Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 4.92 Billion |

| Market Size (2030) | USD 6.88 Billion |

| Growth Rate (2025 - 2030) | 6.93% CAGR |

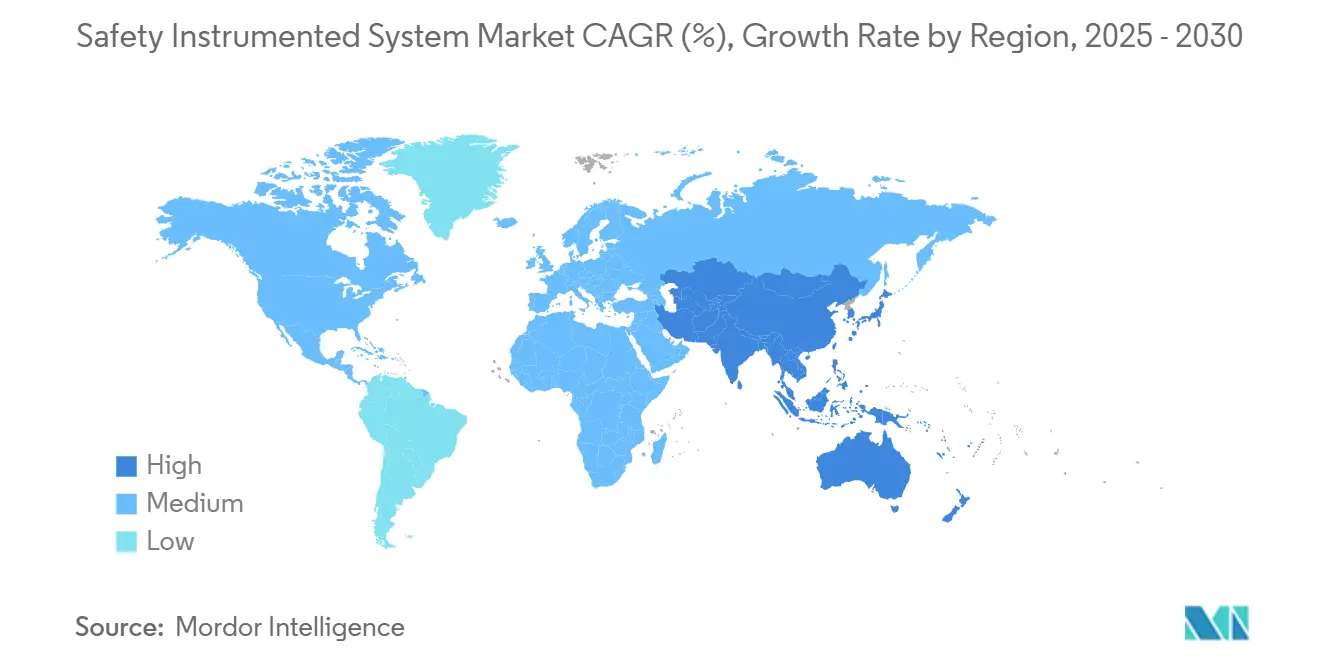

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

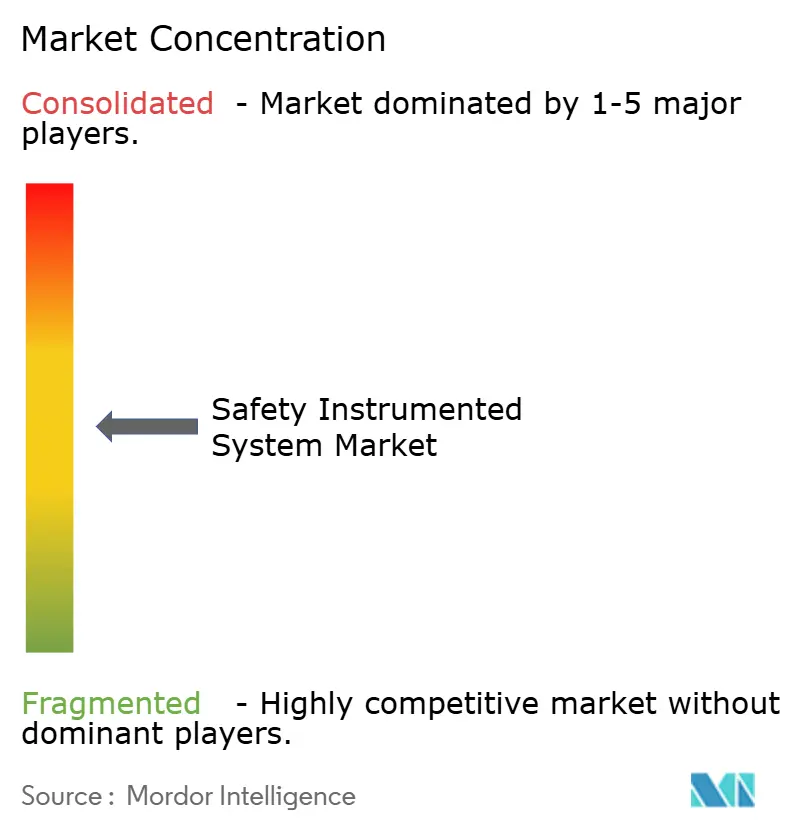

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Safety Instrumented System Market Analysis by Mordor Intelligence

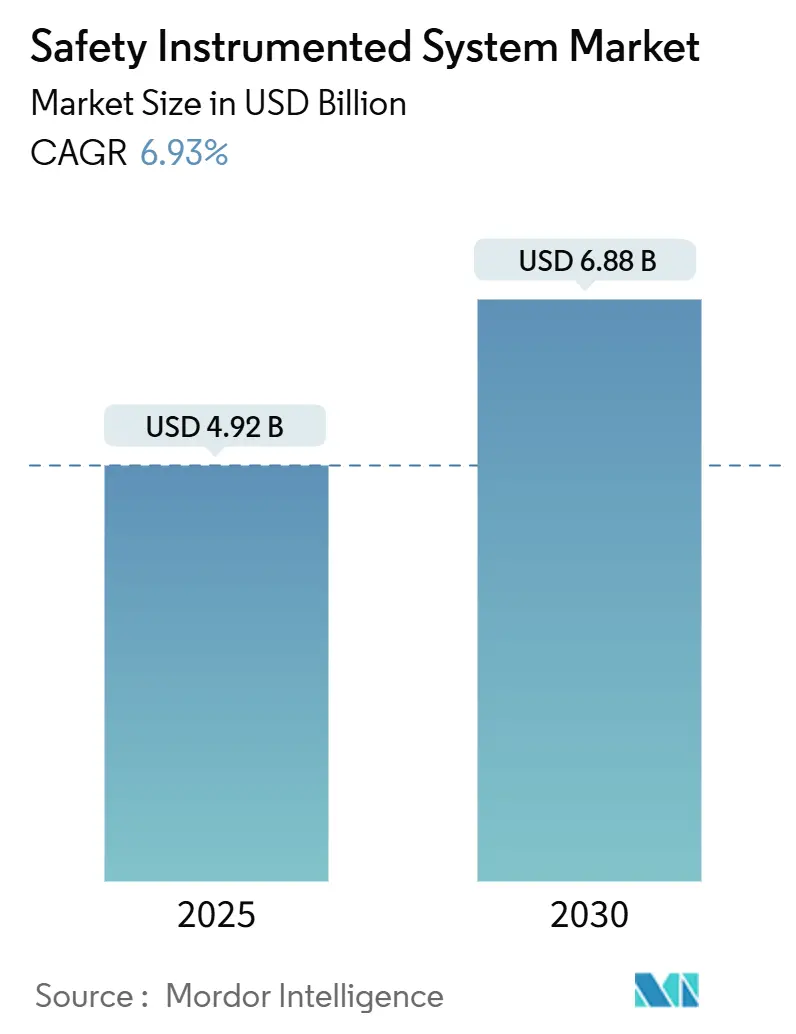

The Safety Instrumented System market size stands at USD 4.92 billion in 2025 and is forecast to reach USD 6.88 billion by 2030, advancing at a 6.93% CAGR. Escalating functional-safety regulations, rising brownfield modernization, and the surge of decarbonization projects position the Safety Instrumented System market for steady capacity additions. Operators in oil, gas, power, and chemicals view certified systems as essential insurance against single events that can incur losses of more than USD 100 million.[1]TÜV Rheinland, “Functional Safety,” tuv.com Digitalized diagnostics are shortening proof-test intervals and trimming maintenance budgets by as much as 30%, while modular “Safety-as-a-Service” offerings unlock new adoption among mid-tier facilities.[2]Schneider Electric, “Safety Solutions,” se.com Competitive rivalry intensifies as niche specialists target high-pressure hydrogen and CO₂ transport with High-Integrity Pressure Protection Systems (HIPPS) capable of handling operating pressures above 1,000 bar and sustaining SIL 3 certification.

