| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 126.32 Billion |

| Market Size (2030) | USD 167.69 Billion |

| CAGR (2025 - 2030) | 5.83 % |

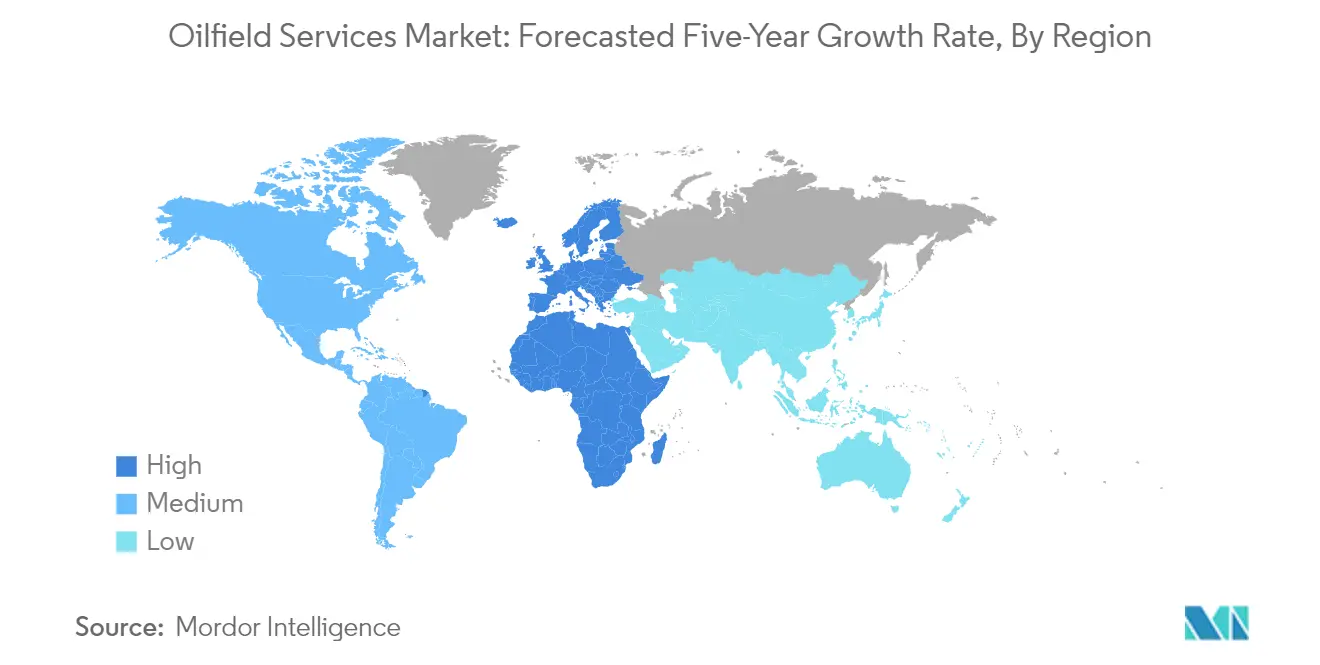

| Fastest Growing Market | Europe |

| Largest Market | North America |

| Market Concentration | High |

Major Players Market Major Players")

*Disclaimer: Major Players sorted in no particular order |

Market Size")

Oilfield Services (OFS) Market Analysis

The Oilfield Services Market size is estimated at USD 126.32 billion in 2025, and is expected to reach USD 167.69 billion by 2030, at a CAGR of 5.83% during the forecast period (2025-2030).

The oilfield services industry is experiencing significant transformation driven by technological advancement and changing market dynamics. Companies are increasingly focusing on developing and implementing advanced technologies to optimize production processes and reduce operational costs. This shift is particularly evident in the adoption of digital solutions, automation, and artificial intelligence across various service segments. The industry has shown remarkable resilience in adapting to market challenges, with major players investing in research and development to enhance service efficiency and maintain competitive advantages. For instance, in December 2023, ADNOC announced plans to grow its conventional drilling activities by 40% by 2025, demonstrating the industry's commitment to expansion despite market uncertainties.

