Ophthalmic Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 40.58 Billion |

| Market Size (2031) | USD 60.29 Billion |

| Growth Rate (2026 - 2031) | 8.24% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ophthalmic Drugs Market Analysis by Mordor Intelligence

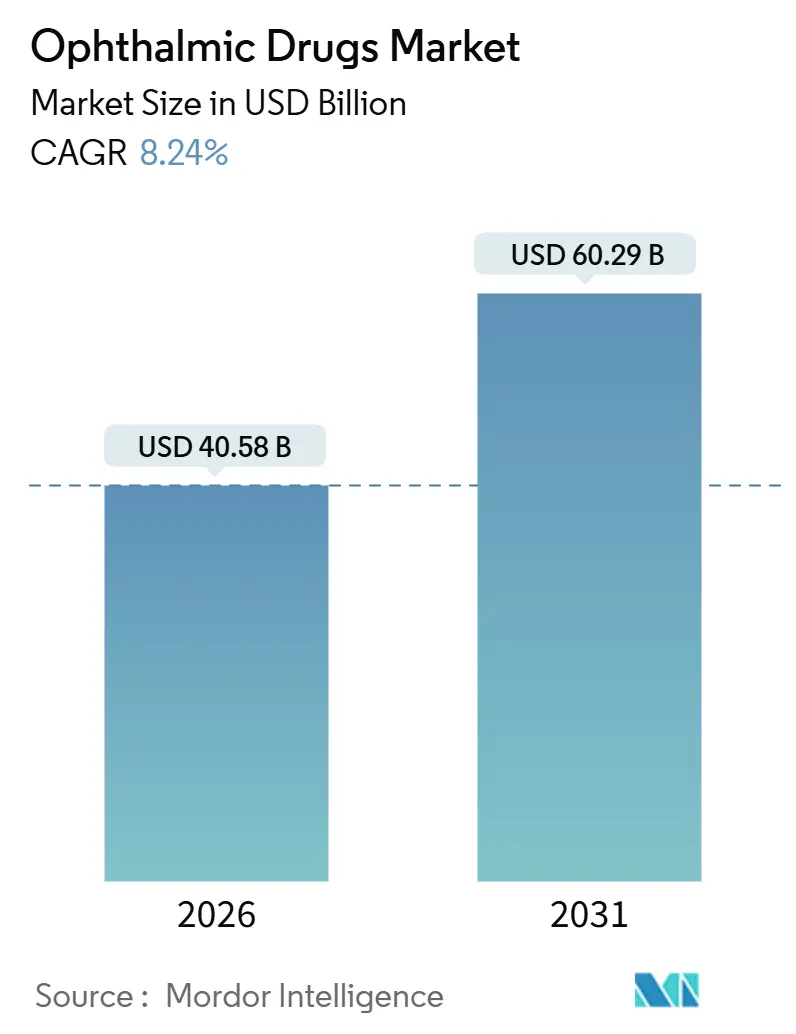

The Ophthalmic Drugs Market size is estimated at USD 40.58 billion in 2026, and is expected to reach USD 60.29 billion by 2031, at a CAGR of 8.24% during the forecast period (2026-2031).

Demographic aging, surging diabetes prevalence, and a rich pipeline of gene and cell therapies are nurturing steady demand, while AI-assisted discovery and localized active-pharmaceutical-ingredient (API) production are reshaping development and supply-chain strategies. Fiscal headwinds from patent expiries are being partly neutralized by premium-priced sustained-release implants and extended-interval biologics, and distribution is migrating toward e-commerce as telehealth prescriptions gain traction. Competitive intensity remains brisk: incumbents rely on lifecycle extensions, whereas emerging biotechs court investors with first-in-class mechanisms. Climate-linked preservative restrictions and sterility regulations are inflating compliance costs, but they also catalyze preservative-free reformulations that differentiate on safety.

