Ophthalmology Drug & Device Market Size

| Study Period | 2019 - 2029 |

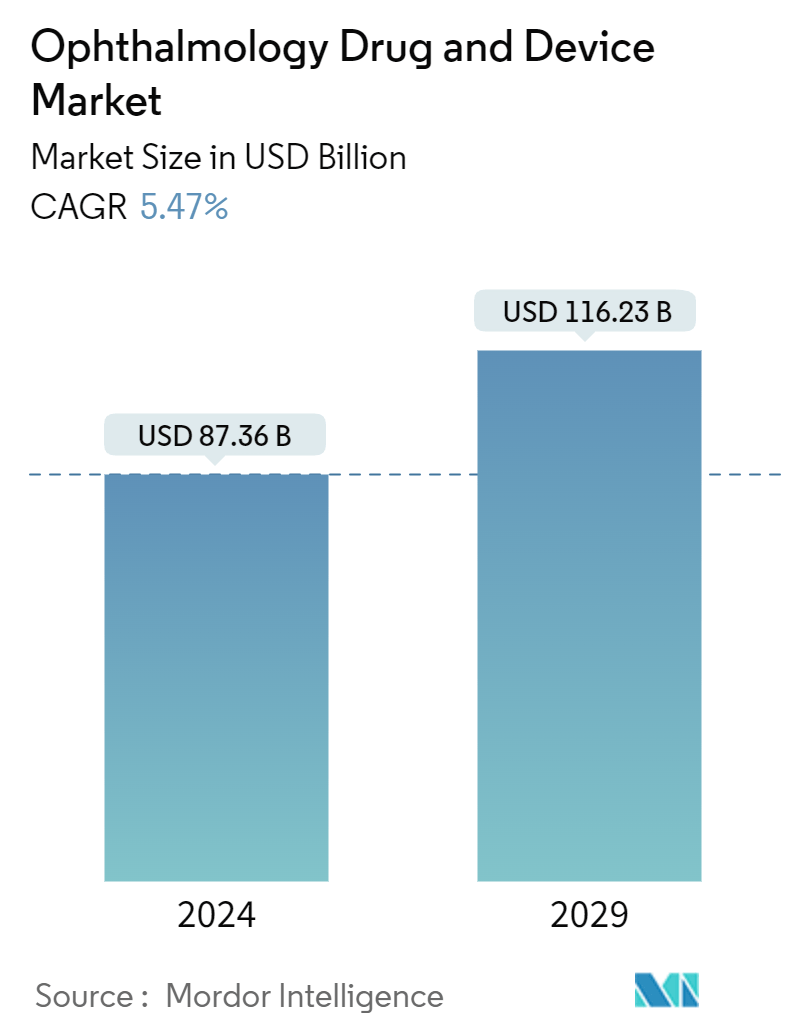

| Market Size (2024) | USD 87.36 Billion |

| Market Size (2029) | USD 116.23 Billion |

| CAGR (2024 - 2029) | 5.47 % |

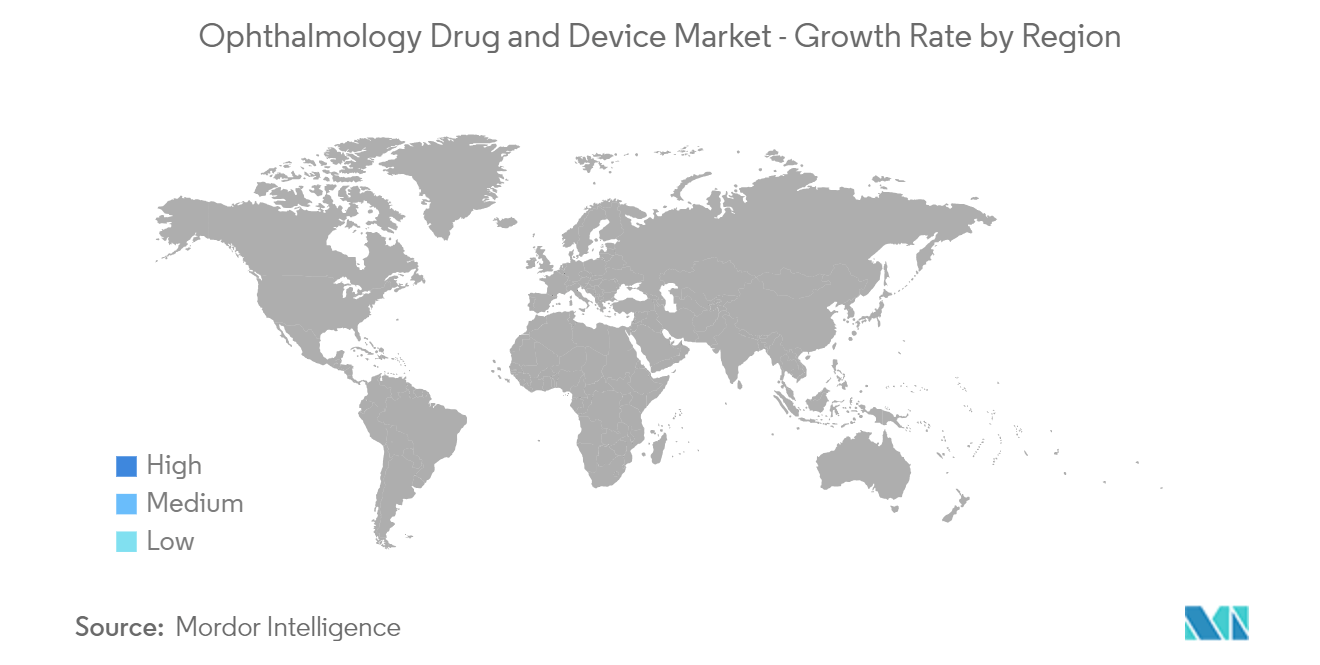

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Ophthalmology Drug & Device Market Analysis

The Ophthalmology Drug And Device Market size is estimated at USD 87.36 billion in 2024, and is expected to reach USD 116.23 billion by 2029, at a CAGR of 5.47% during the forecast period (2024-2029).

The COVID-19 pandemic had a significant impact on the market initially as several countries were in lockdown, and trades were suspended with other countries with travel restrictions, leading to a decline in eye diagnoses. As a cautionary measure, many ophthalmologists temporarily closed their practices during the pandemic. According to an article published by the Indian Journal of Ophthalmology in December 2021, a survey was conducted among the All India Ophthalmological Society (AIOS) members, which stated that COVID-19 had adversely affected ophthalmic care services across the whole of India. As the number of COVID-19 cases has decreased significantly, the market has recovered and started to gain traction. Hence, the market is expected to have stable growth during the forecast period of the study.

Certain factors driving the market's growth include the impact of the prevalence of eye disease, demographic shift, technological advancements in the field of ophthalmology, and the rising geriatric population. According to the data updated by WHO in October 2022, it is estimated