and royalty-based revenue streams.

Dynamic Market Structure Drives Industry Evolution

The semiconductor intellectual property market exhibits a relatively consolidated structure, with global technology conglomerates holding significant market share alongside specialized IP providers. These dominant players have established strong barriers to entry through their extensive patent portfolios, long-standing customer relationships, and sophisticated technological capabilities. The market has witnessed numerous strategic mergers and acquisitions as companies seek to expand their IP portfolios, enhance their technological capabilities, and strengthen their market positions. Large semiconductor companies are increasingly pursuing vertical integration strategies, developing in-house IP capabilities while maintaining relationships with external IP providers.

The industry landscape is characterized by a mix of pure-play IP providers and diversified technology companies that offer both IP and related services. Regional players, particularly in Asia, are gaining prominence as the semiconductor manufacturing base continues to shift eastward. The market structure is further influenced by the increasing complexity of semiconductor designs and the growing need for specialized IP solutions across different application domains. Companies are forming strategic alliances and partnerships to share development costs and risks while expanding their market reach through cross-licensing agreements and joint development initiatives.

Innovation and Adaptability Drive Market Success

Success in the IP industry increasingly depends on companies' ability to anticipate and adapt to rapidly evolving technological requirements while maintaining strong customer relationships. Incumbent players must continuously invest in research and development to expand their IP portfolios, particularly in emerging technologies like AI, 5G, and autonomous systems. Companies need to develop flexible licensing models that accommodate different customer needs while ensuring proper IP protection and compliance with industry standards. The ability to provide comprehensive support services, including design optimization, verification, and integration assistance, has become crucial for maintaining market position.

Market contenders can gain ground by focusing on specialized niches where they can develop unique expertise and differentiated offerings. Success factors include developing strong partnerships with foundries and semiconductor manufacturers, establishing efficient IP verification and quality assurance processes, and building robust customer support capabilities. Companies must also navigate the complex regulatory landscape surrounding IP protection and licensing while managing the risk of IP infringement and maintaining compliance with export control regulations. The increasing concentration of end-users in specific geographic regions and industries requires companies to develop targeted market entry strategies and establish a strong local presence in key markets.

Semiconductor Silicon Intellectual Property (IP) Market Leaders

-

Faraday Technology Corporation

-

Fujitsu Ltd

-

LTIMindtree Limited

-

ARM Ltd (SoftBank )

-

Synopsys Inc.

- *Disclaimer: Major Players sorted in no particular order

_Intellectual_Property_Market_competive_lanscape_12.webp)

Need More Details on Market Players and Competiters?

Download PDF

Semiconductor Silicon Intellectual Property (IP) Market News

- May 2023: CEVA Inc. announced the acquisition of the RealSpace 3D Spatial Audio business, technology, and patents from VisiSonicsCorporation. Based in Maryland, close to CEVA's sensor fusion R&D development center, the VisiSonicsspatial audio R&D team and software expand the Company's application software portfolio for embedded systems, bolstering CEVA's strong market position in wearables, where spatial audio is fast becoming a must-have component.

- March 2023: Synopsys launched a groundbreaking suite of AI-powered electronic design automation tools that spans the entire chip design process, from architecture to manufacturing. Known as the Synopsys.ai suite, it offers the potential to reduce development time significantly, cut costs, enhance performance, and improve yields. These tools are precious for chip designs targeting advanced nodes like 5 nm, 3 nm, two nm-class, and beyond.

Semiconductor Silicon Intellectual Property (IP) Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 An Assessment of the Impact of Key Macro Trends

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growing Demand for Connected Devices

- 5.1.2 Growing Demand for Modern SoC Designs

-

5.2 Market Restraints

- 5.2.1 IP Business Model and Economies of Scale

6. MARKET SEGMENTATION

-

6.1 By Revenue Type

- 6.1.1 License

- 6.1.2 Royalty

- 6.1.3 Services

-

6.2 By IP Type

- 6.2.1 Processor IP

- 6.2.2 Wired and Wireless Interface IP

- 6.2.3 Other IP Types

-

6.3 By End-user Vertical

- 6.3.1 Consumer Electronics

- 6.3.2 Computers and Peripherals

- 6.3.3 Automobile

- 6.3.4 Industrial

- 6.3.5 Other End-user Verticals

-

6.4 By Geography

- 6.4.1 North America

- 6.4.1.1 United States

- 6.4.1.2 Canada

- 6.4.2 Europe

- 6.4.2.1 United Kingdom

- 6.4.2.2 Germany

- 6.4.2.3 France

- 6.4.3 Asia

- 6.4.3.1 China

- 6.4.3.2 Taiwan

- 6.4.3.3 Japan

- 6.4.3.4 South Korea

- 6.4.3.5 India

- 6.4.3.6 Australia and New Zealand

- 6.4.3.7

- 6.4.4 Latin America

- 6.4.5 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Faraday Technology Corporation

- 7.1.2 Fujitsu Ltd

- 7.1.3 LTIMindtree Limited

- 7.1.4 ARM Ltd (SoftBank )

- 7.1.5 Synopsys Inc.

