| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 4.27 % |

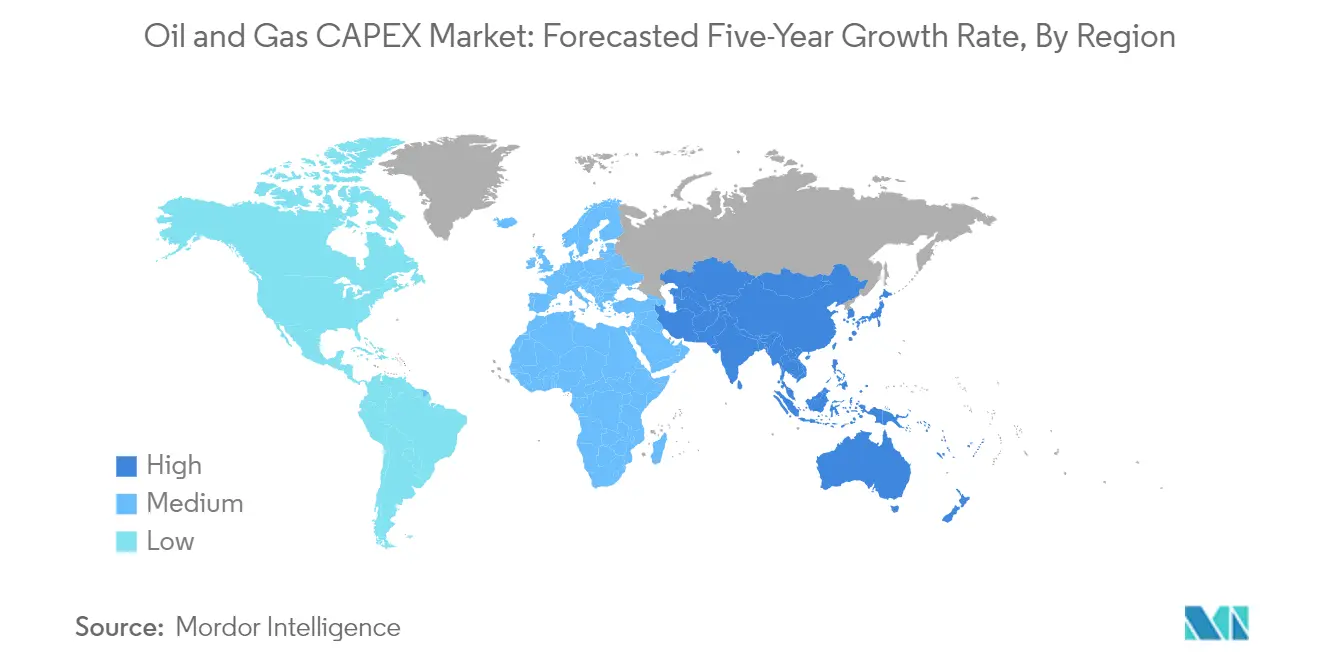

| Fastest Growing Market | Middle East and Africa |

| Largest Market | North America |

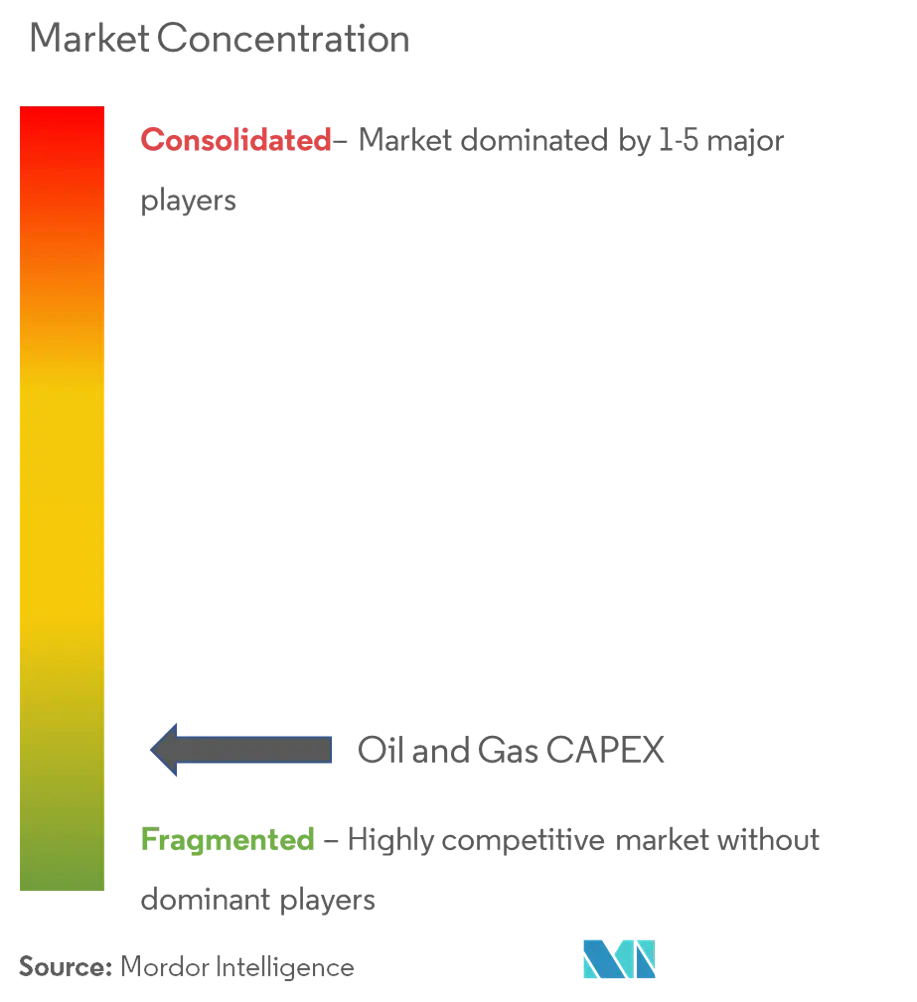

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

CAPEX Oil and Gas Market Analysis

The Oil and Gas CAPEX Market is expected to register a CAGR of 4.27% during the forecast period.

The oil and gas industry is witnessing a significant transformation driven by evolving energy security concerns and strategic infrastructure investments. Major oil-producing nations are reinforcing their market positions, with Saudi Arabia maintaining its dominance by holding 15% of the world's proved oil reserves and 21% of OPEC's proved reserves as of 2022. This concentration of resources has led to increased investments in exploration and production capabilities, particularly in offshore and deep-water projects. The industry is also experiencing a wave of strategic partnerships and joint ventures, as companies seek to share risks and leverage complementary capabilities in complex project developments.

The global LNG infrastructure is undergoing substantial expansion to meet growing international demand for natural gas. According to the International Gas Union (IGU), the global LNG trade demonstrated robust growth of 6.8% in 2022, reaching 401.5 million tonnes, with 20 exporting markets connecting to 48 importing markets. This expansion is reflected in the significant investment in liquefaction capacity, with approximately 178.3 MTPA under construction or approved for development globally as of April 2023. Companies are increasingly focusing on developing integrated LNG value chains, from production to transportation and regasification facilities.

The upstream sector is experiencing a notable shift in investment patterns, particularly in North America. According to the U.S. Energy Information Administration (EIA), in mid-2023, financial reports from 40 publicly traded US oil exploration and production companies revealed that these entities accounted for 32% of all crude oil produced in the United States, demonstrating the significant role of independent producers. The industry is witnessing increased capital allocation toward technological advancement, with particular emphasis on digital transformation and automation to enhance operational efficiency and reduce environmental impact.

The industry is undergoing substantial transformation in terms of project execution and risk management approaches. Major oil and gas companies are increasingly adopting modular construction techniques and standardized project designs to reduce costs and accelerate project delivery timelines. This shift is accompanied by a growing focus on environmental, social, and governance (ESG) considerations in project planning and execution, with companies incorporating carbon capture and storage capabilities into new developments. The trend toward more flexible and adaptable project execution strategies is enabling companies to better manage market volatility and regulatory changes while maintaining competitive positions in the global market.

The oil and gas industry operations and markets are increasingly influenced by oil and gas capital expenditure trends, with a notable emphasis on CAPEX allocation to enhance infrastructure and operational efficiency. This strategic focus is evident in the CAPEX forecast, which underscores the industry's commitment to sustainable growth and innovation.

