Market Size of pet food Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 192.51 Billion |

|

|

Market Size (2029) | USD 290.01 Billion |

|

|

Largest Share by Pets | Dogs |

|

|

CAGR (2024 - 2029) | 8.54 % |

|

|

Largest Share by Region | North America |

|

|

Market Concentration | Low |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

Pet Food Market Analysis

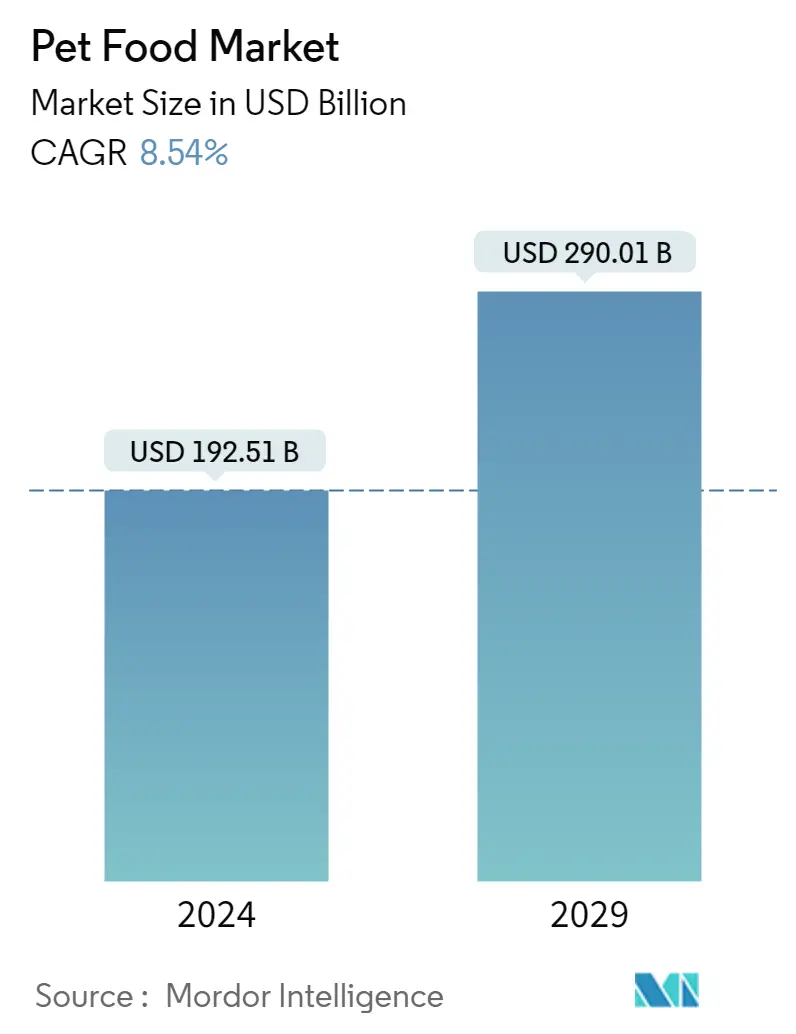

The Pet Food Market size is estimated at USD 192.51 billion in 2024, and is expected to reach USD 290.01 billion by 2029, growing at a CAGR of 8.54% during the forecast period (2024-2029).

192.51 Billion

Market Size in 2024 (USD)

290.01 Billion

Market Size in 2029 (USD)

9.34 %

CAGR (2017-2023)

8.54 %

CAGR (2024-2029)

Largest Market by Product

70.99 %

value share, Food, 2022

The increasing pet population and the growing consumer demand for high-quality and nutritious dry and wet foods to support pets' health increased the share of food products.

Largest Market by Region

44.25 %

value share, North America, 2022

High pet ownership rates and increased purchasing of dry pet foods, wet foods, and treats formulated with functional ingredients have contributed to the region's leading position.

Fastest-growing Market by Product

9.84 %

Projected CAGR, Pet Veterinary Diets, 2023-2029

The rising awareness about pet health and the prevalence of health issues in pets, particularly pet obesity and dental issues, are increasing the usage of veterinary diets.

Fastest-growing Market by Region

12.28 %

Projected CAGR, Africa, 2023-2029

The increasing pet ownership rates and consumers spending more on premium dry and wet food products are the major factors driving its market growth.

Leading Market Player

14.02 %

market share, Mars Incorporated, 2022

Mars, Incorporated is the market leader, with heavy investments in R&D, a focus on product innovation and expansions, and acquisitions of major companies such as Champion Petfoods and NomNomNom.

Dogs dominate the market due to higher usage of commercial foods and high per capita consumption

- The global pet food market shows a positive trend as there is an increasing pet adoption globally. The market witnessed a growth of 59.4% between 2017 and 2022. This growth was attributed to the increasing pet humanization trend, pet premiumization, feeding of commercial foods, and the rise in pet population by 13.0 between 2017 and 2022.

- Globally, dogs are the major pets adopted by pet parents. In 2022, they accounted for the largest share of the global pet food market, accounting for a market value of USD 80.03 billion in 2022. They are anticipated to reach USD 156.60 billion in 2029. This higher share is due to a significant number of pet owners shifting from home-cooked food to commercial food, the higher dietary needs of dogs compared to other pets, and the higher dog population. For instance, the dog population was 604.5 million in 2022, whereas the cat population was 408.2 million globally.

- Cats were the second major consumer of pet food, accounting for 32.3% in 2022, which is estimated to register a CAGR of 6.8% during the forecast period. This growth is due to the significant increase in the cat population by 18.8% between 2017 and 2022, followed by the rise in popularity of cat companionship due to their comparatively low maintenance requirements.

- The other pets segment consists of birds, small mammals, rodents, and ornamental fish. They accounted for 19.0% of the market in 2022 despite the 35.0% population share in the same year. This lower share was due to their smaller body size, resulting in lower food requirements compared to cats and dogs.

- The rise in commercial food usage, pet humanization, and the growing population of pets worldwide are the factors anticipated to drive the market at a CAGR of 7.4% during the forecast period.

North America dominates the global pet food market due to a high pet population, higher disposable incomes, and the prevailing trend of pet humanization

- In 2022, North America emerged as the largest regional market in the global pet food market, with a value of USD 77.43 billion. The United States and Mexico are the major contributors to the North American pet food market due to the high pet ownership rates in these countries. The North American market witnessed an increase of 74.7% between 2017 and 2022, driven by the increasing adoption of pets, rising disposable income, and the prevailing trend of pet humanization.

- Europe holds the second-largest regional share of the market, valued at USD 47.74 billion in 2022. This market is highly driven by the increasing awareness of ingredients, customized food products, grain-free, and organic food. Europe registered significant growth of 23.6% between 2017 and 2021, owing to the increasing pet population in the region, which reached 324.4 million in 2022, rising from 290.5 million in 2017.

- The Asia-Pacific countries have witnessed significant increases in pet humanization and consumer preference for premium pet food products in recent years. Pet owners in the region are increasingly opting for commercial pet food products, which is driving market growth in the region. Due to these factors, the Asia-Pacific pet food market reached USD 29.36 billion in 2022.

- Africa and South America are the fastest-growing regions in the market, with estimated CAGRs of 12.2% and 12.1%, respectively, during the forecast period. This is mainly due to their growing pet populations and a large number of pet owners shifting from home-cooked food to commercial pet food, in line with the rising trend of pet humanization.

- The growing pet population, increased disposable incomes, and pet humanization trends globally are estimated to drive the market during the forecast period.

Pet Food Industry Segmentation

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Cats, Dogs are covered as segments by Pets. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. Africa, Asia-Pacific, Europe, North America, South America are covered as segments by Region.

- The global pet food market shows a positive trend as there is an increasing pet adoption globally. The market witnessed a growth of 59.4% between 2017 and 2022. This growth was attributed to the increasing pet humanization trend, pet premiumization, feeding of commercial foods, and the rise in pet population by 13.0 between 2017 and 2022.

- Globally, dogs are the major pets adopted by pet parents. In 2022, they accounted for the largest share of the global pet food market, accounting for a market value of USD 80.03 billion in 2022. They are anticipated to reach USD 156.60 billion in 2029. This higher share is due to a significant number of pet owners shifting from home-cooked food to commercial food, the higher dietary needs of dogs compared to other pets, and the higher dog population. For instance, the dog population was 604.5 million in 2022, whereas the cat population was 408.2 million globally.

- Cats were the second major consumer of pet food, accounting for 32.3% in 2022, which is estimated to register a CAGR of 6.8% during the forecast period. This growth is due to the significant increase in the cat population by 18.8% between 2017 and 2022, followed by the rise in popularity of cat companionship due to their comparatively low maintenance requirements.

- The other pets segment consists of birds, small mammals, rodents, and ornamental fish. They accounted for 19.0% of the market in 2022 despite the 35.0% population share in the same year. This lower share was due to their smaller body size, resulting in lower food requirements compared to cats and dogs.

- The rise in commercial food usage, pet humanization, and the growing population of pets worldwide are the factors anticipated to drive the market at a CAGR of 7.4% during the forecast period.

| Pet Food Product | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

| Pets | |

| Cats | |

| Dogs | |

| Other Pets |

| Distribution Channel | |

| Convenience Stores | |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

| Region | |||||||||||||||

| |||||||||||||||

| |||||||||||||||

| |||||||||||||||

| |||||||||||||||

|

Pet Food Market Size Summary

The pet food market is experiencing a robust expansion, driven by the increasing global trend of pet adoption and the humanization of pets. This growth is further fueled by the shift from home-cooked meals to commercial pet foods, particularly for dogs, which dominate the market due to their higher dietary needs and larger population compared to other pets. Cats, while second in terms of market share, are gaining traction due to their low maintenance requirements and the rising popularity of cat companionship. The market is also seeing a significant rise in the adoption of other pets, such as birds and small mammals, although their share remains smaller due to lower food requirements. The trend of pet premiumization, where pet owners are willing to invest in high-quality food, is also contributing to the market's growth, as is the increasing awareness of pet health and nutrition.

Regionally, North America leads the market, with the United States and Mexico being major contributors due to high pet ownership rates and disposable incomes. Europe follows, driven by a demand for customized and organic pet food products. The Asia-Pacific region is witnessing a surge in the preference for premium pet food, while Africa and South America are the fastest-growing markets, propelled by rising pet populations and a shift towards commercial pet food. The market is characterized by a shift in purchasing habits from offline to online stores, especially post-pandemic, as consumers seek the convenience and variety offered by online platforms. The market remains fragmented, with major players like Mars Incorporated, Nestle Purina, and The J. M. Smucker Company leading the charge in innovation and product development to cater to the evolving needs of pet owners.

Pet Food Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Pet Food Product

-

1.1.1 Food

-

1.1.1.1 By Sub Product

-

1.1.1.1.1 Dry Pet Food

-

1.1.1.1.1.1 By Sub Dry Pet Food

-

1.1.1.1.1.1.1 Kibbles

-

1.1.1.1.1.1.2 Other Dry Pet Food

-

-

-

1.1.1.1.2 Wet Pet Food

-

-

-

1.1.2 Pet Nutraceuticals/Supplements

-

1.1.2.1 By Sub Product

-

1.1.2.1.1 Milk Bioactives

-

1.1.2.1.2 Omega-3 Fatty Acids

-

1.1.2.1.3 Probiotics

-

1.1.2.1.4 Proteins and Peptides

-

1.1.2.1.5 Vitamins and Minerals

-

1.1.2.1.6 Other Nutraceuticals

-

-

-

1.1.3 Pet Treats

-

1.1.3.1 By Sub Product

-

1.1.3.1.1 Crunchy Treats

-

1.1.3.1.2 Dental Treats

-

1.1.3.1.3 Freeze-dried and Jerky Treats

-

1.1.3.1.4 Soft & Chewy Treats

-

1.1.3.1.5 Other Treats

-

-

-

1.1.4 Pet Veterinary Diets

-

1.1.4.1 By Sub Product

-

1.1.4.1.1 Diabetes

-

1.1.4.1.2 Digestive Sensitivity

-

1.1.4.1.3 Oral Care Diets

-

1.1.4.1.4 Renal

-

1.1.4.1.5 Urinary tract disease

-

1.1.4.1.6 Other Veterinary Diets

-

-

-

-

1.2 Pets

-

1.2.1 Cats

-

1.2.2 Dogs

-

1.2.3 Other Pets

-

-

1.3 Distribution Channel

-

1.3.1 Convenience Stores

-

1.3.2 Online Channel

-

1.3.3 Specialty Stores

-

1.3.4 Supermarkets/Hypermarkets

-

1.3.5 Other Channels

-

-

1.4 Region

-

1.4.1 Africa

-

1.4.1.1 By Country

-

1.4.1.1.1 South Africa

-

1.4.1.1.2 Rest of Africa

-

-

-

1.4.2 Asia-Pacific

-

1.4.2.1 By Country

-

1.4.2.1.1 Australia

-

1.4.2.1.2 China

-

1.4.2.1.3 India

-

1.4.2.1.4 Indonesia

-

1.4.2.1.5 Japan

-

1.4.2.1.6 Malaysia

-

1.4.2.1.7 Philippines

-

1.4.2.1.8 Taiwan

-

1.4.2.1.9 Thailand

-

1.4.2.1.10 Vietnam

-

1.4.2.1.11 Rest of Asia-Pacific

-

-

-

1.4.3 Europe

-

1.4.3.1 By Country

-

1.4.3.1.1 France

-

1.4.3.1.2 Germany

-

1.4.3.1.3 Italy

-

1.4.3.1.4 Netherlands

-

1.4.3.1.5 Poland

-

1.4.3.1.6 Russia

-

1.4.3.1.7 Spain

-

1.4.3.1.8 United Kingdom

-

1.4.3.1.9 Rest of Europe

-

-

-

1.4.4 North America

-

1.4.4.1 By Country

-

1.4.4.1.1 Canada

-

1.4.4.1.2 Mexico

-

1.4.4.1.3 United States

-

1.4.4.1.4 Rest of North America

-

-

-

1.4.5 South America

-

1.4.5.1 By Country

-

1.4.5.1.1 Argentina

-

1.4.5.1.2 Brazil

-

1.4.5.1.3 Rest of South America

-

-

-

-

Pet Food Market Size FAQs

How big is the Pet Food Market?

The Pet Food Market size is expected to reach USD 192.51 billion in 2024 and grow at a CAGR of 8.54% to reach USD 290.01 billion by 2029.

What is the current Pet Food Market size?

In 2024, the Pet Food Market size is expected to reach USD 192.51 billion.