Key Report Takeaways

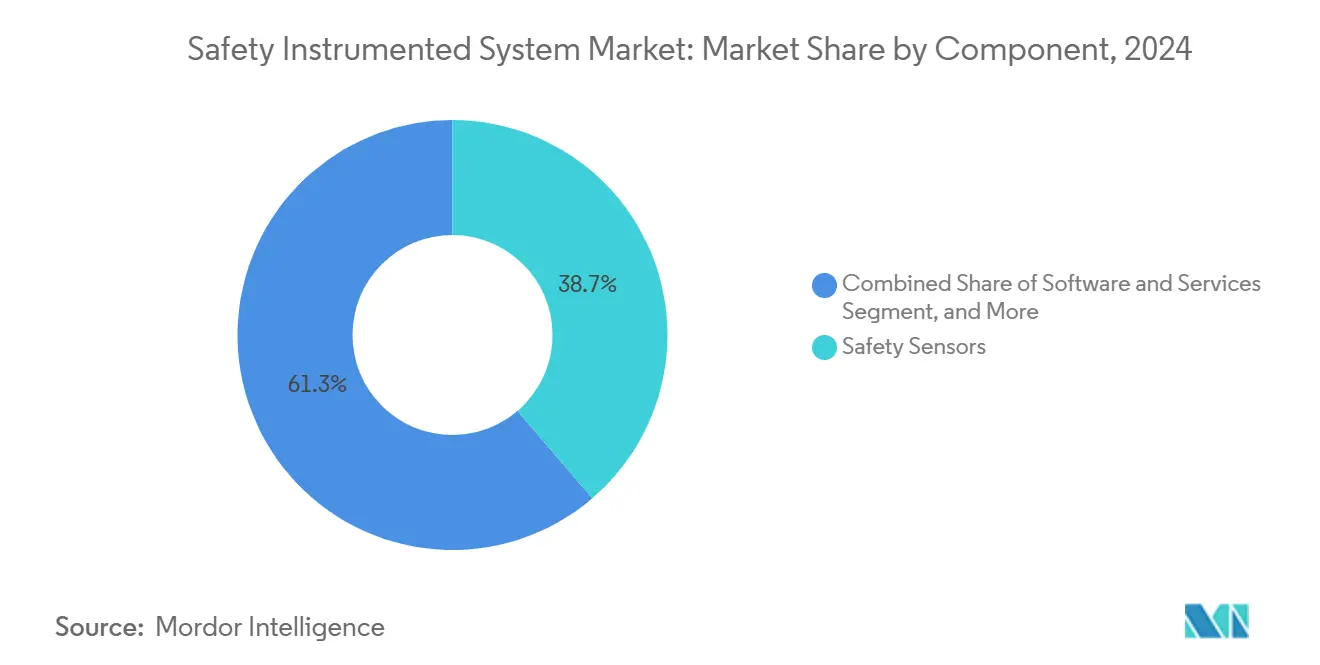

- By component, safety sensors held 38.73% of the safety instrumented system market share in 2024, whereas software and services is projected to post the fastest 7.33% CAGR through 2030.

- By application, emergency shutdown systems dominated with 41.73% revenue in 2024 in the safety instrumented system market, while HIPPS is forecast to expand at a 7.44% CAGR through 2030 owing to decarbonization infrastructure needs.

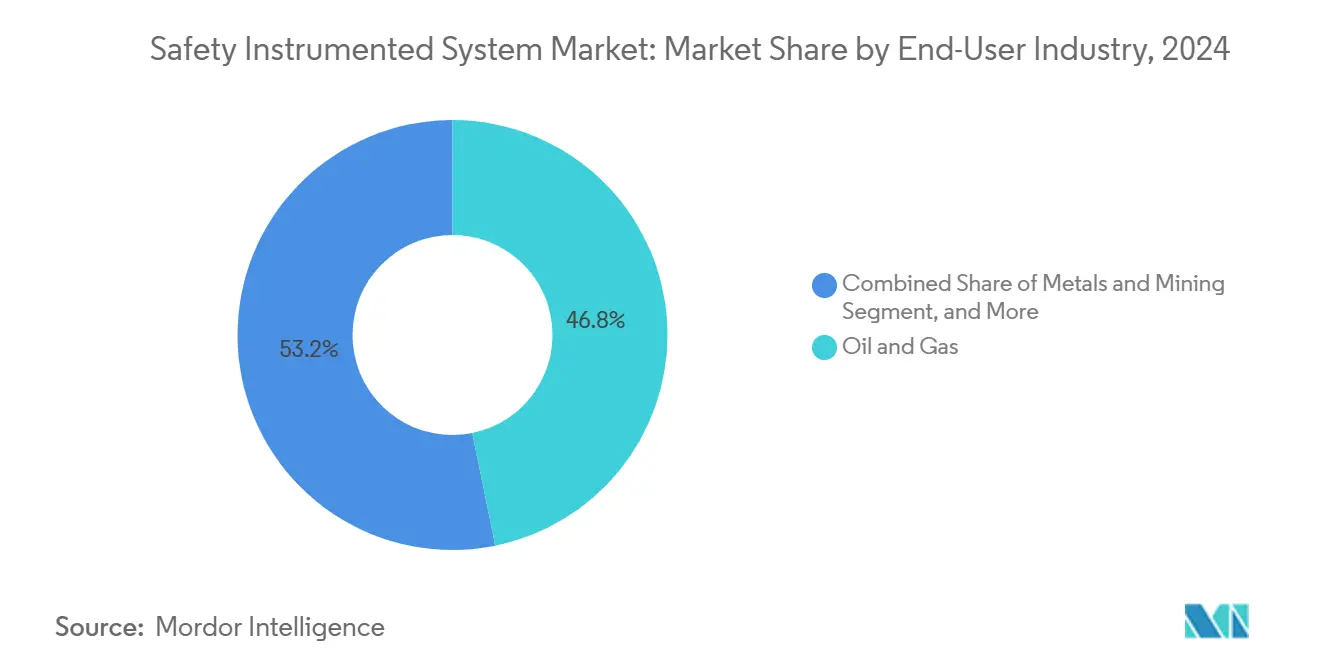

- By end-user, oil and gas contributed 46.82% of the safety instrumented system market size in 2024; power generation is set to grow the quickest at a 7.55% CAGR to 2030 on nuclear life-extension and grid-modernization programs.

- By service, engineering and consulting captured 34.72% share in 2024 in the safety instrumented system market, yet testing, certification and audit is seen rising at a 7.31% CAGR under stricter IEC 61511 audit cycles.

- By geography, North America led with 39.84% of 2024 revenue in the safety instrumented system market, while Asia-Pacific is the fastest-growing region at 8.3% CAGR because greenfield industrial capacity embeds certified safety from project inception.

Global Safety Instrumented System Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stricter global functional-safety regulations (IEC 61511, OSHA PSM) | +1.8% | Global, with strongest enforcement in North America and EU | Medium term (2-4 years) |

| Accelerating brown-field upgrades in oil and gas and chemicals | +1.5% | North America and Middle East core, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Digitalized diagnostics and IIoT cut downtime and proof-test cost | +1.2% | Global, led by North America and Europe | Medium term (2-4 years) |

| SIL-certified cyber-secure architectures drive replacement demand | +1.0% | Global, with priority in critical infrastructure regions | Long term (≥ 4 years) |

| Modular "Safety as-a-Service" platforms for mid-tier plants | +0.8% | Asia-Pacific and emerging markets primarily | Medium term (2-4 years) |

| Decarbonization (blue-H₂, CCUS) projects require new HIPPS | +0.7% | North America, Europe, Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Stricter Global Functional-Safety Regulations Drive Systematic Compliance

Global enforcement of IEC 61511 and OSHA Process Safety Management elevates the Safety Instrumented System market as facilities migrate from periodic audits to continuous performance verification. Functional-safety assessments grew 40% since 2024, stretching engineering resources and elongating project lead times. Operators with legacy platforms face mandatory overhauls, creating a seller’s market for certified integrators able to commit resources and deliver turnkey upgrades within eighteen to twenty-four months. High demand also supports premium pricing for TÜV-certified components, reinforcing revenue growth momentum.

Brownfield Upgrades Accelerate as Aging Infrastructure Meets Modern Standards

The Safety Instrumented System market benefits when older refineries and chemical complexes retrofit integrated safety architectures instead of constructing new plants. Brownfield retrofits already represent 65% of projects; Gulf Coast facilities spearhead activity as insurance underwriters tie coverage to conformance with current standards. Integration engineers bridge legacy protocols with contemporary Safety PLCs, often shrinking retrofit payback to less than four years by combining incident-risk mitigation with downtime reduction.[3]Emerson, “Safety Instrumented Systems,” emerson.com

Digitalized Diagnostics Transform Proof-Testing Economics

Continuous device health monitoring backed by machine learning permits condition-based maintenance. Operators reduce unplanned outages by up to 35% and triple proof-test intervals without lowering SIL ratings. The outcome lowers annual lifecycle cost by 25% and redirects scarce plant labor toward higher-value tasks. Predictive insight also limits false trips that in hydrocarbon processing can cost USD 100,000-500,000 in lost output per event, reinforcing the business case for advanced analytics.

SIL-Certified Cyber-Secure Architectures Address New Threats

Cybersecurity is now integral to functional safety. Updated frameworks stipulate authenticated remote access, encrypted safety logic transfer, and anomaly detection algorithms that flag unsafe code revisions. Vendors partner with OT security specialists to embed threat-mitigation functions that preserve SIL certification. The trend stimulates retrofit demand because equipment installed before 2018 cannot meet current cyber-secure requirements without hardware replacement.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex and lifecycle maintenance cost | -1.2% | Global, particularly impacting mid-tier operators | Short term (≤ 2 years) |

| Legacy-system integration complexity | -0.8% | North America and Europe with aging infrastructure | Medium term (2-4 years) |

| Shortage of TÜV/CFSE-certified safety engineers | -0.6% | Global, most acute in Asia-Pacific and emerging markets | Medium term (2-4 years) |

| SIL-grade component supply-chain constraints | -0.4% | Global, with regional variations in component availability | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital and Lifecycle Costs Challenge Mid-Tier Adoption

Full-facility deployments range from USD 5 million to USD 15 million, a hurdle for mid-size operators. Annual upkeep absorbs 15-20% of initial cost, covering proof-testing, component swaps, and software patches. Capital scarcity in emerging markets hampers replacement planning despite mounting compliance pressure. “Safety-as-a-Service” subscription schemes now spread capital across multi-year operating budgets, yet financing options remain limited, especially where local lenders assign high risk premiums.

Legacy-System Integration Complexity Extends Timelines and Budgets

Proprietary fieldbus protocols and mixed-vendor architectures require custom gateways that double engineering hours for brownfield work. Shortage of integration engineers proficient in both decades-old platforms and contemporary Safety PLCs inflates labor rates 20-30%. Project slippage risks compound if replacement windows coincide with peak demand seasons, pushing some operators to stage phased upgrades that stretch over several budget cycles.

Segment Analysis

By Component: Software and Services Catalyze Predictive Analytics

Software and Services recorded the fastest 7.33% CAGR because cloud analytics, machine learning, and virtual-commissioning tools unlock fresh value streams. The Safety Instrumented System market size for Software and Services is projected to climb from USD 1.27 billion in 2025 to USD 1.82 billion by 2030. AI-enhanced platforms distinguish genuine process excursions from noise, cutting nuisance trips by 50% and conserving production. Sensors retain a 38.73% revenue lead, yet the market pivots toward data-centric offerings that complement hardware with actionable insight.

Logic Solvers and Safety PLCs grow at a steady clip, buoyed by rising demand for high-pressure and high-speed applications. Final Elements leverage smart actuators providing continuous feedback, strengthening proof-test coverage. Vendors bundle sensors with subscription analytics, shifting revenue toward recurring models and reinforcing stickiness among installed-base customers.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: HIPPS Surges on Hydrogen and CO₂ Infrastructure

Emergency Shutdown retains 41.73% share, yet HIPPS experiences the highest 7.44% CAGR. Hydrogen pipelines and blue-ammonia export terminals require HIPPS capable of 2 second closure under 1,000 bar pressure. The Safety Instrumented System market size attached to HIPPS is forecast to almost double by 2030 as governments allocate record hydrogen incentives. Fire and Gas monitoring accelerates on stricter emissions controls, introducing multi-spectrum detectors that reduce false alarms. Burner Management Systems and Turbomachinery Control integrate with plant-wide safety layers, enabling coordinated shutdown to avert cascading failures.

By End-User Industry: Power Generation Outpaces as Grids Modernize

Oil and gas dominated 46.82% of 2024 revenue, propelled by offshore platform mandates after well-publicized disasters. Power generation exhibits a 7.55% CAGR because nuclear life-extension, combined-cycle plant upgrades, and synchronous condenser retrofits require new certified safety layers. The Safety Instrumented System market share is set to rebalance modestly toward power by 2030, aided by renewable integration that adds volatility and amplifies protection needs. Chemicals, pharmaceuticals, and water utilities adopt predictive diagnostics to align with strict product-quality and environmental standards while curbing operating expense.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Service: Testing and Certification Escalates Under IEC 61511 Cycles

Engineering and Consulting held 34.72%, yet Testing, Certification and Audit registers the quickest 7.31% CAGR. Recertification intervals tighten as regulators mandate ongoing proof of performance, elevating demand for TÜV, Exida, and CSA audits. Remote sensor validation and cybersecurity penetration tests gain prominence in integrated service contracts. Predictive analytics platforms funnel device health logs into certification portals, reducing manual document handling and shortening compliance cycles.

Geography Analysis

North America generated 39.84% of 2024 revenue on the back of OSHA Process Safety Management rigor and Gulf Coast brownfield programs. The United States alone houses more than 3,000 newly certified functional-safety engineers every year, sustaining a robust project pipeline. Operators focus on analytics upgrades, integrating cloud dashboards that visualize safety metrics for executive leadership. Canada’s upstream LNG terminals invest in SIL 3 HIPPS to safeguard high-pressure pipelines.

Europe follows with sizeable share under SEVESO III and the push for digital sovereignty that embeds cybersecurity into functional safety. Refiners in Germany and the Netherlands add predictive proof-testing to optimize turnarounds. Offshore North Sea platforms retrofit common-asset safety suites monitored from onshore control centers, shrinking field labor requirements.

Asia-Pacific is the fastest-growing territory at 8.3% CAGR. China and India commission large chemical parks with integrated safety from day one, bypassing legacy barriers. Government hydrogen roadmaps fast-track HIPPS spending, while Southeast Asian petrochemical hubs adopt modular Safety-as-a-Service to cap upfront capital. Australia’s mining sector deploys AI-based diagnostics to balance extreme uptime demands with worker-safety mandates.

The Middle East and Africa channel petro-revenues into high-spec refineries, often engaging international licensors that include certified safety as part of engineering packages. South America shows rising activity within mining and biofuels as operators align with stricter environmental standards and insurer expectations.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The Safety Instrumented System market is moderately consolidated. Five global automation majors account for more than two-thirds of revenue, leveraging cross-portfolio breadth, global service hubs, and extensive TÜV-certification libraries. Honeywell, ABB, Siemens, Emerson, and Schneider Electric differentiate through integrated platforms that marry sensors, logic solvers, and analytics. Software has emerged as the new battleground. Rockwell Automation introduced its Logix SIS controller in January 2025 with embedded machine learning that shrinks proof-test intervals to 18 months without compromising SIL 3 status.

Specialists pursue white-space by focusing on modular cloud architectures that suit mid-tier plants. Vendors such as Nozomi Networks weave cybersecurity into safety diagnostics to address converging threats. Sensor manufacturers partner with safety-system suppliers, evidenced by the SICK and Endress+Hauser collaboration initiated in 2024 to blend field instrumentation with certified logic environments. Acquisitions continue as strategy: Halma bought Global Fire Equipment and MK Test Systems to reinforce fire, gas, and testing coverage, while MSA Safety acquired M&C TechGroup to deepen gas analysis know-how.

Pricing pressure exists, yet life-cycle support contracts and subscription analytics defend margins. Suppliers embed proprietary analytics engines that interpret sensor health and event signatures, thereby locking in clients for multiyear service agreements and creating annuity streams.

