| Study Period | 2021 - 2030 |

| Market Size (2025) | USD 195.96 Billion |

| Market Size (2030) | USD 247.74 Billion |

| CAGR (2025 - 2030) | 4.80 % |

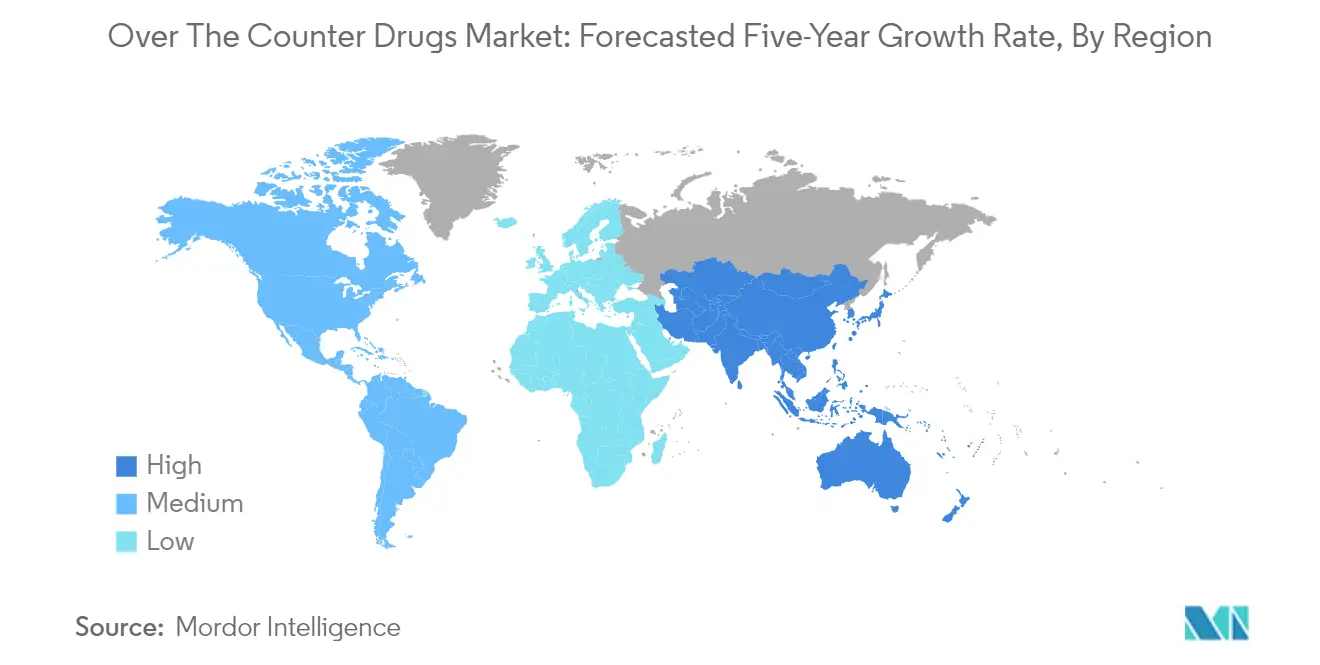

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

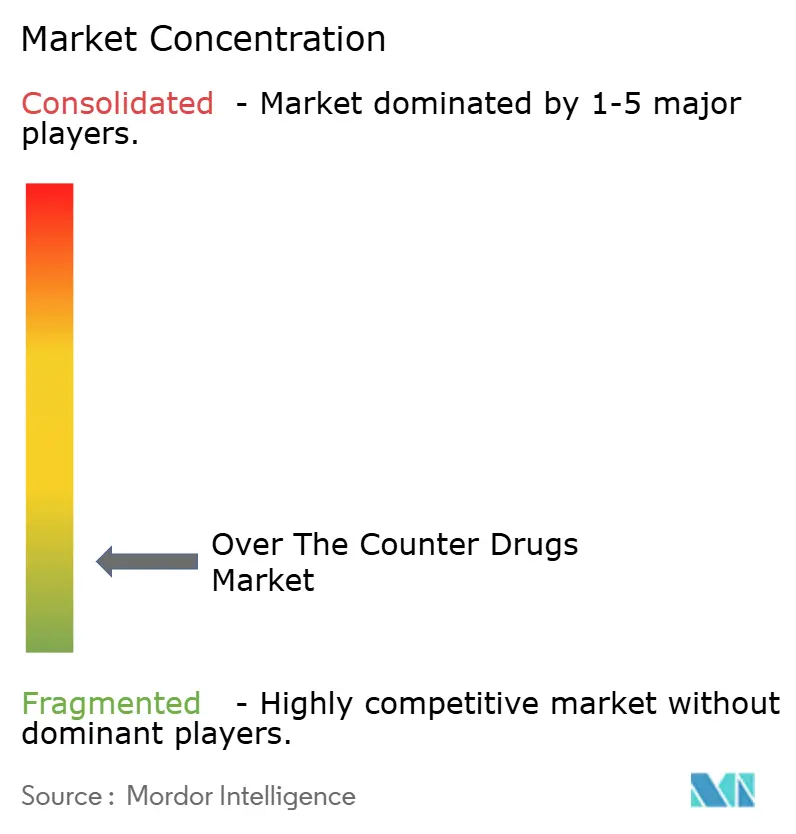

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Over The Counter Drugs Market Analysis

The Over The Counter Drugs Market size is estimated at USD 195.96 billion in 2025, and is expected to reach USD 247.74 billion by 2030, at a CAGR of 4.80% during the forecast period (2025-2030).