- 7.1.6 Cadence Design Systems Inc.

- 7.1.7 CEVA Inc.

- 7.1.8 Andes Technology Corporation

- 7.1.9 MediaTek Inc.

- 7.1.10 Digital Media Professionals

- 7.1.11 Imagination Technologies Ltd

- 7.1.12 VeriSilicon Holdings Co., Ltd

- 7.1.13 Achronix Semiconductor Corporation

- 7.1.14 Rambus Incorporated

- 7.1.15 eMemory Technology Inc.

- 7.1.16 MIPS Tech, LLC

- 7.2 Vendor Market Share

8. INVESTMENT ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Semiconductor Silicon Intellectual Property (IP) Industry Segmentation

A semiconductor intellectual property (IP) core is a reclaimable logic, functional unit, cell, or layout design typically licensed to multiple vendors as building blocks in different chip designs. In today’s IC design era, more and more system functionality is integrated into single chips (system-on-chip/SOC designs). These pre-designed IP cores/blocks are becoming increasingly important in these SOC designs. This is because most of the SOC designs have a standard microprocessor and a lot of system functionality, which are standardized and hence can be re-used across several designs if designed once.

The semiconductor (silicon) intellectual property market is segmented by revenue type (license, royalty, and services), IP type (processor IP, wired & wireless interface IP, and other IP types), end-user vertical (consumer electronics, computers & peripherals, automobile, industrial, and other end-user verticals), and geography (North America (United States, Canada), Europe (United Kingdom, Germany, France, Rest of Europe), Asia Pacific (China, Taiwan, Japan, South Korea, India) Rest of Asia Pacific), and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Revenue Type | License | ||

| Royalty | |||

| Services | |||

| By IP Type | Processor IP | ||

| Wired and Wireless Interface IP | |||

| Other IP Types | |||

| By End-user Vertical | Consumer Electronics | ||

| Computers and Peripherals | |||

| Automobile | |||

| Industrial | |||

| Other End-user Verticals | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Asia | China | ||

| Taiwan | |||

| Japan | |||

| South Korea | |||

| India | |||

| Australia and New Zealand | |||

| Latin America | |||

| Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Semiconductor Silicon Intellectual Property (IP) Market Research FAQs

What is the current Semiconductor (Silicon) Intellectual Property Market size?

The Semiconductor (Silicon) Intellectual Property Market is projected to register a CAGR of 7.38% during the forecast period (2025-2030)

Who are the key players in Semiconductor (Silicon) Intellectual Property Market?

Faraday Technology Corporation, Fujitsu Ltd, LTIMindtree Limited, ARM Ltd (SoftBank ) and Synopsys Inc. are the major companies operating in the Semiconductor (Silicon) Intellectual Property Market.

Which is the fastest growing region in Semiconductor (Silicon) Intellectual Property Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Semiconductor (Silicon) Intellectual Property Market?

In 2025, the North America accounts for the largest market share in Semiconductor (Silicon) Intellectual Property Market.

What years does this Semiconductor (Silicon) Intellectual Property Market cover?

The report covers the Semiconductor (Silicon) Intellectual Property Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Semiconductor (Silicon) Intellectual Property Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Semiconductor (Silicon) Intellectual Property Market Research

Mordor Intelligence provides a comprehensive analysis of the semiconductor intellectual property market. We leverage our extensive experience in semiconductor IP research and consulting. Our latest report examines the evolving landscape of silicon intellectual property and the dynamics of the interface IP market. It offers detailed coverage of semiconductor IP vendors and their IP licensing models. The analysis includes crucial developments in IP cores and emerging trends in semiconductor chip design. This information is available in an easy-to-download report PDF format.

The report offers stakeholders actionable insights into the SIP market value and IP market size. This enables informed decision-making in this rapidly evolving sector. Our comprehensive analysis includes a detailed examination of semiconductor IP companies and their technological innovations. It also provides precise SIP growth rate forecasts and market data. The report is particularly beneficial for investors and industry leaders. It offers deep insights into IP industry trends and developments in semiconductor silicon intellectual property. These insights are supported by robust market forecast methodologies and expert analysis of IP semiconductor dynamics.