Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 436.63 Billion |

| Market Size (2031) | USD 547.52 Billion |

| Growth Rate (2026 - 2031) | 4.63% CAGR |

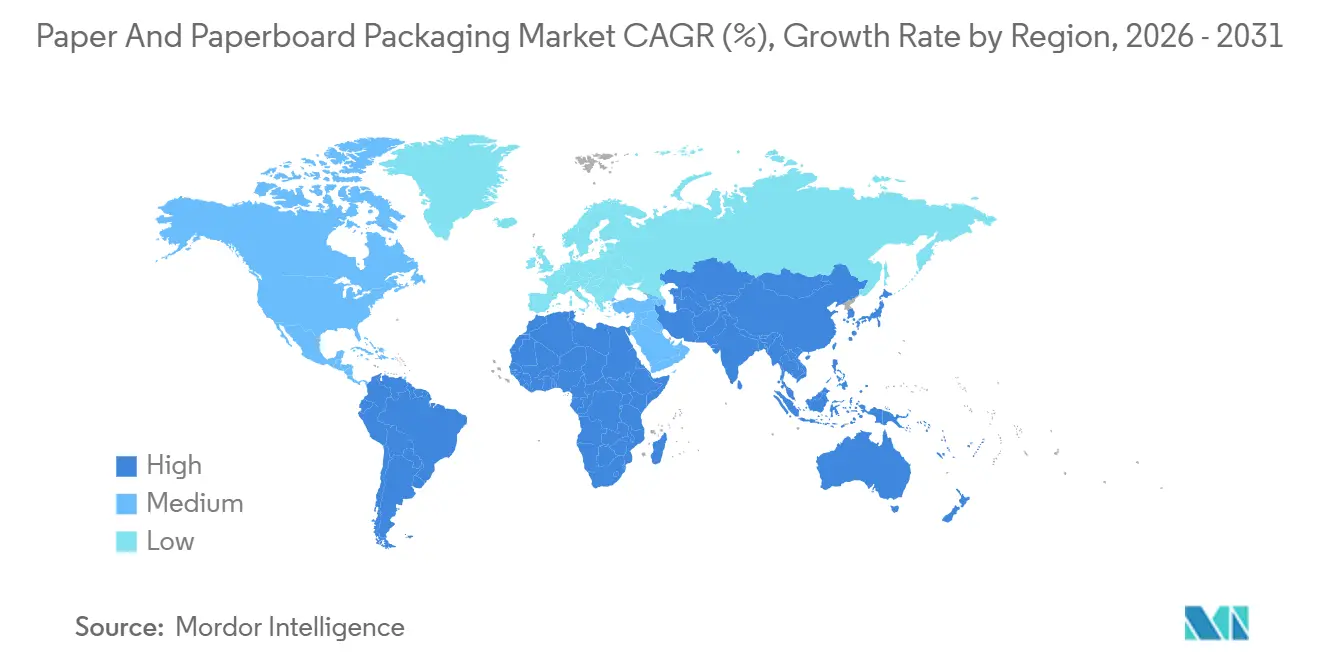

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Paper And Paperboard Packaging Market Analysis by Mordor Intelligence