Key Report Takeaways

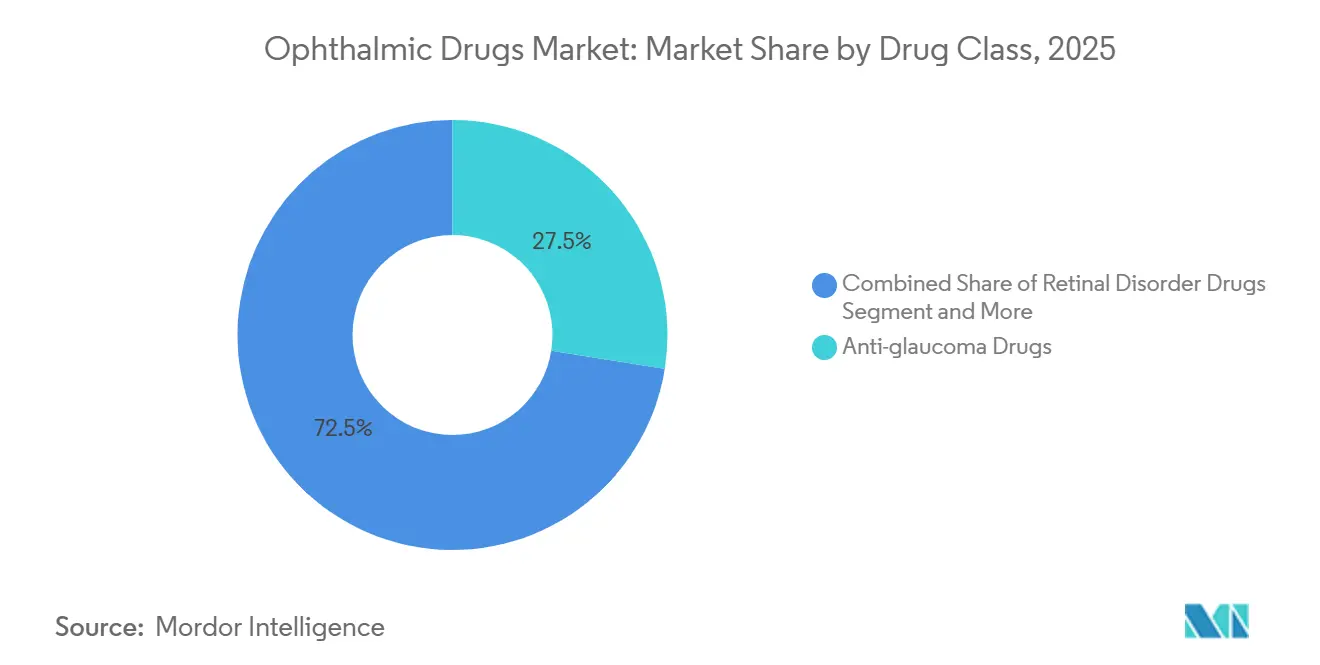

- By drug class, anti-glaucoma agents led with 27.55% of the ophthalmic drugs market share in 2025; retinal disorder therapies are forecast to compound at a 16.25% CAGR through 2031.

- By indication, retinal disorders captured 35.53% share of the ophthalmic drugs market size in 2025, while ocular infections and inflammation are expanding at a 12.85% CAGR to 2031.

- By dosage form, eye drops accounted for 63.63% of the ophthalmic drugs market size in 2025, and implants or inserts are projected to post an 11.87% CAGR between 2026 and 2031.

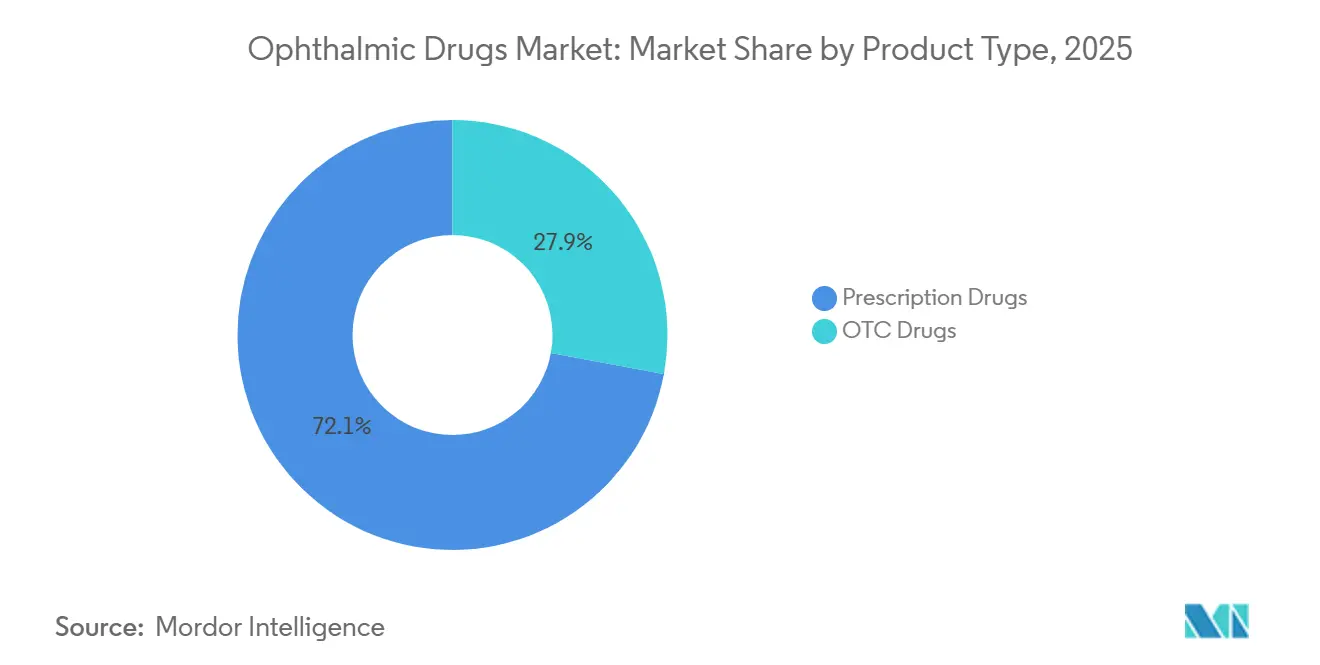

- By product type, prescription medicines held 72.13% of the ophthalmic drugs market share in 2025; the OTC segment is rising at a 9.7% CAGR.

- By distribution channel, hospital pharmacies controlled 47.13% of sales in 2025, yet online pharmacies are advancing at an 11.81% CAGR through 2031.

- By geography, North America commanded 42.13% share in 2025; Asia-Pacific is the fastest region, climbing at a 12.21% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Ophthalmic Drugs Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population and chronic ocular disease surge | +1.8% | Global, acute in North America, Europe, East Asia | Long term (≥ 4 years) |

| Rising diabetes incidence fueling retinal therapies | +2.1% | Global, concentrated in North America, China, India, Middle East | Medium term (2-4 years) |

| Rx-to-OTC switches broadening access | +0.7% | North America, Europe, pilot APAC markets | Short term (≤ 2 years) |

| Gene and cell-therapy pipeline attracting capital | +1.5% | North America, EU, clinical spillover in Australia, Japan | Long term (≥ 4 years) |

| AI-assisted discovery shortening development | +0.9% | North America, Europe, China, Singapore | Medium term (2-4 years) |

| Localized API manufacturing reducing tariff risk | +1.2% | India, China, Mexico, Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population And Chronic Ocular Disease Prevalence Surge

Global life expectancy gains are swelling the population aged 60 and above, which the United Nations forecasts will double to 2.1 billion by 2050. Higher age correlates strongly with glaucoma, macular degeneration, and cataract diagnoses, prompting payers to prioritize preventative screening. Japan illustrates the pressure point: a 29% senior-citizen share in 2026 coincides with a 12% rise in glaucoma diagnoses since 2020, taxing clinic capacity and propelling demand for at-home monitoring and quarterly implants[1]Ministry of Health, Labour and Welfare, “Health Statistics,” mhlw.go.jp. Health systems now encourage self-administered or outpatient therapies to contain procedure costs, pushing manufacturers toward long-acting inserts that reduce visit frequency. These dynamics amplify the ophthalmic drugs market’s growth runway, especially for sustained-release formats. Venture funding also gravitates toward devices that pair with digital adherence apps to manage therapy outside clinical settings.

