Market Size of Global Semiconductor Front-end Equipment Industry

| Study Period | 2019 - 2029 |

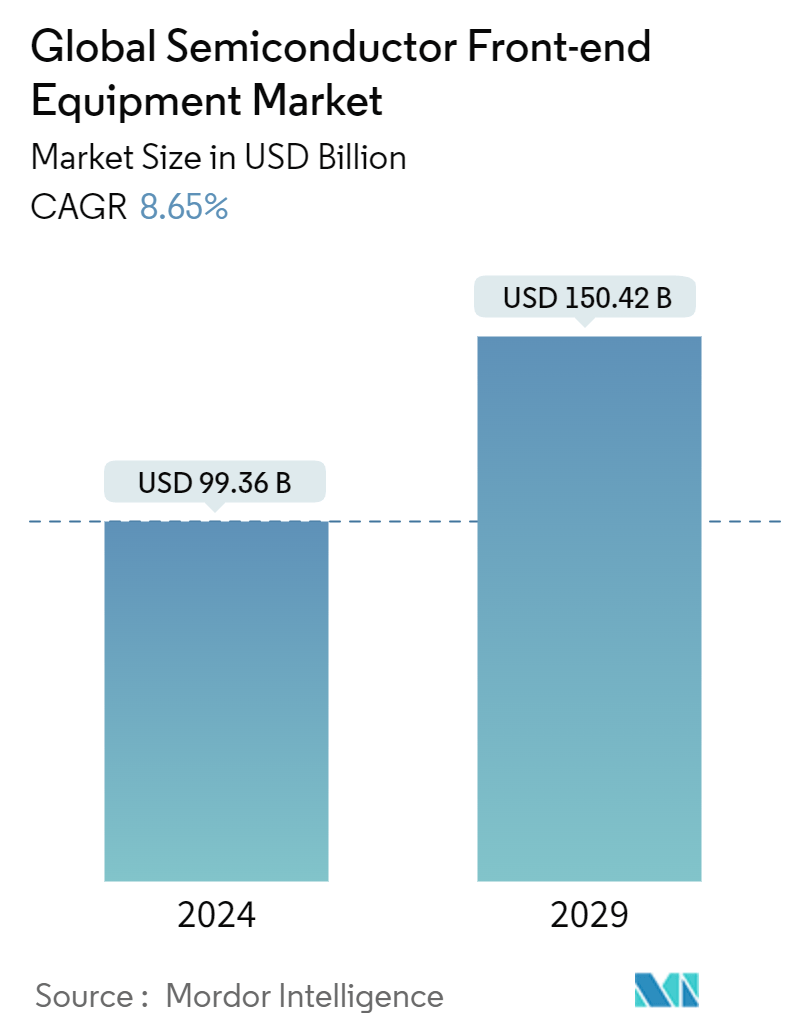

| Market Size (2024) | USD 99.36 Billion |

| Market Size (2029) | USD 150.42 Billion |

| CAGR (2024 - 2029) | 8.65 % |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Semiconductor Front-End Equipment Market Analysis

The Global Semiconductor Front-end Equipment Market size is estimated at USD 99.36 billion in 2024, and is expected to reach USD 150.42 billion by 2029, growing at a CAGR of 8.65% during the forecast period (2024-2029).

The front-end procedure necessitates a multitude of intricate phases to convert a wafer into a completed device. These steps incorporate wafer cleaning, oxidation, and photolithography to pattern devices, along with etching, deposition, doping, and metallization steps. Inspection and metrology equipment is utilized for process control. This is when the wafers are inspected to identify irregularities that potentially induce issues with the end product. In addition to this, optical techniques are also used, and e-beam inspection is often needed to find the smallest defects.

- The demand for semiconductor front-end equipment is expected to observe a noteworthy surge as some of the major front-end equipment-producing companies observed record-breaking revenue against a backdrop of a downturn in the semiconductor industry instead of the mild and short-term correction. It was driven by capacity expansion, new fab projects, and high demand for advanced technologies and solutions across the front-end equipment market.

- After registering a record of significant sales last year, the wafer fab equipment, which includes wafer processing, fab facilities, and mask/reticle equipment, is projected to be a bit low in 2023, and this contraction marks a significant improvement. The upward revision is primarily due to China's strong equipment spending. The market grew managing uncertainties created by geopolitical challenges, including the US and Dutch governments' export control regulations and global macro concerns around inflation, rising interest rates, and lower GDP growth in certain economies.

- Consumer electronics is the fastest-growing segment, contributing to market expansion. The use of smartphones, anticipated to rise with population growth, is the key driver of this market. Consumer electronics drive the industry due to increased demand for tablets, smartphones, laptops, computers, and wearable gadgets. As semiconductors advance, new market areas, such as machine learning, are rapidly being integrated.

- The most fascinating "must-win" technologies of the future, such as artificial intelligence, the Internet of Things, quantum computing, and enhanced wireless networks, are currently supported by semiconductors. Semiconductors and microelectronics are advancing to satisfy the complicated demands of a constantly changing digital environment as the world seamlessly integrates breakthrough technology into every aspect of life. Big Data and AI drive this increase and call for smaller, more powerful chips, making their production more difficult and increasing the need for technological innovation.

- Rapid advancements in data storage, computing power, and algorithms have enabled the development and deployment of AI systems. The increased use of digital devices and the Internet has generated extensive volumes of data. AI systems rely on large datasets to train and improve their performance.