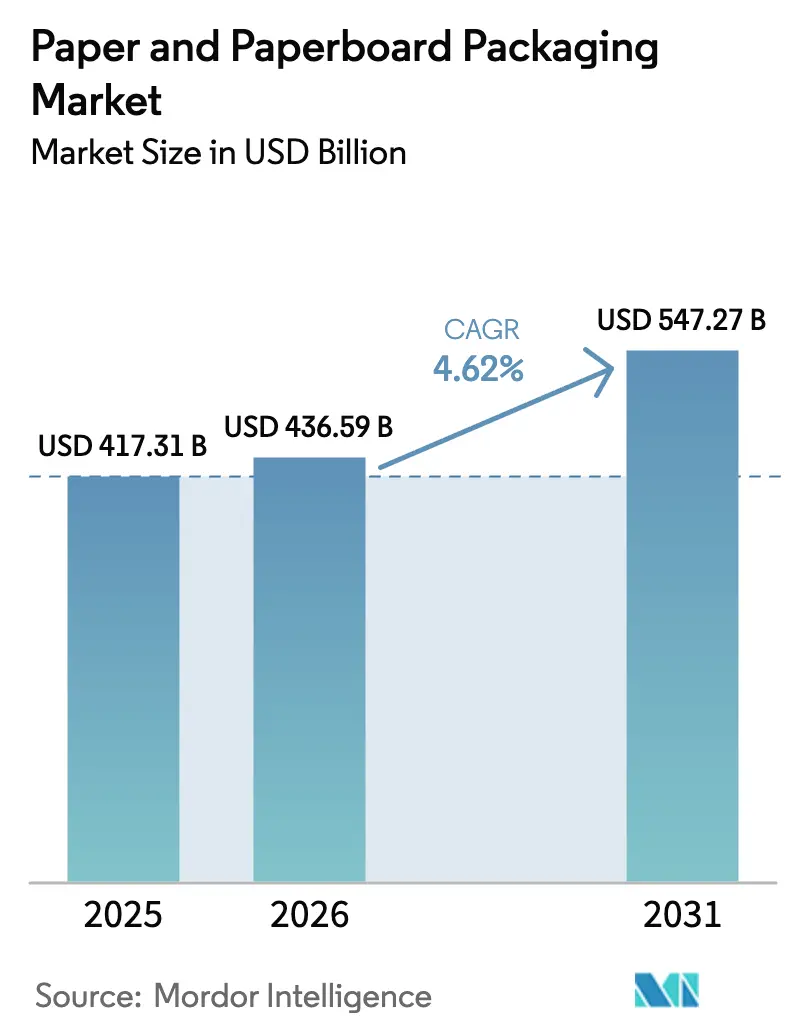

The Paper And Paperboard Packaging Market size is expected to grow from USD 417.31 billion in 2025 to USD 436.63 billion in 2026 and is forecast to reach USD 547.52 billion by 2031 at 4.63% CAGR over 2026-2031.

Continuous substitution of rigid plastics with fiber-based formats, widening e-commerce adoption, and policy-driven sustainability premiums keep demand resilient. Corrugated boxes and molded-fiber trays remain the most effective options for brands that must balance weight, strength, and recyclability, and converters are accelerating investments in digital print lines to serve high-mix, low-volume product launches. Extended producer responsibility laws are tightening post-consumer content thresholds, while retail right-sizing programs are shrinking box, cube, and corrugate consumption. At the same time, volatile old-corrugated-container and virgin-pulp prices compress margins for converters that lack hedging or vertically integrated fiber supply.

Key Report Takeaways

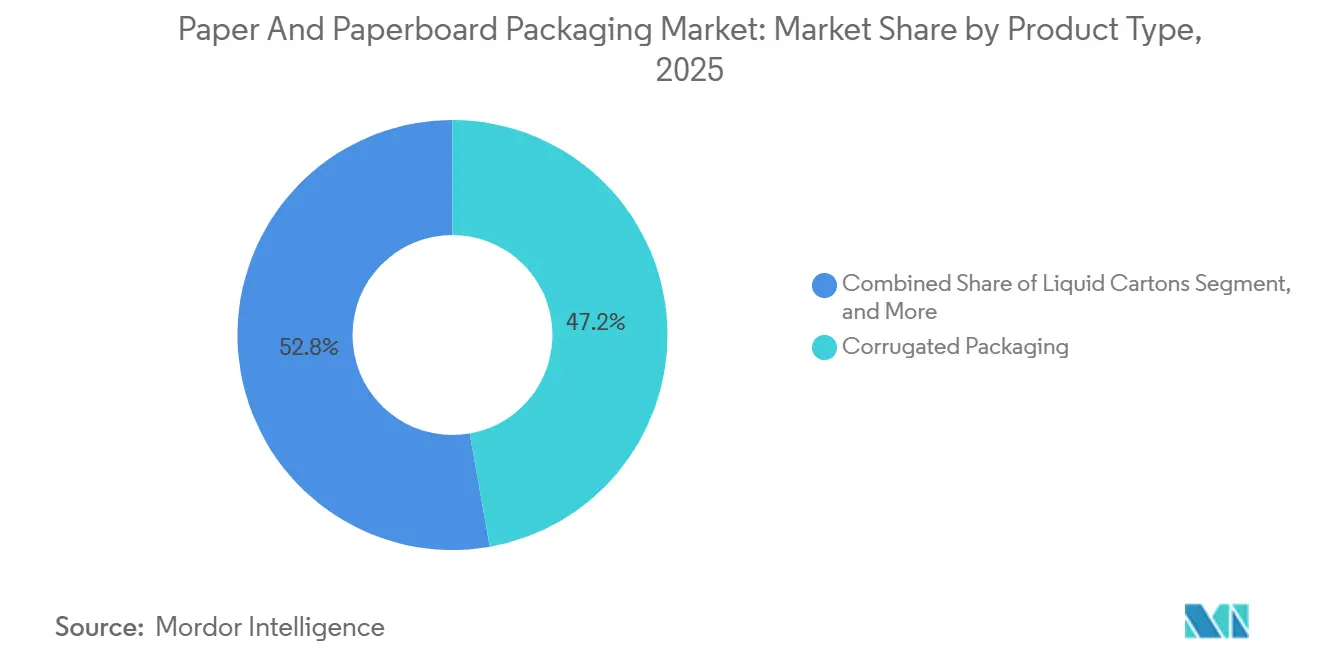

- By product type, corrugated packaging led with 47.23% of paper and paperboard packaging market share in 2025, while liquid cartons are forecast to expand at a 5.44% CAGR through 2031.

- By end-user vertical, food and beverage accounted for 38.64% of 2025 revenue, whereas healthcare and pharma are advancing at a 5.61% CAGR to 2031.

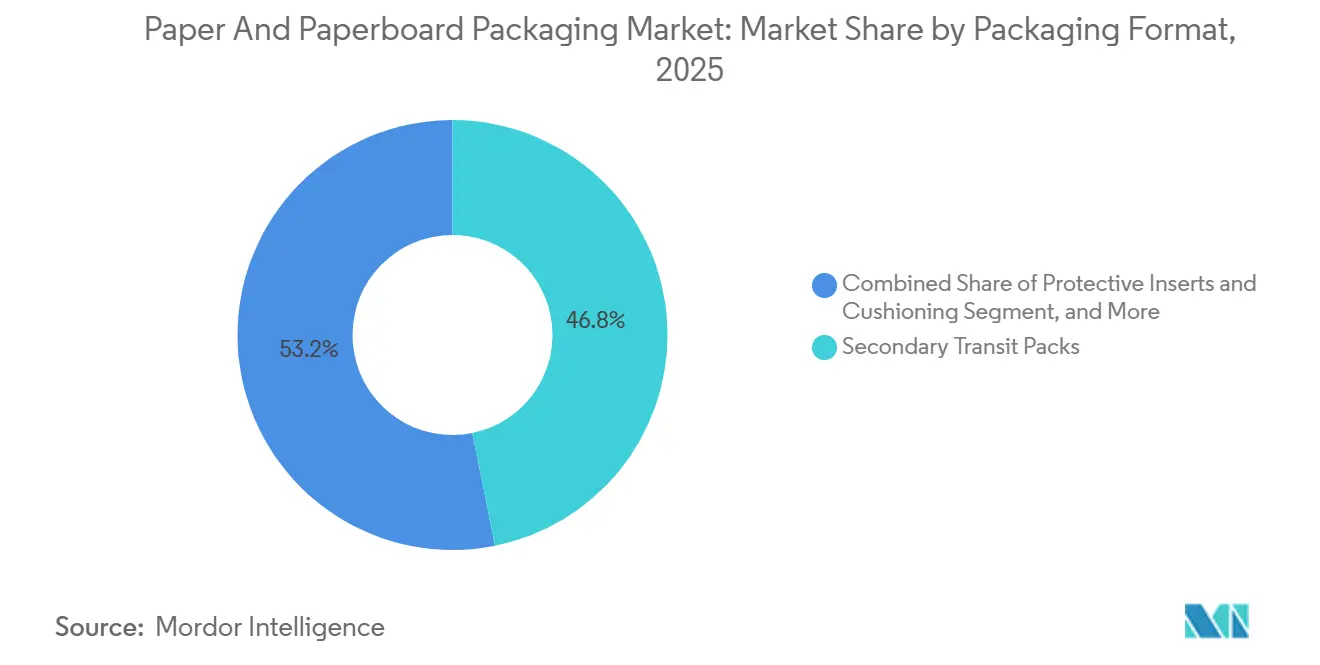

- By packaging format, secondary transit packs held a 46.83% of paper and paperboard packaging market share in 2025, yet protective inserts are climbing at a 5.49% CAGR during the forecast period.

