Global Premium Hair Care Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

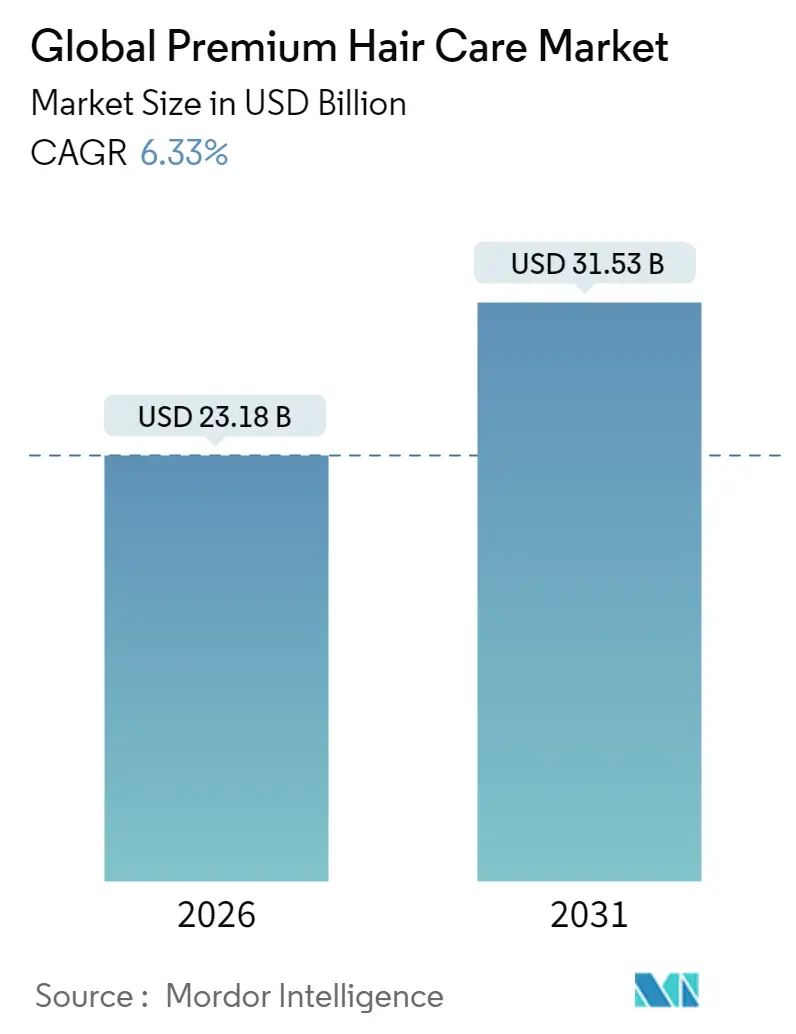

| Market Size (2026) | USD 23.18 Billion |

| Market Size (2031) | USD 31.53 Billion |

| Growth Rate (2026 - 2031) | 6.33% CAGR |

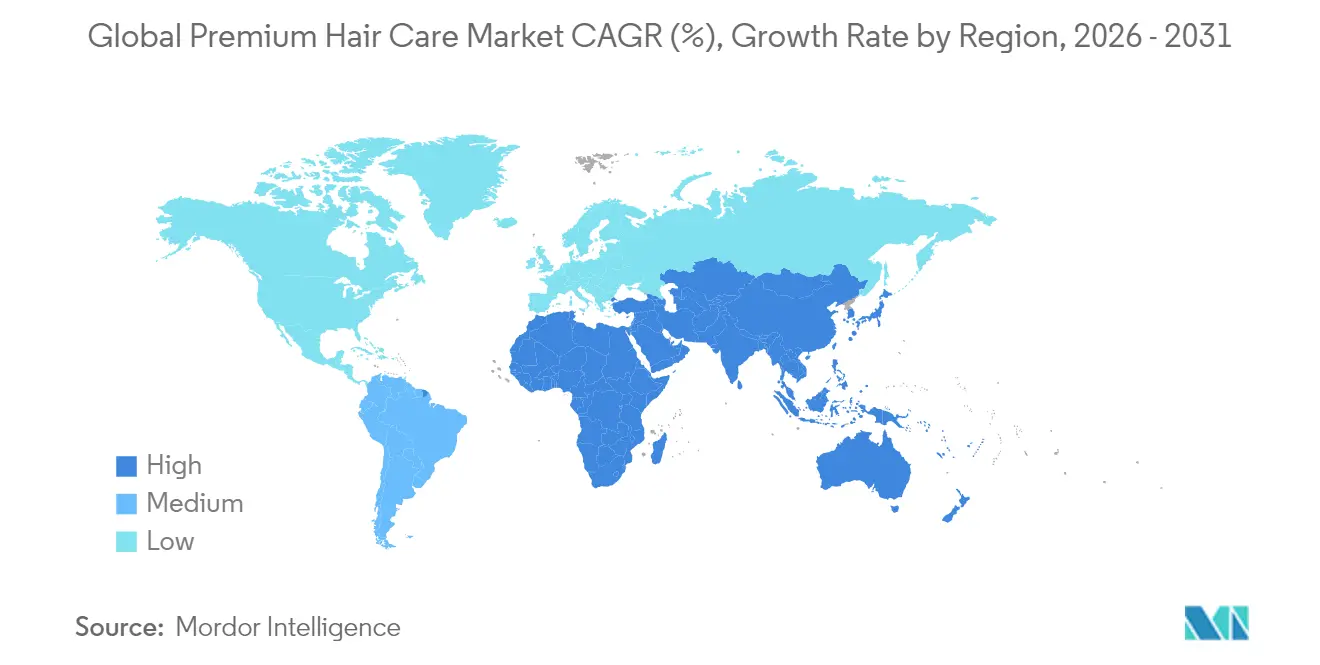

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Premium Hair Care Market Analysis by Mordor Intelligence

The global premium hair care market is expected to grow from USD 21.80 billion in 2025 to USD 23.18 billion in 2026 and is forecast to reach USD 31.53 billion by 2031 at 6.33% CAGR over 2026-2031. The market's growth is driven by multiple factors, including rising disposable incomes in emerging economies, technological innovations in product formulations, and the increasing influence of social media on consumer purchasing decisions. Environmental challenges, particularly urban pollution's impact on hair health, have created demand for protective formulations, as research indicates a correlation between particulate matter exposure and accelerated hair fiber degradation. Consumer behavior continues to evolve, with increased focus on addressing common hair problems such as hair loss and oily scalp, which are often worsened by environmental factors and weather conditions. The frequent use of hair care products, especially daily shampooing, has generated substantial demand for premium solutions. Natural, organic, and vegan hair care products have gained significant market share as consumers become more conscious of ingredient safety. This trend, combined with celebrity endorsements and convenient travel-sized packaging options, is reshaping the market landscape.

Key Report Takeaways

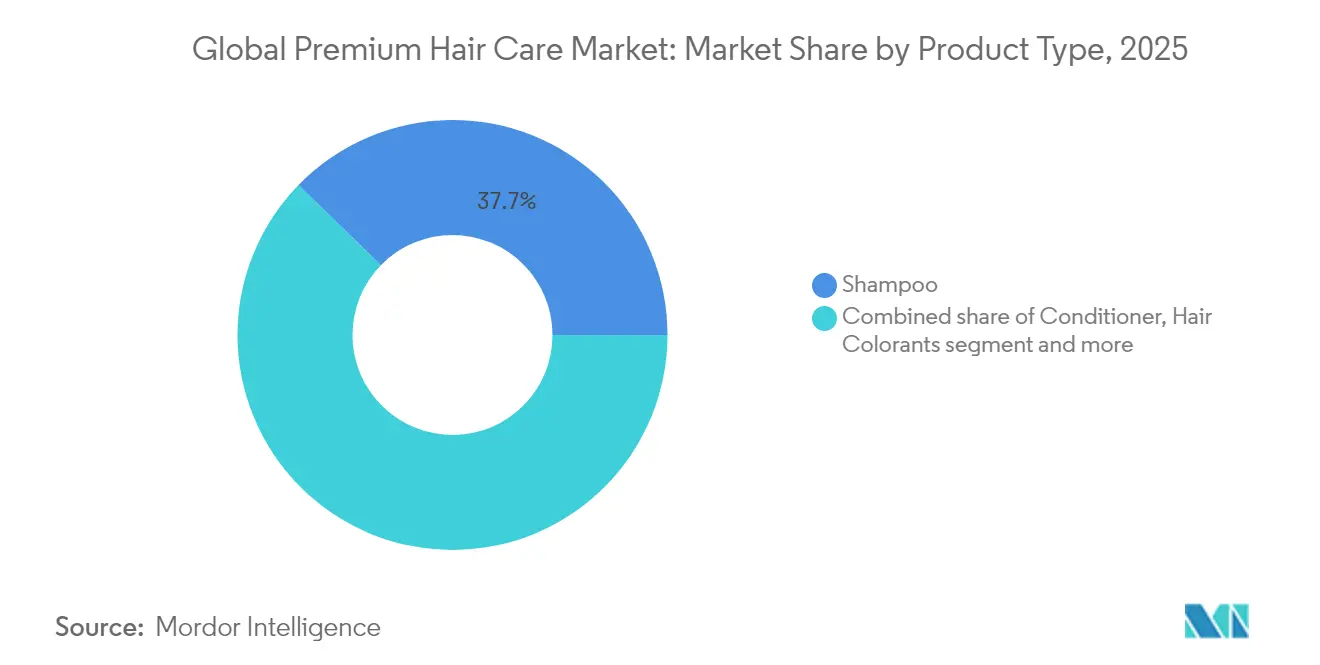

- By product type, shampoo led the premium hair care market with 37.70% revenue share in 2025, while hair styling items are projected to expand at a 6.76% CAGR to 2031.

- By ingredients, synthetic formulations captured 68.59% of the premium hair care market share in 2025, yet natural and organic lines are forecast to grow 7.22% CAGR through 2031.

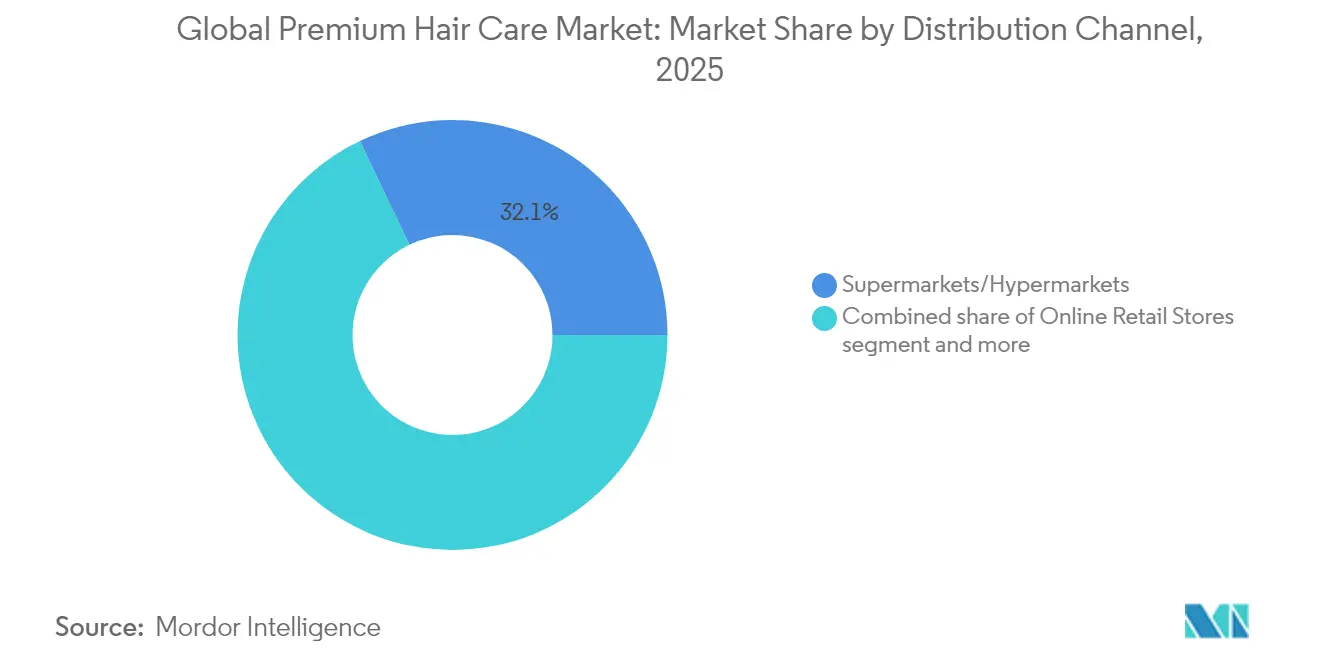

- By distribution channel, supermarkets/hypermarkets accounted for 32.10% of the premium hair care market size in 2025; online retail is advancing at a 7.06% CAGR to 2031.

- By geography, Asia-Pacific commanded 30.50% of the premium hair care market in 2025 and is poised to register a 7.45% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Premium Hair Care Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Influence of social media and celebrity endorsements | +1.2% | Global, North America and Asia-Pacific strongest | Short term (≤ 2 years) |

| Strong demand for products formulated with clean label ingredients | +1.8% | Global, North America and Europe lead | Medium term (2-4 years) |

| Increased consumer spending on self-care products | +1.5% | Global, Asia-Pacific and North America | Medium term (2-4 years) |

| Rising hair health concerns due to environmental and lifestyle factors | +0.9% | Global, urban centers | Long term (≥ 4 years) |

| Technological innovations in product formulations | +0.7% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Demand for multi-functional and damage control products | +0.4% | Global,premium segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Influence of Social Media and Celebrity Endorsement

Social media platforms have fundamentally transformed how consumers discover, evaluate, and purchase hair care products, establishing themselves as crucial channels for brand visibility and consumer engagement. Generation Z consumers, particularly active on Instagram and TikTok, are driving significant market changes through their social media preferences. Companies like Estee Lauder and Good Hair Day (GHD) have leveraged these platforms to build consumer communities, resulting in increased sales and market share. The market has evolved into a dual landscape where authentic storytelling and community engagement often supersede traditional brand equity, compelling established players to adapt their digital strategies. Celebrity collaborations, such as Ashley Tisdale's hair wellness line and Blake Lively's Blake Brown, have generated substantial retail traffic while reshaping consumer expectations regarding product efficacy and brand transparency. This transformation represents a lasting change in how premium hair care brands establish consumer trust and market presence. According to ITU, approximately 5.5 billion people, representing 68% of the world's population, are using the Internet in 2024, providing companies with extensive opportunities to utilize digital platforms for sales growth [1]Source: International Telecommunication Union, “Statistics,” itu.int. As social media continues to evolve, premium hair care brands must maintain adaptability and authenticity in their digital strategies to remain competitive in this rapidly changing market landscape.

Strong Demand for Products Formulated with Clean Label Ingredients

Consumer demand for clean beauty products has emerged as a key market driver, with increasing focus on ingredient transparency and verification. The accessibility of ingredient information through mobile applications and social media has doubled skincare-related interest in five years, leading consumers to prioritize ingredient transparency over brand reputation. This shift has prompted companies to develop plant-based alternatives to conventional ingredients, extending beyond simple substitution to encompass comprehensive sustainability narratives, including biodegradable packaging and ethically sourced raw materials. The transition presents formulation challenges, as natural alternatives often require different preservation systems and may exhibit performance variations compared to synthetic counterparts. According to NSF, in 2024, 74% of consumers consider organic ingredients important in personal care products, while 65% of consumers prioritize clear ingredient labeling for identifying potentially harmful components, fundamentally reshaping product development priorities across the industry [2]Source: NSF International, “Consumers Consider Personal Care Organic Ingredients Important,” nsf.org. As the clean beauty movement continues to gain momentum, manufacturers must balance consumer demands for natural ingredients with product efficacy and stability requirements.

Increased Consumer Spending on Self-care Products

The post-pandemic era has witnessed a sustained increase in consumer spending on self-care products, with hair care emerging as a significant beneficiary of this broader wellness trend. Despite inflation concerns, consumers remain committed to investing in products that offer clear benefits, particularly those focused on hair and scalp health. This shift has driven premiumization across all market segments, as consumers increasingly view hair care as an investment in personal confidence rather than a basic hygiene necessity. The COVID-19 pandemic accelerated this transformation, as people dedicated more time to hair care routines and sought salon-quality products for at-home use. Consumers now show greater willingness to invest in high-quality hair treatments, masks, and serums that deliver professional results, supported by growing awareness of hair health and preference for sustainable, natural ingredients. The influence of social media and beauty influencers has further educated consumers about premium hair care benefits, enabling brands to introduce higher-margin products with sophisticated formulations, such as peptide-based treatments and scalp microbiome-balancing solutions. A 2023 survey by Professional Beauty in the United Kingdom found that average consumers spent over GBP 4,600 annually on wellness and self-care, underscoring this significant market transformation [3]Source: Professional Beauty, “Brits Spend Over £45K on Self-Care Annually,” professionalbeauty.co.uk . This evolving consumer behavior indicates a lasting shift in the hair care market, suggesting continued growth opportunities for premium product innovations and specialized treatments.

Rising Hair Health Concerns Due to Environmental and Lifestyle Factors

Urban pollution has established direct links to hair fiber degradation through scientific research. Studies show that particulate matter penetrates hair follicles, causing keratinocyte cell death and increasing inflammatory responses. This environmental damage, along with UV radiation, harsh weather, stress, poor nutrition, and chemical treatments, has led to increased hair-related issues such as hair loss, thinning, and damage among urban residents. The hair care industry has developed protective formulations with antioxidants and environmental shields to address these challenges. Companies like BASF have introduced climate-adaptive beauty solutions. Water quality concerns have also influenced product development, as heavy metal exposure from contaminated water can damage hair protein structures, leading to the inclusion of chelating agents in modern formulations. Consumer awareness of environmental impacts on hair health, coupled with rising disposable incomes, has increased demand for premium hair care products that combine cleansing with environmental protection. As urban pollution continues to pose significant challenges to hair health, the development of innovative protective solutions remains crucial for the hair care industry's growth and consumer satisfaction.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of traditional at-home hair care solutions | -0.8% | Global, Asia-Pacific, Middle East and Africa stronger | Medium term (2-4 years) |

| Health concerns over chemical ingredients | -1.3% | Global, North America and Europe lead | Short term (≤ 2 years) |

| Enhanced presence of counterfeit products | -1.1% | Global, developing markets concentrate | Short term (≤ 2 years) |

| High production costs restrict market growth in developing regions | -0.6% | Asia-Pacific, Latin America, Middle East and Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Adoption of Traditional At-Home Hair Care Solutions

The increasing adoption of traditional hair care methods presents a significant restraint to the premium hair care market. Consumers are increasingly turning to DIY solutions and natural ingredients such as apple cider vinegar and avocado oil, either independently or in homemade preparations, instead of commercial products. This trend is particularly pronounced in emerging markets where traditional knowledge systems remain strong and in regions where cultural heritage intersects with cost considerations. Value-conscious consumers are especially drawn to these alternatives to premium-priced commercial products, creating a comprehensive alternative ecosystem to manufactured products. In response, manufacturers must demonstrate their products' advantages over traditional methods, often emphasizing scientifically proven benefits that DIY approaches cannot replicate, while also incorporating traditional ingredients into their formulations to attract consumers who prefer these elements.

Enhanced Presence of Counterfeit Products

Counterfeit hair care products pose a significant restraint to the premium hair care market, impacting both consumer safety and manufacturer revenues. These fraudulent products often contain harmful substances such as benzene, methylene chloride, and heavy metals, which can cause severe health issues, including liver damage, cancer, scalp irritation, and hair damage. The counterfeit market particularly thrives in emerging markets and regions with limited regulatory oversight, creating geographic disparities in product safety and market integrity. E-commerce platforms have unintentionally facilitated the distribution of counterfeit products by providing anonymous selling channels, making brand protection efforts more complex. While premium hair care manufacturers are implementing anti-counterfeiting measures such as holographic labels, QR codes, and blockchain technology for product authentication, the sophisticated nature of counterfeit operations and their ability to replicate packaging continues to undermine consumer trust and market growth. These fake products typically target price-sensitive consumer segments, requiring manufacturers to invest in both authentication technologies and consumer education initiatives to combat the problem effectively.

Segment Analysis

By Product Type: Shampoo Dominance Drives Routine Essentials

Shampoo products maintain commanding market leadership with a 37.70% share in 2025, reflecting their fundamental role in daily hair care routines across all demographic segments. The segment's dominance is reinforced by continuous innovation in formulations that address specific consumer concerns, with anti-dandruff and anti-hair fall variants experiencing strong demand. However, the segment faces emerging challenges, including consumer experimentation with alternatives and extended wash cycles. Manufacturers are responding through innovations in oil-infused formulations, dry shampoos, and personalized solutions tailored to specific hair types.

Hair styling products are emerging as the fastest-growing segment with a 6.76% CAGR through 2031, driven by premiumization trends and multi-functional formulations. The segment's growth reflects evolving consumer preferences for products that deliver multiple benefits, including heat protection, environmental defense, and aesthetic enhancement in single applications. While conditioner products maintain the second-largest market position, hair colorants are gaining momentum through technological innovations, including AI-powered color matching systems that enhance salon precision and customer satisfaction.

Note: Segment shares of all individual segments available upon report purchase

By Ingredients: Natural Surge Challenges Conventional Leadership

Conventional/synthetic ingredients maintain market dominance with a 68.59% share in 2025, while natural and organic formulations exhibit the fastest growth at 7.22% CAGR through 2031. This market evolution reflects the balance between proven synthetic performance and increasing consumer preference for clean beauty products that emphasize ingredient transparency and environmental sustainability. Biotechnology partnerships, such as Syensqo's collaboration with Bota Bio, are developing biomimetic ingredients that bridge the efficacy gap between conventional and natural solutions.

The natural segment's growth is driven by innovations in precision fermentation and plant-based alternatives that address traditional performance limitations while meeting clean beauty standards. While consumers demonstrate a willingness to pay premium prices for natural formulations, conventional ingredients maintain their significance in applications requiring immediate results or extreme durability, particularly in professional and specialized use cases. The increasing focus on sustainable sourcing and eco-friendly production methods has encouraged manufacturers to invest in research and development of natural alternatives. This investment has led to improved stability and shelf life of natural formulations, making them more commercially viable across various product categories.

By Distribution Channel: Digital Transformation Accelerates Retail Evolution

Supermarkets/hypermarkets hold the dominant distribution share at 32.10% in 2025, benefiting from their accessibility and ability to drive impulse purchases among mass-market consumers seeking convenience and competitive pricing. However, online retail stores are experiencing the fastest growth at 7.06% CAGR through 2031, supported by personalization capabilities, subscription models, and extensive product ranges that physical stores cannot match. The expansion of e-commerce is gradually reducing the market share of traditional retail formats. This shift is particularly evident in urban areas where digital literacy and smartphone penetration are high.

The evolution in distribution channels reflects changing consumer preferences, with online platforms providing detailed ingredient information, user reviews, and personalized recommendations that build purchase confidence. Specialty stores serve professional and premium segments, while traditional retailers implement omnichannel strategies that integrate digital platforms with physical stores. This approach reflects market data showing that successful hair care distribution requires both online product discovery and in-store testing opportunities. Virtual try-on capabilities and AI-driven product recommendations enhance the integration between physical and digital retail channels.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

Asia-Pacific commands both the largest market share at 30.50% in 2025 and the fastest regional growth at 7.45% CAGR through 2031, establishing the region as the primary driver of global hair care expansion. This dominance stems from a convergence of demographic, economic, and cultural factors, including large populations with rising disposable incomes, rapid urbanization, and cultural emphasis on hair care as essential to personal presentation. China drives regional growth through digital commerce innovation, while Japan and South Korea contribute through premium product innovation and beauty technology leadership, exemplified by companies like Polyphenol Factory launching advanced anti-hair loss formulations.

North America and Europe maintain substantial market positions through distinct competitive advantages. North American consumers demonstrate a high willingness to invest in premium, high-performance products while maintaining innovation leadership. European markets distinguish themselves through sustainability initiatives and regulatory standards that influence global product development. Both regions benefit from established distribution networks, sophisticated consumer education programs, and regulatory frameworks that ensure product safety while encouraging innovation.

Middle Eastern markets present unique opportunities characterized by hybrid consumption patterns, particularly evident in Saudi Arabia, where traditional herbal remedies coexist with commercial hair care products. This market dynamic is especially pronounced among younger demographics, who are influenced by social media and healthcare professional recommendations. The region's emerging consumer base creates opportunities for products that bridge traditional and modern hair care solutions, requiring carefully tailored localization strategies from manufacturers.

Competitive Landscape

The premium hair care market demonstrates moderate consolidation, characterized by competition among established multinational corporations while maintaining fragmentation that allows for specialized brands and emerging disruptors. Major players such as The Estee Lauder Companies Inc., Coty Inc., and L'Oréal S.A. maintain their market positions through extensive distribution networks and research and development investments. However, these companies face growing competition from biotechnology-enabled startups and culturally authentic brands that effectively leverage social media influence over traditional advertising channels.

The industry shows a clear trend toward vertical integration and biotechnology partnerships, exemplified by developments like Kao's introduction of The Answer, a premium hair care brand in October 2024. This high-quality, result-driven brand demonstrates the industry's focus on premium offerings and technological advancement. Also, companies are increasingly investing in AI-powered solutions for personalized formulations, making technology adoption a crucial competitive differentiator.

Significant opportunities exist in specialized segments, including pollution-defense formulations, scalp microbiome optimization, and culturally specific products that combine traditional practices with modern efficacy standards. The success of emerging companies like K18 illustrates how biotechnology innovation paired with effective social media strategies can achieve substantial market penetration, even with limited traditional marketing resources. This shift reflects the industry's evolution from commodity-based competition toward differentiated positioning through ingredient innovation and sustainability initiatives.

Global Premium Hair Care Industry Leaders

The Estee Lauder Companies Inc.

Coty Inc

Loreal S.A

Kao Corporation

Kenvue Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Tsubaki introduced Premium EX Hair Fall Care and Repair, a product line developed for damaged hair and scalp strengthening. The product range integrates scalp health and hair restoration treatments, establishing Tsubaki's first comprehensive solution that targets both conditions.

- May 2025: Hindustan Unilever introduced Nexxus in India to expand its premium hair care segment. The brand's launch represented the company's expansion into India's high-end and professional beauty market. Nexxus products incorporated Protein Transfusion Technology, which combined proteins and lipids in their formulations.

- March 2025: K18 established its presence in the United Kingdom market through a pop-up store at Harrods. The company launched a new anti-aging haircare product, aligning with its strategy of developing science-based haircare solutions.

- February 2025: Olaplex expanded its product portfolio through the introduction of scalp care products and the implementation of a new brand identity. These products focused on hair repair and health improvement, delivering sustained benefits for maintaining healthy hair.

Global Premium Hair Care Market Report Scope

The premium hair care market comprises high-end hair care products manufactured with advanced formulations, specialized ingredients, and innovative technologies. These products include shampoos, conditioners, treatments, styling products, and hair colorants that command higher prices due to their superior performance and targeted solutions. The market focuses on customized solutions and product efficacy, primarily utilizing professional-grade formulations.

The global premium hair care market studied is segmented by product type, ingredients, distribution channel, and geography. Based on product type, the market studied is segmented into shampoo, conditioner, hair colorants, hair styling products, and other types. Based on ingredients, the market is segmented into conventional and natural/organic. Based on distribution channels, the market studied is segmented into specialty stores, hypermarkets/supermarkets, online retail stores, and other distribution channels. Based on geography, the market studied is segmented into North America, Europe, Asia-Pacific, South America, the Middle East & Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Shampoo |

| Conditioner |

| Hair Colorants |

| Hair Styling Products |

| Other Product Types |

| Conventional |

| Natural/Organic |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Spain | |

| Netherlands | |

| Italy | |

| Sweden | |

| Poland | |

| Belgium | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Indonesia | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | United Arab Emirates |

| South Africa | |

| Nigeria | |

| Saudi Arabia | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Product Type | Shampoo | |

| Conditioner | ||

| Hair Colorants | ||

| Hair Styling Products | ||

| Other Product Types | ||

| By Ingredients | Conventional | |

| Natural/Organic | ||

| By Distribution Channel | Specialty Stores | |

| Supermarkets/Hypermarkets | ||

| Online Retail Stores | ||

| Other Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Spain | ||

| Netherlands | ||

| Italy | ||

| Sweden | ||

| Poland | ||

| Belgium | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Indonesia | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Colombia | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | United Arab Emirates | |

| South Africa | ||

| Nigeria | ||

| Saudi Arabia | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the premium hair care market?

The premium hair care market generated USD 23.18 billion in 2026 and is forecast to reach USD 31.53 billion by 2031.

Which region is growing fastest in the premium hair care market?

Asia-Pacific leads growth with a projected 7.45% CAGR through 2031, driven by rising incomes and advanced digital retail ecosystems.

Which product type dominates sales?

Shampoo commands the largest slice, securing 37.70% of 2025 revenue owing to its integral role in daily routines.

Why are natural ingredients gaining traction?

Consumers view organic inputs as important, prompting brands to swap synthetics for plant-based, biotech-engineered actives without compromising performance.

How are counterfeit products affecting the premium hair care market?

Fake items erode consumer trust and manufacturer revenue, especially in regions with limited regulatory oversight, prompting brands to implement authentication measures such as QR codes and blockchain tracking.

What technological innovations are shaping future product formats?

Precision-fermented peptides, AI-driven diagnostics, and multi-functional polymers that resist pollution and heat damage are steering formulation trends and reinforcing premium positioning within the category.