Rising Diabetes Incidence Driving Retinal Disorder Therapies

Diabetic retinopathy and macular edema track the diabetes epidemic, which the International Diabetes Federation expects to swell to 783 million adults by 2045[2]International Diabetes Federation, “Diabetes Atlas,” idf.org. The U.S. FDA cleared EYLEA HD in 2023, extending intravitreal dosing intervals to 16 weeks, lessening clinic loads while preserving efficacy. Genentech’s Susvimo port-delivery system earned approval in 2024, shifting revenue toward refill cartridges rather than episodic injections. These innovations create annuity-style cash flows and intensify competition in the retinal segment of the ophthalmic drugs market. Payers, recognizing avoided procedure costs, have demonstrated reimbursement flexibility for technologies that cut injection frequency. Consequently, capital allocation is tilting toward device-assisted delivery that can secure premium pricing and loyalty.

Rx-to-OTC Switches Expanding Consumer Access

Regulators are expediting nonprescription status for topical antihistamines and lubricants, as evidenced by the FDA’s streamlined OTC monograph pathway in 2023. The European Medicines Agency followed with antihistamine eye-drop switches in 2024. OTC migration opens mass retail shelves but compresses per-unit margins, compelling brands to invest in consumer advertising and preservative-free singles that justify a price premium. Dry eye and allergy therapies especially benefit because self-diagnosis is common and adherence hinges on convenience. The trend also dilutes insurance friction, smoothing patient uptake and scaling volumes for late life-cycle assets.

Gene And Cell-Therapy Pipeline Attracting New Capital

Conditional European approval of LUMEVOQ in 2024 marked the first mitochondrial disease gene therapy, signaling commercial validation for one-time treatments. Lineage Cell Therapeutics posted encouraging 12-month OpRegen data, sustaining visual acuity in dry AMD, while Adverum advanced Ixo-vec into pivotal trials aiming to replace serial anti-VEGF injections. Manufacturing costs often exceed USD 500,000 per dose, yet payers are open to lump-sum coverage that removes lifelong injection outlays. U.S. regulators have prioritized expedited review for rare retinal diseases, accelerating time-to-market. These developments heighten investor enthusiasm; however, scale-up complexity remains a gating factor.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Patent expiries and generic erosion | -1.4% | North America, Europe | Short term (≤ 2 years) |

| High formulation complexity and sterility rules | -0.9% | Global, stricter in North America, EU, Japan | Medium term (2-4 years) |

| Patient non-adherence to multi-dose regimens | -0.6% | Global, acute in elderly and low-income regions | Long term (≥ 4 years) |

| Climate-driven preservative bans | -0.5% | Europe, spillover to North America, select APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Patent Expiries And Generic Erosion Compressing Margins

Lucentis biosimilars entered Europe in 2022 and the United States in 2024 at 30% discounts, slicing incumbents’ revenue trajectories. Generic timolol prices fell further when preservative-free versions debuted in the U.S. market at 40% below legacy brands. Innovators respond with extended-release or high-dose variants, yet Medicare price-negotiation clauses amplify pressure. Net effect: short-term revenue declines that temper ophthalmic drugs market expansion until replacement products scale.

High Formulation Complexity And Stringent Sterility Regulations

Revised FDA aseptic-processing guidance in 2024 mandated enhanced environmental monitoring, adding 6–12 months to validation timelines. EMA Annex 1 revisions and Japan’s PMDA alignment impose similar cleanroom upgrades costing up to USD 20 million per site. Smaller contract development organizations face capacity bottlenecks, consolidating manufacturing in the hands of cash-rich incumbents and slowing newcomer entry into the ophthalmic drugs market.

Segment Analysis

By Drug Class: Retinal Therapies Outpace Legacy Glaucoma Agents

Retinal therapeutics generated the largest revenue increment in 2025 and are advancing at a 16.25% CAGR, while anti-glaucoma drugs, which held 27.55% of the ophthalmic drugs market share in 2025, are expanding more slowly. The ophthalmic drugs market size for retinal therapies will expand further as high-dose anti-VEGF biologics and gene therapies move into commercial channels. Apellis’s Syfovre launched the first lesion-slowing treatment for geographic atrophy, unlocking a U.S. patient pool exceeding 1 million. Dry eye therapeutics, led by Bausch + Lomb’s lipid-based Miebo, continue to post double-digit growth owing to digital-screen fatigue in working adults. Anti-infective lines suffer from antimicrobial-resistance concerns; however, fourth-generation fluoroquinolones approved in 2024 offer broader coverage. Combination therapies like Rocklatan simplify regimens and justify premiums but remain niche because of price sensitivity.

During 2026-2031, investment gravitates toward retinal and dry eye mechanisms with de-risked reimbursement pathways. Anti-glaucoma innovation focuses on preservative-free or once-weekly drops, reflecting incremental rather than breakthrough change. Capital flows mirror this divergence: venture funding chases retinal gene therapy platforms, while private equity backs manufacturing scale-ups for generic glaucoma formulations.

Note: Segment shares of all individual segments available upon report purchase

By Indication: Retinal Disorders Dominate, Infections Surge

Retinal indications secured 35.53% of 2025 sales and maintain pricing power because therapies often cost more than USD 2,000 per injection. Ocular infections and inflammation, buoyed by rising cataract surgeries, are predicted to post a 12.85% CAGR. Dry eye therapies receive a lift from alternative delivery modes like Tyrvaya’s nasal spray, widening access for contact-lens wearers and screen-heavy professionals. Glaucoma volumes remain high but revenue growth lags due to generics. Allergic conjunctivitis is steady yet migratory toward OTC, thinning prescription tallies. Presbyopia treatments are emerging, with Vuity’s 2023 launch validating pharmacologic accommodation modulation.

Segment differentials will persist: retinal care benefits most from biologic and gene therapy advances, while infections leverage novel antibiotics to stay ahead of resistance. Manufacturers aiming at glaucoma need neuroprotective angles or device-based adherence solutions to reignite growth.

By Dosage Form: Implants Gain Ground On Drops

Eye drops remain dominant at 63.63% of 2025 revenues, yet implants and inserts are projected to clock an 11.87% CAGR by 2031 as adherence advantages resonate with clinicians and payers. Durysta, released by Glaukos, offers four-month intraocular pressure control, and its commercial uptake shows physicians’ readiness to shift procedural paradigms. Ointments and gels occupy postoperative niches, whereas systemic tablets continue to wane. Nasal and spray routes, inaugurated by Tyrvaya, introduce patient-preferred alternatives that bypass ocular surface discomfort.

Over the forecast, sustained-release implants are poised to siphon share from multi-dose drops, especially in chronic conditions, as cost-effectiveness analyses favor fewer visits. However, surgical placement requirements and reimbursement complexity temper immediate replacement.

By Product Type: Prescription Drugs Retain Dominance

Prescription medicines held 72.13% of sales in 2025 and will remain the backbone of the ophthalmic drugs market as biologics, gene, and cell therapies necessitate specialist oversight and cold-chain integrity. OTC offerings expand behind antihistamine and lubricant switches, capturing volume with retail convenience. Premium loyalty programs and digital coupons enable manufacturers to defend scripts from generic substitution. Online pharmacist portals now deliver both categories, further widening consumer choice.

While the ophthalmic drugs market size for OTC products will climb, the absolute revenue delta favors prescription segments because of higher unit pricing. Still, mass-market OTC penetration broadens brand visibility, potentially converting self-treating patients into prescription therapies as diseases progress.

By Distribution Channel: Online Pharmacies Disrupt Traditional Models

Hospital pharmacies commanded 47.13% of 2025 turnover owing to in-clinic preparation of intravitreal injections. Yet online pharmacies, advancing at an 11.81% CAGR, are reshaping refill behavior for chronic diseases. Amazon Pharmacy’s same-day service and transparent pricing prompt legacy chains to fast-follow, accelerating digital adoption. Retail storefronts preserve foot traffic via immunizations and clinical-service bundles but concede repeat prescription volumes to automated delivery.

Manufacturers now pilot direct-to-patient logistics that bypass wholesalers, improving margins and capturing adherence data. Regulatory oversight on interstate fulfillment and pharmacovigilance adds complexity, yet consumer expectation for frictionless service sets a durable trend.

Geography Analysis

North America generated 42.13% of 2025 revenue, supported by Medicare Part B coverage of anti-VEGF injections and early uptake of premium implants. The region benefits from robust clinician density and high diagnostic rates, sustaining elevated per-capita spending levels. Canada and Mexico, while smaller, exhibit generic adoption that tempers unit prices but broadens access. Competitive launches like EYLEA HD cement biologics’ hold, and payer frameworks continue to reimburse innovations that reduce clinic visits[3]Centers for Medicare & Medicaid Services, “Medicare Coverage,” cms.gov.

Europe represents a mature yet regulation-intensive landscape. Centralized EMA approvals streamline multi-nation launches, but national health technology assessments demand real-world evidence, compressing margins. Germany, France, and the United Kingdom remain launch priorities, though reference pricing keeps price escalation in check. The ophthalmic drugs market size in Europe grows steadily from sustained-release approvals that demonstrate cost offset against surgical resource use. Climate-driven preservative restrictions are steeper here, compelling earlier reformulation investment.

Asia-Pacific is the fastest-growing territory at a 12.21% CAGR through 2031, propelled by China’s expanded reimbursement list and India’s API self-sufficiency pushes. Urbanization and myopia epidemics add demand for glaucoma and retinal therapies. Japan’s senior population maintains high prescription volumes, while Australia and South Korea serve as early-adopter hubs for digital adherence platforms. Local manufacturers leverage production-linked incentives to capture regional share, sharpening price competition but also enlarging patient reach. Southeast Asian nations invest in tele-ophthalmology to bridge specialist shortages, funneling prescriptions through online pharmacy channels.

Latin America and the Middle East & Africa collectively remain modest contributors but register double-digit growth off low bases. Brazilian generic houses are scaling topical formulations, and Gulf Cooperation Council nations invest in vision-care infrastructure. Currency volatility and tariff barriers temper premium biologic uptake, yet public-health campaigns to reduce blindness ensure baseline therapy demand.

Competitive Landscape

Market players, including AbbVie (formerly Allergan), Novartis, Regeneron, Alcon, and Bausch + Lomb, collectively controlled significant global revenue in 2025, underscoring a moderately consolidated market structure. These incumbents maintain share via high-dose or preservative-free extensions and device-enabled formulations that refresh patent life. Regeneron’s EYLEA franchise still generated USD 6.8 billion in 2024, though biosimilar entrants and Medicare negotiations impose pricing tension.

Mid-sized innovators such as Ocular Therapeutix, Apellis, and Glaukos focus on first-in-class implants and gene therapies targeting retinal and glaucoma niches. Their agility attracts venture capital, accelerating clinical timelines. GenSight’s 2024 European approval for LUMEVOQ validated the one-and-done gene therapy commercial model and signaled investor appetite for similar ophthalmic assets. Patent-filing activity rose 18% in 2024 per WIPO, indicating sustained innovation despite generic erosion.

Technology partnerships are proliferating. Insilico Medicine’s AI alliance with a major ophthalmic brand exemplifies computational design convergence with wet-lab expertise. Companies pair digital adherence tools with drug launches to secure payer contracts that hinge on real-world outcomes. Local manufacturing capacity, especially in India and China, offers supply security but also arms generic rivals with cost advantages, spurring branded players to differentiate through value-added services.

Ophthalmic Drugs Industry Leaders

AbbVie (Allergan)

Novartis AG

Regeneron Pharmaceuticals Inc.

Alcon Inc.

Bausch & Lomb Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Amneal received FDA approval for bimatoprost ophthalmic solution 0.01% as a generic to LUMIGAN.

- May 2025: Alcon’s TRYPTYR (acoltremon ophthalmic solution) 0.003% gained FDA clearance for dry eye disease.

Global Ophthalmic Drugs Market Report Scope

As per the scope of the report, ophthalmic drugs are used to treat various disorders associated with the eyes, such as glaucoma, cataracts, and diabetic retinopathy, to name a few. The ophthalmic drugs market report is segmented by drug class, indication, dosage form, product type, distribution channel, and geography. By drug class, the market is segmented into anti-glaucoma drugs, dry eye drugs, anti-inflammatory drugs, anti-infective drugs, retinal disorder drugs, anti-allergy drugs, and combination therapies. By indication, the market is segmented into glaucoma, dry eye syndrome, retinal disorders, allergic conjunctivitis, ocular infections & inflammation, and others. By dosage form, the market is segmented into eye drops, ointments & gels, capsules & tablets, implants & inserts, and sprays & nasal delivery. By product type, the market is segmented into OTC drugs and prescription drugs. By distribution channel, the market is segmented into hospital pharmacies, retail pharmacies & drug stores, and online pharmacies. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East, and Africa, and South America. The industry report also covers the estimated market share and market trends for 17 countries across major global regions. The market research report offers the value (in USD) for the above segments.

| Anti-glaucoma Drugs |

| Dry Eye Drugs |

| Anti-inflammatory Drugs |

| Anti-infective Drugs |

| Retinal Disorder Drugs |

| Anti-allergy Drugs |

| Combination Therapies |

| Glaucoma |

| Dry Eye Syndrome |

| Retinal Disorders |

| Allergic Conjunctivitis |

| Ocular Infections & Inflammation |

| Others (Presbyopia, Post-surgical, Rare Diseases) |

| Eye Drops |

| Ointments & Gels |

| Capsules & Tablets |

| Implants & Inserts |

| Sprays & Nasal Delivery |

| Prescription Drugs |

| OTC Drugs |

| Hospital Pharmacies |

| Retail Pharmacies & Drug Stores |

| Online Pharmacies |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Anti-glaucoma Drugs | |

| Dry Eye Drugs | ||

| Anti-inflammatory Drugs | ||

| Anti-infective Drugs | ||

| Retinal Disorder Drugs | ||

| Anti-allergy Drugs | ||

| Combination Therapies | ||

| By Indication | Glaucoma | |

| Dry Eye Syndrome | ||

| Retinal Disorders | ||

| Allergic Conjunctivitis | ||

| Ocular Infections & Inflammation | ||

| Others (Presbyopia, Post-surgical, Rare Diseases) | ||

| By Dosage Form | Eye Drops | |

| Ointments & Gels | ||

| Capsules & Tablets | ||

| Implants & Inserts | ||

| Sprays & Nasal Delivery | ||

| By Product Type | Prescription Drugs | |

| OTC Drugs | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies & Drug Stores | ||

| Online Pharmacies | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of ophthalmic drugs?

The segment stands at USD 40.58 billion in 2026 and is projected to reach USD 60.29 billion by 2031, advancing at an 8.24% CAGR.

Which therapy area generates the highest revenue within ophthalmic treatments?

Retinal disorder drugs contribute the largest share, accounting for 35.53% of 2025 sales and expanding at a 16.25% compound rate through 2031.

How fast is Asia-Pacific demand for ophthalmic medicines growing?

Asia-Pacific revenue is forecast to rise at a 12.21% CAGR to 2031, outpacing all other regions as insurance coverage and local API manufacturing expand.

Why are implants and inserts gaining adoption in eye care?

Sustained-release implants reduce clinic visits and improve adherence, which helps offset their higher upfront cost; they are expected to grow at 11.87% annually.

How do gene therapies affect long-term treatment costs for retinal diseases?

One-time gene therapies carry manufacturing costs surpassing USD 500,000 per dose, but payers increasingly support them because they can eliminate lifelong injection expenses.

What drives the shift from hospital to online pharmacy dispensing of eye treatments?

Telehealth prescriptions and same-day fulfillment services make refills convenient, enabling online pharmacies to expand at an 11.81% CAGR while hospital channels remain focused on in-clinic procedures.