- The Internet of Things (IoT), big data, cloud manufacturing, cyber-physical systems (CPS), the Internet of Services (IoS), robotics, augmented reality, and other emerging technologies are included in the Industry 4.0 idea. Creating additional smart industrial processes depends on adopting these technologies, which will unite the physical and digital worlds by encompassing several future industrial advancements.

- As global work-from-home trends gain momentum, the demand for cloud services surges, prompting data center providers to expand their capacities. This, in turn, fuels the global appetite for chips and memory. SEMI reports a notable uptick in investments in 300 mm fabs. Projections suggest that the industry will witness the addition of a minimum of 38 new 300 mm fabs between 2020 and 2024.

- This surge is set to boost the capacity by approximately 1.8 million wafers, pushing the total beyond 7 million. Notably, Taiwan is slated to host 11 of these new volume fabs, with China following closely with eight. Additionally, TSMC is in the process of constructing a new 300 mm fab in Arizona. By the close of 2024, the tally of 300 mm volume fabs is anticipated to hit a significant 161 units.

Semiconductor Front-End Equipment Industry Segmentation

The front end and back end are two ways to separate semiconductor processes. Creating a finished wafer from a blank wafer is known as front-end semiconductor manufacturing. The wafer is spun during several front-end procedures. The front end involves fabricating silicon wafers, photolithography, deposition, etching, ion implantation, and mechanical polishing devices.

The semiconductor front-end equipment market is segmented by type (lithography equipment, etching equipment, deposition equipment, and other equipment types), end-user industry (semiconductor fabrication plant and semiconductor electronics manufacturing), and geography (United States, Europe, China, South Korea, Taiwan, Japan, Rest of Asia-Pacific, and Rest of The World). The report offers market forecasts and size in USD for all the above segments.

| By Type | |

| Lithography Equipment | |

| Etching Equipment | |

| Deposition Equipment | |

| Other Equipment Types |

| By End-user Industry | |

| Semiconductor Fabrication Plant | |

| Semiconductor Electronics Manufacturing |

| By Geography*** | |

| United States | |

| Europe | |

| China | |

| South Korea | |

| Taiwan | |

| Japan | |

| Latin America | |

| Middle East and Africa |

Global Semiconductor Front-end Equipment Market Size Summary

The semiconductor front-end equipment market is poised for significant growth, driven by the complex processes involved in transforming wafers into finished devices. This market encompasses various stages such as wafer cleaning, oxidation, photolithography, etching, deposition, doping, and metallization, with inspection and metrology equipment playing a crucial role in ensuring process control. The demand for these equipment is expected to surge due to capacity expansions, new fabrication projects, and the increasing need for advanced technologies. Despite challenges like geopolitical tensions and economic uncertainties, the market has shown resilience, with substantial investments in new fabs and equipment, particularly in regions like China, Taiwan, and the United States. The consumer electronics sector, fueled by the rising use of smartphones and other digital devices, is a key driver of this market expansion.

The market landscape is characterized by the presence of major players such as Applied Materials, ASML Holding, Tokyo Electron, LAM Research, and KLA Corporation, who are actively engaging in partnerships, innovations, and acquisitions to strengthen their market position. The industry is also witnessing a shift towards emerging technologies like artificial intelligence, the Internet of Things, and quantum computing, which are increasingly reliant on advanced semiconductors. As these technologies evolve, they demand smaller, more powerful chips, thereby driving the need for technological advancements in semiconductor fabrication. The market's growth is further supported by the expansion of cloud services and data centers, which are boosting the demand for chips and memory. Overall, the semiconductor front-end equipment market is set to experience robust growth, supported by technological innovations and strategic investments in fabrication capabilities.

Global Semiconductor Front-end Equipment Market Size - Table of Contents

-

1. MARKET INSIGHTS

-

1.1 Market Overview

-

1.2 Industry Attractiveness - Porter's Five Forces Analysis

-

1.2.1 Bargaining Power of Suppliers

-

1.2.2 Bargaining Power of Buyers

-

1.2.3 Threat of New Entrants

-

1.2.4 Threat of Substitute Products

-

1.2.5 Degree of Competition

-

-

1.3 Industry Value Chain Analysis

-

1.4 Impact of COVID-19 Pandemic on the Market

-

-

2. MARKET SEGMENTATION

-

2.1 By Type

-

2.1.1 Lithography Equipment

-

2.1.2 Etching Equipment

-

2.1.3 Deposition Equipment

-

2.1.4 Other Equipment Types

-

-

2.2 By End-user Industry

-

2.2.1 Semiconductor Fabrication Plant

-

2.2.2 Semiconductor Electronics Manufacturing

-

-

2.3 By Geography***

-

2.3.1 United States

-

2.3.2 Europe

-

2.3.3 China

-

2.3.4 South Korea

-

2.3.5 Taiwan

-

2.3.6 Japan

-

2.3.7 Latin America

-

2.3.8 Middle East and Africa

-

-

Global Semiconductor Front-end Equipment Market Size FAQs

How big is the Global Semiconductor Front-end Equipment Market?

The Global Semiconductor Front-end Equipment Market size is expected to reach USD 99.36 billion in 2024 and grow at a CAGR of 8.65% to reach USD 150.42 billion by 2029.

What is the current Global Semiconductor Front-end Equipment Market size?

In 2024, the Global Semiconductor Front-end Equipment Market size is expected to reach USD 99.36 billion.