- By material grade, recycled fiber represented 53.67% of paper and paperboard packaging market share in 2025, and hybrid and mixed-fiber blends are growing at a 5.23% CAGR between 2026 and 2031.

- By geography, Asia-Pacific accounted for 43.89% of global demand in 2025, while Africa is the fastest-growing region, with a 5.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Paper And Paperboard Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce-Led SKU Explosion | +1.2% | Global, strongest in North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Plastic Use Bans and Taxes | +0.9% | Global, led by Europe, North America, select Asia-Pacific markets | Medium term (2-4 years) |

| Quick-Service Food Expansion in Tier-2 Cities | +0.7% | Asia-Pacific, Africa, South America | Medium term (2-4 years) |

| Rise of Industrial Composting Standards | +0.5% | North America, Europe, emerging Asia-Pacific | Medium term (2-4 years) |

| Direct-to-Consumer Pharma Fulfilment | +0.4% | Global, earliest in North America and Europe | Short to medium term (≤ 4 years) |

| Sustainability-Driven Packaging Shift | +0.6% | Global, premium-brand leadership in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce-Led SKU Explosion

Online retail platforms added thousands of stock-keeping units in 2025, and parcel volumes grew in double digits in North America and Europe, while average parcel weights fell as shoppers favored smaller, more frequent orders. Converters responded with digital presses and on-demand die-cutters, enabling them to produce short-run boxes at line speeds once reserved for long-run jobs. Retailers introduced right-sizing protocols that lowered corrugate use by up to 20%, so converters must now optimize board grade, print customization, and board geometry in tandem. The trend also fuels demand for premium unboxing elements such as printed inserts and tissue wraps, which turn corrugated mailers into marketing touchpoints.

Plastic Use Bans and Taxes

The United Kingdom began levying GBP 200 per tonne on non-compliant plastic packs in April 2025, the European Union instructed that all food-contact packs be recyclable or compostable by 2030, and California mandated a 25% cut in single-use plastics by 2032. These measures accelerated brand migration from foam and film to molded-fiber clamshells, barrier-coated paperboard trays, and grease-resistant wraps.[1]European Commission, “Packaging and Packaging Waste Regulation,” ec.europa.eu Converters that can certify a minimum of 30 % recycled content or validated compostability now command volume commitments from global food-service chains.

Quick-Service Food Expansion in Tier-2 Cities

Restaurant chains grew fastest in India, Indonesia, and Nigeria in 2025, where food delivery app downloads rose by 20% to 30%. Grease and humidity push brands toward dispersion-coated or aqueous-coated paperboard that resists moisture without laminated polyethylene. Franchisees in these markets keep margins tight, so they prefer unbleached kraft and lightweight grades that cost 10 % less than bleached substrates while still passing migration and strength tests.

Rise of Industrial Composting Standards

North American and European certifiers tightened pass-fail thresholds for compostable packaging, requiring 90% disintegration within 84 days and a residue below 1% after 12 weeks.[2]Biodegradable Products Institute, “BPI Certification Standards Update,” bpiworld.org These stricter metrics favor uncoated or water-based coated boards and push suppliers to adopt bio-based coatings derived from polylactic acid or polyhydroxyalkanoates. Although such coatings raise unit cost by up to 40%, they grant access to municipal organic waste schemes that divert waste from landfill.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile OCC and Virgin Pulp Prices | –0.8% | Global, highest in import-dependent markets | Short to medium term (≤ 4 years) |

| Deforestation-Driven NGO Pressure | –0.3% | Global, sourcing regions with weak governance | Medium to long term (≥ 2 years) |

| In-House Corrugation by Mega-Etailers | –0.4% | North America, Asia-Pacific | Medium term (2-4 years) |

| Carbon-Border Adjustment Costs | –0.3% | Europe and exporting nations | Short to medium term (≤ 4 years) |

| Source: Mordor Intelligence | |||

Volatile OCC and Virgin Pulp Prices

Old-corrugated-container prices swung 30 % to 40 % in 2025, moving between USD 80 and USD 130 per short ton in the United States, while northern bleached softwood kraft pulp rose from USD 1,100 to USD 1,350 per tonne. Without futures markets, converters find themselves vulnerable to price volatility. As a result, many opt to pass quarterly surcharges downstream to manage their financial risks. However, this approach often puts a strain on their relationships with brand owners, who are tied to annual price lists and may face challenges in absorbing these additional costs.

Deforestation-Driven NGO Pressure

Greenpeace satellite images linked several Southeast Asian mills to primary forest loss in 2025, prompting retailer delistings and boycotts.[3]Greenpeace, “Deforestation and Pulp Mill Sourcing Practices,” greenpeace.org Certification schemes added tighter traceability rules down to the forest management unit, but smallholders in Africa and South America struggled to cover audit costs, slowing certified acreage growth to only 2%. Brand owners now pay premiums to integrated producers that can document end-to-end custody, leaving spot-market buyers exposed to reputational risk.

Segment Analysis

By Product Type: Corrugated Strength Meets Carton Innovation

Corrugated packaging accounted for 47.23% of the paper and paperboard packaging market share in 2025, underscoring its unrivaled cost-to-strength performance for palletized logistics. Liquid cartons, aided by aseptic barrier breakthroughs that remove polyethylene layers, are on track to grow at 5.44% through 2031, outpacing the overall paper and paperboard packaging market. In single-serve beverages, formats under 200 ml delivered 12% volume growth in Asia-Pacific quick-service channels in 2025. Brand owners now view carton innovation as an enabler for ambient dairy and plant-based drinks where cold-chain gaps persist. Folding cartons hold their own in cosmetics and confectionery because litho print quality and rigid edges justify a 15% to 20% price premium over micro-flute corrugated. Digital hybrid presses let converters profitably serve limited-edition runs, shrinking setup fees that once discouraged niche SKUs.

Competition is widening between rigid boxes, composite cans, and molded-fiber shells in luxury gifting, where tactile finishing and circularity claims carry equal weight. Robust adoption of digital finishing lowers minimum order quantities, supporting influencer-driven launches that demand box deliveries in weeks rather than months. Corrugated still dominates heavy goods due to bursting strengths above 275 psi, and honeycomb paperboard is displacing solid fiberboard in white-goods shipments because it provides >1,000 psi compression at lower density.

Note: Segment shares of all individual segments available upon report purchase

By End-User Vertical: Food Staples and Pharma Momentum

Food and beverage retained the largest slice of value at 38.64% in 2025, with cereal cartons, produce trays, and shelf-ready packs anchoring consumption. Demand for branded fresh fruit packaging lifted orders for mold-resistant coatings that extend shelf life in humid climates. Healthcare and pharma are the fastest risers, advancing at a 5.61% CAGR as global serialization deadlines require tamperproof folding cartons embedded with holograms, RFID inlays, and scannable data matrix codes. Cold-chain biologics are riding a surge in e-pharmacy channels, where corrugated shippers loaded with phase-change materials maintain 2°C to 8°C for up to 4 days.

Personal care and cosmetics thrive on tactile differentiation, such as embossing and soft-touch coatings, which translate into shelf premiums. Electronics brands are integrating antistatic coatings and molded-pulp buffers to replace polystyrene, meeting International Safe Transit Association 3A drop-test requirements with lighter materials. In the automotive and industrial applications, heavy-duty double-wall boards with >40% virgin long fiber meet stacking and racking requirements in tiered distribution centers.

By Packaging Format: Transit Boxes Rule, Inserts Accelerate

Secondary transit packs accounted for 46.83% of 2025 shipments, reflecting the centrality of corrugated shippers in e-commerce, grocery, and wholesale hubs. Parcel carriers impose surcharges once boxes exceed a 108-inch length-plus-girth, so right-sizing software now computes optimal cube in real time, shaving freight costs and board usage. Protective inserts and cushioning lines are advancing at a 5.49% CAGR following retailers' pledges to remove foam and bubble wrap from online orders. Molded-fiber inserts cut the package cube by 10% to 15% and pass 32-inch drop tests that once required expanded polystyrene.

Primary retail packs focus on shelf appeal and brand storytelling, merging QR codes and near-field communication tags to connect shoppers to recipe videos and carbon footprint information. Shelf-ready displays, equipped with perforated tear-strips, let store associates convert cases to displays in under 30 seconds, saving about USD 0.75 labor per unit. RFID at the case level gains traction in high-value cosmetics, cutting out-of-stocks and shrink.

Note: Segment shares of all individual segments available upon report purchase

By Material Grade: Blends Balance Cost and Strength

Recycled fiber accounted for 53.67% of volume in 2025, driven by minimum post-consumer thresholds in Europe and North America. Yet mechanical degradation limits fiber reuse to roughly 7 loops, so converters increasingly blend 20% to 30% virgin long fiber to meet burst and puncture tests without inflating basis weight. Hybrid grades are expanding at 5.23 % CAGR, giving converters room to lightweight corrugated from 200 gsm to 180 gsm and save USD 0.03 per case on long-haul freight.

Virgin fiber still dominates direct-food-contact packs, where regulators cap mineral oil and phthalate transfer from recycled layers. European quick-service chains replaced fluorochemical grease barriers with virgin-pulp-based dispersion coatings that meet burger wrap oil-repellency at half the migration thresholds allowed in 2019. Hybrid blends unlock both cost and performance, supporting shelf-ready cases that need strong corners while claiming>70% recycled content.

Geography Analysis

Asia-Pacific accounted for 43.89% of 2025 global demand, bolstered by Chinese, Indian, and Southeast Asian capacity additions, as well as national policies that tightened contamination limits on imported wastepaper. China’s extended National Sword directive capped contamination at 0.3%, prompting local mills to invest in advanced optical sorting and de-inking lines. Nine Dragons Paper spent CNY 2 billion (USD 280 million) on its Dongguan upgrade, proving that domestic recovered fiber can meet box plant furnish specs. India outlawed multilayer plastic sachets below 120 microns, prompting detergent and shampoo brands to pivot to lightweight paper pouches that meet sub-USD 0.12 retail price points.

Africa delivers the fastest expansion, with a 5.67% CAGR through 2031. Urban populations in Lagos, Nairobi, and Johannesburg are growing by 3.5% annually, nurturing modern retail and fast-food chains that demand branded takeaway packs. South Africa enforced extended producer responsibility in 2024, obliging pack producers to fund collection and recycling, which accelerated investment in mixed-fiber material recovery. Egypt earmarked USD 500 million for three integrated pulp-and-paper complexes in the Nile Delta to trim its 40% import dependency recorded in 2024.

North America and Europe collectively accounted for roughly 35 % of 2025 volumes. Energy and wage inflation lifted conversion costs by 8% to 12%, so several U.S. box makers opened satellite plants in northern Mexico, taking advantage of tariff-free provisions under the United States-Mexico-Canada Agreement. Europe’s 2025 Packaging and Packaging Waste Regulation requires all packs to be recyclable by 2030 and sets a 65 % recycled-content floor for fiber by 2035, fueling capex in closed-loop systems across Germany, France, and the Netherlands. Germany’s deposit return scheme boosted beverage-carton collection to 85% within one year, signaling momentum for similar programs across the bloc.

Competitive Landscape

The competitive field is moderately concentrated, with the five largest suppliers accounting for about one-third of installed capacity worldwide, leaving significant space for regional converters focused on niche formats such as molded-fiber inserts or high-barrier cartons. Smurfit Kappa and WestRock completed their USD 34 billion merger in July 2025, creating a single entity that now operates more than 500 converting sites and can leverage global fiber procurement to offset raw-material swings. International Paper broadened its Asian footprint in December 2025 by acquiring a 60% stake in a joint venture with Hengan International, pairing corrugation expertise with a fast-moving consumer goods distribution network targeting USD 500 million in annual sales by 2028. Mondi followed with a EUR 150 million expansion at its Štětí mill, adding 200,000 tonnes of kraft paper capacity and an in-line water-resistant coating, strengthening its position in fresh produce and e-commerce sleeves.

Vertical integration by e-commerce giants is reshaping supply economics, as Amazon and Alibaba continue installing on-site corrugation lines that reportedly trim per-box costs by up to 15 %, pressuring independent converters to differentiate through services such as design, kitting, and fulfillment support. To maintain margins, many established box makers have accelerated automation; vision-guided quality-control systems now flag print or die-cut defects at line speeds exceeding 500 feet per minute, lifting first-pass yield by roughly 3 %. Sustainability-driven innovation offers another path to premium pricing, as illustrated by DS Smith’s 2025 algae-based grease-barrier patent that removes fluorochemicals while still meeting food-service oil-repellency tests. Smaller specialists, often backed by private equity, are targeting molded-fiber trays, electronics cushioning, and digitally printed short-run cartons where large multinationals have less scale advantage.

Strategic alliances and divestitures support portfolio rationalization. Packaging Corporation of America is locked in a 10-year supply agreement with a leading North American online retailer that links pricing to market OCC indices, reducing margin volatility while guaranteeing 500,000 tonnes of annual volume. Stora Enso’s Imatra biocomposite line turns pulp sidestreams into molded shells for quick-service meals, cutting reliance on external fiber and positioning the firm for compostable takeaway formats. Nippon Paper’s Tokyo carton-collection pilot achieved a 78 % recovery rate in six months and signals how closed-loop programs can build brand credibility with retailers that publish recycled-content scorecards. With regional specialists still active and global leaders actively automating, integrating, and greening their portfolios, competitive intensity is likely to remain elevated even as demand expands at a steady 4% to 5% pace.

Paper And Paperboard Packaging Industry Leaders

International Paper Company

Smurfit Westrock plc

Mondi plc

Packaging Corporation of America

Stora Enso Oyj

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Mondi announced a EUR 150 million (USD 165 million) expansion at its Štětí mill in the Czech Republic, adding 200,000 tonnes of kraft-paper capacity.

- December 2025: International Paper acquired 60 % of a joint venture with Hengan International Group in southern China, targeting USD 500 million revenue by 2028.

- November 2025: Stora Enso started a EUR 120 million (USD 132 million) biocomposite line at Imatra, making molded-fiber trays from pulp sidestreams.

- October 2025: Packaging Corporation of America signed a decade-long deal to supply 500,000 tonnes of corrugated boxes a year to a North American e-commerce retailer.

Global Paper And Paperboard Packaging Market Report Scope

The Paper and Paperboard Packaging Market Report is Segmented by Product Type (Folding Cartons, Corrugated Packaging, Liquid Cartons, Other Product Types), End-User Vertical (Food and Beverage, Healthcare and Pharma, Personal Care and Cosmetics, Electrical and Electronics, Industrial and Automotive), Packaging Format (Primary Retail Packs, Secondary Transit Packs, Shelf-Ready / Display Packs, Protective Inserts and Cushioning), Material Grade (Virgin Fiber, Recycled Fiber, Hybrid / Mixed Fiber), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Folding Cartons |

| Corrugated Packaging |

| Liquid Cartons |

| Other Product Types |

By End-User Vertical

| Food and Beverage |

| Healthcare and Pharma |

| Personal Care and Cosmetics |

| Electrical and Electronics |

| Industrial and Automotive |

By Packaging Format

| Primary Retail Packs |

| Secondary Transit Packs |

| Shelf-Ready / Display Packs |

| Protective Inserts and Cushioning |

By Material Grade

| Virgin Fiber |

| Recycled Fiber |

| Hybrid / Mixed Fiber |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Product Type | Folding Cartons | ||

| Corrugated Packaging | |||

| Liquid Cartons | |||

| Other Product Types | |||

| By End-User Vertical | Food and Beverage | ||

| Healthcare and Pharma | |||

| Personal Care and Cosmetics | |||

| Electrical and Electronics | |||

| Industrial and Automotive | |||

| By Packaging Format | Primary Retail Packs | ||

| Secondary Transit Packs | |||

| Shelf-Ready / Display Packs | |||

| Protective Inserts and Cushioning | |||

| By Material Grade | Virgin Fiber | ||

| Recycled Fiber | |||

| Hybrid / Mixed Fiber | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 value of the paper and paperboard packaging market?

The paper and paperboard packaging market is expected to reach USD 436.63 billion in 2026.

Which segment currently holds the largest share?

Corrugated packaging led with 47.23 % of paper and paperboard packaging market share in 2025.

Which region is expanding the fastest through 2031?

Africa is projected to grow at a 5.67 % CAGR during 2026-2031.

Why are healthcare companies increasing fiber-based pack use?

Serialization laws in the United States and European Union drive demand for tamper-evident, track-and-trace paperboard cartons, lifting the healthcare segment at a 5.61 % CAGR.

How are retailers reducing corrugate consumption?

E-commerce right-sizing software customizes box dimensions, trimming corrugated use by up to 20 % per shipment while cutting dimensional-weight fees.

Page last updated on: