Orthopedic Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

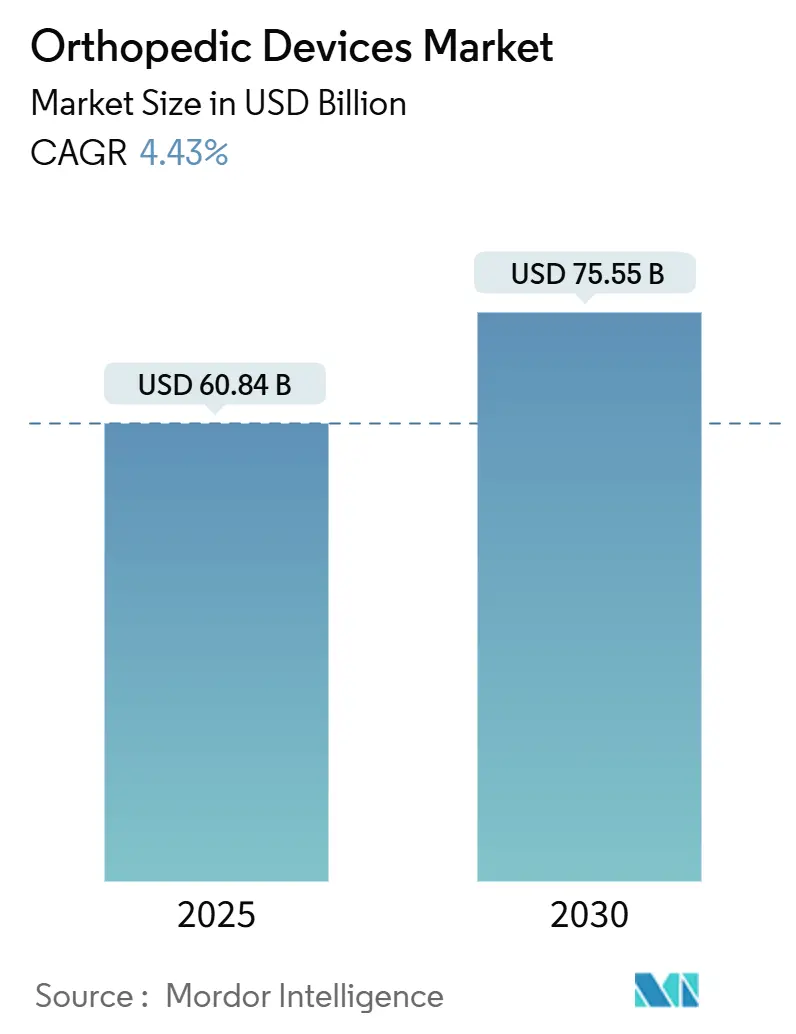

| Market Size (2025) | USD 60.84 Billion |

| Market Size (2030) | USD 75.55 Billion |

| Growth Rate (2025 - 2030) | 4.43% CAGR |