The exploration and production landscape continues to evolve with new discoveries and development projects shaping market dynamics. Recent exploration activities have yielded promising results, particularly in offshore sectors. In Norway alone, new discoveries made in 2023 have preliminary estimates of 77 million standard cubic meters of recoverable oil equivalents, spread across multiple regions including the North Sea and Norwegian Sea. This trend of successful exploration activities has encouraged increased investment in oilfield services, particularly in regions with proven reserves and established infrastructure.

The industry is witnessing a notable shift towards sustainable and efficient operations, with companies investing in environmentally conscious technologies and practices. This transformation is evident in the development of new drilling techniques, waste management solutions, and energy-efficient equipment. Service providers are increasingly focusing on offering integrated solutions that combine traditional services with environmental considerations, meeting both operational requirements and sustainability goals. The United Arab Emirates exemplifies this trend, with completed wells increasing to 440 in recent years, while simultaneously implementing advanced technologies for more sustainable operations.

The market is characterized by strategic collaborations and contract awards that are reshaping service delivery models. Major oilfield services companies are forming partnerships to enhance their service capabilities and market reach. A significant example is the recent contract awarded by Baker Hughes, Halliburton, and Schlumberger worth USD 455 million for drilling and well services, highlighting the industry's robust activity levels. These collaborations are not only driving innovation but also creating more efficient service delivery models that benefit both service providers and operators. The trend towards integrated service offerings is particularly prominent, with companies bundling various services to provide comprehensive solutions to operators.

Oilfield Services (OFS) Market Trends

Growing Global Oil and Gas Demand

The increasing global energy consumption continues to drive substantial growth in oil and gas demand, creating significant opportunities for oilfield service providers. According to OPEC statistics, the worldwide crude oil demand reached approximately 102.21 million barrels per day in 2023, showing a notable increase from 99.57 million barrels in 2022. This rising demand has put considerable pressure on oil and gas operating companies to increase their production capacity and efficiency, directly benefiting the oilfield services industry. The demand growth is particularly pronounced in developing economies, with India and China expected to contribute around 50% of the global oil demand by 2024.

The surge in global energy demand has led to increased exploration and production activities, requiring comprehensive oilfield services across the value chain. This is evidenced by recent industry developments, such as Transocean securing new extension contracts for its drilling rigs at enhanced day rates, with one rig deployed in India under contract with Reliance Industries Limited seeing an increase from USD 330,000 to USD 348,000 per day. Such contracts demonstrate the industry's willingness to invest in quality oilfield services to meet growing production demands.

Understand The Key Trends Shaping This Market

Download PDF

Shift Towards Unconventional Reserve Exploitation

As conventional oil and gas fields show signs of maturity, operating companies are increasingly shifting their focus toward exploiting unconventional reserves, driving demand for specialized oilfield drilling services. This transition requires advanced technologies and expertise in areas such as horizontal drilling, hydraulic fracturing, and enhanced oil recovery techniques. The development of shale plays and tight oil reserves has created a substantial market for specialized drilling and completion services, particularly in regions with significant unconventional resources.

The industry's commitment to unconventional resource development is reflected in continued investments in technology and infrastructure. Service providers are responding by expanding their capabilities in areas such as directional drilling, measurement while drilling (MWD), and logging while drilling (LWD) services. This trend is particularly evident in regions with substantial shale resources, where operators require sophisticated well construction and completion solutions to optimize production from these challenging formations.

Expansion of Offshore Drilling Activities

The offshore drilling sector is experiencing significant growth, driven by technological advancements and the need to access deep-water reserves. This expansion is exemplified by strategic industry moves such as Seadrill Limited's acquisition of Aquadrill LLC in April 2023, a USD 958 million all-stock transaction that created a high-specification fleet comprising 12 floaters, three harsh environment rigs, four benign jack-ups, and three tender-assisted rigs. Such consolidation activities demonstrate the industry's commitment to building robust offshore drilling capabilities to meet growing demand.