Regulatory Fluency: From Compliance Burden to Competitive Edge

The over the counter (OTC) drugs market now operates in a complex regulatory landscape that requires manufacturers to be highly adaptable. In the United States, the guidance for OTC medication in Title 21 was updated as recently as February 25, 2025, affecting global supply chains and product development. This ongoing regulatory change means companies need to maintain flexible compliance systems. The rule that an OTC drug condition must have been marketed for at least 5 continuous years in the same country to qualify for the monograph system highlights the need for consistent market presence and thorough documentation. These evolving regulations require significant investment in regulatory intelligence and compliance tools. Companies with advanced regulatory tracking gain advantages in bringing products to market quickly and operating efficiently. The key takeaway for otc companies is straightforward: regulatory compliance should be viewed not as just a cost, but as a strategic asset that enables market access and competitive advantage. Organizations that build capabilities to effectively navigate regulations while staying compliant will create significant value compared to competitors who merely react to compliance requirements.

The Channel Evolution: Physical-Digital Integration Redefines Access

While retail pharmacies still play a central role in the otc drug market, digital channels are creating new ways to reach consumers. Physical stores remain important, but the growth of online pharmacy platforms has created a mixed distribution system that manufacturers need to approach strategically. This digital shift goes beyond just selling products online to include new ways of engaging consumers before they make a purchase. The FDA's proposed rule for switching prescription drugs to OTC with additional conditions points to more products potentially becoming available through digital channels, creating new opportunities for consumer education. Major pharma OTC companies are now developing strategies that integrate both physical and digital approaches rather than treating them separately. The requirement for companies to report any failures in Additional Conditions for Nonprescription Use (ACNU) within 15 calendar days shows the regulatory oversight in this evolving landscape. Forward-looking companies are using this mix of channels to create smooth consumer experiences that build brand loyalty and trust. The important lesson for market participants is that distribution strategy has evolved from simply placing products in stores to managing a complex ecosystem that spans both physical and digital touchpoints throughout the consumer's journey.

Regional Regulatory Diversity: The Localization Imperative

The global OTC product market features vastly different regulations across regions, creating challenges for manufacturers with international operations. These differences appear in how products are classified, what packaging is required, and guidelines for use that demand market-specific approaches. In India, rules state that treatment with OTC drugs should not exceed five days, with package sizes limited accordingly - quite different from markets with more flexible guidelines. These regional differences create both challenges and opportunities. Companies that can adapt their supply chains and packaging systems can effectively serve multiple markets while meeting local requirements. These regulatory variations also affect decisions about product formulation, clinical development, and market entry strategies. OTC pharmaceutical products that succeed globally typically use flexible design approaches that can adapt to regional requirements without complete reformulation. The key insight for manufacturers is that regulatory differences should be considered from the beginning of product development rather than as an afterthought during commercialization. Organizations that build regulatory flexibility into their development process gain significant competitive advantages in international markets.

Over The Counter Drugs Market Trends

Prescription Price Pressures: Why Consumers Are Turning to OTC Alternatives

Rising prescription drug costs are pushing more consumers toward affordable over the counter drugs options. This cost-driven shift is changing buying patterns across all demographic groups, especially among budget-conscious consumers. Despite the slow pace of Rx-to-OTC switches in the US—only one in 2022 and two in 2023—consumer interest remains high. Manufacturers have noticed this trend and are expanding their OTC product lines with formulations that offer similar benefits at lower prices. This strategy creates value for consumers who increasingly see OTC medication as an affordable first option for managing their health.The growing price gap between prescription and otc medicine has changed what used to be a convenience choice into a financial necessity for many families. This isn't just about saving money today—it shows how consumers are taking a more active role in managing their healthcare costs through prevention and self-care. The FDA's 2023 approval of Eroxon as an OTC treatment for erectile dysfunction shows that regulators recognize the significance of OTC drugs in making healthcare more accessible. Smart retailers and drug companies are now focusing on consumer education programs that help people get the most benefit from OTC options while avoiding the risks of incorrect self-diagnosis.

Regulatory Progress: More OTC Drug Approvals on the Horizon

Regulatory agencies are gradually opening more pathways for over the counter medications as health authorities adopt more practical approaches to OTC classifications. In the US, after years of limited activity, the FDA showed new openness by approving Eroxon for erectile dysfunction as an OTC product in June 2023, marking an important step in giving consumers access to treatments that previously required prescriptions. This approval indicates that regulators increasingly believe properly labeled OTC drugs can safely treat certain conditions while reducing pressure on the healthcare system. Drug companies working in this area now have both new opportunities and responsibilities—they need to develop good consumer education while taking advantage of broader market access.This regulatory progress is especially noticeable in developing markets, where approval processes are being simplified to improve healthcare access. In May 2022, India's Ministry of Health drafted an amendment to exempt about 16 medications from prescription requirements, creating new growth opportunities in the otc drug market. These varying regional approaches create both challenges and opportunities for global pharmaceutical companies. The increase in OTC pharmaceutical products goes beyond just reclassifying existing drugs—it's driving companies to create new dosage forms, delivery methods, and ingredient combinations designed specifically for consumer self-selection. Companies that align their product development with these regulatory trends will gain advantage as more consumers look for effective, accessible, and affordable health solutions.

Segment Analysis: By Product Type

Cold & Flu Relief: The Cornerstone of OTC Markets

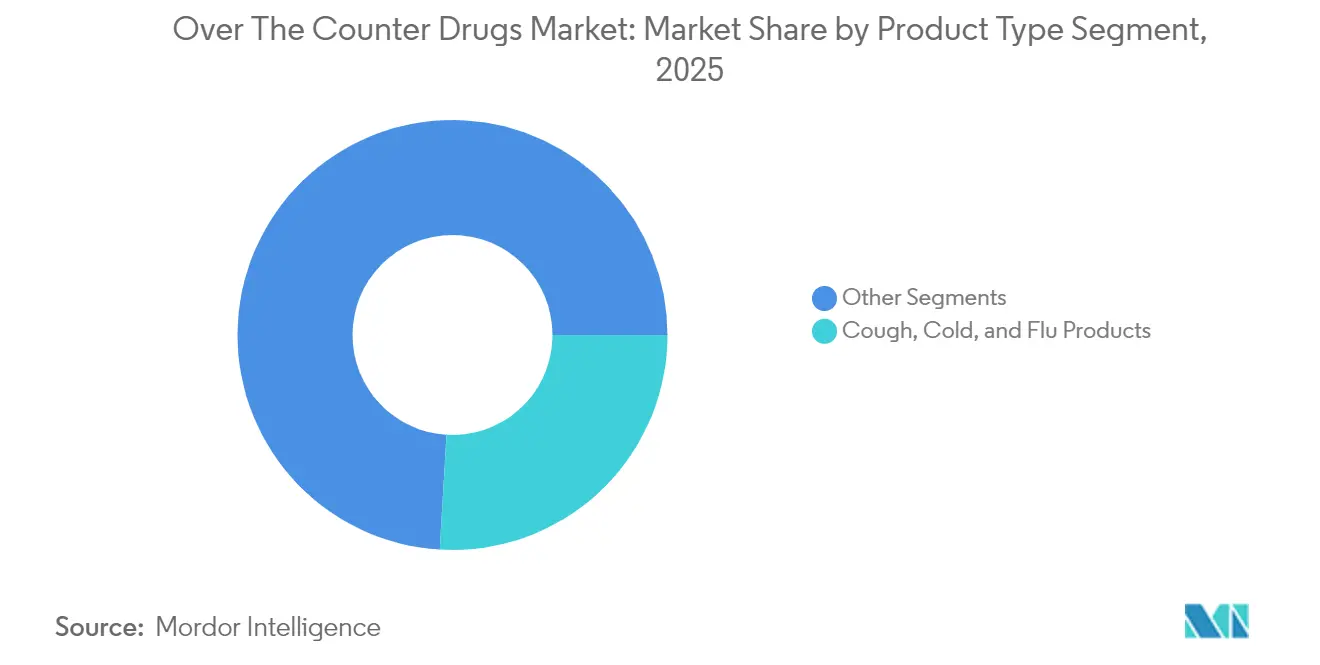

Cough, Cold, and Flu Products continue to anchor the over the counter drugs market with a commanding 25.95% market share, reflecting these products' essential role in consumer self-care regimens. This dominance stems from the ubiquitous nature of respiratory ailments, which affect virtually every demographic annually regardless of economic cycles. The segment's resilience has been reinforced by consumers' heightened health consciousness following global respiratory health concerns, driving them toward pre-emptive and early-intervention approaches. The true competitive edge for manufacturers lies in developing differentiated formulations that address specific symptom clusters rather than all-in-one solutions. Companies that achieve the optimal balance between effectiveness and side-effect management are capturing premium pricing opportunities, as consumers increasingly seek targeted relief rather than broad-spectrum treatments.

Pain Management Solutions: The Rising Star in Consumer Health

Analgesics are experiencing remarkable momentum with a 6.23% CAGR, outpacing other OTC drug categories and signaling a fundamental shift in consumer self-care priorities. This growth trajectory is being fueled by an aging global population, increased prevalence of chronic pain conditions, and consumers' growing preference for managing mild-to-moderate pain without prescription medications. The segment's expansion is supported by scientific advances in pain management, with newer products offering longer-lasting relief. For instance, naproxen-based OTC NSAIDs provide pain relief lasting 8-12 hours compared to just 4-8 hours for other non-prescription pain relievers. The strategic opportunity for market players is clear: investing in extended-release technologies and enhanced safety profiles will capture value in a segment where consumers increasingly understand that not all pain relievers are created equal, especially as the CDC's definition of chronic pain (lasting three months or more) becomes more widely recognized among self-treating consumers.

Specialty OTC Categories: The Innovation Pipeline

Beyond respiratory and pain relief categories, the OTC healthcare market is experiencing nuanced evolution across its specialty segments. Dermatology and gastrointestinal products are benefiting from consumers' increasing willingness to self-treat conditions previously reserved for physician consultation, while vitamins and supplements continue their steady expansion as preventative healthcare becomes mainstream. Weight loss products are witnessing a transformation as consumers shift from miracle-promising solutions to evidence-backed formulations, and ophthalmic products benefit from increased screen time driving higher incidence of eye strain and dryness. This diversification presents a critical strategic opportunity for manufacturers to build multi-category portfolios that can weather seasonal fluctuations and capitalize on cross-selling opportunities. These specialty segments collectively represent the industry's innovation laboratory - where novel delivery systems, specialized ingredients, and unique positioning strategies often emerge before migrating to larger categories, providing valuable testing grounds for innovations that can eventually transform mainstream portfolios.

Segment Analysis: By Formulation Type

Tablet Dominance: The Enduring Foundation of OTC Drug Delivery

Tablets maintain their preeminent position in the OTC medication landscape with an impressive 41.52% market share, reflecting both consumer preference and manufacturing efficiency. This continued dominance stems from tablets' inherent advantages: precise dosing, exceptional stability, cost-effective production, and consumer familiarity that transcends geographic and demographic boundaries. Even as alternative delivery systems emerge, tablets remain the benchmark against which other formulations are measured, particularly for conditions requiring consistent, reliable dosing. While tablet formulations may appear mature, significant competitive differentiation remains possible through innovations in absorption rates, tablet coatings that mask bitter active ingredients, and scored designs that facilitate dose customization. Companies investing in these subtle yet meaningful tablet enhancements are securing consumer loyalty in a segment where convenience and consistency continue to outweigh the novelty offered by alternative delivery mechanisms.

Spray Innovations: Transforming Treatment Delivery

Spray formulations are experiencing remarkable growth, redefining consumer expectations for treatment immediacy and targeted application. This acceleration reflects consumers' increasing demand for no-touch applications, precise dosing, and rapid absorption—particularly evident in categories like nasal decongestants, throat sprays, and topical pain relievers. The category's expansion is being propelled by innovations in spray technologies that provide more controlled delivery, reduced waste, and enhanced user experience compared to traditional formats. Spray formulations offer a unique capacity to deliver active ingredients directly to affected areas while minimizing systemic absorption—addressing the growing consumer preference for treatments that work rapidly at the site of discomfort without unnecessary total-body exposure. Companies that master the technological challenges of stable, precisely-dosed spray formulations while solving issues like taste, scent, and consistent particle size are positioning themselves at the forefront of this high-growth segment.

Liquid and Ointment Solutions: Meeting Distinct Therapeutic Needs

Liquid and ointment formulations maintain critical positions within the over the counter ecosystem, each addressing distinct therapeutic requirements and consumer preferences that cannot be satisfied through other delivery systems. Liquids continue to dominate pediatric and geriatric formulations where swallowing tablets presents challenges, while offering faster absorption rates that appeal to consumers seeking rapid relief. Simultaneously, ointments provide targeted, sustained delivery for dermatological and pain management applications where direct, prolonged contact with affected areas delivers therapeutic advantage. These formulations, while not leading in overall market share, often command premium pricing and inspire greater brand loyalty due to their specialized nature. Companies that enhance these formulations' sensory characteristics—improving taste profiles for liquids and creating non-greasy, quickly-absorbing ointments—are finding substantial growth opportunities even within these mature subsegments, demonstrating that delivery system refinement can drive category expansion even without novel active ingredients.

Segment Analysis: By Distribution Channel

Retail Pharmacy Stronghold: The Trusted Consumer Gateway

Retail pharmacies continue to dominate the OTC drug distribution landscape with a substantial 51.90% market share, maintaining their position as consumers' preferred destination for self-medication products despite digital alternatives. This continued leadership stems from the unique combination of immediate product availability, tangible product evaluation, and critically, access to professional pharmacist consultation that consumers value when making health-related purchases. Traditional pharmacies have successfully leveraged their trusted healthcare status while evolving their merchandising strategies to highlight symptom-based solutions rather than brand-centric displays, effectively guiding consumers through increasingly complex OTC medicine choices. While omnichannel approaches are essential, retail pharmacy-specific strategies—including pharmacist education programs, strategic shelf positioning, and point-of-purchase decision tools—remain the most direct path to market share gains in the self-medication category, particularly for products addressing more complex health conditions where professional guidance influences purchase decisions.

Digital Health Commerce: The Acceleration of Online Pharmacy

Online pharmacies are experiencing remarkable momentum with a 6.44% CAGR, fundamentally altering how consumers discover, evaluate, and purchase OTC products. This accelerated growth reflects the convergence of expanded digital health literacy, enhanced logistics infrastructure enabling rapid delivery, and consumers' increasing comfort with purchasing health products through digital channels. The segment's expansion is being fueled by distinctive online advantages: 24/7 availability, price transparency, user reviews that substitute for traditional word-of-mouth recommendations, and discreet purchasing for sensitive health concerns. The digital channel offers unique capacity to educate consumers through detailed product information and symptom checkers—capabilities that physical packaging cannot match. Companies that develop channel-specific digital assets, optimize product descriptions for searchability, and create engaging educational content are capturing disproportionate share in this rapidly expanding channel, particularly among younger demographics who increasingly view online purchasing as their default rather than alternative shopping method.

Healthcare Institution Channels: Professional Influence on Consumer Choice

Hospital pharmacies constitute a distinctive distribution environment within the OTC drug market, operating at the critical intersection between professional healthcare and consumer self-care. These institutional channels hold unique strategic value despite their smaller share, serving as essential proving grounds where healthcare professionals first encounter and evaluate new OTC formulations. This professional exposure creates powerful downstream effects as physicians and nurses subsequently recommend trusted products to outpatients. The hospital pharmacy environment also plays a crucial educational role, particularly for recently switched prescription-to-OTC products where professional guidance significantly influences initial consumer adoption patterns. Hospital pharmacy presence delivers value far beyond direct sales volumes: it confers implicit medical endorsement that resonates through other distribution channels. Companies that develop targeted hospital pharmacy strategies—including professional education programs, institutional pack sizes, and transition-of-care initiatives connecting inpatient experience with outpatient self-care—are establishing competitive advantages that extend well beyond this channel's immediate sales contribution.

Geography Analysis

North America: Leading the Global OTC Market

North America holds the top position in the global over the counter drugs market, representing approximately 41.52% of worldwide market share in 2025. This leadership comes from strong healthcare infrastructure, high consumer spending on healthcare, and growing preference for self-medication. The region benefits from notable price differences between prescription and non-prescription options—in the United States, Medicare Part D pays 2.3 times more for medications than their over-the-counter cash prices. This cost gap encourages both consumers and healthcare systems to choose OTC products when possible. Major companies like Johnson & Johnson, Bayer AG, and Pfizer compete through product innovation and marketing campaigns. For companies in this space, the key challenge is finding the right balance between premium pricing and value options as consumers become more price-conscious.

United States: Driving North American OTC Growth

The United States leads the North American OTC drug market with roughly 25.95% of global market share. This dominance comes from its large consumer base, extensive pharmacy networks, and increasing FDA approvals for prescription-to-OTC switches. The economics of the U.S. healthcare system create strong market opportunities—for common heartburn medications, Medicare Part D pays $28.75 per capsule while the OTC version costs just USD 0.80. This remarkable 36-fold price difference explains why many consumers prefer OTC options. Companies that can successfully navigate the regulatory process for moving prescription drugs to OTC status while maintaining safety will gain significant advantages in this valuable market segment.

Canada: Integrating Digital Health into OTC Distribution

Canada shows the fastest growth within North America's OTC drugs sector, driven by progressive regulations and digital health innovation. The Canadian market features an expanded role for pharmacists in recommending OTC medicines. Canadian pharmacy chains are adopting data-driven engagement strategies—similar to markets where prescription-based predictive models have improved customer retention by 70%. Growth is further supported by Canada's universal healthcare system, which encourages appropriate self-care to manage costs. For companies in this market, success depends on developing specialized OTC portfolios that address Canada's unique demographic needs, with particular attention to bilingual packaging and educational resources for the country's diverse population.

Mexico: Blending Traditional and Modern OTC Approaches

Mexico offers a unique mix of traditional and modern approaches in the OTC drug industry. Unlike its northern neighbors, Mexico has more flexible regulations for certain medication categories and maintains strong traditional medicine practices alongside conventional OTC products. This creates opportunities for specialized formulations that combine traditional ingredients with modern delivery systems. The market shows particular strength in pain management and gastrointestinal OTC pharmaceutical products, reflecting local health priorities and preferences. Distribution differs from U.S. and Canadian patterns, with independent pharmacies and community stores maintaining significant market share alongside growing pharmacy chains. International manufacturers should recognize Mexico's value both as a growth market and as a testing ground for products that may appeal to Hispanic consumers throughout the Americas.

