Market Size of Global Patient-centric Health Care App Industry

| Study Period | 2019 - 2029 |

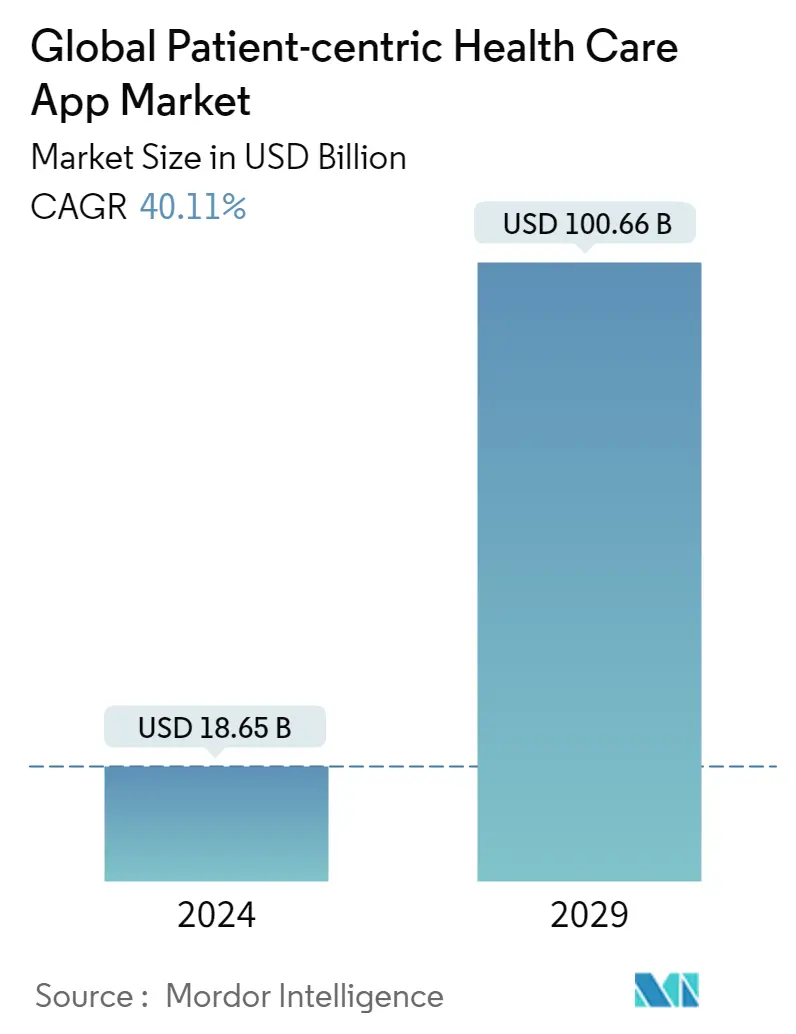

| Market Size (2024) | USD 18.65 Billion |

| Market Size (2029) | USD 100.66 Billion |

| CAGR (2024 - 2029) | 40.11 % |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

Major Players*Disclaimer: Major Players sorted in no particular order |

Patient Centric Healthcare App Market Analysis

The Global Patient-centric Health Care App Market size is estimated at USD 18.65 billion in 2024, and is expected to reach USD 100.66 billion by 2029, growing at a CAGR of 40.11% during the forecast period (2024-2029).

The COVID-19 pandemic had an impact on the healthcare industry. The outbreak of COVID-19 led to disruption, challenges, limitations, and changes in every industry sector. The pandemic also impacted the studied market. The outbreak of COVID-19 showed a positive impact on the market, as lockdowns led to the lower availability of doctors in clinical settings.

Thus, patients were more inclined to use apps to manage their chronic conditions, such as diabetes, hypertension, and other chronic diseases. Moreover, there have been a large number of patient care apps launched for COVID-19 management. Nationwide lockdowns resulted in providing healthcare services by the hospitals and clinics, which led to the rise in the use of patient-centric healthcare app that aims toward the management of diseases.

For instance, according to a research study by Haridimos Kondylakis et al., published in the Journal of Medical Internet Research in December 2020, mobile apps were considered to be a valuable tool for health professionals, citizens, and decision-makers in facing critical challenges imposed by the pandemic such as reducing the burden on hospitals, tracking the symptoms and mental health of individuals, providing access to credible information, and discovering new predictors, leading to the high adoption of mobile health apps across the industry both from providers and consumers.

The major factors driving the market growth include the increased incidence of chronic disorders, such as cancers, diabetes, and rheumatoid arthritis, especially in the geriatric population. Treating chronic diseases requires continuous monitoring and evaluation of physiological changes for proper diagnosis and medication.

For instance, as per the IDF Diabetes Atlas Tenth edition 2021, in 2021, about 537 million adults were living with diabetes. The total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045. The increasing number of diabetes patients drives them to demand more monitoring apps and drives the market

According to World Health Organization (WHO) data published in October 2021, between 2015 and 2050, the proportion of the global population over 60 years will nearly double from 12% to 22% in 2050, and 80% of older people will be living in low- and middle-income countries. All countries face major challenges in ensuring their health and social systems are ready to make the most of this demographic shift. Thus, healthcare apps come in the role of monitoring vital parameters. This is expected to drive the market. Thus, the growing elderly population, rise in government initiatives to maintain electronic health record systems, and increased demand for technology-based treatment to avoid medication errors are likely to drive the patient-centric healthcare app (PCHA) market over the forecast period.

Patient Centric Healthcare App Industry Segmentation

As per the scope of the report, patient-centric health care apps are applications that run on various technological devices and help patients with their health conditions, and physicians deliver the services on their premises. These apps help provide easier access to health information, such as series of cardiac events, dehydration levels in the body, the number of calories consumed, and other medical insights that improve quality of life. The global patient-centric health care app market is segmented by mode of operation (phone-based, web-based, and hybrid patient-centric apps), application (wellness management, disease and treatment management, and other applications), and geography (North America, Europe, Asia-Pacific, Middle-East and Africa, and South America). The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the segments mentioned above.

| By Mode of Operation | |

| Phone-based | |

| Web-based | |

| Hybrid Patient-centric Apps |

| By Application | |

| Wellness Management | |

| Disease And Treatment Management | |

| Other Applications |

| By Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Global Patient-centric Health Care App Market Size Summary

The patient-centric healthcare app market is poised for significant growth, driven by the increasing prevalence of chronic diseases and the rising geriatric population. The COVID-19 pandemic acted as a catalyst, accelerating the adoption of mobile health applications as patients sought alternatives to in-person consultations. This shift was facilitated by the need for continuous monitoring and management of conditions such as diabetes and hypertension, which are prevalent among older adults. The market is characterized by a surge in the development and deployment of apps aimed at managing chronic conditions, providing healthcare services, and enhancing patient engagement. The integration of technology in healthcare, supported by government initiatives and the growing demand for telehealth services, is expected to further propel the market's expansion.

North America is anticipated to maintain its dominance in the patient-centric healthcare app market, attributed to its large population with chronic health issues and a robust healthcare infrastructure. The region's focus on technology adoption and patient-centric care models is driving the market forward. The competitive landscape is moderately active, with key players engaging in strategic initiatives such as mergers, acquisitions, and technological advancements to strengthen their market positions. Companies like Siemens Healthineers AG, Koninklijke Philips NV, and Bayer AG are at the forefront, leveraging innovations to enhance their offerings. The market's growth trajectory is supported by the increasing healthcare expenditure, heightened health awareness, and a shift towards digital health solutions, which are expected to shape the industry's future over the forecast period.

Global Patient-centric Health Care App Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Increasing Prevalence of Chronic Diseases and Rising Geriatric Population

-

1.2.2 Enhanced Access and Flexibility with Novel Technologies

-

-

1.3 Market Restraints

-

1.3.1 The High Cost of Development

-

1.3.2 Reluctance by Regular Healthcare Providers

-

-

1.4 Porter's Five Force Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 By Mode of Operation

-

2.1.1 Phone-based

-

2.1.2 Web-based

-

2.1.3 Hybrid Patient-centric Apps

-

-

2.2 By Application

-

2.2.1 Wellness Management

-

2.2.2 Disease And Treatment Management

-

2.2.3 Other Applications

-

-

2.3 By Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

2.3.1.3 Mexico

-

-

2.3.2 Europe

-

2.3.2.1 Germany

-

2.3.2.2 United Kingdom

-

2.3.2.3 France

-

2.3.2.4 Italy

-

2.3.2.5 Spain

-

2.3.2.6 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 Japan

-

2.3.3.3 India

-

2.3.3.4 Australia

-

2.3.3.5 South Korea

-

2.3.3.6 Rest of Asia-Pacific

-

-

2.3.4 Middle-East and Africa

-

2.3.4.1 GCC

-

2.3.4.2 South Africa

-

2.3.4.3 Rest of Middle-East and Africa

-

-

2.3.5 South America

-

2.3.5.1 Brazil

-

2.3.5.2 Argentina

-

2.3.5.3 Rest of South America

-

-

-

Global Patient-centric Health Care App Market Size FAQs

How big is the Global Patient-centric Health Care App Market?

The Global Patient-centric Health Care App Market size is expected to reach USD 18.65 billion in 2024 and grow at a CAGR of 40.11% to reach USD 100.66 billion by 2029.

What is the current Global Patient-centric Health Care App Market size?

In 2024, the Global Patient-centric Health Care App Market size is expected to reach USD 18.65 billion.