at least 2.2 billion people will have a near or distant vision impairment globally. Among these, at least 1 billion people's vision impairment could have been prevented or yet to get addressed. These 1 billion people include those with moderate or severe distance vision impairment or blindness due to various diseases like unaddressed refractive error (88.4 million), cataract (94 million), age-related macular degeneration (8 million), glaucoma (7.7 million), diabetic retinopathy (3.9 million), as well as near vision impairment caused by unaddressed presbyopia (826 million). In many countries, cataract surgery is the most common surgical procedure performed, significantly improving the quality of life of the elderly population at low costs. An increase in the elderly population and the high prevalence of ophthalmic disorders increases the demand for ophthalmological devices and projects the future cataract surgery needs vital for human health resources, hospitals, and surgical centre management and planning. Other factors, such as the availability of new devices and new drugs and the growing incidence of eye disease, are also expected to drive the market over the forecast period.

In addition, new product launches and strategic activities by major players in the market are positively affecting the growth of the studied market. For example, in June 2022, Biogen Inc. and Samsung Bioepis Co., Ltd. launched ranibizumab-nuna (Byooviz, Biogen), an ophthalmic biosimilar referencing ranibizumab (Lucentis, Genentech) in the US. Thus, due to the product launches and partnerships, the studied market is expected to grow significantly over the forecast period.

Therefore, owing to the factors above, the studied market is anticipated to witness growth over the analysis period. However, the higher cost of ophthalmic devices and treatment and strict FDA guidelines for drug approval is likely to impede the market's growth.

Ophthalmology Drug & Device Industry Overview

The Glaucoma Segment is Expected to Show Significant Growth in the Forecast Years

Globally, glaucoma is one of the most common causes of vision loss or blindness. Being irreversible, the early detection and management of glaucoma are of utmost importance. With increasing ageing, the incidence of glaucoma is expected to rise shortly, driving market growth.

According to the data published by the MoHFW, Government of India, in March 2021, glaucoma is estimated to be the second most common cause of blindness worldwide, and WHO estimated that 4.5 million people are blind due to glaucoma. The data further revealed that in India, glaucoma is the leading cause of irreversible blindness, with a minimum of 12 million people affected and nearly 1.2 million people blind from the disease. It is also estimated that more than 90% of glaucoma cases are undiagnosed in the community. With the high prevalence of glaucoma, it is expected to drive market growth in the coming years.

Primary open-angle glaucoma is a significant public health burden in Europe, likely increasing the demand for devices soon. For instance, as per an article published by ScienceDirect in August 2022, most individuals affected with glaucoma require regular active monitoring and management to prevent irreversible vision loss. The article further states glaucoma care currently accounts for an estimated 20% workload of hospital eye service outpatients in the UK, with over 1 million glaucoma-related outpatient visits made each year to hospital eye services in England. With an ageing population, increased access to sight testing, and more rigorous optometry screening (including retinal imaging), the number of glaucoma-related outpatient visits is expected to rise.

Furthermore, according to a research article published by the Journal of Ophthalmology in May 2022, glaucoma is considered one of the most frequent vision-threatening eye diseases. It is frequently associated with excessive Intraocular Pressure (IOP) that causes vision loss and possibly blindness if the eye's (optic) nerve fails. Factors such as the increasing geriatric population are also expected to increase the number of glaucoma patients as the disorder primarily affects older people.

Thus, the high incidence of glaucoma is expected to raise demand for drugs and devices and show significant growth over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

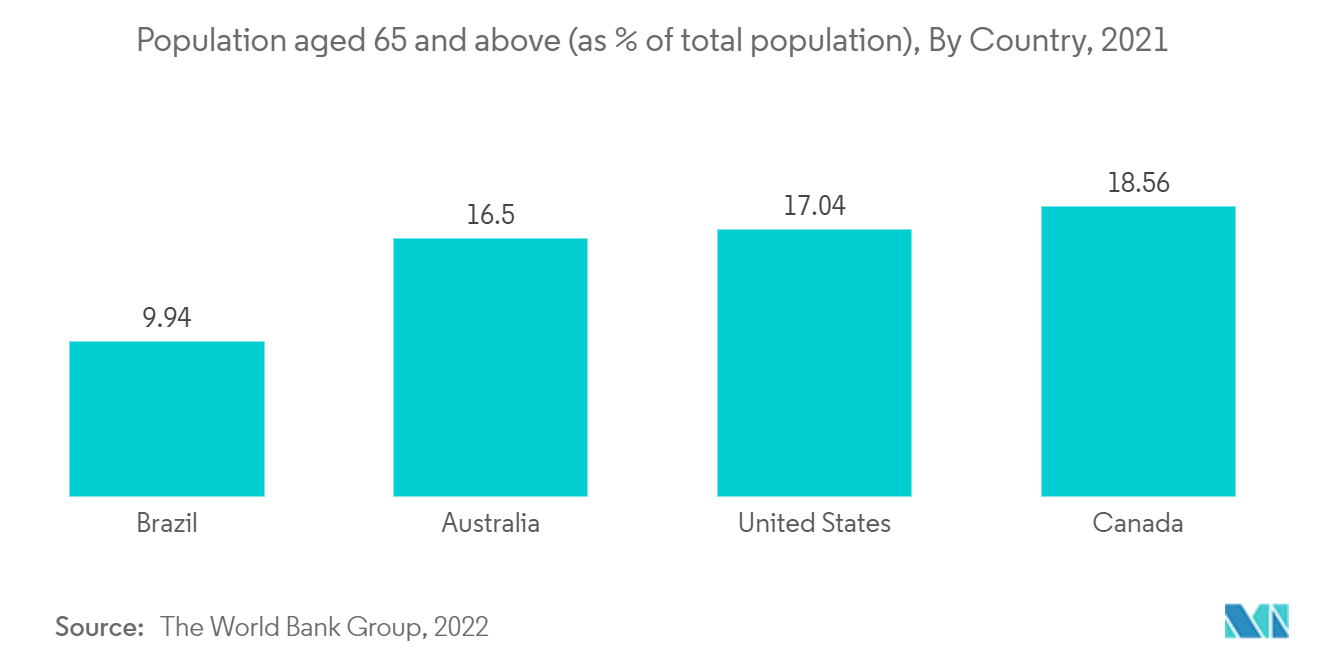

Due to the presence of well-established healthcare facilities, the rise in the geriatric population in the region, and the presence of large companies, the North American region is expected to grow significantly. Due to the constant increase in the American elderly population, a move toward vision correction and its usage among crucial demographics, an increase in rates for most eyewear types was observed in the US. The United States holds a substantial share of the ophthalmology diagnostics market in the North American region. The market is expected to grow due to the rapidly increasing geriatric population and the rising prevalence of eye diseases due to high stress and unhealthy lifestyles, which can result in conditions such as diabetic retinopathy. The geriatric population is increasing, and it is more susceptible to developing eye diseases, which is further anticipated to widen the base for market growth.

There has been a rising prevalence of eye diseases, such as glaucoma, cataract, macular degeneration, and diabetic retinopathy, which is anticipated to propel the market over the forecast period. As per the data by the Glaucome Research Foundation in February 2022, it is estimated that over 3 million Americans have glaucoma. Still, only half of those are aware of the disease. In the United States, more than 120,000 are blind from glaucoma, accounting for 9% to 12% of all cases of blindness. Hence, an increase in eye disorders will lead to a growing demand for drugs and devices.

Key product launches, high concentration of market players, or manufacturers' presence in the United States are some factors driving the studied market growth in the country. For instance, in April 2022, Sandoz launched its generic combination eyedrop brimonidine tartrate/timolol maleate ophthalmic solution 0.2%/0.5%. It is an AB-rated generic equivalent to AbbVie's COMBIGAN to lower eye pressure in patients with ocular hypertension (high eye pressure) in the United States. Furthermore, in December 2021, Allergan launched VUITY (pilocarpine HCl ophthalmic solution) 1.25%, the first and only eye drop approved by the US FDA to treat presbyopia. These continuous product launches in the region are anticipated to drive market growth in the country.

Therefore, owing to the factors above, the growth of the studied market is anticipated in the North American region.

Ophthalmology Drug & Device Industry Overview

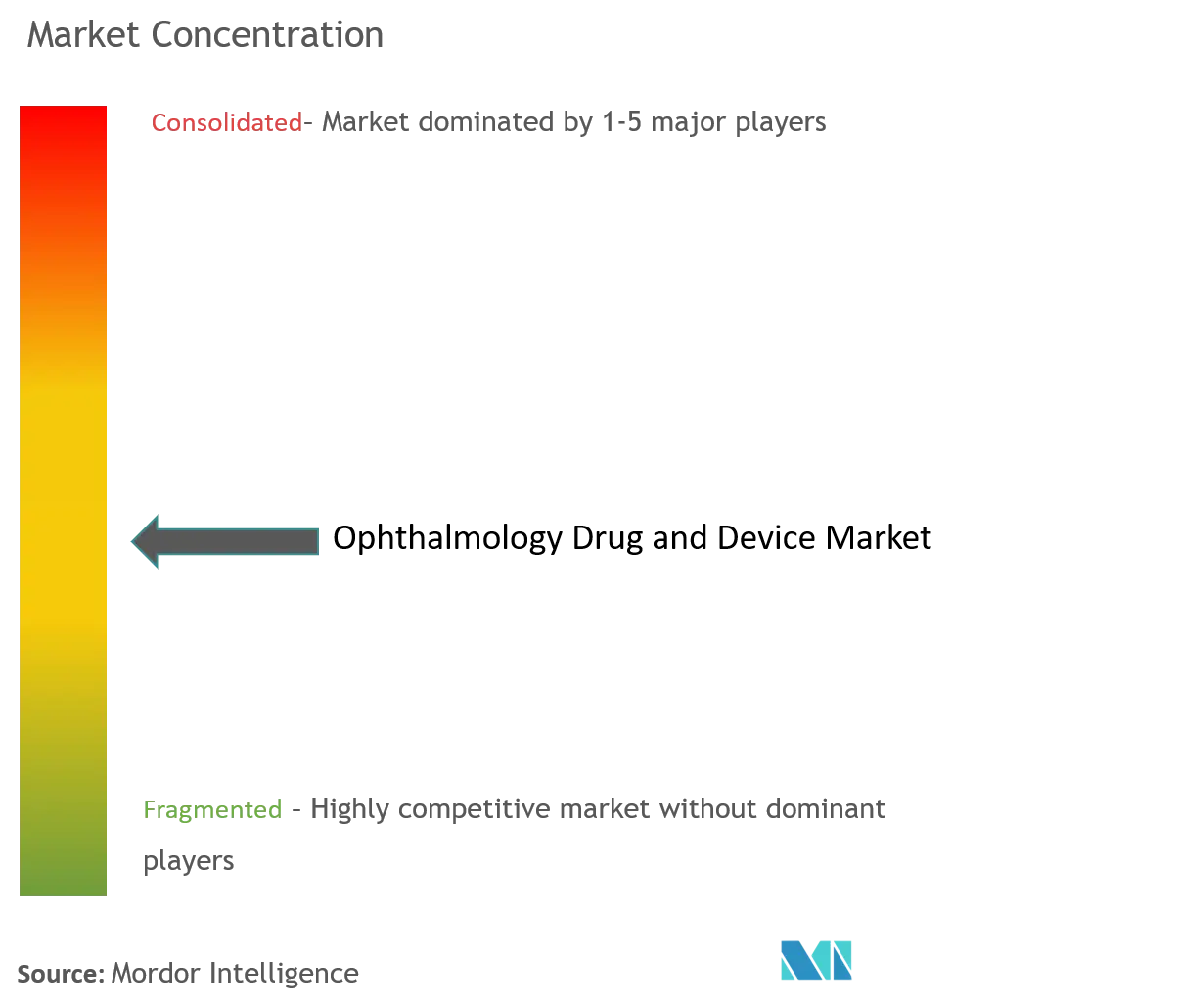

The ophthalmology drug and device market are moderately fragmented in nature. The competitive landscape includes an analysis of a few international and local companies that hold market shares and are well known. It consists of major players such as Alcon Inc., Bausch Health Companies Inc., Carl Zeiss Meditec AG, Essilor International SA, Haag-Streit Group (Metall Zug AG), Johnson & Johnson, Nidek Co. Ltd, Topcon Corporation, Ziemer Group AG, among others.

Ophthalmology Drug & Device Market Leaders

-

Alcon Inc.

-

Bausch Health Companies Inc.

-

Carl Zeiss Meditec AG

-

Johnson & Johnson

-

Topcon Corporation

*Disclaimer: Major Players sorted in no particular order

Ophthalmology Drug & Device Market News

- October 2022: Remidio launched Instaref R20, a lightweight and portable ophthalmic auto refractometer at the American Academy of Ophthalmology in Chicago.

- September 2022: Santen and UBE announced that the FDA has approved Omlonti (omidenepag isopropyl ophthalmic solution) 0.002% eye drops. It reduces elevated intraocular pressure in patients with primary open-angle glaucoma or ocular hypertension.

Ophthalmology Drug And Device Market Report - Table of Contents

1. INTRODUCTION

1.1 Study Assumptions and Market Definition

1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

4.1 Market Overview

4.2 Market Drivers

4.2.1 Demographic Shift and Impact of Prevalence of Eye Disease

4.2.2 Technological Advancements in the Field of Ophthalmology

4.3 Market Restraints

4.3.1 Higher Cost of the Ophthalmic Devices and Treatment

4.3.2 Strict FDA Guidelines for Drug Approval

4.4 Porter's Five Forces Analysis

4.4.1 Bargaining Power of Suppliers

4.4.2 Bargaining Power of Buyers/Consumers

4.4.3 Threat of New Entrants

4.4.4 Threat of Substitute Products

4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 By Product

5.1.1 Devices

5.1.1.1 Surgical Devices

5.1.1.1.1 Intraocular Lenses

5.1.1.1.2 Ophthalmic Lasers

5.1.1.1.3 Other Surgical Devices

5.1.1.2 Diagnostic Devices

5.1.2 Drugs

5.1.2.1 Glaucoma Drugs

5.1.2.2 Retinal Disorder Drugs

5.1.2.3 Dry Eye Drugs

5.1.2.4 Allergic Conjunctivitis and Inflammation Drugs

5.1.2.5 Other Drugs

5.2 By Disease

5.2.1 Glaucoma

5.2.2 Cataract

5.2.3 Age-Related Macular Degeneration

5.2.4 Inflammatory Diseases

5.2.5 Refractive Disorders

5.2.6 Other Diseases

5.3 Geography

5.3.1 North America

5.3.1.1 United States

5.3.1.2 Canada

5.3.1.3 Mexico

5.3.2 Europe

5.3.2.1 Germany

5.3.2.2 United Kingdom

5.3.2.3 France

5.3.2.4 Italy

5.3.2.5 Spain

5.3.2.6 Rest of Europe

5.3.3 Asia-Pacific

5.3.3.1 China

5.3.3.2 Japan

5.3.3.3 India

5.3.3.4 Australia

5.3.3.5 South Korea

5.3.3.6 Rest of Asia-Pacific

5.3.4 Middle East and Africa

5.3.4.1 GCC

5.3.4.2 South Africa

5.3.4.3 Rest of Middle East and Africa

5.3.5 South America

5.3.5.1 Brazil

5.3.5.2 Argentina

5.3.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

6.1 Company Profiles

6.1.1 Alcon Inc.

6.1.2 Bausch Health Companies Inc.

6.1.3 Carl Zeiss Meditec AG

6.1.4 Essilor International SA

6.1.5 Haag-Streit Group (Metall Zug AG)

6.1.6 Johnson & Johnson

6.1.7 Nidek Co. Ltd

6.1.8 Topcon Corporation

6.1.9 NIDEK Co. Ltd

6.1.10 Lumenis Ltd

6.1.11 Ziemer Ophthalmic Systems AG

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Ophthalmology Drug & Device Industry Segmentation

As per the scope of the report, ophthalmology drug and device includes all the products that ophthalmologists use to diagnose, treat, and care for the eyes. The Ophthalmology Drug and Device Market are segmented by product (devices and drugs), disease (Glaucoma, Cataract, age-related macular degeneration, inflammatory diseases, refractive disorders, and other diseases), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major global regions. The report offers the value in ( USD million) for the abovementioned segments.

| By Product | ||||||||

| ||||||||

|

| By Disease | |

| Glaucoma | |

| Cataract | |

| Age-Related Macular Degeneration | |

| Inflammatory Diseases | |

| Refractive Disorders | |

| Other Diseases |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Ophthalmology Drug And Device Market Research Faqs

How big is the Ophthalmology Drug And Device Market?

The Ophthalmology Drug And Device Market size is expected to reach USD 87.36 billion in 2024 and grow at a CAGR of 5.47% to reach USD 116.23 billion by 2029.

What is the current Ophthalmology Drug And Device Market size?

In 2024, the Ophthalmology Drug And Device Market size is expected to reach USD 87.36 billion.

Which is the fastest growing region in Ophthalmology Drug And Device Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Ophthalmology Drug And Device Market?

In 2024, the North America accounts for the largest market share in Ophthalmology Drug And Device Market.

What years does this Ophthalmology Drug And Device Market cover, and what was the market size in 2023?

In 2023, the Ophthalmology Drug And Device Market size was estimated at USD 82.58 billion. The report covers the Ophthalmology Drug And Device Market historical market size for years: 2019, 2020, 2021, 2022 and 2023. The report also forecasts the Ophthalmology Drug And Device Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Ophthalmology Drug And Device Industry Report

Statistics for the 2024 Ophthalmology Drug and Device market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Ophthalmology Drug and Device analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.