CAPEX Oil and Gas Market Trends

Growing Demand for Natural Gas and Developing Gas Infrastructure

The global natural gas sector has witnessed substantial growth in production and consumption as countries increasingly shift from coal to natural gas as their primary energy source to meet carbon emission targets. According to industry statistics, total global natural gas production reached approximately 4,043.8 billion cubic meters (bcm) in 2022, marking a 4.75% increase from 2020 levels. The United States and Russia emerged as the world's largest natural gas producers, collectively accounting for nearly 40% of global natural gas production in 2022. This growing emphasis on natural gas has driven significant investments in exploration, production, and infrastructure development, with several countries implementing measures to support the adoption of natural gas and improve the development of gas reserves.

The expanding natural gas infrastructure landscape is evidenced by major investment announcements throughout 2023. In December 2023, Pembina Pipeline Corporation declared a capital expenditure of approximately USD 880 million for developing pipeline infrastructure, including the completion of Northeast British Columbia (NEBC) spanning 145 km and the Cochin Pipeline System extending over 3,000 km in Canada. Similarly, in August 2023, the Gas Authority of India Limited (GAIL) announced plans to invest about USD 3.6 billion in pipeline projects over the next three years. The liquefied natural gas (LNG) sector has also witnessed remarkable growth, with approximately 178.3 million tonnes per annum (MTPA) of liquefaction capacity under construction or approved for development globally as of April 2023. Additionally, about 997.1 MTPA of aspirational liquefaction capacity is in the pre-FID stage, with the majority concentrated in the United States, Canada, Russia, and Australia. According to the International Energy Agency (IEA), the average annual investment in gas transmission and distribution pipeline infrastructure in advanced economies is projected to be around USD 31 billion between 2031-2040, highlighting the long-term commitment to developing natural gas infrastructure.

The sector's oil and gas capital expenditure spending reflects a strategic focus on enhancing infrastructure to meet rising demand. Companies are increasingly engaging in oil and gas capital forecasting management to optimize their investments. Notably, TC Energy's 30% increase in capital expenditure for natural gas pipelines in North America in 2023 underscores the industry's commitment to expanding capacity. Such initiatives are pivotal in addressing the anticipated growth in natural gas consumption, further supported by a robust oil and gas capital expenditure strategy.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: Sector

Upstream Segment in Oil and Gas CAPEX Market

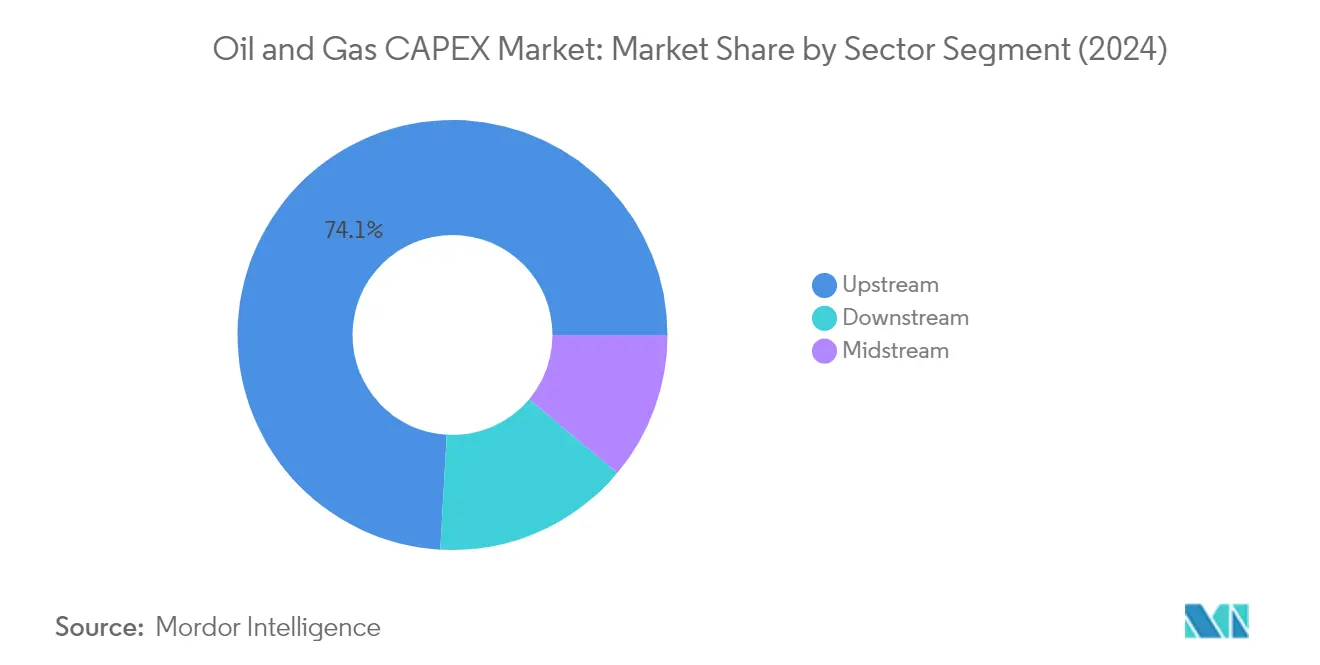

The upstream segment dominates the global oil and gas capital expenditure market, accounting for approximately 74% of the total market share in 2024. This substantial market share is driven by extensive investments in both onshore and offshore exploration and production activities. Major oil and gas companies are focusing on developing new fields and enhancing production from existing assets, particularly in regions like the United States, Saudi Arabia, and the United Arab Emirates. The segment's dominance is further reinforced by significant discoveries in deep and ultra-deep water areas, which require substantial CAPEX investments for development. Additionally, technological advancements in drilling and production techniques have encouraged companies to invest more in upstream activities to improve operational efficiency and maximize resource recovery.

Midstream Segment in Oil and Gas CAPEX Market

The midstream segment, comprising pipelines and storage & terminals infrastructure, is expected to witness steady growth during the forecast period 2024-2029. The growth is primarily driven by increasing investments in natural gas infrastructure, particularly LNG terminals and transportation networks. The expansion of cross-border pipeline projects, especially in regions like North America and the Middle East, is contributing to the segment's growth. Furthermore, the development of new LNG export facilities and the modernization of existing pipeline networks to enhance transportation efficiency and safety are creating significant opportunities in this segment. The increasing focus on energy security and the need for reliable transportation infrastructure is expected to sustain investment momentum in the midstream sector, reflecting the ongoing CAPEX trends.

Remaining Segments in Sector

The downstream segment, encompassing refineries and petrochemical plants, plays a crucial role in the oil and gas CAPEX market. This segment is witnessing significant developments through modernization projects and capacity expansions, particularly in Asia-Pacific and the Middle East. Refineries are investing in upgrading their facilities to meet stricter environmental regulations and improve operational efficiency, while petrochemical plants are expanding their capacities to meet growing demand for petrochemical products. The integration of digital technologies and automation in downstream operations is also driving CAPEX investments in this sector, as companies seek to optimize their processes and enhance productivity.

Oil and Gas CAPEX Outlook Geography Segment Analysis

Oil and Gas CAPEX Market in North America

North America represents a dominant force in the global oil and gas capital expenditure landscape, with significant investments across upstream, midstream, and downstream sectors. The region's market is primarily driven by the United States and Canada, with both countries focusing heavily on shale gas development, offshore exploration, and infrastructure modernization. The presence of major oil and gas companies, advanced technological capabilities, and supportive regulatory frameworks has enabled sustained investment growth across the region's hydrocarbon sector.

Oil and Gas CAPEX Market in United States

The United States maintains its position as North America's largest oil and gas capital expenditure market, holding approximately 77% market share in 2024. The country's dominance is supported by extensive shale operations in the Permian Basin, offshore developments in the Gulf of Mexico, and significant LNG export terminal expansions. Major companies like Chevron and ExxonMobil continue to drive substantial investments in both conventional and unconventional resources. The US market benefits from advanced drilling technologies, robust infrastructure, and a well-established regulatory framework that supports ongoing capital investments across the value chain.

Oil and Gas CAPEX Market in United States - Growth Analysis

The United States is also positioned as the fastest-growing market in North America, with a projected growth rate of approximately 4% from 2024-2029. This growth is primarily driven by increasing investments in LNG export facilities, expansion of pipeline infrastructure, and continued development of unconventional resources. The country's focus on energy independence, technological advancements in drilling and extraction methods, and the presence of abundant shale resources continue to attract significant capital expenditure investments from both domestic and international players.

Oil and Gas CAPEX Market in Europe

Europe's oil and gas capital expenditure market demonstrates a diverse investment landscape shaped by varying national energy policies and resource availability. The region's market is primarily influenced by activities in Russia, Norway, and the United Kingdom, with each country pursuing distinct investment strategies. The European market has shown resilience despite geopolitical challenges, with continued investments in offshore developments, infrastructure modernization, and natural gas projects.

Oil and Gas CAPEX Market in Russia

Russia emerges as Europe's largest oil and gas capital expenditure market, commanding approximately 62% of the region's market share in 2024. The country's dominant position is supported by its vast hydrocarbon reserves, extensive pipeline network, and ongoing development of new oil and gas fields. Despite international challenges, Russia continues to maintain significant investments in upstream activities, particularly in Arctic development projects and LNG facilities.

Oil and Gas CAPEX Market in United Kingdom

The United Kingdom positions itself as Europe's fastest-growing market with a projected growth rate of approximately 3% from 2024-2029. The country's growth is driven by renewed focus on North Sea developments, enhanced oil recovery projects, and investments in infrastructure modernization. The UK's commitment to maintaining domestic energy security while transitioning to cleaner energy sources has created a balanced investment environment that supports sustained capital expenditure in the oil and gas sector.

Oil and Gas CAPEX Market in Asia-Pacific

The Asia-Pacific region represents a dynamic market for oil and gas capital expenditure, characterized by diverse investment opportunities across mature and emerging markets. Countries like China, India, and Australia lead the region's investment landscape, with significant focus on expanding domestic production capabilities, developing LNG infrastructure, and modernizing existing facilities. The region's growing energy demand and push for energy security continue to drive substantial investments across the entire oil and gas value chain.

Oil and Gas CAPEX Market in China

China stands as the dominant force in Asia-Pacific's oil and gas capital expenditure market. The country's market leadership is driven by aggressive expansion of domestic exploration and production activities, development of unconventional resources, and significant investments in LNG infrastructure. State-owned companies like CNPC and CNOOC continue to spearhead major investment initiatives across upstream, midstream, and downstream sectors, focusing on both onshore and offshore developments.

Oil and Gas CAPEX Market in China - Growth Analysis

China also leads the region's growth trajectory, demonstrating strong investment momentum in its oil and gas sector. The country's expansion is supported by ambitious exploration programs, development of new gas fields, and continued investments in infrastructure modernization. China's commitment to enhancing energy security and reducing dependency on imports continues to drive substantial capital expenditure investments across the sector.

Oil and Gas CAPEX Market in South America

South America's oil and gas capital expenditure market is characterized by significant investments in offshore developments, unconventional resources, and infrastructure modernization. The region's investment landscape is primarily shaped by activities in Brazil and Argentina, with Brazil emerging as both the largest and fastest-growing market. Brazil's pre-salt developments and Argentina's Vaca Muerta shale formation continue to attract substantial investments, while both countries focus on expanding their production capabilities and modernizing infrastructure.

Oil and Gas CAPEX Market in Middle East & Africa

The Middle East & Africa region maintains its position as a crucial market for oil and gas capital expenditure, with investments spanning across upstream, midstream, and downstream sectors. The region's market is led by Saudi Arabia, UAE, and Egypt, with Saudi Arabia emerging as both the largest and fastest-growing market. The region's investment landscape is characterized by major capacity expansion projects, development of gas resources, and modernization of existing facilities, supported by national oil companies and international partners.

Get Analysis on Important Geographic Markets

Download PDF

CAPEX Oil and Gas Industry Overview

Top Companies in Oil and Gas CAPEX Market

The global oil and gas CAPEX market features prominent players like BP PLC, Shell PLC, Chevron Corporation, TotalEnergies SE, and ExxonMobil Corporation leading the industry through strategic initiatives. These companies are increasingly focusing on technological innovation, particularly in the digitalization and automation of operations, to optimize costs and improve operational efficiency. The industry is witnessing a significant shift towards sustainable practices, with major players investing in lower emission projects and clean energy technologies. Companies are expanding their geographical presence through strategic acquisitions and joint ventures, particularly in emerging markets and untapped regions. The market leaders are also emphasizing offshore exploration activities and developing integrated projects that span across upstream, midstream, and downstream segments, while simultaneously modernizing existing infrastructure to enhance productivity and reduce operational costs.

Dynamic Market Structure Drives Industry Evolution

The CAPEX oil and gas market exhibits a complex competitive structure characterized by the presence of both global integrated energy corporations and specialized regional players. The market demonstrates moderate consolidation, with major international oil companies holding significant market share while competing with national oil companies that dominate their respective regional markets. The industry has witnessed increased merger and acquisition activities, particularly focused on acquiring technological capabilities and expanding geographical footprints, with notable transactions like Chevron's acquisition of Hess Corporation and ExxonMobil's agreement to acquire Pioneer Natural Resources.

The competitive landscape is further shaped by strategic partnerships and joint ventures, especially in capital-intensive offshore projects and emerging market operations. Companies are increasingly collaborating to share risks and leverage complementary capabilities, particularly in technologically challenging deep-water projects and large-scale LNG developments. The market also sees active participation from service providers and equipment suppliers who play crucial roles in project execution and technological advancement, creating a complex web of interdependencies among various stakeholders in the value chain.

Innovation and Adaptability Drive Future Success

Success in the oil and gas industry operations and markets increasingly depends on companies' ability to balance traditional operational excellence with technological innovation and environmental responsibility. Market leaders are strengthening their positions through investments in digital technologies, including artificial intelligence, automation, and data analytics, while simultaneously developing capabilities in renewable energy and low-carbon solutions. Companies are also focusing on portfolio optimization, prioritizing high-return assets and divesting non-core operations to maintain competitive advantages in their chosen markets.

The industry's future competitive dynamics will be significantly influenced by regulatory frameworks, particularly regarding environmental standards and emissions controls. Companies must navigate these challenges while maintaining operational efficiency and meeting growing energy demand. Success factors for new entrants and smaller players include developing specialized capabilities in niche markets, forming strategic alliances with established players, and leveraging technological innovations to compete effectively. The ability to adapt to changing market conditions, maintain cost competitiveness, and demonstrate environmental stewardship will be crucial for long-term success in this evolving market landscape.

CAPEX Oil and Gas Market Leaders

-

Exxon Mobil Corporation

-

BP PLC

-

Chevron Corporation

-

Shell Plc

-

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

CAPEX Oil and Gas Market News

- In January 2023, Cairn Oil & Gas, Vedanta Limited, one of the major oil and gas exploration and production companies in India, signed a proposal for USD 2.5 billion investment in the oil and gas sector. Cairn Vedanta has started exploration and other development works in the Petroleum Exploration Licence (PEL) and Petroleum Mining Lease (PML) blocks in Barmer and Jalore districts, Rajasthan.

- In February 2022, the Government of India owned Public Sector Units (PSUs) such as Oil and Natural Gas Corporation (ONGC), Indian Oil Corporation Limited (IOCL), GAIL (India) Ltd., Bharat Petroleum Corporation Limited, and Hindustan Petroleum Corporation Limited (HPCL) announced USD 14.5 billion, as part of center's massive spending on an expansion drive to spur economic growth.

CAPEX Oil and Gas Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD, till 2028

- 4.3 Crude Oil Production and Consumption Forecast, till 2028

- 4.4 Natural Gas Production and Consumption Forecast, till 2028

- 4.5 Installed Pipeline Historic Capacity and Forecast in Kilometers, till 2028

- 4.6 Historic and Production Forecast of Tight Oil, Oil Sands, and Crude from Deepwater in kb/d, until 2030

- 4.7 Recent Trends and Developments

- 4.8 Government Policies and Regulations

-

4.9 Market Dynamics

- 4.9.1 Drivers

- 4.9.1.1 Increasing Demand for Natural Gas and Developing Gas Infrastructure

- 4.9.1.2 Increasing Offshore Oil & Gas Exploration Activities

- 4.9.2 Restraints

- 4.9.2.1 Adoption of Cleaner Alternatives

- 4.9.2.2 High Volatility of Crude Oil Prices

- 4.10 Supply Chain Analysis

-

4.11 Porter's Five Forces Analysis

- 4.11.1 Bargaining Power of Suppliers

- 4.11.2 Bargaining Power of Consumers

- 4.11.3 Threat of New Entrants

- 4.11.4 Threat of Substitutes Products and Services

- 4.11.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Sector

- 5.1.1 Upstream

- 5.1.2 Midstream

- 5.1.3 Downstream

-

5.2 Location

- 5.2.1 Onshore

- 5.2.2 Offshore

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 Russia

- 5.3.2.4 Norway

- 5.3.2.5 Netherlands

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Malaysia

- 5.3.3.4 Indonesia

- 5.3.3.5 ASEAN Countries

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Venezuela

- 5.3.4.3 Argentina

- 5.3.4.4 Colombia

- 5.3.4.5 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates (UAE)

- 5.3.5.3 Egypt

- 5.3.5.4 Nigeria

- 5.3.5.5 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 BP plc

- 6.3.2 Shell plc

- 6.3.3 Chevron Corporation

- 6.3.4 Total Energies SE

- 6.3.5 Exxon Mobil Corporation

- 6.3.6 Oil and Natural Gas Corporation (ONGC)

- 6.3.7 China National Petroleum Corporation (CNPC)

- 6.3.8 Cairn Oil & Gas, Vertical of Vedanta Limited

- 6.3.9 Petroleo Brasileiro SA

- 6.3.10 Equinor ASA

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Untapped Oil and Gas Potential in Emerging Markets

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

CAPEX Oil and Gas Industry Segmentation

Capital expenditure (CAPEX) is the funds used by a company/organization to acquire, upgrade, and maintain physical assets, such as property, plants, buildings, technology, or equipment. CAPEX is often used to undertake new projects or investments by a company. The global oil and gas CAPEX market consider the total capital expenditure of oil and gas operators worldwide annually. The CAPEX/investments in the upstream, midstream, and downstream oil and gas projects across different regions are taken into consideration while estimating the market size.

The oil & gas CAPEX market is segmented by sector, location and geography. By sector, the market is segmented into upstream, midstream, and downstream. By location, the market is segmented into onshore and offshore. The report also covers the market size and forecasts for the oil & gas CAPEX market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Sector | Upstream | ||

| Midstream | |||

| Downstream | |||

| Location | Onshore | ||

| Offshore | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| Russia | |||

| Norway | |||

| Netherlands | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Malaysia | |||

| Indonesia | |||

| ASEAN Countries | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Venezuela | |||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Middle-East and Africa | Saudi Arabia | ||

| United Arab Emirates (UAE) | |||

| Egypt | |||

| Nigeria | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

CAPEX Oil and Gas Market Research FAQs

What is the current Oil and Gas CAPEX Market size?

The Oil and Gas CAPEX Market is projected to register a CAGR of 4.27% during the forecast period (2025-2030)

Who are the key players in Oil and Gas CAPEX Market?

Exxon Mobil Corporation, BP PLC, Chevron Corporation, Shell Plc and TotalEnergies SE are the major companies operating in the Oil and Gas CAPEX Market.

Which is the fastest growing region in Oil and Gas CAPEX Market?

Middle East and Africa is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Oil and Gas CAPEX Market?

In 2025, the North America accounts for the largest market share in Oil and Gas CAPEX Market.

What years does this Oil and Gas CAPEX Market cover?

The report covers the Oil and Gas CAPEX Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Oil and Gas CAPEX Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Oil and Gas CAPEX Outlook Research

Mordor Intelligence delivers comprehensive insights into oil and gas industry operations and markets. We specialize in detailed analysis of oil and gas CAPEX trends and future projections. Our extensive research covers upstream capital expenditures and oil production CAPEX. This provides stakeholders with crucial CAPEX forecasts through 2028. The report offers in-depth analysis of oil and gas capital expenditure patterns. It incorporates advanced forecasting of capital management methodologies to ensure accurate projections of CAPEX oil investments.

Stakeholders gain valuable insights through our detailed oil and gas CAPEX by year analysis. This is supported by robust CAPEX forecast models that extend to CAPEX 2028. The report, available as an easy-to-download PDF, includes comprehensive oil and gas CAPEX forecasts. It also provides a detailed examination of oil and gas CAPEX spending trends. Our analysis incorporates the impacts of IT spending in oil and gas market, offering stakeholders actionable intelligence for strategic decision-making. The report's oil pro CAPEX radar methodology ensures thorough coverage of industry dynamics. This enables businesses to optimize their capital allocation strategies effectively.