Market Size of satellite manufacturing Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 244.93 Billion |

|

|

Market Size (2029) | USD 389.69 Billion |

|

|

Largest Share by Orbit Class | LEO |

|

|

CAGR (2024 - 2029) | 9.73 % |

|

|

Largest Share by Region | North America |

|

|

Market Concentration | High |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

Satellite Manufacturing Market Analysis

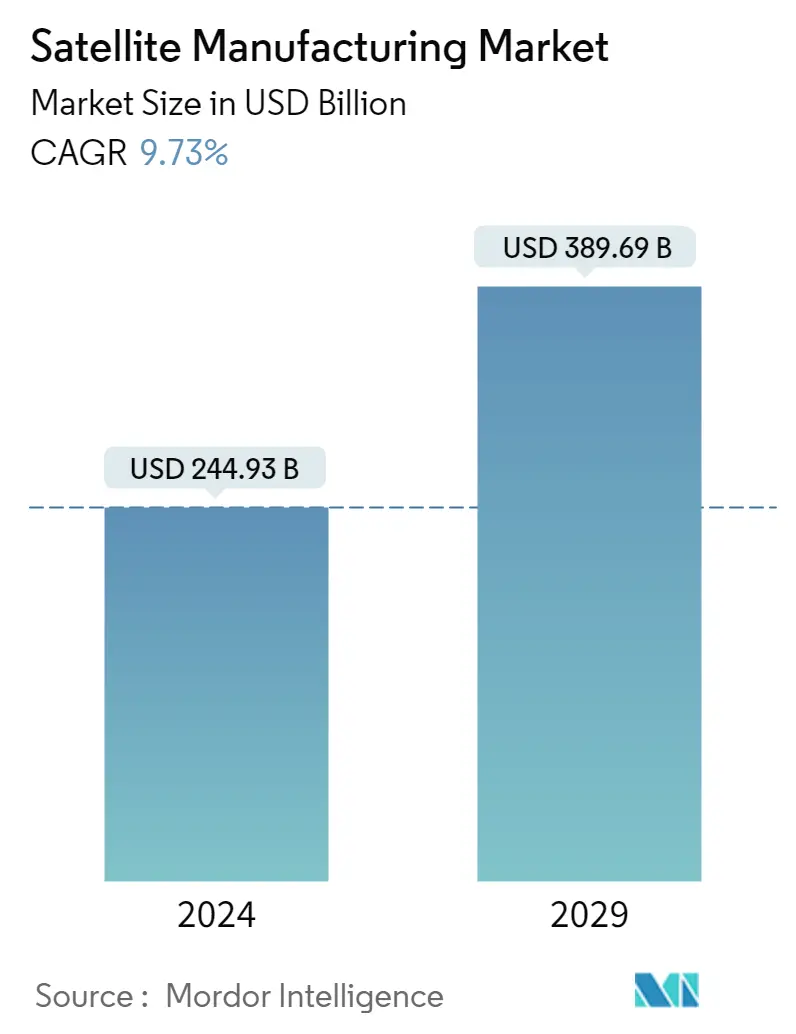

The Satellite Manufacturing Market size is estimated at USD 244.93 billion in 2024, and is expected to reach USD 389.69 billion by 2029, growing at a CAGR of 9.73% during the forecast period (2024-2029).

244.93 Billion

Market Size in 2024 (USD)

389.69 Billion

Market Size in 2029 (USD)

13.38 %

CAGR (2017-2023)

9.73 %

CAGR (2024-2029)

Largest Market by Satellite Mass

65.83 %

value share, 100-500kg, 2022

Minisatellites with expanded capacity for enterprise data (retail and banking), oil, gas, and mining, and governments in developed countries pose high demand. The demand for minisatellites with a LEO is increasing due to their expanded capacity.

Largest Market by Application

78.69 %

value share, Communication, 2022

Governments, space agencies, defense agencies, private defense contractors, and private space industry players are emphasizing the enhancement of the communication network capabilities for various public and military reconnaissance applications.

Largest Market by Orbit Class

72.49 %

value share, LEO, 2022

LEO satellites are increasingly being adopted in modern communication technologies as they play an important role in Earth observation applications.

Largest Market by Propulsion Tech

73.93 %

value share, Liquid Fuel, 2022

Because of its high efficiency, controllability, reliability, and long lifespan, liquid fuel-based propulsion technology is becoming an ideal choice for space missions. It can be used in various orbit classes for satellites.

Leading Market Player

53.10 %

market share, Space Exploration Technologies Corp., 2022

SpaceX is the leading player in the global satellite launch vehicle market and maintains its market share globally through its Starlink project. The company produces 120 satellites per month.

LEO Satellites Segment is Expected to Lead the Market

- A satellite or a spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey based on the application of a satellite. Out of the three orbits, namely Low Earth (LEO), Geostationary (GEO), and Medium Earth (MEO), it has been noted that LEO is the widely chosen one because of its proximity to the Earth.

- Many weather and communication satellites tend to have high Earth orbits farthest from the surface. Satellites in medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most science satellites, including NASA's Earth Observation System, are in low Earth orbit.

- Different satellites manufactured and launched across all the regions have different applications. For instance, during 2017-2022, out of the 56 satellites launched in MEO, most were built for Navigation/Global Positioning purposes. Similarly, out of the 133 satellites in the GEO orbit, most were deployed for communication and earth observation purposes. Around 4,025+ LEO satellites, manufactured and launched, were owned by various countries across the globe.

- The increasing use of satellites in areas such as electronic intelligence, earth science/meteorology, laser imaging, optical imaging, and meteorology is expected to drive the demand for the development of satellites during the forecast period.

Growing demand for satellite services such as communications, navigation, and earth observation is aiding the market growth

- The global satellite manufacturing market is a dynamic and rapidly changing industry that plays an important role in modern society. This industry includes companies that design, manufacture, and launch a wide range of satellites, from small cubes to large Earth observation and communication satellites.

- The industry is driven by various factors, including growing demand for satellite services such as communications, navigation, and Earth observation, and increasing accessibility to space for public and private organizations. As a result, the industry has seen significant growth in recent years, with new players entering the market and established companies expanding their capabilities.

- Satellite manufacturing is a complex process with many technologies, including advanced materials, electronics, and software. Companies in this field must have a deep understanding of these technologies and be able to integrate them into sophisticated systems that can withstand the harsh conditions of space. Major satellite manufacturers include Airbus Defense and Space, The Boeing Company, Lockheed Martin, and Thales Alenia Space.

- North America and Europe are more established markets in the industry, while Asia-Pacific is a more lucrative market for growth opportunities. From 2017 to May 2022, around 4300 satellites were manufactured and launched globally. The global satellite manufacturing market is projected to grow and innovate as demand for satellite services grows and space access expands.

Satellite Manufacturing Industry Segmentation

Communication, Earth Observation, Navigation, Space Observation, Others are covered as segments by Application. 10-100kg, 100-500kg, 500-1000kg, Below 10 Kg, above 1000kg are covered as segments by Satellite Mass. GEO, LEO, MEO are covered as segments by Orbit Class. Commercial, Military & Government are covered as segments by End User. Propulsion Hardware and Propellant, Satellite Bus & Subsystems, Solar Array & Power Hardware, Structures, Harness & Mechanisms are covered as segments by Satellite Subsystem. Electric, Gas based, Liquid Fuel are covered as segments by Propulsion Tech. Asia-Pacific, Europe, North America are covered as segments by Region.

- A satellite or a spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey based on the application of a satellite. Out of the three orbits, namely Low Earth (LEO), Geostationary (GEO), and Medium Earth (MEO), it has been noted that LEO is the widely chosen one because of its proximity to the Earth.

- Many weather and communication satellites tend to have high Earth orbits farthest from the surface. Satellites in medium Earth orbit include navigational and specialized satellites designed to monitor a specific area. Most science satellites, including NASA's Earth Observation System, are in low Earth orbit.

- Different satellites manufactured and launched across all the regions have different applications. For instance, during 2017-2022, out of the 56 satellites launched in MEO, most were built for Navigation/Global Positioning purposes. Similarly, out of the 133 satellites in the GEO orbit, most were deployed for communication and earth observation purposes. Around 4,025+ LEO satellites, manufactured and launched, were owned by various countries across the globe.

- The increasing use of satellites in areas such as electronic intelligence, earth science/meteorology, laser imaging, optical imaging, and meteorology is expected to drive the demand for the development of satellites during the forecast period.

| Application | |

| Communication | |

| Earth Observation | |

| Navigation | |

| Space Observation | |

| Others |

| Satellite Mass | |

| 10-100kg | |

| 100-500kg | |

| 500-1000kg | |

| Below 10 Kg | |

| above 1000kg |

| Orbit Class | |

| GEO | |

| LEO | |

| MEO |

| End User | |

| Commercial | |

| Military & Government | |

| Other |

| Satellite Subsystem | |

| Propulsion Hardware and Propellant | |

| Satellite Bus & Subsystems | |

| Solar Array & Power Hardware | |

| Structures, Harness & Mechanisms |

| Propulsion Tech | |

| Electric | |

| Gas based | |

| Liquid Fuel |

| Region | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

Satellite Manufacturing Market Size Summary

The satellite manufacturing market is a vital and evolving sector that encompasses the design, production, and launch of various types of satellites, including small cubes and large Earth observation and communication satellites. This industry is propelled by the increasing demand for satellite services such as communications, navigation, and Earth observation, alongside the growing accessibility of space for both public and private entities. The market is characterized by significant growth, with new entrants and established companies expanding their capabilities. The complexity of satellite manufacturing involves advanced technologies, including materials, electronics, and software, necessitating a deep understanding and integration of these systems to endure the harsh conditions of space. Major players in the industry include Airbus Defense and Space, The Boeing Company, Lockheed Martin, and Thales Alenia Space, with North America and Europe being more established markets, while Asia-Pacific presents lucrative growth opportunities.

The market is projected to experience substantial expansion, driven by the increasing use of satellites in diverse applications such as electronic intelligence, earth science, and meteorology. The ability of small satellites to perform functions at a reduced cost has enhanced the feasibility of small satellite constellations, contributing to market growth. North America, led by the United States, is a significant contributor to the market, with substantial government investment in space programs. Europe, with countries like Germany, France, and the UK, is also a major player, focusing on maintaining competitiveness through increased space funding. In the Asia-Pacific region, China, Japan, and India are key manufacturers, with significant investments in space capabilities. The market is fairly consolidated, with the top five companies holding a dominant share, and recent developments include contracts and satellite launches by major players, indicating ongoing innovation and expansion in the sector.

Satellite Manufacturing Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Application

-

1.1.1 Communication

-

1.1.2 Earth Observation

-

1.1.3 Navigation

-

1.1.4 Space Observation

-

1.1.5 Others

-

-

1.2 Satellite Mass

-

1.2.1 10-100kg

-

1.2.2 100-500kg

-

1.2.3 500-1000kg

-

1.2.4 Below 10 Kg

-

1.2.5 above 1000kg

-

-

1.3 Orbit Class

-

1.3.1 GEO

-

1.3.2 LEO

-

1.3.3 MEO

-

-

1.4 End User

-

1.4.1 Commercial

-

1.4.2 Military & Government

-

1.4.3 Other

-

-

1.5 Satellite Subsystem

-

1.5.1 Propulsion Hardware and Propellant

-

1.5.2 Satellite Bus & Subsystems

-

1.5.3 Solar Array & Power Hardware

-

1.5.4 Structures, Harness & Mechanisms

-

-

1.6 Propulsion Tech

-

1.6.1 Electric

-

1.6.2 Gas based

-

1.6.3 Liquid Fuel

-

-

1.7 Region

-

1.7.1 Asia-Pacific

-

1.7.1.1 By Country

-

1.7.1.1.1 Australia

-

1.7.1.1.2 China

-

1.7.1.1.3 India

-

1.7.1.1.4 Japan

-

1.7.1.1.5 New Zealand

-

1.7.1.1.6 Singapore

-

1.7.1.1.7 South Korea

-

-

-

1.7.2 Europe

-

1.7.2.1 By Country

-

1.7.2.1.1 France

-

1.7.2.1.2 Germany

-

1.7.2.1.3 Russia

-

1.7.2.1.4 United Kingdom

-

-

-

1.7.3 North America

-

1.7.3.1 By Country

-

1.7.3.1.1 Canada

-

1.7.3.1.2 United States

-

-

-

1.7.4 Rest of World

-

1.7.4.1 By Country

-

1.7.4.1.1 Brazil

-

1.7.4.1.2 Iran

-

1.7.4.1.3 Saudi Arabia

-

1.7.4.1.4 United Arab Emirates

-

1.7.4.1.5 Rest of World

-

-

-

-

Satellite Manufacturing Market Size FAQs

How big is the Satellite Manufacturing Market?

The Satellite Manufacturing Market size is expected to reach USD 244.93 billion in 2024 and grow at a CAGR of 9.73% to reach USD 389.69 billion by 2029.

What is the current Satellite Manufacturing Market size?

In 2024, the Satellite Manufacturing Market size is expected to reach USD 244.93 billion.