Robotic Arms In Laboratories Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

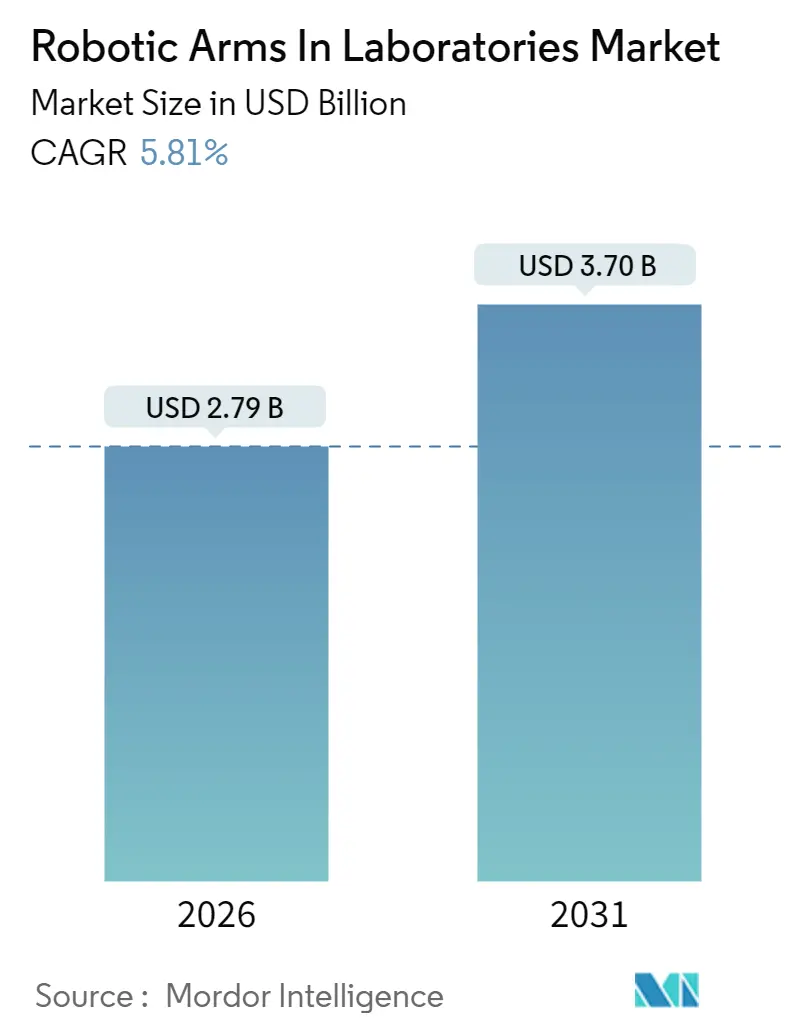

| Market Size (2026) | USD 2.79 Billion |

| Market Size (2031) | USD 3.7 Billion |

| Growth Rate (2026 - 2031) | 5.81% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

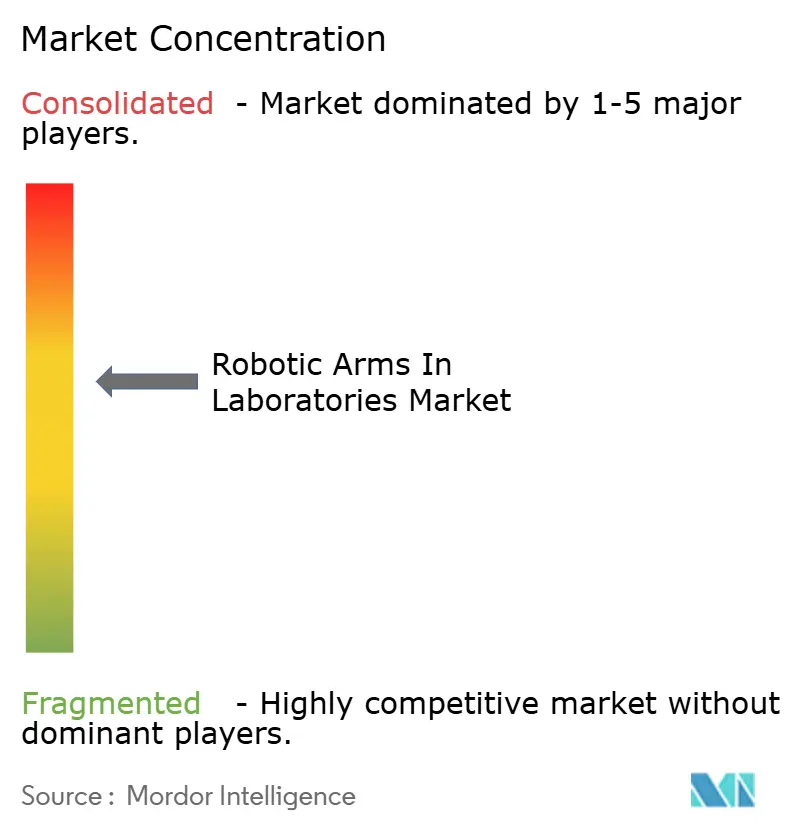

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Robotic Arms In Laboratories Market Analysis by Mordor Intelligence

The robotic arms in laboratories market is expected to grow from USD 2.64 billion in 2025 to USD 2.79 billion in 2026 and is forecast to reach USD 3.7 billion by 2031 at 5.81% CAGR over 2026-2031. This trajectory reflects a global shift from manual pipetting to automated workflows as drugmakers, contract research organizations, and diagnostic labs pursue faster cycle times, improved data integrity, and reduced contamination risk. Pharmaceutical discovery teams now screen hundreds of thousands of compounds per campaign, while biobanks and next-generation sequencing facilities require sub-microliter precision under stringent biosafety rules. Vendors compete on cleanroom compliance, collaborative safety features, and software connectivity, with open-source robot operating system platforms putting price pressure on traditional liquid-handling incumbents. New installations are concentrated in North America, Europe, and the rapidly expanding Asia Pacific, as governments fund biosafety infrastructure and continuous manufacturing pilots.

Key Report Takeaways

- By type, articulated arms held 40.58% of the robotic arms in laboratories market share in 2025, while collaborative arms are expected to expand at a 7.33% CAGR through 2031.

- By application, drug discovery led with 32.35% revenue share in 2025; genomics and proteomics are advancing at an 6.86% CAGR through 2031.

- By payload capacity, systems weighing up to 5 kg accounted for 44.05% of the robotic arms in laboratories market size in 2025, and heavy-duty units weighing above 15 kg are projected to grow at a 7.69% CAGR through 2031.

- By end-user, pharmaceutical and biotechnology companies represented 37.96% demand in 2025, whereas contract research organizations are recording a 6.47% CAGR to 2031.

- By geography, North America accounted for 34.05% of the revenue in 2025. The Asia Pacific is the fastest-growing region, with a 6.78% CAGR projected by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Robotic Arms In Laboratories Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Demand for High-Throughput Screening | +1.7% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Rising Adoption of Collaborative Laboratory Robots (Cobots) | +1.9% | Global, early gains in Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Stricter Occupational Safety Mandates in Biosafety Labs | +0.9% | Global, led by US CDC and European Centre for Disease Prevention and Control | Medium term (2-4 years) |

| Pharmaceutical Shift Toward Continuous Manufacturing | +0.8% | North America and Europe, pilot expansions in India | Long term (≥ 4 years) |

| Growth of Precision Medicine Driving Sample-Prep Automation | +0.7% | Global, strongest in North America and Western Europe | Long term (≥ 4 years) |

| Emerging Government Grants for Smart Lab Infrastructure | +0.5% | North America, Europe, China, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Demand for High-Throughput Screening Drives Miniaturization and Speed

Pharmaceutical discovery pipelines now process between 100,000 and 1 million compounds per campaign, volumes that make manual pipetting unsustainable. Roche’s uMed acoustic liquid handler, launched in 2024, pairs sub-nanoliter dispensing with machine-vision inspection, trimming reagent use by 40% while enabling fully unattended 384-well plate shuttling by articulated robotic arms.[1]Roche Diagnostics, “Roche Introduces uMed Acoustic Liquid Handling Platform,” roche.com The United States Food and Drug Administration’s 2024 strategic plan recognizes automated high-throughput screening as critical for faster investigational new drug submissions, encouraging laboratories to invest in audit-ready robots. Public-sector facilities follow suit; the National Institutes of Health’s translational sciences center now tests 10,000 compounds daily using robotic lines, demonstrating that academic labs can achieve commercial-grade throughput when adequately funded. As a result, robotic arms in laboratories market deployments that support high-throughput screening continue to climb across both commercial and academic sites.

Rising Adoption of Collaborative Laboratory Robots Reshapes Cleanrooms

Collaborative arms enable technicians to work safely alongside robots without full safety caging, a benefit that preserves floor space and reduces installation costs by approximately 40%. DENSO Wave’s COBOTTA PRO, released in January 2025, achieves a contact pressure of 10 newtons, aligning with ISO/TS 15066 force limits and experiencing early uptake in Asian pharmaceutical cleanrooms. Wave’s COBOTTA PRO, released in January 2025, achieves a contact pressure of 10 newtons, aligning with ISO/TS 15066 force limits and experiencing early uptake in Asian pharmaceutical cleanrooms. Universal Robots’ UR20, already installed at over 200 drug-manufacturing sites, lifts 20 kg while occupying a 245 mm footprint, freeing valuable bench area. Europe’s Annex 1 aseptic guidelines and the updated ISO/TS standard have trimmed validation times from 18 months to under 12, accelerating purchases in Italian and German fill-finish plants. These safety and compliance gains underpin the 7.56% CAGR for collaborative units, reinforcing growth momentum for the robotic arms in laboratories market.

Stricter Occupational Safety Mandates in Biosafety Labs Elevate Engineering Controls

The World Health Organization’s 2024 Laboratory Biosafety Manual and the United States Centers for Disease Control and Prevention’s sixth edition of the BMBL prioritize engineering controls over personal protective equipment.[2]World Health Organization, “Laboratory Biosafety Manual, Fourth Edition,” who.int Both texts explicitly endorse robotic manipulation for Risk Groups 3 and 4 pathogens to cut aerosol exposure. Labs now deploy arms inside HEPA-filtered enclosures with UV-C cycles to handle Ebola, Marburg, and coronavirus strains, reducing human exposure incidents by an estimated 60%. United States dual-use research policy revisions require proof that automation minimizes contact with enhanced pathogens, driving demand for tele-operated robots equipped with haptic feedback. These regulatory tailwinds strengthen safety-driven orders within the robotic arms in laboratories market.

Pharmaceutical Shift Toward Continuous Manufacturing Demands Integrated Robots

The United States Food and Drug Administration’s 2024 guidance and the European Medicines Agency’s reflection paper on continuous manufacturing encourage real-time release testing, which relies on robots that automatically feed samples from reactors to analyzers without manual intervention. Continuous lines run 24 hours a day, generating up to 20 samples per hour, a cadence incompatible with human labor alone. Thermo Fisher Scientific and Multiply Labs piloted articulated arms that adjust feed rates based on real-time analytics, cutting out-of-spec batches by 30%.[3]Thermo Fisher Scientific, “Thermo Fisher Scientific and Multiply Labs Announce Strategic Partnership,” thermofisher.com India’s forthcoming guidance, expected in late 2025, is poised to unlock similar investments. Integrated robotics, therefore, remain essential to continuous-manufacturing economics, supporting the long-term expansion of robotic arms in laboratories market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capital Outlay for ISO-Compliant Robotic Cells | -1.4% | Global, acute in academic and small biotech sectors | Short term (≤ 2 years) |

| Limited Dexterity in Handling Fragile Micro-volume Tasks | -0.7% | Global, concentrated in proteomics and single-cell genomics | Medium term (2-4 years) |

| Integration Challenges with Legacy LIMS and ELN Platforms | -1.1% | North America and Europe, where legacy systems dominate | Medium term (2-4 years) |

| Scarcity of Skilled Mechatronics Personnel in Academic Labs | -0.6% | Global, severe in Asia Pacific and Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capital Outlay for ISO-Compliant Robotic Cells Deters Academic Adopters

A six-axis arm with a cleanroom enclosure and ISO 17025 validation often exceeds USD 300,000, with service contracts adding 12-15% yearly. Academic labs relying on three-year NIH R01 grants struggle to allocate such funds, favoring manual workflows. ISO 15189 accreditation further mandates semi-annual gravimetric calibration, which costs up to USD 12,000 per cycle and approximately 60 technician hours. Small biotechnology firms, which form 70% of United States startups, lack capital reserves and instead outsource assays to contract research organizations. Horizon Europe grants require 30-40% cost sharing, slowing cobot purchases in Southern and Eastern member states. These financial barriers continue to temper near-term uptake within the robotic arms in laboratories market.

Integration Challenges with Legacy LIMS and ELN Platforms Fragment Data Workflows

Systems deployed before 2015 rarely offer modern application programming interfaces, forcing technicians to manually upload robot run logs, which erodes throughput benefits and risks transcription errors. Middleware projects that close these gaps cost USD 50,000–100,000 per site and can stall installations for months. Surveys indicate that 40-50% of robotic deployments remain isolated from enterprise data systems, leading to batch release delays of up to 48 hours. ISO 23494, released in 2024, defines semantic-interoperability rules, but adoption lags as legacy vendors prioritize backward compatibility. Until connectivity improves, integration friction will continue to weigh on the robotic arms in laboratories market.

Segment Analysis

By Type: Collaborative Arms Gain Share in Space-Constrained Cleanrooms

Articulated systems captured 40.58% of the robotic arms in laboratories market share in 2025, thanks to sub-50 µm repeatability and six-degree-of-freedom capabilities that suit microplate handling. Dual-arm robots remain a niche technology, but they enable parallel tasks, cutting the screening cycle time by up to 30%. Parallel-link architectures excel at rapid pick-and-place for vial capping in high-volume diagnostic labs. Collaborative designs recorded the fastest growth, expanding at 7.33% CAGR as manufacturers retrofit ISO Class 7 and 8 suites without cages. A FANUC CRX unit completes barcode scanning and seal-peel steps while sensing nearby staff, meeting Machinery Directive limits. The industry anticipates the forthcoming revision of IEC 61010-2-061 in 2026 to clarify safety criteria, thereby further enhancing the collaborative adoption of this standard. The robotic arms in laboratories market size for collaborative units is projected to surpass that of articulated platforms by 2028.

Collaborative arms thrive because they reduce installation costs by approximately 40%, compress commissioning schedules, and adapt to changing workflows. Pharmaceutical plants transitioning to personalized medicines value cobots that can be redeployed within hours. Yaskawa’s HC-series integrates machine vision to distinguish between human hands and labware, thereby avoiding pinch points. Universities favor lightweight units, such as the Opentrons OT-2, for teach-pendant simplicity under constrained grant budgets. These dynamics underscore why collaborative designs now anchor vendor roadmaps inside the broader robotic arms in laboratories market.

Note: Segment shares of all individual segments available upon report purchase

By Application: Genomics and Proteomics Step Up Automation

Drug discovery dominated 32.35% revenue in 2025, but sample-prep loads in genomics and proteomics now outpace it, with an 6.86% CAGR. Sequencers like Illumina NovaSeq X Plus require robots that transfer 384-well plates through heating, bead cleanup, and fluorometric checks in under 90 minutes, slashing hands-on work by 80%.Proteomics labs running Orbitrap Astral instruments rely on robots for 2 µL pickups, eliminating carryover. Clinical diagnostics centers deploy similar arms in ISO Class 5 biosafety cabinets to process respiratory panels, maintaining operator safety. Digital imaging, including whole-slide histopathology, uses arms to load 200 slides per hour. Systems biology groups culture organoids with robotic microfluidics to study drug metabolism. Collectively, these high-precision tasks expand the market size of robotic arms in laboratories, particularly within genomics and proteomics facilities.

The United States Food and Drug Administration guidance on companion diagnostics encourages the use of automated preparation to reduce pre-analytical variance. Laboratories pursuing College of American Pathologists accreditation, therefore, favor systems that generate electronic audit logs. This regulatory pull, coupled with falling genome-sequencing costs, sustains double-digit growth for robots serving genomics workloads. Vendors now package library-prep kits with pre-calibrated motion files, making installation easier. As adoption broadens, the robotic arms in laboratories market reinforce their strategic role in multi-omic science.

By Payload Capacity: Heavy-Duty Robots Enable Continuous Manufacturing

Arms lifting to 5 kg held a 44.05% share in 2025, covering tasks such as handling microplates, vials, and tubes. Mid-range 5–15 kg units serve automated biobanking and cryovial logistics. Above-15 kg machines, however, expand fastest at 7.69% CAGR, reflecting continuous-manufacturing projects that move 20 L carboys or 10 L media bottles with zero spills. Kawasaki’s duAro dual arm, rated at 30 kg total, dispenses powders into drums for oral solid dosage runs. Heavy-payload units also transport bioreactor vessels across cleanroom suites, thereby mitigating the risk of technician injuries and meeting ISO 10993-5 endotoxin control guidelines. As pharmaceutical plants pursue 24-hour lines, demand for robust actuators and hygienic stainless-steel joints rises, enlarging heavy-duty revenues within the robotic arms in laboratories market.

Heavy-payload systems further reduce ergonomic strain and overtime in media prep areas. Contract research organizations operating high-volume viral-vector suites rely on these arms to lift Centrifuge buckets and manage waste drums under biosafety cabinets, maintaining containment integrity. Regulatory auditors value electronic batch logs that document every transfer, streamlining inspections. Consequently, suppliers invest in torque-dense motors and wash-down-rated housing, underscoring the importance of heavy-duty tech to the robotic arms in laboratories market.

Note: Segment shares of all individual segments available upon report purchase

By End-User: Contract Research Organizations Scale Rapidly

Pharmaceutical and biotechnology companies accounted for 37.96% of 2025 sales, driven by the automation of cell-line development and formulation screening. Contract research organizations follow closely, growing at a 6.47% CAGR by offering sponsors faster turnaround without capital expense. Charles River Laboratories’ USD 292 million acquisition of Vigene Biosciences introduced fully robotic viral-vector lines, underscoring the strategic value of automation capacity. WuXi AppTec invested more than USD 400 million in 2024 to expand its robotic lines across multiple Chinese sites, catering to North American and European drugmakers. Academic institutes adopt robots through National Science Foundation Smart and Connected Health grants, focusing on cancer genomics. Clinical diagnostics labs rely on cobots to process polymerase chain reaction panels, meeting the College of American Pathologists checklist for validated automation. These diverse buyers widen the customer base, reinforcing healthy demand in the robotic arms in laboratories market.

Hospitals seeking rapid oncology biomarker results automate slide staining and molecular extraction, reducing pathologist turnaround to under 24 hours. Smaller biotech startups leverage Biosero's automation-as-a-service subscriptions to access robotic capacity without incurring capital risk. This pay-per-use model lowers entry barriers and fosters future upgrades, supporting the sustained growth of robotic arms in laboratories market.

Geography Analysis

North America held 34.05% of the revenue in 2025, reflecting the concentration of life-science hubs in Boston, the San Francisco Bay Area, and Research Triangle Park. The National Institutes of Health set aside USD 1.2 billion for shared instrumentation in fiscal 2025, funding cobots that assist translational oncology projects. Canada’s National Research Council launched a CAD 50 million (USD 37 million) Smart Lab Initiative targeting 30% productivity gains in government facilities. Mexico’s pharmaceutical plants in Jalisco and Mexico City automate vial filling to comply with the United States' current Good Manufacturing Practice, illustrating regional spillover. Together, these factors strengthen North American dominance within the robotic arms in laboratories market.

Europe followed with around 27.82% share in 2025 as Annex 1 aseptic rules and data-integrity expectations spurred upgrades. The United Kingdom awarded GBP 40 million (USD 51 million) to the Francis Crick and Wellcome Sanger institutes for genomics automation. Germany’s Fraunhofer network installed cobots for media prep in 2024, while Italy and Spain onshored sterile fill-finish capacity in response to pandemic supply shocks. These investments keep Europe at the forefront of collaborative safety standards and validate the robotic arms in laboratories market across the region.

The Asia Pacific is projected to grow at a 6.78% CAGR through 2031, the fastest worldwide, as governments invest in biosafety labs and smart-manufacturing pilots. China earmarked CNY 3 billion (USD 420 million) for robotic automation at top academies, focusing on synthetic biology. India’s Department of Biotechnology has launched a USD 150 million grant to modernize vaccine labs, aligning with the country's self-reliance goals. Japan’s pharmaceutical majors are retrofitting plants with cobots to offset labor shortages, and South Korea has invested KRW 80 billion (USD 60 million) in a national cell-therapy center.

Meanwhile, Israel and Gulf states are automating diagnostics to serve the medical tourism industry. Although Africa and South America remain nascent, pilots in South Africa and Brazil hint at future uptake. These regional dynamics underline the Asia Pacific’s role as the growth engine for robotic arms in laboratories market.

Competitive Landscape

The top five suppliers, Thermo Fisher Scientific, Hamilton Company, Tecan Group, Beckman Coulter, and PerkinElmer, control approximately 45-50% of the revenue, indicating moderate concentration. Legacy liquid-handling incumbents leverage validation protocols that ease regulatory submission; however, they face price pressure from open-source robot operating system platforms that offer a 30-40% lower capital outlay. Thermo Fisher’s March 2024 partnership with Multiply Labs bundles articulated arms, process analytics, and cloud data in a turnkey package, locking customers into proprietary ecosystems. Tecan reported first-half 2024 revenue softness due to drug makers delaying orders, but expects a rebound in high-throughput screening demand.

Industrial robotics veterans, FANUC, Yaskawa, Kawasaki, and DENSO Wave, apply automotive know-how to lab settings, selling collaborative arms 20-30% below traditional decks and squeezing margins. Software start-ups such as Biosero and Opentrons deliver middleware that integrates multi-vendor hardware, enabling subscription-based automation for cash-constrained biotech. Patent filings surged in 2024 around vision-guided grippers and haptic telemanipulation, reflecting innovation aimed at fragile container handling. Vendors able to ship ISO 17025 and ISO 15189 documentation out of the box gain a share of the clinical diagnostics market as CAP accreditation timelines shorten. Overall, competition is shifting from motion hardware to software orchestration, a trend that is shaping the future dynamics of the robotic arm market in the laboratory.

Robotic Arms In Laboratories Industry Leaders

Thermo Fisher Scientific Inc.

Hamilton Company

Hudson Robotics, Inc.

Tecan Group

Anton Paar GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2024: Thermo Fisher Scientific collaborated with Multiply Labs to embed articulated arms in continuous manufacturing suites, reducing out-of-spec batches by 30%.

- February 2024: Illumina launched the NovaSeq X Plus sequencer with integrated robotic library prep.

- February 2024: GITAI USA Inc., a firmspace robotics startup, is set to dispatch its 1.5-meter-long autonomous dual robotic arm system, dubbed S2, to the International Space Station (ISS). After successfully passing stringent NASA safety evaluations, the S2 is slated for external installation on the ISS's Nanoracks Bishop Airlock

- January 2024: Merck KGaA partnered with Opentrons Labworks to link the OT-2 robot with Milli-Q water systems, automating media preparation.

Global Robotic Arms In Laboratories Market Report Scope

A robotic arm is a mechanical, programmable device that manipulates objects in a manner similar to a human arm. Various medical institutions apply robotic arms to drive innovations in the healthcare industry. Robotic arms can prepare blood tests and medications in laboratories, assist in physical therapy, and more.

The Robotic Arms in Laboratories Market Report is Segmented by Type (Articulated Arm, Dual Arm, Parallel Link Arm, Collaborative Arm, Others), Application (Drug Discovery, Digital Imaging, Genomics and Proteomics, Clinical Diagnostics, Systems Biology, Others), Payload Capacity (Up To 5 kg, 5 kg to 15 kg, Above 15 kg), End-User (Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, Clinical Diagnostics Laboratories, Contract Research Organizations), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Articulated Arm |

| Dual Arm |

| Parallel Link Arm |

| Collaborative Arm |

| Other Arm Types |

| Drug Discovery |

| Digital Imaging |

| Genomics and Proteomics |

| Clinical Diagnostics |

| Systems Biology |

| Other Applications |

| Up To 5 kg |

| 5 kg - 15 kg |

| Above 15 kg |

| Pharmaceutical and Biotechnology Companies |

| Academic and Research Institutes |

| Clinical Diagnostics Laboratories |

| Contract Research Organizations |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Arm Type | Articulated Arm | |

| Dual Arm | ||

| Parallel Link Arm | ||

| Collaborative Arm | ||

| Other Arm Types | ||

| By Application | Drug Discovery | |

| Digital Imaging | ||

| Genomics and Proteomics | ||

| Clinical Diagnostics | ||

| Systems Biology | ||

| Other Applications | ||

| By Payload Capacity | Up To 5 kg | |

| 5 kg - 15 kg | ||

| Above 15 kg | ||

| By End-User | Pharmaceutical and Biotechnology Companies | |

| Academic and Research Institutes | ||

| Clinical Diagnostics Laboratories | ||

| Contract Research Organizations | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the robotic arms in laboratories market today?

The robotic arms in laboratories market size reached USD 2.79 billion in 2026.

What is the projected growth rate for robotic lab arms through 2031?

The market is forecast to grow at a 5.81% CAGR, hitting USD 3.7 billion by 2031.

Which application segment is growing fastest?

Genomics and proteomics workflows are expanding at an 6.86% CAGR as next-generation sequencing volumes rise.

Why are collaborative robots gaining popularity in laboratories?

Cobots operate safely beside technicians without cages, cut installation cost by 40%, and comply with updated ISO/TS 15066 standards.