Safety Instrumented System Industry Leaders

-

Rockwell Automation Inc.

-

Emerson Electric Company

-

Honeywell International Inc.

-

Yokogawa Electric Corporation

-

ABB Ltd.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- May 2025: MSA Safety completed acquisition of M&C TechGroup for USD 200 million, expanding gas-analysis capabilities for hydrogen and CCUS sectors.

- January 2025: Rockwell Automation launched its Logix SIS safety controller platform embedding machine learning for predictive maintenance.

- October 2024: Honeywell and Chevron initiated an AI partnership to cut refining maintenance outlays while elevating safety integrity.

- September 2024: ABB signed an MoU with EVE Energy to deliver safety systems for lithium-ion battery plants, targeting thermal-runaway risk mitigation.

Global Safety Instrumented System Market Report Scope

Safety instrumented systems (SIS) are being implemented across industries to complement their process control systems to reduce the risk of accidents on the industry floor and in the operation process. There are many ways in which safety instrumentation is being deployed. Compliance with international standards, such as IEC 61508 and IEC 61511, which indicate an acceptable quality in the design and management of safety controls across industries, drives the implementation of SIS.

The safety instrumented systems market is segmented by application (emergency shutdown systems [ESD], fire and gas monitoring and control [F&GC], high integrity pressure protection systems [HIPPS], burner management systems [BMS], turbo machinery control, and other applications), end user (chemicals and petrochemicals, power generation, pharmaceutical, food and beverage, oil and gas, and other end users), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The report offers market forecasts and size in value (USD) for all the above segments.

By Component

| Safety Sensors |

| Logic Solvers / Safety PLCs |

| Final Elements (Valves, Actuators, Solenoids) |

| Software and Services |

By Application

| Emergency Shutdown Systems (ESD) |

| Fire and Gas Monitoring and Control (FandG) |

| High-Integrity Pressure Protection Systems (HIPPS) |

| Burner Management Systems (BMS) |

| Turbomachinery Control (TMC) |

By End-User Industry

| Oil and Gas |

| Chemicals and Petrochemicals |

| Power Generation (incl. Nuclear and Renewables) |

| Pharmaceuticals and Life Sciences |

| Food and Beverage |

| Metals and Mining |

| Water and Wastewater |

| Other End-User Industries |

By Service

| Engineering and Consulting |

| Integration and Installation |

| Testing, Certification and Audit |

| Maintenance and Training |

By Geography

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Component | Safety Sensors |

| Logic Solvers / Safety PLCs | |

| Final Elements (Valves, Actuators, Solenoids) | |

| Software and Services | |

| By Application | Emergency Shutdown Systems (ESD) |

| Fire and Gas Monitoring and Control (FandG) | |

| High-Integrity Pressure Protection Systems (HIPPS) | |

| Burner Management Systems (BMS) | |

| Turbomachinery Control (TMC) | |

| By End-User Industry | Oil and Gas |

| Chemicals and Petrochemicals | |

| Power Generation (incl. Nuclear and Renewables) | |

| Pharmaceuticals and Life Sciences | |

| Food and Beverage | |

| Metals and Mining | |

| Water and Wastewater | |

| Other End-User Industries | |

| By Service | Engineering and Consulting |

| Integration and Installation | |

| Testing, Certification and Audit | |

| Maintenance and Training | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will global demand for certified safety systems be by 2030?

The Safety Instrumented System market is forecast to climb to USD 6.88 billion by 2030, reflecting a 6.93% CAGR over 2025-2030.

Which segment shows the fastest sales momentum?

High-Integrity Pressure Protection Systems post a 7.44% CAGR as hydrogen and carbon-capture infrastructures proliferate.

Why are Software and Services growing faster than hardware?

AI-driven diagnostics slash maintenance cost and shrink proof-test intervals, prompting users to invest in subscription analytics that enhance existing hardware.

What drives expansion in power generation applications?

Nuclear life-extension projects and grid-modernization efforts that integrate renewables require upgraded functional-safety layers with cyber-secure connectivity.

Which region leads in installed base upgrades?

North America commands nearly 40% of 2024 revenue thanks to OSHA regulation and Gulf Coast brownfield spending.

Page last updated on: