| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 107.95 Billion |

| Market Size (2030) | USD 163.45 Billion |

| CAGR (2025 - 2030) | 8.65 % |

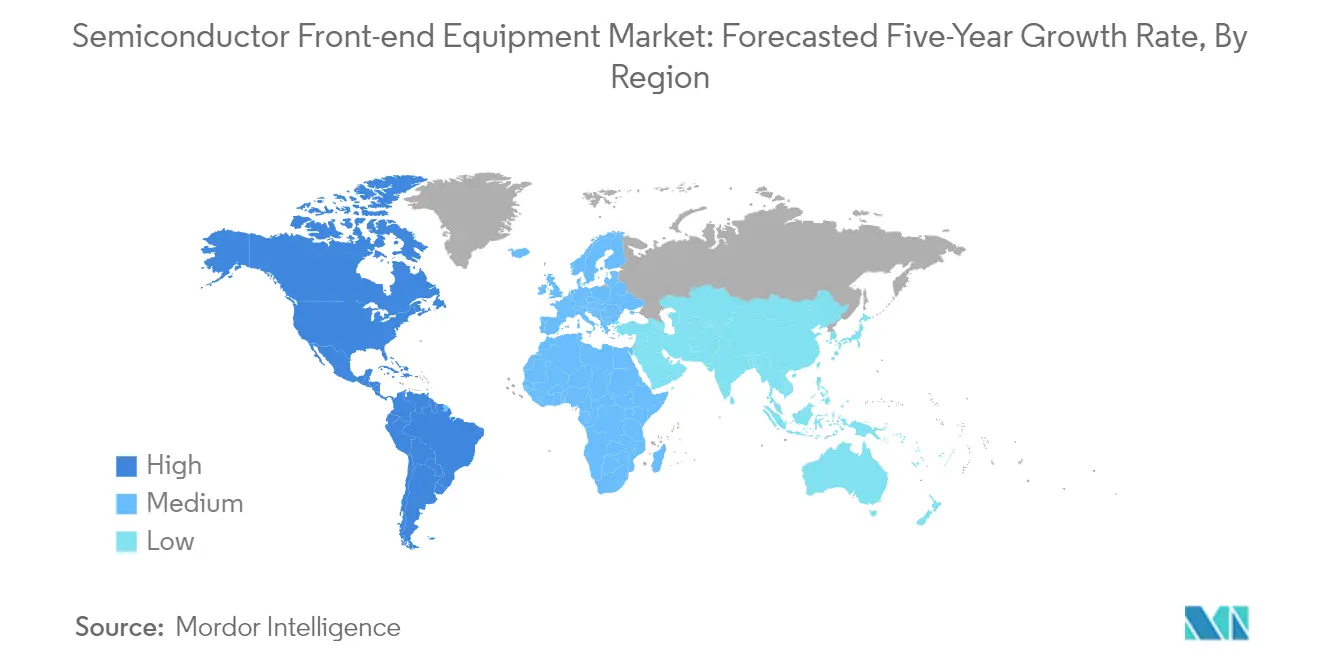

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

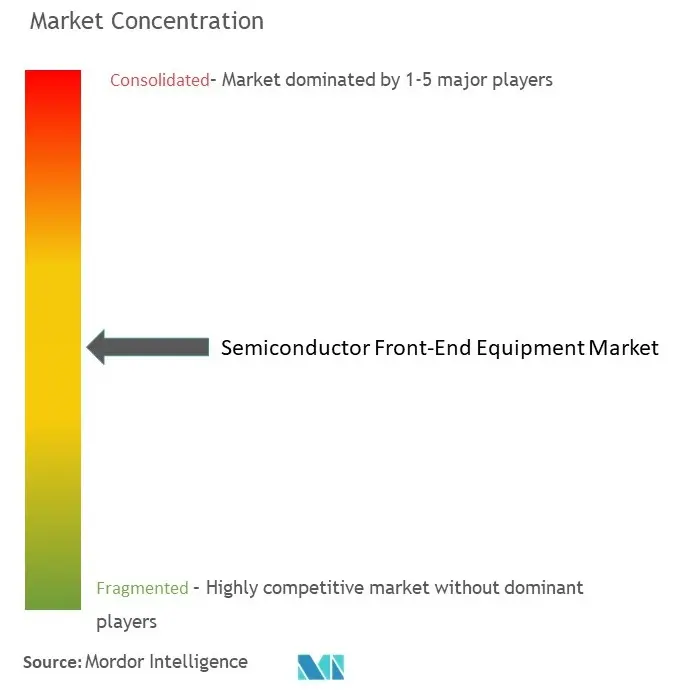

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Semiconductor Front-End Equipment Market Analysis

The Semiconductor Front End Equipment Market size is estimated at USD 107.95 billion in 2025, and is expected to reach USD 163.45 billion by 2030, at a CAGR of 8.65% during the forecast period (2025-2030).