The momentum in offshore activities is further evidenced by expansion plans of major service providers. For instance, ADNOC Drilling's qualification to bid for rig supply contracts in Oman and its pursuit of approvals to participate in tenders in Saudi Arabia and Kuwait demonstrate the growing regional demand for offshore services. The company's strategic plan to have sufficient rig capacity for deployment outside the United Arab Emirates by the end of 2024 indicates strong industry confidence in the offshore sector's growth potential.

Investment in Mature Field Development

The need to maximize recovery from existing fields has led to increased investment in mature field development and enhanced oil recovery (EOR) techniques. Operating companies are focusing on improving production efficiency and extending the life of mature fields through advanced well intervention and workover services. This trend has created significant opportunities for oil service companies specializing in production optimization, well maintenance, and reservoir management services.

The industry's commitment to mature field development is demonstrated through the adoption of advanced technologies and integrated service approaches. Service providers are expanding their capabilities in areas such as artificial lift systems, well integrity services, and production monitoring solutions. This focus on mature field optimization requires a comprehensive range of services, from well intervention and workover operations to advanced reservoir characterization and monitoring solutions, driving sustained demand for oil and gas field services across the asset lifecycle.

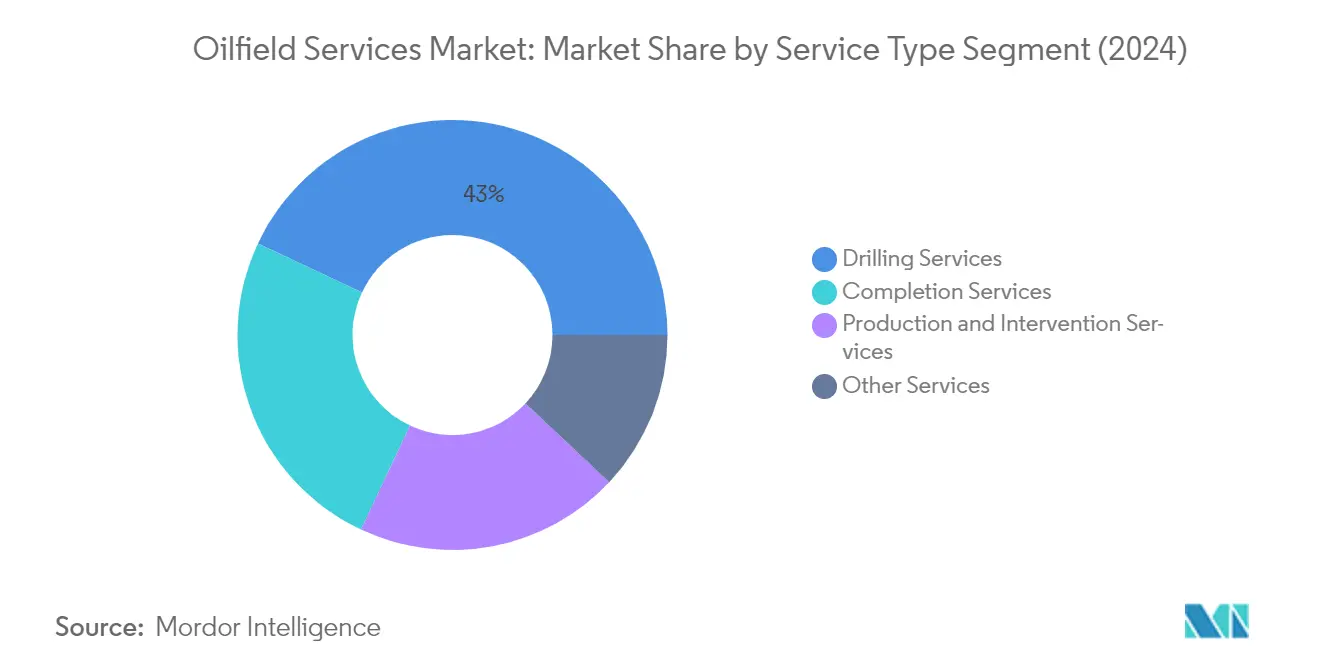

Segment Analysis: Service Type

Drilling Services Segment in Oilfield Services Market

The oilfield drilling services segment dominates the global oilfield services market, accounting for approximately 43% of the total market share in 2024. This segment encompasses both offshore contract drilling and other drilling services, with offshore contract drilling contributing significantly to the overall revenue. The segment's dominance is primarily driven by increasing deepwater and ultra-deepwater exploration activities, particularly in regions like Brazil, the Gulf of Mexico, and West Africa. The rising demand for advanced drilling technologies, including directional drilling and measurement while drilling (MWD) services, further strengthens this segment's market position. Additionally, the recovery of oil prices above $45 per barrel has led to increased drilling contracts and activities, particularly in mature fields requiring advanced drilling solutions.

Completion Services Segment in Oilfield Services Market

The completion services segment is projected to witness the fastest growth during the forecast period 2024-2029, driven by increasing unconventional resource development and the growing need for hydraulic fracturing services. This growth is particularly evident in regions with significant shale resources, such as North America and China. The segment's expansion is further supported by technological advancements in completion techniques, including multi-stage fracturing and smart completion systems. The rising focus on well optimization and enhanced recovery methods has led to increased demand for cementing services and other completion solutions. Additionally, operators are increasingly investing in advanced completion technologies to improve well productivity and reduce overall operational costs.

Remaining Segments in Service Type Segmentation

The production and intervention services segment, along with other services, plays a crucial role in the oilfield services industry. Production services encompass various critical activities, including logging services, well services, and production monitoring, which are essential for maintaining optimal well performance throughout its lifecycle. The intervention services focus on well workover and maintenance activities, becoming increasingly important as global oil fields mature. Other services, including seismic services and offshore support vessels, provide vital support to exploration and production activities. These segments are particularly significant in mature fields where production optimization and maintenance are key priorities for operators seeking to maximize recovery rates and extend field life.

Segment Analysis: Location of Deployment

Onshore Segment in Oilfield Services Market

The onshore segment continues to dominate the global oilfield services market, commanding approximately 60% of the total market share in 2024. This dominance is primarily attributed to the lower operational costs and easier accessibility compared to offshore operations. The segment's strength is further reinforced by increasing investments in conventional onshore and shale oil and gas segments, particularly from National Oil Companies (NOCs). The onshore segment benefits from the development of mature fields and the growing focus on unconventional resources, especially in regions like North America and the Middle East. The segment's market position is supported by technological advancements in drilling and completion technologies, which have made onshore operations more efficient and cost-effective. Additionally, the presence of extensive shale resources and the continuous development of new onshore fields in key markets contribute to the segment's market leadership.

Offshore Segment in Oilfield Services Market

The offshore segment is emerging as the fastest-growing segment in the oil and gas field services market for the period 2024-2029. This growth is driven by increasing deep-water and ultra-deepwater exploration activities, particularly in regions like Brazil, the Gulf of Mexico, and West Africa. The segment is experiencing rapid expansion due to technological advancements in offshore drilling capabilities and the discovery of significant reserves in deep-water locations. The development of new offshore fields, particularly in regions like the Middle East and Asia-Pacific, is contributing to this growth momentum. Enhanced recovery techniques and improved offshore drilling technologies are making previously uneconomical offshore projects viable. The segment is also benefiting from increased investments in offshore infrastructure and the development of new offshore exploration blocks by major oil and gas companies.

Oilfield Services (OFS) Market Geography Segment Analysis

Oilfield Services Market in North America

North America continues to dominate the global oilfield services market, commanding approximately 42% of the total market share in 2024. The region's prominence is primarily driven by its extensive shale operations and technological advancements in drilling and completion services. The United States leads the regional market with its prolific shale formations, particularly in the Permian Basin, Eagle Ford, and Bakken regions. The market benefits from well-established infrastructure, the presence of major oilfield companies, and continuous technological innovations in hydraulic fracturing and horizontal drilling techniques. Advanced digital technologies and automation solutions are increasingly being adopted across the region's oilfield operations, improving operational efficiency and cost-effectiveness. The region's market is characterized by a strong focus on operational efficiency, environmental compliance, and the integration of sustainable practices in oilfield operations. The presence of major oilfield service market companies and their manufacturing facilities in the region contributes to competitive pricing and readily available technical expertise.

Oilfield Services Market in Europe

The European oilfield services market has demonstrated resilience with a modest growth rate of approximately 2% during the period 2019-2024. The market is primarily driven by activities in the North Sea region, with Norway and the United Kingdom being the key contributors. The region's market is characterized by a strong focus on technological innovation, particularly in offshore drilling technologies and subsea operations. European operators are increasingly emphasizing environmental sustainability and carbon footprint reduction in their operations, leading to the adoption of cleaner technologies and more efficient processes. The market benefits from well-established regulatory frameworks and strong government support for energy security initiatives. Mature field optimization and enhanced oil recovery techniques play a crucial role in sustaining production levels across the region's aging fields. The region's commitment to energy transition is shaping the evolution of oilfield services, with increasing integration of renewable energy solutions in offshore operations.

Oilfield Services Market in Asia-Pacific

The Asia-Pacific oilfield services market is projected to grow at a compound annual growth rate of approximately 4% during the period 2024-2029. The region represents a dynamic market characterized by diverse operational environments ranging from mature onshore fields to deepwater developments. China leads the regional market with its ambitious domestic production targets and technological advancements in oilfield services. The market is witnessing increased investment in exploration and production activities, particularly in offshore areas. Digital transformation and the adoption of advanced technologies are reshaping operational practices across the region. Local service providers are expanding their capabilities and market presence, creating a more competitive landscape. The region's growing energy demand and focus on energy security continue to drive investment in oil and gas exploration and production activities. Environmental considerations and regulatory compliance are becoming increasingly important factors in service delivery and technology adoption.

Oilfield Services Market in South America

The South American oilfield services market is experiencing significant transformation driven by developments in Brazil's pre-salt fields and Argentina's Vaca Muerta shale formation. The region's market is characterized by a mix of mature field optimization and new field developments, particularly in offshore areas. Brazil leads the regional market with its extensive deepwater and ultra-deepwater operations, while Argentina focuses on developing its unconventional resources. The market is witnessing increased adoption of advanced technologies to improve operational efficiency and reduce costs. Local content requirements and regulatory frameworks significantly influence market dynamics and service delivery models. The region's service providers are increasingly focusing on integrated service offerings and technological solutions to address complex operational challenges. Environmental considerations and sustainable practices are becoming increasingly important in service delivery and project execution.

Oilfield Services Market in Middle East & Africa

The Middle East & Africa oilfield services market maintains its strategic importance in the global oil and gas industry, driven by the region's vast hydrocarbon reserves and ongoing field development activities. Saudi Arabia, UAE, and Kuwait lead the market with their ambitious production targets and field development programs. The region is witnessing an increased focus on technology adoption and operational efficiency improvements across its oilfield services sector. Local content requirements and nationalization programs are reshaping the competitive landscape and service delivery models. The market is characterized by a mix of conventional field optimization and new field developments, particularly in offshore areas. Digital transformation initiatives are gaining momentum across the region's oilfield operations. The region's service providers are increasingly focusing on developing local capabilities and technological expertise to meet evolving market demands.

Get Analysis on Important Geographic Markets

Download PDF

Oilfield Services (OFS) Industry Overview

Top Companies in Oilfield Services Market

The oilfield service companies market is characterized by continuous technological advancement and strategic partnerships among major players. Companies are increasingly focusing on developing innovative solutions like automated well control technology, digital platforms for reservoir management, and advanced drilling technologies to optimize operations and reduce costs. There has been a notable trend towards the integration of artificial intelligence and machine learning capabilities across service offerings, particularly in areas like well testing and drilling operations. Strategic collaborations and joint ventures have become commonplace, especially in developing regions, as companies seek to expand their geographical footprint and service capabilities. The industry has witnessed significant investment in research and development, particularly in areas like electric fracking, advanced drill bits, and digitalization of oilfield operations, demonstrating the sector's commitment to technological evolution and operational efficiency.

Fragmented Market with Strong Regional Players

The oil field service industry exhibits a moderately fragmented structure with a mix of global conglomerates and regional specialists. Major international players like Schlumberger, Halliburton, and Baker Hughes dominate the market through their comprehensive service portfolios and global presence, while regional players maintain strong positions in specific geographic markets or specialized service segments. The market has witnessed significant consolidation through mergers and acquisitions, particularly among larger players seeking to expand their technological capabilities and geographic reach. The formation of strategic alliances and joint ventures has become increasingly common, especially in emerging markets where local expertise and relationships are crucial for market entry and expansion.

The industry landscape is characterized by varying levels of integration, with some companies focusing on specialized services while others offer end-to-end solutions. Market consolidation has been driven by the need to achieve economies of scale, enhance technological capabilities, and strengthen market position in key regions. The trend towards partnerships between international and local players has become more pronounced, particularly in regions with strong national oil companies and local content requirements. This has led to a dynamic market structure where success depends on both global reach and local market understanding.

Innovation and Adaptability Drive Market Success

Success in the global oilfield services market increasingly depends on companies' ability to innovate and adapt to changing market conditions. Incumbent players are focusing on developing integrated service offerings, investing in digital technologies, and optimizing their operational efficiency to maintain their market position. The ability to provide cost-effective solutions while maintaining service quality has become crucial, particularly in price-sensitive markets. Companies are also emphasizing the development of environmentally sustainable technologies and practices, recognizing the growing importance of environmental considerations in client decision-making. Building strong relationships with national oil companies and maintaining a robust local presence in key markets has become essential for long-term success.

For new entrants and smaller players, success lies in identifying and focusing on niche market segments or specific geographic regions where they can build competitive advantages. The development of specialized technological solutions and the ability to offer flexible, customized services are key differentiators. Companies must also navigate complex regulatory environments and maintain strong safety standards while managing costs effectively. The increasing focus on digitalization and automation presents opportunities for technology-focused oil service companies to gain market share, while partnerships with established players can provide access to broader market opportunities and resources. The ability to adapt to cyclical market conditions and maintain financial stability during downturns remains crucial for long-term success in the industry.

Oilfield Services (OFS) Market Leaders

-

Weatherford International Plc

-

Schlumberger Limited

-

Halliburton Company

-

Baker Hughes Company

-

China Oilfield Services Limited

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Oilfield Services (OFS) Market News

- September 2023: SLB signed a subsurface technology agreement with INEOS Energy, the energy division of INEOS, a global chemical and manufacturing company. INEOS Energy will partner with SLB’s Performance Centre in Aberdeen to collaborate and innovate subsurface technologies, including AI capabilities, to help it drive operational performance for continued growth, new acquisitions, and carbon capture and storage (CCS).

- April 2023: QatarEnergy, formerly Qatar Petroleum, a state-owned petroleum company of Qatar, agreed with Shell PLC to acquire a 40% working interest in the C-10 block located offshore Mauritania. Shell PLC and QatarEnergy have decided to explore the C-10 block, which is approximately 50 kilometers off the coast of Mauritania, Africa.

Oilfield Services (OFS) Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2029

- 4.3 Crude Oil and Natural Gas Production and Forecast, till 2029

- 4.4 Onshore and Offshore Active Rig Count, till 2023

- 4.5 Recent Trends and Developments

- 4.6 Government Policies and Regulations

-

4.7 Market Dynamics

- 4.7.1 Drivers

- 4.7.1.1 Increasing Development of Gas Reserves and Advanced Technology, Tools, and Equipment

- 4.7.1.2 Increasing Investment in the Oilfield Services across World

- 4.7.2 Restraints

- 4.7.2.1 The Volatile Oil Prices Over the Recent Period, Owing to the Supply-Demand Gap

- 4.8 Supply Chain Analysis

-

4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Consumers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes Products and Services

- 4.9.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Service Type

- 5.1.1 Drilling Services

- 5.1.2 Completion Services

- 5.1.3 Production and Intervention Services

- 5.1.4 Other Services

-

5.2 Location of Deployment

- 5.2.1 Onshore

- 5.2.2 Offshore

-

5.3 Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)})

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 France

- 5.3.2.3 United Kingdom

- 5.3.2.4 Italy

- 5.3.2.5 Russia

- 5.3.2.6 Spain

- 5.3.2.7 NORDIC

- 5.3.2.8 Turkey

- 5.3.2.9 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Malaysia

- 5.3.3.6 Thailand

- 5.3.3.7 Vietnam

- 5.3.3.8 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Nigeria

- 5.3.5.5 Qatar

- 5.3.5.6 Egypt

- 5.3.5.7 Rest of the Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Schlumberger Limited

- 6.3.2 Weatherford International PLC

- 6.3.3 Baker Hughes Company

- 6.3.4 Halliburton Company

- 6.3.5 Transocean Ltd

- 6.3.6 Valaris PLC

- 6.3.7 China Oilfield Services Limited

- 6.3.8 Nabors Industries Inc.

- 6.3.9 Basic Energy Services Inc.

- 6.3.10 OiLSERV

- 6.3.11 Expro Group

- *List Not Exhaustive

- 6.4 Market Ranking/Share (%) Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Focus on New Technologies and Methods to Optimize its Production Cost of Hydrocarbons

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Oilfield Services (OFS) Industry Segmentation

Oilfield services (OFS) refer to all the services that support onshore and offshore oil and gas extraction and production processes. These include drilling and formation evaluation, well construction, and completion services.

The oilfield services market is segmented by service type, location of deployment, and geography. The market is segmented by service type into drilling, completion, production, and other services. By location of deployment, the market is segmented into onshore and offshore. The report also covers the market size and forecasts for the oilfield services market across major regions. Market sizes and forecasts for each segment are based on revenue (USD).

| Service Type | Drilling Services | ||

| Completion Services | |||

| Production and Intervention Services | |||

| Other Services | |||

| Location of Deployment | Onshore | ||

| Offshore | |||

| Geography (Regional Market Analysis {Market Size and Demand Forecast till 2028 (for regions only)}) | North America | United States | |

| Canada | |||

| Rest of North America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Russia | |||

| Spain | |||

| NORDIC | |||

| Turkey | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Thailand | |||

| Vietnam | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle East and Africa | Saudi Arabia | ||

| United Arab Emirates | |||

| South Africa | |||

| Nigeria | |||

| Qatar | |||

| Egypt | |||

| Rest of the Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Oilfield Services (OFS) Market Research FAQs

How big is the Oilfield Services Market?

The Oilfield Services Market size is expected to reach USD 126.32 billion in 2025 and grow at a CAGR of 5.83% to reach USD 167.69 billion by 2030.

What is the current Oilfield Services Market size?

In 2025, the Oilfield Services Market size is expected to reach USD 126.32 billion.

Who are the key players in Oilfield Services Market?

Weatherford International Plc, Schlumberger Limited, Halliburton Company, Baker Hughes Company and China Oilfield Services Limited are the major companies operating in the Oilfield Services Market.

Which is the fastest growing region in Oilfield Services Market?

Europe is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Oilfield Services Market?

In 2025, the North America accounts for the largest market share in Oilfield Services Market.

What years does this Oilfield Services Market cover, and what was the market size in 2024?

In 2024, the Oilfield Services Market size was estimated at USD 118.96 billion. The report covers the Oilfield Services Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Oilfield Services Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Oilfield Services (OFS) Market Research

Mordor Intelligence offers a comprehensive analysis of the global oilfield services industry. We leverage our extensive expertise in the oil and gas services industry to provide a detailed report. This report covers the entire spectrum of oilfield services activities, including drilling services, onshore oilfield services, and upstream services. As a leading authority in industrial oilfield services analysis, we offer in-depth insights into oilfield service providers and their operational dynamics. We pay particular attention to oil field services companies and their strategic positioning in the evolving market landscape.

The report provides stakeholders with crucial insights into oilfield services business opportunities and industry trends. It is available in an easy-to-read report PDF format for download. Our analysis includes oilfield services competition data, market size projections, and detailed industry overview segments. This research is particularly beneficial for oil and gas field services companies seeking to understand market dynamics. It also provides valuable insights for oilfield service provider organizations looking to optimize their market strategies. The report includes comprehensive oilfield services market analysis and market outlook forecasts. These are supported by robust oilfield services industry survey data and expert analysis of oil field services industry developments.