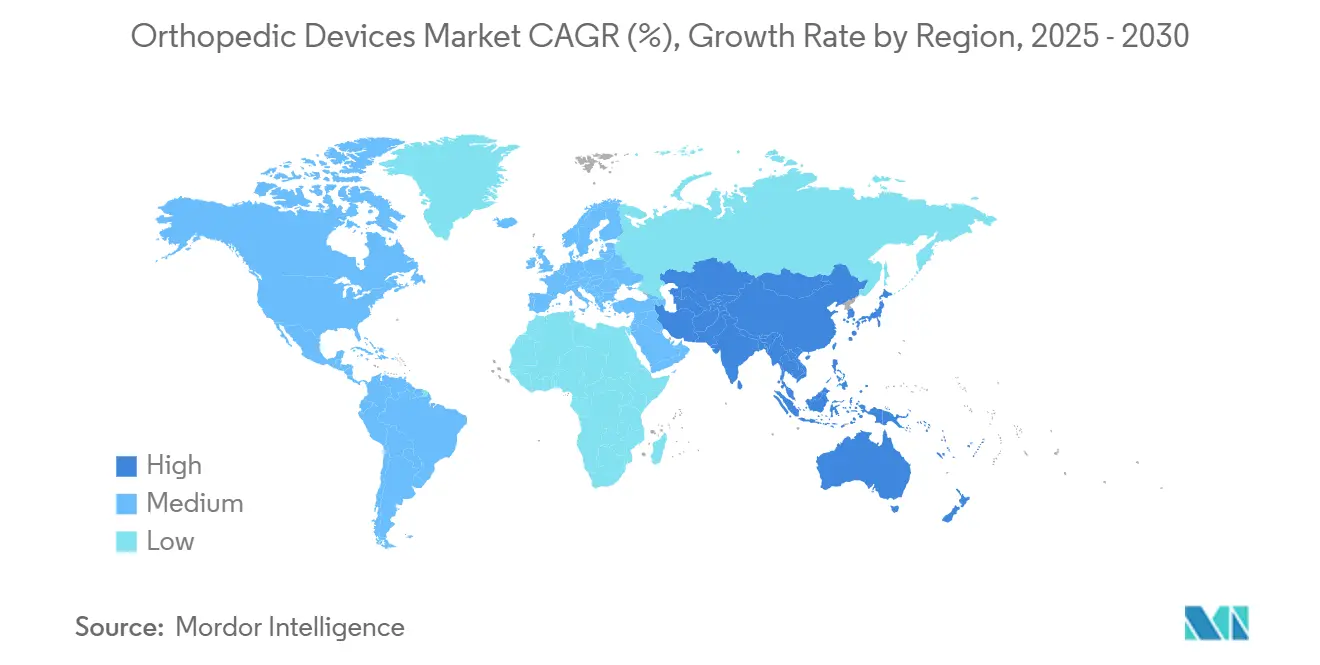

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

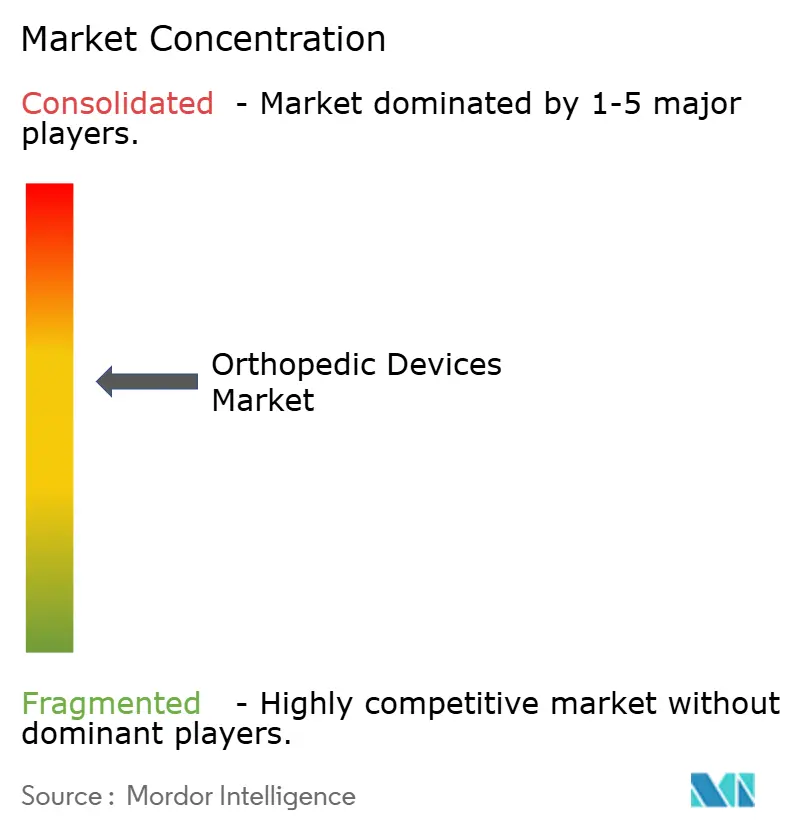

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Orthopedic Devices Market Analysis by Mordor Intelligence

The orthopedic devices market is valued at USD 60.84 billion in 2025 and is forecast to reach USD 75.55 billion by 2030, advancing at a 4.43% CAGR. The growth curve is steady rather than rapid, reflecting maturing demand, stricter reimbursement policies, and a pivot toward value-based purchasing. Joint reconstruction volumes continue to expand on the back of population aging, while AI-assisted surgical planning and robotic guidance improve clinical precision and shorten recovery windows. Manufacturers are also investing in 3-D printed and bioabsorbable implants to overcome limitations of traditional metals, supporting a pipeline of patient-specific solutions. At the same time, the orthopedic devices market feels pressure from complex approval pathways and surgeon reimbursement cuts, factors that temper acceleration despite favorable demographics.[1]PubMed, “Reimbursement Patterns in Total Joint Arthroplasty,” pubmed.ncbi.nlm.nih.gov

Key Report Takeaways

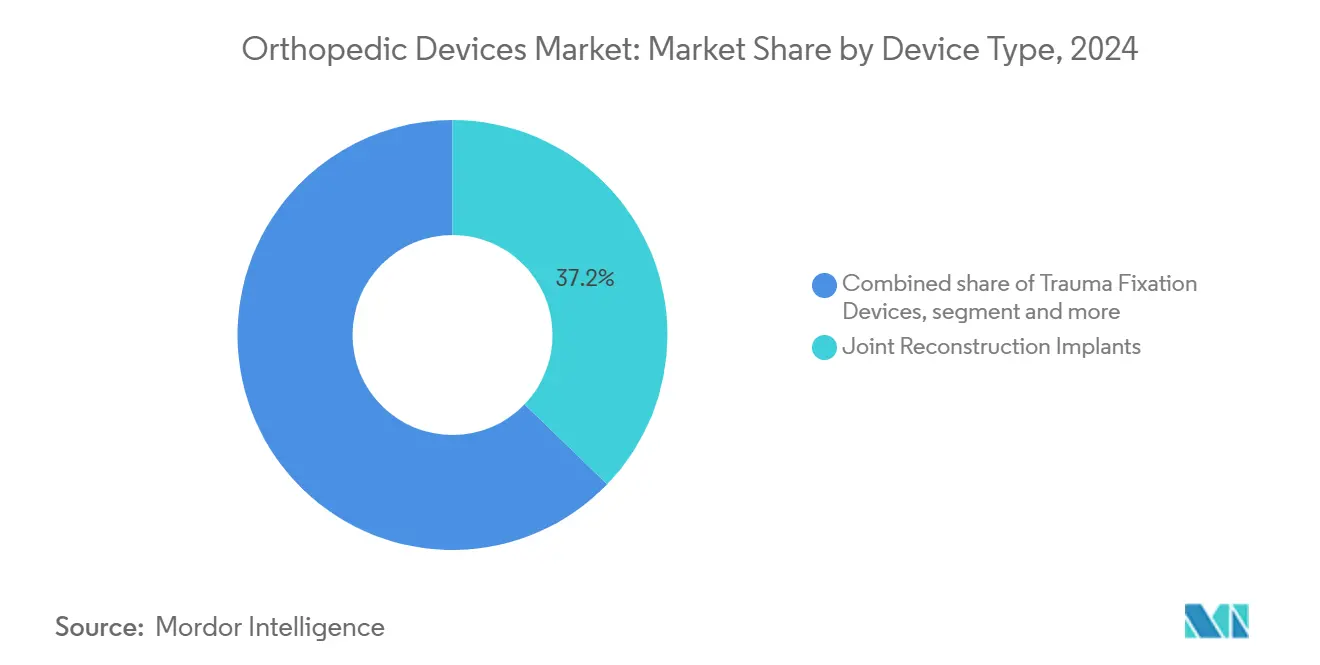

- By device type, joint reconstruction implants held 37.16% of orthopedic devices market share in 2024, while orthobiologics is projected to grow at a 5.86% CAGR to 2030.

- By material, titanium and titanium alloys accounted for 42.84% share of the orthopedic devices market size in 2024; bioabsorbable and composite materials are forecast to expand at a 6.58% CAGR through 2030.

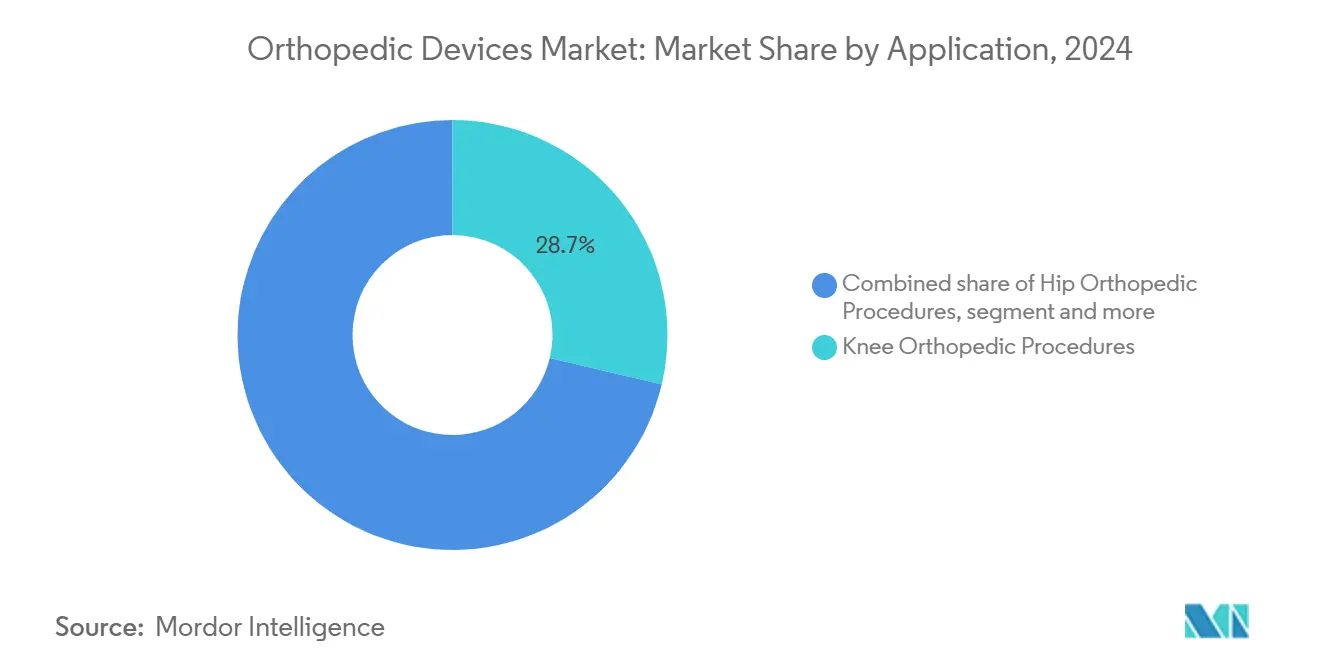

- By application, knee procedures captured 28.73% share of the orthopedic devices market size in 2024, whereas spine procedures are advancing at a 5.67% CAGR to 2030.

- By end user, hospitals controlled 62.32% revenue share in 2024, while ambulatory surgery centers record the highest projected CAGR at 6.12% through 2030.

- By geography, North America led with 44.62% revenue share in 2024; Asia-Pacific is set to post the fastest growth at a 7.23% CAGR over the same period.

Global Orthopedic Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population driving degenerative-joint procedures | +1.2% | Global; highest in North America & Europe | Long term (≥ 4 years) |

| Increasing number of large-joint reconstruction surgeries | +0.8% | Global; notably Asia-Pacific and North America | Medium term (2-4 years) |

| Technological advances in 3-D printed & bioabsorbable implants | +0.6% | North America & Europe leading; expanding to Asia-Pacific | Medium term (2-4 years) |

| AI-driven surgical planning & robotics improve outcomes | +0.5% | North America & Europe; selective uptake in Asia-Pacific | Medium term (2-4 years) |

| Rising orthopedic trauma & accident incidence | +0.4% | Global; stronger growth in emerging markets | Short term (≤ 2 years) |

| Value-based care boosting modular cost-efficient implants | +0.3% | Primarily North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Population Driving Degenerative-Joint Procedures

Hip replacements in the United States are projected to reach 635,000 cases and knee replacements 1.28 million by 2030, illustrating how longevity shifts demand toward large-joint implants. Similar trajectories appear worldwide; Colombia expects 39,270 lower limb arthroplasties by 2050 and Germany projects a 55% rise in total knee arthroplasty by 2040. Younger, active individuals are also opting for surgery earlier, extending implant duty cycles and fueling premium material uptake. Health systems must therefore expand surgical capacity, reinforce rehabilitation networks, and standardize outcome tracking to manage procedure surges efficiently.

Technological Advances in 3-D Printed & Bioabsorbable Implants

Additive manufacturing now delivers patient-matched geometries that speed osseointegration and cut operating time. FDA clearance for the first PEEK cranial implant in 2024 demonstrated regulatory acceptance of 3-D printed polymers in load-bearing indications. Industrial-scale printers in Alabama can already fabricate spine cages with minimal waste, signaling cost competitiveness. Bioabsorbable devices address sports and trauma cases where permanent hardware is unnecessary, a capability strengthened by recent FDA authorizations of platelet-rich plasma systems that encourage biologic healing. These innovations differentiate suppliers and open regenerative pathways that may reduce revision burdens long term.

AI-Driven Surgical Planning & Robotics Improve Outcomes

Machine-learning algorithms predict optimal implant sizing with up to 89.5% accuracy, enhancing alignment and reducing revision risk. Robotic systems such as Mako SmartRobotics cut variability in knee and hip procedures, and the platform’s 2025 update now supports complex hip revisions. Zimmer Biomet performed the first robotic shoulder replacement in 2024, evidencing rapid expansion into additional joints. Early data show robotic cases yield higher functional scores and fewer complications, factors that can offset acquisition costs under bundled-payment models.

Rising Orthopedic Trauma & Accident Incidence

Urban mobility, sports participation, and falls among older adults have raised fracture volumes, sustaining demand for plates, screws, and specialized extremity devices. The FDA issued updated guidance on trauma plating in 2024 to ensure supply keeps pace with quality standards.[2]Federal Register, “Orthopedic Non-Spinal Bone Plate Guidance,” federalregister.gov Johnson & Johnson’s newly launched VOLT Plating System reflects industry focus on complex fracture patterns. Growth is especially strong in middle-income economies where motor-vehicle injuries remain high, creating near-term opportunities for mid-priced product lines tailored to regional reimbursement limits.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent multi-region regulatory approvals | −0.8% | Global; Europe most affected by MDR | Medium term (2-4 years) |

| Unfavorable reimbursement & shortage of skilled surgeons | −1.1% | North America & Europe | Long term (≥ 4 years) |

| Supply-chain volatility in titanium & PEEK materials | −0.4% | Global; manufacturing concentrated in Asia | Short term (≤ 2 years) |

| Outpatient migration eroding inpatient implant margins | −0.6% | North America & Europe; trend spreading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Multi-Region Regulatory Approvals

Europe’s Medical Device Regulation, enforced fully in 2024, raised evidence thresholds and extended review cycles, delaying product launches and inflating development budgets. Parallel changes at the FDA, including new coating guidance and change-control plans, add additional documentation layers, particularly for antimicrobial or surface-modified implants. Firms must now conduct multi-center clinical studies and maintain post-market surveillance systems that stretch smaller innovators’ resources and may slow technology diffusion.

Unfavorable Reimbursement & Shortage of Skilled Surgeons

Surgeon payment for primary and revision arthroplasty has declined across both Medicare Advantage and commercial plans, trimming procedure profitability and dampening adoption of premium implants. Claims denials have also become more frequent as payers scrutinize necessity, adding administrative burden. Concurrently, orthopedic residency slots are insufficient to meet rising demand, and robotic platforms require added training. Hospitals therefore tread carefully before investing in costly new systems, limiting near-term upside for device vendors.

Segment Analysis

By Device Type: Joint Reconstruction Leads Innovation

Joint reconstruction implants held 37.16% of orthopedic devices market share in 2024, anchored by hip and knee replacement volumes that will keep rising well into the next decade. Manufacturers focus on long-wearing polyethylene liners, porous titanium scaffolds, and smart sensors that relay load data to clinicians. Orthobiologics, though smaller, is the fastest-growing group at a 5.86% CAGR, propelled by cartilage repair matrices and growth-factor-enriched grafts. The orthopedic devices market continues to shift toward combination products that blend mechanics with biology, a trend underscored by CARTIHEAL AGILI-C’s 87% reduction in conversion to total knee arthroplasty at four years.[3]Ortho Spine News, “CARTIHEAL AGILI-C Four-Year Follow-Up,” orthospinenews.com

Sports-medicine instrumentation and arthroscopes benefit from younger cohorts seeking preventive repairs, while spine devices absorb gains from minimally invasive techniques that shorten recovery. Trauma sets remain resilient thanks to steady accident rates. Vendors therefore manage a broad development slate, balancing high-volume reconstructive workhorse implants with specialized biologics to hedge against reimbursement squeezes in commoditized segments of the orthopedic devices market.

Note: Segment shares of all individual segments available upon report purchase

By Material: Titanium Dominance Faces Bioabsorbable Challenge

Titanium and its alloys accounted for 42.84% of the orthopedic devices market size in 2024, thanks to strength-to-weight advantages and proven biocompatibility. Supply-chain volatility, however, drives exploration of alternatives as titanium costs range from USD 6 to USD 30 per pound depending on refinement grade. Bioabsorbable polymers and composites grow fastest at 6.58% CAGR, offering temporary fixation that dissolves once healing completes, a property prized in sports injuries and pediatric fractures.

PEEK maintains a foothold in spine cages because it yields artifact-free imaging and modulus compatibility with bone; more than 15 million PEEK devices are implanted worldwide. Advanced beta-titanium alloys with niobium and zirconium reduce modulus mismatch to limit stress shielding, while magnesium-based resorbables advance through trials. These shifts indicate a gradual transition away from permanent metallic hardware, positioning the orthopedic devices market for more regenerative, life-cycle-oriented therapies.

By Application: Knee Procedures Drive Volume Growth

Knee surgeries represented 28.73% share of the orthopedic devices market size in 2024, reflecting widespread osteoarthritis and earlier surgical intervention among active adults. Implant makers push cementless fixation and personalized alignment guides to meet longevity expectations. Spine procedures post the highest CAGR at 5.67%, encouraged by aging populations and AI-guided navigation that reduces pedicle-screw misplacement. The orthopedic devices market benefits from minimally invasive lumbar decompressions that shift care to ambulatory sites, opening incremental demand for compact instrument sets.

Hip arthroplasty stays robust due to demographic dynamics, whereas trauma implants stabilize on accident prevalence. Innovative solutions such as total talus replacements fill highly specialized gaps. Interest also rises in upper-extremity replacements where robotics is now entering the shoulder space, diversifying revenue streams inside the orthopedic devices market.

Note: Segment shares of all individual segments available upon report purchase

By End User: ASCs Reshape Healthcare Delivery

Hospitals retained 62.32% revenue in 2024 by handling complex revisions and polytrauma cases requiring large surgical teams. Nevertheless, ambulatory surgery centers log a 6.12% CAGR as payers push procedures to low-overhead sites that deliver equivalent outcomes. Outpatient hip and knee arthroplasty show safety parity with inpatient care and cut episode cost by double-digit percentages. This favors standardized implant systems that streamline sterilization and turnover.

Orthopedic specialty clinics feed referral pipelines and perform less-invasive tendon repairs, while rehabilitation centers deploy sensor-enabled braces for recovery monitoring. Vendors now package implants with digital follow-up platforms to help ASCs satisfy bundled-payment contracts, reinforcing the outpatient shift within the orthopedic devices market.

Geography Analysis

North America controlled 44.62% of orthopedic devices market revenue in 2024 as robust insurance coverage and early adoption of robotics accelerated premium implant uptake. CMS has introduced new patient-reported outcome measures for joint arthroplasty in 2025, linking reimbursement to functional improvement and nudging suppliers toward evidence-based pricing.[4]Noridian, “2025 HCPCS Update,” med.noridianmedicare.com Meanwhile, the region’s ASC build-out is slated to lift outpatient orthopedic volumes by 21% over the next decade, pressuring vendors to sharpen cost-to-value propositions.

Asia-Pacific, growing at 7.23% CAGR, gains from rising middle-class incomes, government investment in surgical robotics, and soaring incidence of degenerative spinal disease. China alone targets a medical-device market of USD 210 billion by 2025, and regional production hubs supply titanium and PEEK, shortening lead times and reducing import tariffs. Local companies co-develop products with multinationals, hastening technology transfer and customizing features for smaller stature patients.

Europe posts steady expansion despite Medical Device Regulation hurdles that extend approval cycles. Germany projects total knee arthroplasty incidence will climb 55% by 2040, creating durable baseline demand even as hospitals consolidate implant vendors. Middle East–Africa and South America remain nascent but attractive; orthopedic tourism in the Gulf boosts high-acuity procedure volumes, while macro-economic recovery in Brazil unlocks capital budgets for trauma and sports-medicine inventory.

Competitive Landscape

The orthopedic devices market shows moderate consolidation: the top three players account for a significant portion of worldwide revenue but still face nimble entrants that commercialize niche solutions. Johnson & Johnson’s DePuy Synthes leverages global distribution and broad indication coverage, integrating VELYS robotics for knee revisions to cement surgeon loyalty. Stryker advances its Mako platform across hip, knee, spine, and soon shoulder, while absorbing smaller innovators such as Vertos Medical to blanket adjacent pain-management segments.

Zimmer Biomet builds complementary software around its ROSA suite and introduced Oxford Cementless Partial Knee to capture younger patients requiring bone preservation. Globus Medical’s USD 250 million purchase of Nevro in 2025 highlights convergence between orthopedic hardware and neuromodulation, expanding chronic-pain addressability. Start-ups concentrate on 3-D printed craniomaxillofacial implants, bioresorbables, and AI planning tools, often positioning themselves as acquisition targets once clinical data mature.

Competition revolves less around list price and more around procedural efficiency, evidence generation, and digital-health integration. Companies bundle implant, instrumentation, analytics, and patient-engagement apps to satisfy value-based contracts. Those unable to prove outcome advantages or navigate complex regulatory filings risk share erosion as providers standardize purchasing across fewer, full-service vendors in the orthopedic devices market.

Orthopedic Devices Industry Leaders

-

Smith & Nephew PLC

-

Zimmer Biomet

-

Stryker Corporation

-

Johnson & Johnson Inc

-

Medtronic PLC.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stryker revealed the fourth-generation Mako 4 system with the first robotic hip-revision mode at AAOS 2025.

- March 2025: Johnson & Johnson MedTech showcased VELYS robotic knee, KINCISE 2 automated system, and VOLT Plating for trauma at AAOS 2025.

- February 2025: Medtronic introduced the CD Horizon ModuLeX spinal platform within its AiBLE ecosystem, integrating navigation, robotics, and AI.

- August 2024: DePuy Synthes launched the TriLEAP foot-and-ankle system, widening its extremities catalog.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global orthopedic devices market as all implantable and reusable products that surgically repair, replace, or stabilize human bones and joints, including joint reconstruction systems, trauma fixation plates, spinal instrumentation, arthroscopy tools, and orthobiologics.

Scope exclusion: Assistive braces, external rehabilitation aids, and crutches are not counted.

Segmentation Overview

- By Device Type

- Joint Reconstruction Implants

- Trauma Fixation Devices

- Spine Surgery Devices

- Craniomaxillofacial Devices

- Sports Medicine & Arthroscopy Devices

- Orthobiologics

- Other Orthopedic Devices

- By Material

- Titanium & Titanium Alloys

- Stainless Steel

- Polymeric Biomaterials

- Bioabsorbable & Composite Materials

- Others

- By Application

- Hip Orthopedic Procedures

- Knee Orthopedic Procedures

- Spine Orthopedic Procedures

- Trauma Fixation

- Other Applications

- By End User

- Hospitals

- Orthopedic & Specialty Clinics

- Ambulatory Surgical Centers (ASCs)

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing orthopedic surgeons, procurement managers at multi-specialty hospitals, and regional distributors across North America, Europe, and Asia-Pacific. These conversations refined utilization rates, validated emerging procedure mix changes, and tested our draft price curves before numbers were frozen.

Desk Research

We drew foundational inputs from open-access sources such as the U.S. Census aging tables, Eurostat surgery statistics, OECD hospital discharge data, and FDA 510(k) device clearances, in addition to trade-association yearbooks from the International Society of Orthopaedic Surgery and local orthopedic registries. Company 10-Ks, investor decks, and reputable news articles were screened through Dow Jones Factiva for recent ASP shifts and capacity announcements. D&B Hoovers supplied revenue splits that aided device-type weighting. The sources listed remain illustrative; many other datasets informed our evidence stack.

Market-Sizing & Forecasting

We began with a top-down reconstruction that linked hip, knee, and spine procedure volumes to average selling prices, which are then calibrated against export-import shipment values and hospital spend surveys. Supplier roll-ups and sampled hospital channel checks provided a selective bottom-up view to cross-verify totals. Key model drivers include elective surgery backlog clearance pace, geriatric population growth, implant mix shift to titanium, robotics-assisted penetration, average length-of-stay trends, and currency-adjusted ASP progression. A multivariate regression with GDP-per-capita, population 65+, and trauma incidence underpins the 2025-2030 forecast while scenario analysis buffers for reimbursement changes. Data gaps in smaller geographies were bridged by prevalence-based demand pools anchored to regional registry ratios.

Data Validation & Update Cycle

Outputs pass three-step variance checks, peer review, and senior sign-off. We refresh the full model annually and trigger interim updates if regulatory recalls, landmark technology approvals, or +/-10% ASP swings occur.

Why Mordor's Orthopedic Devices Baseline Commands Confidence

Published estimates often differ because each firm chooses unique product baskets, price assumptions, and refresh cadences.

Key gap drivers include whether spinal biologics are bundled, how unreimbursed emerging-market procedures are treated, and the vintage of ASP curves; Mordor's scope mirrors real surgical use while some peers adopt narrow implant lists or apply undiscounted catalog prices.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 60.84 B (2025) | Mordor Intelligence | - |

| USD 51.61 B (2024) | Global Consultancy A | Excludes orthobiologics and uses 2021 ASP benchmarks |

| USD 62.80 B (2024) | Industry Journal B | Counts external braces and averages list prices without regional discounting |

| USD 62.22 B (2024) | Regional Consultancy C | Applies aggressive 5% annual price escalation and no currency adjustment |

In sum, our disciplined product scope, dual-track modeling, and rolling validation give decision-makers a transparent baseline that balances realism with analytical rigor.

Key Questions Answered in the Report

What is the current size of the orthopedic devices market?

The orthopedic devices market is valued at USD 60.84 billion in 2025 and is projected to grow to USD 75.55 billion by 2030.

Which segment holds the largest orthopedic devices market share?

Joint reconstruction implants lead with 37.16% share in 2024, driven by hip and knee replacement demand.

Why are ambulatory surgery centers important for orthopedic device growth?

ASCs offer lower costs and same-day discharge; their orthopedic case volume is expected to expand 21% over the next decade, fueling device demand in outpatient settings.

Which region will grow fastest through 2030?

Asia-Pacific is forecast to register a 7.23% CAGR on the back of wider healthcare access and rapid technology adoption.

How are robotics influencing orthopedic surgery outcomes?

Robotic platforms such as Mako and ROSA improve implant alignment, lower complication rates, and support complex revisions, which can improve long-term patient function.

Page last updated on: