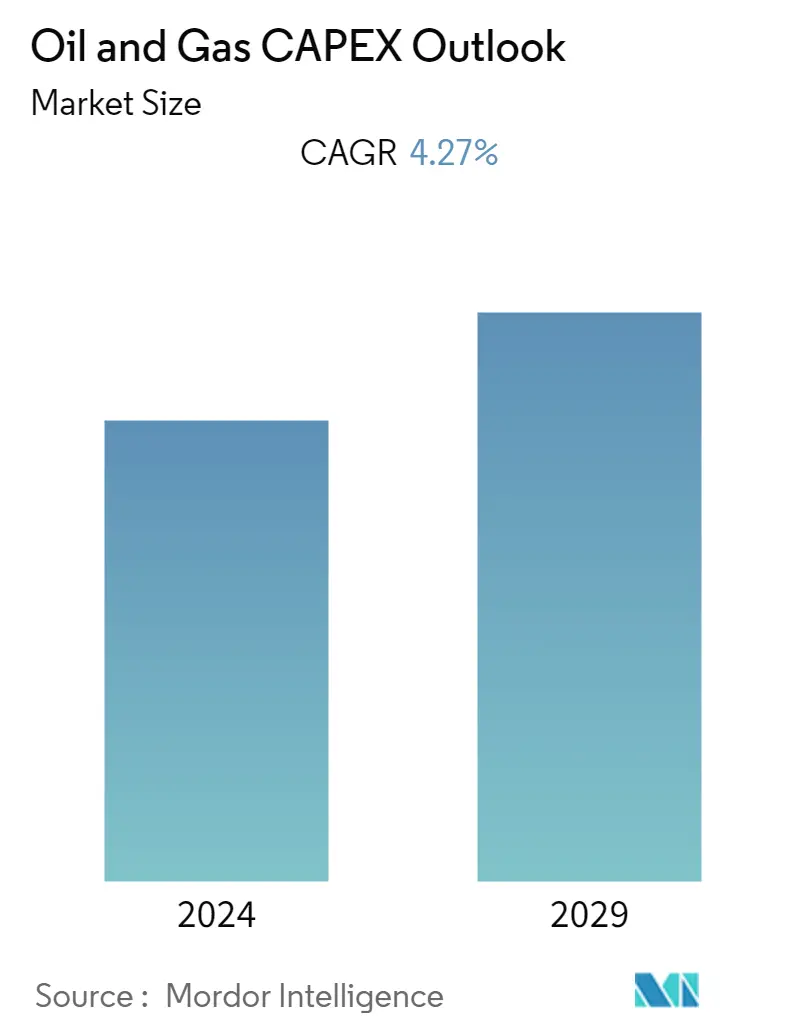

Market Size of Oil and Gas CAPEX Outlook

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 4.27 % |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

CAPEX Oil and Gas Market Analysis

The Oil and Gas CAPEX is expected to grow from USD 797.58 billion in 2023 to USD 983.04 billion by 2028, at a CAGR of 4.27% during the forecast period (2023-2028).

The market was impacted by COVID-19 in 2020. Presently the market has now reached pre-pandemic levels.

- Over the medium term, the rising investments in offshore oil & gas activities owing to the surging energy demand, depleting onshore reserves, and efforts from governments across nations to explore their offshore resources are expected to drive the growth of the oil & gas capex market in the coming years.

- On the other hand, volatile crude oil and natural gas prices, coupled with slow economic growth at a global level, are expected to restrain the oil and gas CAPEX during the forecast period.

- Nevertheless, several offshore, deep, and ultra-deepwater explorations in the North Sea, Gulf of Mexico, and developing countries such as Senegal and Mauritiana, provide ample opportunity for increased capital expenditure.

- North America has recorded the highest gains in CAPEX, owing to operations of globally integrated majors, along with national oil companies and new investments during the forecast period.

CAPEX Oil and Gas Industry Segmentation

Capital expenditure (CAPEX) is the funds used by a company/organization to acquire, upgrade, and maintain physical assets, such as property, plants, buildings, technology, or equipment. CAPEX is often used to undertake new projects or investments by a company. The global oil and gas CAPEX market consider the total capital expenditure of oil and gas operators worldwide annually. The CAPEX/investments in the upstream, midstream, and downstream oil and gas projects across different regions are taken into consideration while estimating the market size.

The oil & gas CAPEX market is segmented by sector, location and geography. By sector, the market is segmented into upstream, midstream, and downstream. By location, the market is segmented into onshore and offshore. The report also covers the market size and forecasts for the oil & gas CAPEX market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Sector | |

| Upstream | |

| Midstream | |

| Downstream |

| Location | |

| Onshore | |

| Offshore |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Oil and Gas CAPEX Outlook Size Summary

The oil and gas CAPEX market is poised for substantial growth over the forecast period, driven by increasing investments in offshore activities due to rising energy demand and depleting onshore reserves. Governments worldwide are actively exploring offshore resources, which is expected to bolster market expansion. However, the market faces challenges from volatile crude oil and natural gas prices and slow global economic growth. Despite these challenges, opportunities abound in offshore, deep, and ultra-deepwater explorations in regions like the North Sea and Gulf of Mexico, as well as in developing countries such as Senegal and Mauritania. North America, particularly the United States, is a significant contributor to CAPEX growth, supported by operations of integrated majors and national oil companies.

The upstream sector is anticipated to dominate CAPEX investments, with state-owned companies focusing on domestic projects to enhance energy security. The market's recovery post-COVID-19 lockdowns has been fueled by increased demand and rising crude oil prices, leading to a surge in investments. Major oil and gas companies have announced significant increases in capital expenditures, with a focus on high-margin growth opportunities. The United States leads in global oil and gas production, with substantial CAPEX plans for petrochemical plants and new upstream projects. Similarly, Canada is witnessing significant investments from major operators. The market is moderately fragmented, with key players like BP, Exxon Mobil, TotalEnergies, Chevron, and Shell actively participating in CAPEX activities.

Oil and Gas CAPEX Outlook Market Size - Table of Contents

-

1. MARKET OVERVIEW

-

1.1 Introduction

-

1.2 Market Size and Demand Forecast in USD, till 2028

-

1.3 Crude Oil Production and Consumption Forecast, till 2028

-

1.4 Natural Gas Production and Consumption Forecast, till 2028

-

1.5 Installed Pipeline Historic Capacity and Forecast in Kilometers, till 2028

-

1.6 Historic and Production Forecast of Tight Oil, Oil Sands, and Crude from Deepwater in kb/d, until 2030

-

1.7 Recent Trends and Developments

-

1.8 Government Policies and Regulations

-

1.9 Market Dynamics

-

1.9.1 Drivers

-

1.9.1.1 Increasing Demand for Natural Gas and Developing Gas Infrastructure

-

1.9.1.2 Increasing Offshore Oil & Gas Exploration Activities

-

-

1.9.2 Restraints

-

1.9.2.1 Adoption of Cleaner Alternatives

-

1.9.2.2 High Volatility of Crude Oil Prices

-

-

-

1.10 Supply Chain Analysis

-

1.11 Porter's Five Forces Analysis

-

1.11.1 Bargaining Power of Suppliers

-

1.11.2 Bargaining Power of Consumers

-

1.11.3 Threat of New Entrants

-

1.11.4 Threat of Substitutes Products and Services

-

1.11.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION

-

2.1 Sector

-

2.1.1 Upstream

-

2.1.2 Midstream

-

2.1.3 Downstream

-

-

2.2 Location

-

2.2.1 Onshore

-

2.2.2 Offshore

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

2.3.1.3 Mexico

-

-

2.3.2 Europe

-

2.3.2.1 Germany

-

2.3.2.2 United Kingdom

-

2.3.2.3 Russia

-

2.3.2.4 Norway

-

2.3.2.5 Netherlands

-

2.3.2.6 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 India

-

2.3.3.3 Malaysia

-

2.3.3.4 Indonesia

-

2.3.3.5 ASEAN Countries

-

2.3.3.6 Rest of Asia-Pacific

-

-

2.3.4 South America

-

2.3.4.1 Brazil

-

2.3.4.2 Venezuela

-

2.3.4.3 Argentina

-

2.3.4.4 Colombia

-

2.3.4.5 Rest of South America

-

-

2.3.5 Middle-East and Africa

-

2.3.5.1 Saudi Arabia

-

2.3.5.2 United Arab Emirates (UAE)

-

2.3.5.3 Egypt

-

2.3.5.4 Nigeria

-

2.3.5.5 Rest of Middle East and Africa

-

-

-

Oil and Gas CAPEX Outlook Market Size FAQs

What is the current Oil and Gas CAPEX Market size?

The Oil and Gas CAPEX Market is projected to register a CAGR of 4.27% during the forecast period (2024-2029)

Who are the key players in Oil and Gas CAPEX Market?

Exxon Mobil Corporation, BP PLC, Chevron Corporation, Shell Plc and TotalEnergies SE are the major companies operating in the Oil and Gas CAPEX Market.