The semiconductor front-end equipment industry is experiencing significant transformation driven by geopolitical dynamics and technological advancements. Major semiconductor equipment manufacturers are adapting to new export control regulations implemented by the US and Dutch governments while managing global macro concerns around inflation and interest rates. This has led to a notable shift in supply chains, exemplified by China's substantial equipment procurement in November 2023, including 42 lithography systems worth USD 816.8 million, with 16 systems from the Netherlands alone marking a tenfold increase from the previous year. The industry's resilience is evident in its ability to maintain growth despite these regulatory challenges.

The market is witnessing unprecedented levels of investment in manufacturing capabilities and infrastructure. Intel's collaboration with the German government for a EUR 30 billion investment in a leading-edge wafer fabrication site in Magdeburg and Samsung's USD 17 billion commitment to build a semiconductor fabrication plant in Austin, Texas, demonstrate the industry's focus on geographical diversification. These investments are complemented by technological advancements, particularly in lithography equipment, with companies acquiring next-generation tools like high-NA EUV lithography machines to compete at advanced nodes like 2nm.

The rollout of 5G infrastructure continues to be a significant driver for semiconductor production equipment demand. Germany leads the European Union in 5G deployment with approximately 90,000 base stations installed as of 2023, highlighting the growing infrastructure requirements. The industry is also adapting to support emerging technologies like Wi-Fi 6, requiring more sophisticated manufacturing equipment for producing advanced chips. This technological evolution is pushing manufacturers to develop more precise and efficient front-end semiconductor manufacturing equipment.

Regional dynamics are reshaping the industry landscape, with countries focusing on building domestic semiconductor capabilities. China's strategic push into semiconductor manufacturing is evident in developments like Shanghai Micro Electronics Equipment Group's introduction of its first 28nm-class process technology-capable lithography machine. The electric vehicle sector is emerging as a significant demand driver, with China alone reporting sales of approximately 846,000 new energy vehicles in August 2023. These trends are prompting equipment manufacturers to enhance their product portfolios to meet diverse manufacturing requirements across different technology nodes.

Semiconductor Front-End Equipment Market Trends

Increasing Needs of Consumer Electronic Devices Boosting Manufacturing Prospects

The proliferation of consumer electronics is driving unprecedented demand for semiconductor manufacturing equipment. The expansion of smartphones, which is predicted to increase with population growth, serves as the primary catalyst for market growth. The industry is experiencing increased demand across various product categories, including tablets, smartphones, laptop computers, and wearable devices. As semiconductor technology advances, new market areas such as machine learning are being rapidly integrated, requiring more sophisticated manufacturing equipment.

The integration of semiconductors in various consumer devices has become more complex and sophisticated. According to Cisco, the growth in connected wearable devices, from 835 million devices in 2020 to 1,105 million in 2022, demonstrates the expanding market potential, particularly in healthcare applications. Sensors and ICs are gaining momentum in smart home devices such as smart refrigerators, microwaves, washing machines, televisions, and others. The rising urban population and changing consumer buying behavior drive the demand for smart home appliances, which in turn fuels the need for more sophisticated front-end manufacturing equipment capable of handling new materials, processes, and specifications.

Understand The Key Trends Shaping This Market

Download PDF

Proliferation of AI, IoT, and Connected Devices Across Industry Verticals

The convergence of artificial intelligence, the Internet of Things, and connected devices is revolutionizing semiconductor manufacturing requirements. According to Ericsson, the number of connected devices worldwide is set to almost double between 2022 and 2028, primarily driven by an increase in short-range IoT devices, with 28.72 billion such devices forecast by 2028. This explosive growth in connected devices demands more sophisticated and powerful semiconductors, driving the need for advanced semiconductor capital equipment industry capable of producing increasingly complex chips.

The semiconductor industry is evolving rapidly to create "smart everything" product lines, requiring new production sophistication, excellent responsiveness, greater component reliability, and maximum precision. Several tech companies are making significant investments in AI capabilities, exemplified by Amazon's USD 4 billion investment in Anthropic in September 2023, and Wipro's announcement of a USD 1 billion investment in artificial intelligence over three years. These investments are driving demand for more advanced semiconductor manufacturing equipment capable of producing chips that can support AI applications. The integration of semiconductors in data centers further supports the sector's growth through artificial intelligence, with data centers being outfitted with AI chips to enhance efficiency and lower operational expenses.

Segment Analysis: By Type

Lithography Equipment Segment in Semiconductor Front-end Equipment Market

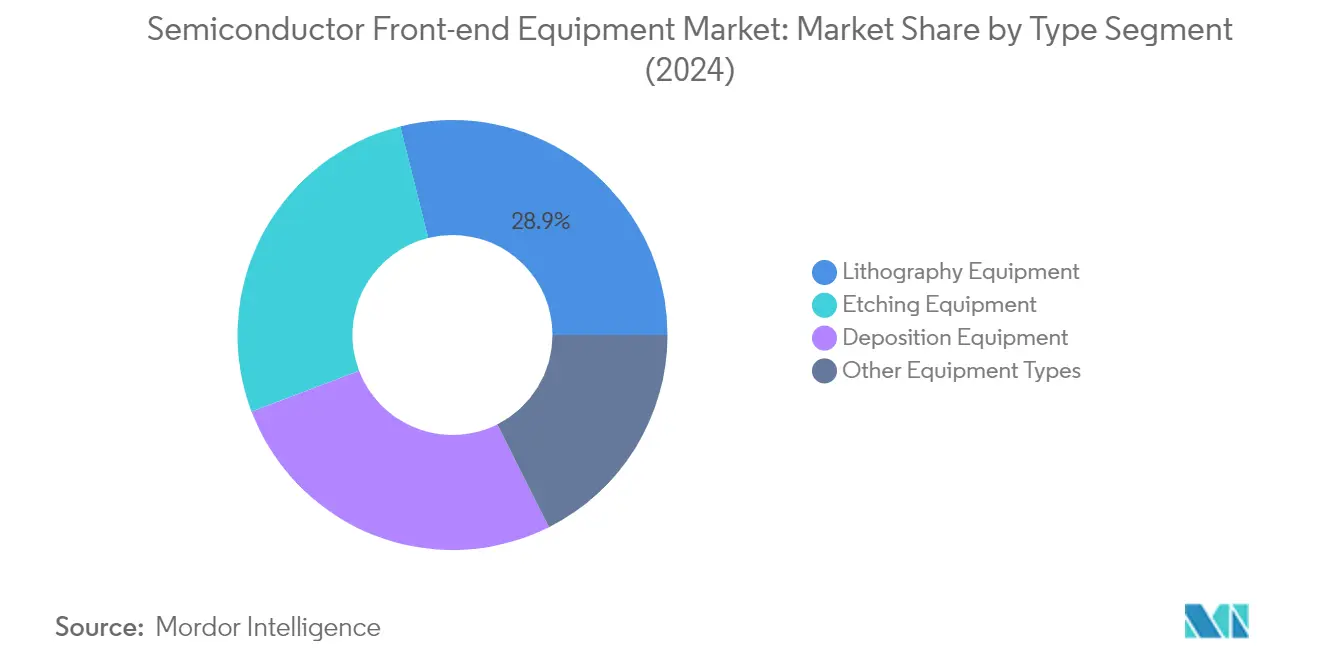

The semiconductor lithography equipment segment dominates the global semiconductor front-end equipment market, commanding approximately 29% of the total market share in 2024. This segment's prominence is driven by its crucial role in semiconductor manufacturing, where it enables the drawing of highly complex circuit patterns on photomasks using ultra-high-performance lenses. The segment is experiencing robust growth, projected to grow at around 10% through 2029, the highest among all segments. This growth is primarily fueled by the increasing demand for advanced semiconductor manufacturing processes, particularly in EUV (Extreme Ultraviolet) lithography technology. Major players like ASML, Canon, and Nikon continue to innovate in this space, with developments in high-NA EUV technology and next-generation lithography systems driving the segment's expansion. The segment's leadership position is further strengthened by the critical role lithography plays in enabling smaller feature sizes and more complex chip designs required for emerging technologies like AI, 5G, and advanced computing applications.

Remaining Segments in Semiconductor Front-end Equipment Market

The remaining segments in the semiconductor front-end equipment market include semiconductor etching equipment, semiconductor deposition equipment, and other equipment types, each playing vital roles in the semiconductor manufacturing process. Semiconductor etching equipment, essential for removing material from semiconductor surfaces to create various patterns, represents a significant portion of the market. Semiconductor deposition equipment, crucial for applying blanket materials on wafer surfaces, continues to evolve with advanced techniques like atomic layer deposition and chemical vapor deposition. The other equipment types category, which includes semiconductor cleaning equipment, ion implanters, and process control equipment, provides critical support functions in the semiconductor manufacturing process. These segments collectively contribute to the advancement of semiconductor manufacturing capabilities, enabling the production of increasingly sophisticated and powerful semiconductor devices.

Segment Analysis: By End-User Industry

Semiconductor Fabrication Plant Segment in Global Semiconductor Front-end Equipment Market

The semiconductor fab equipment segment dominates the global semiconductor front-end equipment market, commanding approximately 79% of the total market share in 2024. This segment's prominence is driven by the increasing complexity of semiconductor manufacturing processes and the growing demand for advanced chip fabrication capabilities. The segment encompasses both integrated device manufacturers (IDMs) that manufacture chips based on their designs and foundries that operate independently to manufacture chips for third-party customers. Major players like TSMC, Samsung, and Intel are making substantial investments in new fabrication facilities and expanding their existing capabilities to meet the rising demand for semiconductors across various applications. The segment's growth is further supported by government initiatives worldwide to strengthen domestic semiconductor manufacturing capabilities, particularly in regions like the United States, Europe, and Asia. Additionally, the increasing adoption of advanced technologies such as 5G, artificial intelligence, and the Internet of Things (IoT) continues to drive the demand for sophisticated fabrication equipment in semiconductor manufacturing plants.

Semiconductor Electronics Manufacturing Segment in Global Semiconductor Front-end Equipment Market

The semiconductor electronics manufacturing segment represents a crucial component of the semiconductor front-end equipment market, focusing on the production of electronic devices and components. This segment is experiencing steady growth driven by the increasing integration of semiconductors in modern electronics and the rising demand for connected devices. The segment's expansion is supported by the growing adoption of advanced manufacturing technologies and the increasing complexity of electronic devices. Companies in this segment are actively investing in upgrading their manufacturing capabilities to meet the evolving demands of the electronics industry, particularly in areas such as smartphones, tablets, wearables, and other consumer electronics. The segment is also benefiting from the increasing focus on self-sustainability in the supply chain, with many electronic manufacturers investing in their semiconductor manufacturing facilities to reduce dependence on external suppliers.

Global Semiconductor Front-end Equipment Market Geography Segment Analysis

Semiconductor Front-end Equipment Market in China

China continues to dominate the global semiconductor equipment market, commanding approximately 27% of the global semiconductor equipment market share in 2024. The country's semiconductor industry has shown remarkable resilience despite international trade restrictions, particularly in lithography equipment procurement. Chinese manufacturers are actively working to enhance their self-dependency in semiconductor fabrication equipment manufacturing, with significant investments in research and development. Companies like Shanghai Micro Electronics Equipment Group (SMEE) have made substantial progress, introducing advanced lithography machines capable of processing wafers using cutting-edge technology. The Chinese government's commitment to achieving semiconductor self-sufficiency has led to substantial investments in domestic chip production capabilities. Local manufacturers are increasingly focusing on higher-node chips with various applications in emerging industries, particularly electric vehicles. The growing emphasis on domestic production capabilities, coupled with government initiatives and increasing investments by local vendors, has created a robust ecosystem for the front-end semiconductor market in China.

Semiconductor Front-end Equipment Market in United States

The United States semiconductor equipment market is projected to experience robust growth with a CAGR of approximately 11% during 2024-2029. The country's strategic focus on rebuilding its semiconductor manufacturing capabilities has been driven by both public and private sector initiatives. The implementation of the CHIPS Act has catalyzed significant investments in domestic semiconductor manufacturing equipment infrastructure. American companies maintain a strong position across the semiconductor value chain, particularly in electronic design automation tools, intellectual property cores, integrated circuit design, and manufacturing equipment. The presence of major equipment manufacturers like Applied Materials, Lam Research, and KLA Corporation in Silicon Valley continues to drive innovation in the sector. The increasing adoption of artificial intelligence technologies and the Department of State's active role in establishing international policy frameworks for AI development have further strengthened the market's growth prospects. The robust demand for consumer electronics and the widespread adoption of 5G technology have created additional momentum for market expansion.

Semiconductor Front-end Equipment Market in Taiwan

Taiwan maintains its position as a crucial hub in the global semiconductor capital equipment landscape, supported by its comprehensive ecosystem of wafer fabrication companies and foundries. The country's semiconductor industry benefits from the presence of major players like TSMC, UMC, and numerous other manufacturers. The establishment of advanced research centers and manufacturing facilities has strengthened Taiwan's position in the market. The country's expertise in semiconductor manufacturing has attracted significant investments from global equipment manufacturers, with companies like Lam Research establishing research centers dedicated to advanced nodes. Taiwan's domestic supply chain is increasingly contributing to customized equipment, modules, and precision machining, particularly in emerging application areas like third-generation compound semiconductors and energy efficiency solutions. The collaboration between Taiwanese equipment suppliers and international chip manufacturers has created a robust network that continues to drive innovation and technological advancement in the sector.

Semiconductor Front-end Equipment Market in South Korea

South Korea's semiconductor equipment company ranking is characterized by strong government support and strategic investments from major electronics firms. The country's ambitious plans to construct the world's largest semiconductor cluster in Gyeonggi Province demonstrate its commitment to maintaining its competitive position. The collaboration between government initiatives and private sector investments, particularly from companies like Samsung Electronics and SK Hynix, has created a robust ecosystem for semiconductor manufacturing. The country's focus on achieving self-reliance in crucial chip manufacturing materials, components, and machinery has spurred significant developments in the front-end equipment sector. The establishment of advanced research and development facilities, coupled with strategic partnerships with international equipment manufacturers, has positioned South Korea as a key player in the global semiconductor equipment market. The country's emphasis on developing cutting-edge technologies and improving manufacturing capabilities continues to attract investments and drive innovation in the sector.

Semiconductor Front-end Equipment Market in Other Countries

The semiconductor front-end equipment market in other regions shows varying degrees of development and potential. Japan maintains its significant position in producing semiconductor manufacturing equipment, with companies like Tokyo Electron and Hitachi High-Technologies driving innovation. European countries, particularly the Netherlands and Germany, are strengthening their position through strategic investments and partnerships in advanced semiconductor manufacturing capabilities. Emerging markets in the Asia-Pacific region, including India, Malaysia, and Vietnam, are showing increasing potential in the semiconductor manufacturing landscape. These countries are developing their capabilities through government initiatives and international collaborations. The Middle East, particularly the UAE, is emerging as a potential hub for semiconductor innovation, while Latin American countries like Brazil and Costa Rica are gradually developing their semiconductor ecosystems through strategic partnerships and investments. This diverse geographical spread of semiconductor manufacturing capabilities indicates the industry's ongoing globalization and the emergence of new regional players in the market.

Get Analysis on Important Geographic Markets

Download PDF

Semiconductor Front-End Equipment Industry Overview

Top Companies in Semiconductor Front-end Equipment Market

The semiconductor equipment companies market is dominated by established players, including Applied Materials, ASML Holding, Tokyo Electron, Lam Research, and KLA Corporation, who collectively shape industry dynamics through continuous innovation and strategic initiatives. These semiconductor manufacturing equipment companies demonstrate a strong commitment to research and development, evidenced by substantial investments in advancing technologies like EUV lithography, atomic layer deposition, and plasma etching solutions. Market leaders are actively expanding their global footprint through strategic facility investments across Asia, Europe, and North America, while simultaneously strengthening their service networks to support an expanding customer base. The industry witnesses ongoing collaboration between equipment manufacturers and semiconductor fabrication companies to develop next-generation solutions, particularly focusing on emerging technologies like AI, 5G, and IoT applications. Companies are increasingly emphasizing sustainable manufacturing practices and automated solutions while building resilient supply chains through strategic partnerships and localized production capabilities.

High Consolidation with Strong Regional Presence

The semiconductor front-end equipment market exhibits a highly consolidated structure dominated by global conglomerates with sophisticated technological capabilities and extensive manufacturing networks. These major players have established strong regional presences, particularly in key semiconductor manufacturing hubs across the Asia Pacific, North America, and Europe, while maintaining significant research and development facilities in multiple locations to serve local markets effectively. The industry's high entry barriers, including substantial capital requirements, complex technological expertise, and established customer relationships, have contributed to market concentration among a few key players who have built their positions through decades of innovation and strategic investments.

The market demonstrates active merger and acquisition activity, primarily focused on expanding technological capabilities and strengthening market presence in emerging semiconductor manufacturing regions. Leading semiconductor equipment companies are pursuing strategic acquisitions to enhance their product portfolios, particularly in advanced processing technologies and specialized equipment segments. The industry also witnesses strategic partnerships and joint ventures between equipment manufacturers and semiconductor companies, creating integrated ecosystems that support technological advancement and market expansion while addressing the growing complexity of semiconductor manufacturing processes.

Innovation and Adaptability Drive Market Success

Success in the semiconductor front-end equipment market increasingly depends on companies' ability to innovate and adapt to rapidly evolving technological requirements while maintaining operational efficiency. Market incumbents are focusing on developing comprehensive solution portfolios that address the entire spectrum of semiconductor manufacturing needs, from advanced lithography to precise etching and deposition processes. Companies are investing heavily in research and development to maintain technological leadership, while simultaneously expanding their service and support capabilities to provide comprehensive solutions to their customers. The ability to offer integrated solutions that combine hardware excellence with advanced software capabilities and process optimization has become crucial for maintaining market position.

For new entrants and emerging players, success strategies center on identifying and exploiting niche market opportunities while building strong technological foundations and customer relationships. Companies must navigate complex regulatory environments, particularly regarding export controls and technology transfer restrictions, while maintaining flexibility to adapt to changing market conditions. The industry's future success factors include the ability to support customers' sustainability initiatives, manage supply chain complexities, and develop solutions for emerging applications in artificial intelligence, quantum computing, and advanced packaging. Market players must also balance the need for standardization with customization capabilities to serve diverse customer requirements while maintaining cost competitiveness and operational efficiency.

Semiconductor Front-End Equipment Market Leaders

-

Applied Materials Inc.

-

ASML Holding NV

-

Tokyo Electron Limited

-

LAM Research Corporation

-

KLA Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Semiconductor Front-End Equipment Market News

- February 2024 - At the SPIE Advanced Lithography + Patterning conference, Applied Materials unveiled a new lineup of products to address the intricate patterning demands of chips in the "Angstrom era," specifically at 2nm and below process nodes. The portfolio leverages innovative materials engineering and metrology techniques to tackle challenges associated with EUV and high-NA EUV patterning, such as line edge roughness and edge placement errors. This expansion in Applied Materials' Patterning Solutions Portfolio aims to assist chipmakers in navigating issues like tip-to-tip spacing limitations and bridge defects as they advance towards increasingly minuscule chip dimensions.

- December 2023 - Tokyo Electron announced the launch of Ulucus G, a wafer thinning system for 300 mm wafer fabrication, integrating an originally developed grinding unit with the LITHIUS Pro Z platform that has been fully production-proven in coating/developing applications. The new wafer thinning system enables the fabrication of higher-quality silicon wafers while reducing the workforce needed for mass production.

Semiconductor Front End Equipment Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Degree of Competition

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of COVID-19 Pandemic on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Increasing Needs of Consumer Electronic Devices Boosting the Manufacturing Prospects

- 5.1.2 Proliferation of Artificial Intelligence, IoT, and Connected Devices Across Industry Verticals

-

5.2 Market Restraints

- 5.2.1 Dynamic Nature of Technologies Requires Several Changes in Manufacturing Equipment

6. MARKET SEGMENTATION

-

6.1 By Type

- 6.1.1 Lithography Equipment

- 6.1.2 Etching Equipment

- 6.1.3 Deposition Equipment

- 6.1.4 Other Equipment Types

-

6.2 By End-user Industry

- 6.2.1 Semiconductor Fabrication Plant

- 6.2.2 Semiconductor Electronics Manufacturing

-

6.3 By Geography***

- 6.3.1 United States

- 6.3.2 Europe

- 6.3.3 China

- 6.3.4 South Korea

- 6.3.5 Taiwan

- 6.3.6 Japan

- 6.3.7 Latin America

- 6.3.8 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Applied Materials Inc.

- 7.1.2 ASML Holding NV

- 7.1.3 Tokyo Electron Limited

- 7.1.4 LAM Research Corporation

- 7.1.5 KLA Corporation

- 7.1.6 Nikon Corporation

- 7.1.7 VEECO Instruments Inc.

- 7.1.8 Plasma Therm

- 7.1.9 Hitachi High -Technologies Corporation

- 7.1.10 Carl Zeiss AG

- 7.1.11 Screen Holdings Co. Ltd

8. INVESTMENTS ANALYSIS

9. FUTURE OF THE MARKET

**Subject to Availability

*** In the Final Report Asia, Australia and New Zealand will be Studied Together as 'Asia Pacific'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Semiconductor Front-End Equipment Industry Segmentation

The front end and back end are two ways to separate semiconductor processes. Creating a finished wafer from a blank wafer is known as front-end semiconductor manufacturing. The wafer is spun during several front-end procedures. The front end involves fabricating silicon wafers, photolithography, deposition, etching, ion implantation, and mechanical polishing devices.

The semiconductor front-end equipment market is segmented by type (lithography equipment, etching equipment, deposition equipment, and other equipment types), end-user industry (semiconductor fabrication plant and semiconductor electronics manufacturing), and geography (United States, Europe, China, South Korea, Taiwan, Japan, Rest of Asia-Pacific, and Rest of The World). The report offers market forecasts and size in USD for all the above segments.

| By Type | Lithography Equipment |

| Etching Equipment | |

| Deposition Equipment | |

| Other Equipment Types | |

| By End-user Industry | Semiconductor Fabrication Plant |

| Semiconductor Electronics Manufacturing | |

| By Geography*** | United States |

| Europe | |

| China | |

| South Korea | |

| Taiwan | |

| Japan | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Semiconductor Front End Equipment Market Research FAQs

How big is the Global Semiconductor Front-end Equipment Market?

The Global Semiconductor Front-end Equipment Market size is expected to reach USD 107.95 billion in 2025 and grow at a CAGR of 8.65% to reach USD 163.45 billion by 2030.

What is the current Global Semiconductor Front-end Equipment Market size?

In 2025, the Global Semiconductor Front-end Equipment Market size is expected to reach USD 107.95 billion.

Who are the key players in Global Semiconductor Front-end Equipment Market?

Applied Materials Inc., ASML Holding NV, Tokyo Electron Limited, LAM Research Corporation and KLA Corporation are the major companies operating in the Global Semiconductor Front-end Equipment Market.

Which is the fastest growing region in Global Semiconductor Front-end Equipment Market?

North America is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Global Semiconductor Front-end Equipment Market?

In 2025, the Asia Pacific accounts for the largest market share in Global Semiconductor Front-end Equipment Market.

What years does this Global Semiconductor Front-end Equipment Market cover, and what was the market size in 2024?

In 2024, the Global Semiconductor Front-end Equipment Market size was estimated at USD 98.61 billion. The report covers the Global Semiconductor Front-end Equipment Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Global Semiconductor Front-end Equipment Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Semiconductor Front-end Equipment Industry Report

Mordor Intelligence provides comprehensive industry analysis and market outlook for the semiconductor front end equipment market, offering detailed insights into market size, growth trends, and competitive dynamics. Our research covers the entire spectrum of semiconductor manufacturing equipment and wafer fabrication technologies, including detailed market segmentation across key application areas and geographies. The report pdf includes in-depth analysis of market leaders, emerging technologies, and growth opportunities in the semiconductor equipment industry, enabling stakeholders to make informed decisions based on reliable market data and forecasts.

Beyond traditional market research, our consulting expertise extends to technology scouting and R&D analysis critical for semiconductor capital equipment innovations. We assist clients with competition assessment and go-to-market strategies specific to front end manufacturing solutions, leveraging our extensive knowledge of semiconductor process equipment dynamics. Our capabilities include comprehensive analysis of emerging technologies in wafer processing equipment and semiconductor fabrication equipment, product positioning strategies, and detailed assessment of regional market opportunities. Through advanced data analytics and visualization techniques, we provide actionable insights that help stakeholders navigate the complex landscape of semiconductor production equipment development and deployment.