Asia-Pacific: The Growth Engine of the Global OTC Market

The Asia-Pacific region represents the most dynamic area in the over the counter drugs market, growing at the highest rate globally. This impressive growth comes from expanding middle classes with increasing disposable income, government policies promoting self-care to reduce healthcare costs, and cultural traditions that align well with non-prescription remedies. The region presents diverse market conditions for OTC pharmaceutical companies—in Japan, only 0.7% of convenience stores nationwide sold medicines as of February 2023, showing strict control of distribution channels, while other Asian markets are rapidly embracing digital sales platforms. For global manufacturers, success in this region requires developing targeted product portfolios that address specific regional health concerns while navigating varying regulatory frameworks across different countries.

China: Where Traditional Medicine Meets Modern Retail

China leads the Asia-Pacific OTC drug market with its massive scale and evolving retail landscape. The country's large population and growing middle class create substantial demand for OTC medications, particularly for respiratory conditions, digestive health, and wellness supplements. China uniquely integrates traditional Chinese medicine with modern pharmaceutical approaches, creating distinctive product categories rarely found in Western markets. The retail environment is transforming as pharmacy chains expand and e-commerce platforms enter the medication delivery space. Chinese consumers often rely heavily on pharmacist recommendations, giving retail chains significant influence over purchasing decisions. Companies should develop strategies that respect traditional healing practices while introducing science-backed formulations that appeal to increasingly knowledgeable urban consumers looking for both convenience and effectiveness.

India: Digital Innovation Driving Exceptional OTC Growth

India leads growth in Asia-Pacific's OTC healthcare market with an impressive CAGR. This rapid expansion is transforming India from a market of potential to a center of innovation in the OTC segment. Growth comes from improved healthcare accessibility, with OTC products filling gaps in areas with limited formal healthcare. Digital transformation is changing how products reach consumers—implementation of data analytics has improved customer retention by 70% for one pharmaceutical retail chain in India, while increasing sales of high-value drugs by 11%. These technological advances create new ways to reach consumers beyond traditional stores. Rural areas remain largely untapped, representing significant opportunities as distribution networks expand. Companies should focus on developing affordable OTC product portfolios that address India's specific health needs while investing in digital platforms to overcome distribution challenges.

Diverse Markets of Asia-Pacific: From Developed to Emerging Economies

Beyond China and India, Asia-Pacific includes diverse OTC drugs markets at various development stages. Japan represents a mature market with strict regulations and consumer preference for premium products, shown by its controlled distribution where traditional outlets dominate—only 0.7% of convenience stores sold medicines in 2023. Australia features clear regulatory guidelines, specifying that "fast" or "rapid" claims on OTC medicine labels must be supported by dissolution data showing 70% dissolution of active ingredients within 15 minutes. South Korea combines advanced technology with established pharmacy practices, while Southeast Asian nations show varied approaches to OTC pharmaceutical products based on their healthcare systems and cultural preferences. This diversity requires tailored market strategies rather than standardized approaches. Companies should develop flexible distribution models and product portfolios that can adapt to the specific requirements and consumer preferences in each market.

Europe: Tradition and Innovation in a Mature OTC Market

Europe's OTC drugs market combines innovation with established consumer expectations and diverse regulations. The region values balanced healthcare approaches, with the UK alone reporting £6.4 billion in NHS savings on prescriptions and appointments due to OTC usage. European healthcare systems increasingly encourage appropriate self-medication with OTC medications for both economic and practical reasons. The market shows interesting contrasts—while Europeans embrace digital health technology, they maintain strong loyalty to traditional pharmacies for purchasing medications. This preference creates challenges for online pharmacies, which face intense scrutiny; in the UK, online pharmacies accounted for almost 2,000 regulatory concerns over a five-year period. Germany leads in market volume, while the UK shows strength in consumer-focused innovation. Companies operating across European markets must navigate different regulatory requirements while developing products that meet high standards for effectiveness, safety documentation, and increasingly important sustainability credentials.

Middle East & Africa: Diverse Markets with Varying Growth Potential

The Middle East and Africa present highly diverse conditions in the global OTC drug market, with significant differences in healthcare infrastructure, regulations, and consumer purchasing power. Gulf Cooperation Council (GCC) countries feature advanced healthcare systems and higher spending on OTC products, while African markets show rapid growth from smaller starting points. South Africa represents the continent's most developed OTC healthcare market, combining Western pharmaceutical practices with local approaches. Urban centers across the region are seeing expanded pharmacy chain presence, gradually shifting OTC medication purchases from traditional markets to organized retail outlets. Digital health initiatives are gaining momentum in wealthier markets, though online sales regulations vary significantly by country. Companies looking to succeed in this region should develop market-specific strategies that address the unique disease patterns and consumer preferences in each area, focusing on tailored product portfolios rather than standardized approaches.

South America: Cultural Factors Shaping OTC Consumer Behavior

South America's OTC drug market shows distinctive characteristics influenced by regional economic conditions, cultural preferences, and healthcare traditions. Brazil dominates as the largest market, with its large population and well-developed pharmacy networks driving consumption of OTC medicines. Argentina follows with its sophisticated urban consumers. Throughout the region, there's a unique interaction between modern pharmaceuticals and traditional remedies. The OTC segment shows particular growth in pain management, digestive health, and vitamins—categories that align with regional health concerns. While physical pharmacies remain the primary distribution channel, e-commerce is growing in major cities, especially following pandemic-related behavior changes. Pharmacists have significant influence over product selection, similar to other markets where data-driven approaches have improved sales substantially. Companies should focus on building strong relationships with pharmacy chains and independent retailers who serve as key gatekeepers for consumer access, while developing brand strategies that connect with the region's preference for trusted healthcare names.

Over The Counter Drugs Industry Overview

Digital Integration: The New Competitive Battleground for OTC Giants

The fight for dominance in the OTC drug market is moving beyond store shelves to digital platforms. Leading otc companies like Johnson & Johnson and Bayer AG aren't just competing on product variety anymore—they're racing to build digital ecosystems that connect with consumers at every touchpoint. This shift is evident in how payment systems now integrate with over 32 banks globally, using contactless technology to make purchasing faster and simpler. But the real value isn't just in easier transactions—it's in the consumer data these digital systems collect. This information gives companies unprecedented insights into buying patterns, allowing for more targeted product development and marketing. For manufacturers in the global OTC market, the message is clear: build your digital capabilities or risk being left behind. Companies that master this digital integration aren't just selling pills and remedies; they're creating holistic consumer experiences that build loyalty beyond the product itself.

Regulatory Mastery: The Hidden Competitive Edge in OTC Markets

While flashy marketing campaigns grab headlines, the quieter battle over regulatory expertise is often what separates winners from losers among top OTC companies. Take the FDA's 180-day exclusivity period for first-filed generic applications, which also applies to Rx-to-OTC switches—this policy creates a golden window of opportunity for companies with regulatory foresight. This explains why giants like GlaxoSmithKline and Pfizer have built specialized regulatory teams, while ambitious players like Sun Pharmaceutical strategically target categories ripe for prescription-to-OTC conversion. The benefits extend far beyond temporary exclusivity; companies that navigate these regulatory pathways successfully gain authority status with healthcare providers and often secure prime shelf positioning in stores. For players in the OTC drug industry, regulatory expertise isn't just a defensive necessity—it's an offensive weapon that can lock out competitors and secure market advantage for years beyond any exclusivity period. The companies investing in this capability now are positioning themselves for outsized returns in an increasingly competitive marketplace.

Subscription Models: The Price Disruptor Reshaping OTC Competition

The one-time purchase model that has dominated the otc drug sector for decades is facing a serious challenge from subscription-based alternatives. Amazon's RxPass program—offering monthly access to common medications for just $5, comparable to a single prescription copay—signals a major shift in how consumers might soon pay for their health products. This approach is forcing every player in the over the counter drugs market to rethink their business models. Traditional manufacturers like Reckitt Benckiser and Sanofi are responding by buying digital health platforms and creating their own subscription services, while companies like Perrigo are teaming up with pharmacy chains on membership programs that combine products with healthcare services. The companies that figure out subscription models won't just enjoy steady, predictable revenue—they'll build direct customer relationships that bypass retail middlemen and create ongoing engagement opportunities. In an industry where brand loyalty has traditionally been fickle, subscription services create stickier customer relationships that can fundamentally alter competitive dynamics across the entire OTC market.

Over The Counter Drugs Market Leaders

-

Johnson and Johnson

-

Perrigo Company Plc

-

Bayer AG

-

Sanofi

-

Pfizer

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Over The Counter Drugs Market News

- April 2024: Amneal Pharmaceuticals Inc. received the US Food and Drug Administration approval for over-the-counter naloxone hydrochloride nasal spray, which can be used in the treatment of drug overdose from opioids, including heroin, fentanyl, and prescription opioid medicines.

- March 2024: Perrigo launched the OTC birth control pill Opill, which was approved by the US Food and Drug Administration. This pill can be purchased without a prescription from in-store and online retailers in the United States.

Over The Counter Drugs Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 High Cost of Rx Drugs Leading to Shift Towards OTC Drugs

- 4.2.2 Increasing Approval of OTC Drugs

-

4.3 Market Restraints

- 4.3.1 Stringent Regulatory Policies

- 4.3.2 Lack of Awareness and Drug Abuse

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

-

5.1 By Product Type

- 5.1.1 Cough, Cold, and Flu Products

- 5.1.2 Analgesics

- 5.1.3 Dermatology Products

- 5.1.4 Gastrointestinal Products

- 5.1.5 Vitamins, Mineral, and Supplements (VMS)

- 5.1.6 Weight Loss/Dietary Products

- 5.1.7 Ophthalmic Products

- 5.1.8 Sleeping Aids

- 5.1.9 Other Product Types

-

5.2 By Formulation Type

- 5.2.1 Tablets

- 5.2.2 Liquids

- 5.2.3 Ointments

- 5.2.4 Sprays

-

5.3 By Distribution Channel

- 5.3.1 Hospital Pharmacies

- 5.3.2 Retail Pharmacies

- 5.3.3 Online Pharmacy

-

5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Johnson and Johnson

- 6.1.2 Bayer AG

- 6.1.3 Viatris (Mylan NV)

- 6.1.4 Sanofi S.A.

- 6.1.5 Pfizer Inc.

- 6.1.6 GlaxoSmithKline PLC

- 6.1.7 Perrigo Company PLC

- 6.1.8 Reckitt Benckiser Group PLC

- 6.1.9 Takeda Pharmaceutical Company Ltd

- 6.1.10 Boehringer Ingelheim International GmbH

- 6.1.11 Sun Pharmaceutical Industries Ltd

- 6.1.12 Teva Pharmaceutical Industries Ltd

- 6.1.13 Glenmark Pharmaceuticals Ltd

- 6.1.14 Dr. Reddy's Laboratories

- 6.1.15 Piramal Enterprises

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape Covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Over The Counter Drugs Industry Segmentation

As per the scope of this industry research report, over-the-counter drugs are referred to as non-prescription drugs. These medicines can be bought by an individual without a doctor's prescription and are safe for consumption without the doctor's consent.

The over-the-counter drugs market segmentation covers product type, formulation type, distribution channel, and geography. By product type, the market is segmented into cough, cold, and flu products, analgesics, dermatology products, gastrointestinal products, vitamins, minerals, and supplements (VMS), weight loss/dietary products, ophthalmic products, sleeping aids, and other product types. By formulation type, the market is segmented into tablets, liquids, ointments, and sprays. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies, online pharmacies, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The industry research report also covers the estimated sales data and market trends for 17 different countries across major regions globally. For each segment, the industry size and forecast are provided in terms of value (USD).

| By Product Type | Cough, Cold, and Flu Products | ||

| Analgesics | |||

| Dermatology Products | |||

| Gastrointestinal Products | |||

| Vitamins, Mineral, and Supplements (VMS) | |||

| Weight Loss/Dietary Products | |||

| Ophthalmic Products | |||

| Sleeping Aids | |||

| Other Product Types | |||

| By Formulation Type | Tablets | ||

| Liquids | |||

| Ointments | |||

| Sprays | |||

| By Distribution Channel | Hospital Pharmacies | ||

| Retail Pharmacies | |||

| Online Pharmacy | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Over The Counter Drugs Market Research Faqs

How big is the Over The Counter Drugs Market?

The Over The Counter Drugs Market size is expected to reach USD 195.96 billion in 2025 and grow at a CAGR of 4.80% to reach USD 247.74 billion by 2030.

What is the current Over The Counter Drugs Market size?

In 2025, the Over The Counter Drugs Market size is expected to reach USD 195.96 billion.

Which is the fastest growing region in Over The Counter Drugs Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Over The Counter Drugs Market?

In 2025, the North America accounts for the largest market share in Over The Counter Drugs Market.

What years does this Over The Counter Drugs Market cover, and what was the market size in 2024?

In 2024, the Over The Counter Drugs Market size was estimated at USD 186.55 billion. The report covers the Over The Counter Drugs Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Over The Counter Drugs Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Over The Counter Drugs Industry Report

The global over-the-counter (OTC) drugs market is on an upward trajectory, poised for significant expansion, with North America at the forefront due to a preference for OTC over prescription drugs, alongside a rise in self-medication trends in Europe and Asia-Pacific. This growth is propelled by the increasing demand for self-medication, a shift from prescription to OTC drugs as a cost-saving measure, and the introduction of new products. Key trends shaping the market include the transition from prescription (Rx) to OTC drugs and the emergence of private-label products, with industry leaders innovating to address consumer health needs. Despite challenges such as incorrect self-diagnosis and potential side effects, additionally the market is dominated by cold and cough remedies, analgesics, and vitamins and minerals as leading product segments, with drug stores and retail pharmacies serving as the primary distribution channels. For detailed insights on market trend, market statistics, industry profiles, and market value, Mordor Intelligence™ provides a comprehensive analysis of the market outlook, which is available for download as a free-market report PDF.