| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 6.91 Billion |

| Market Size (2030) | USD 11.30 Billion |

| CAGR (2025 - 2030) | 10.35 % |

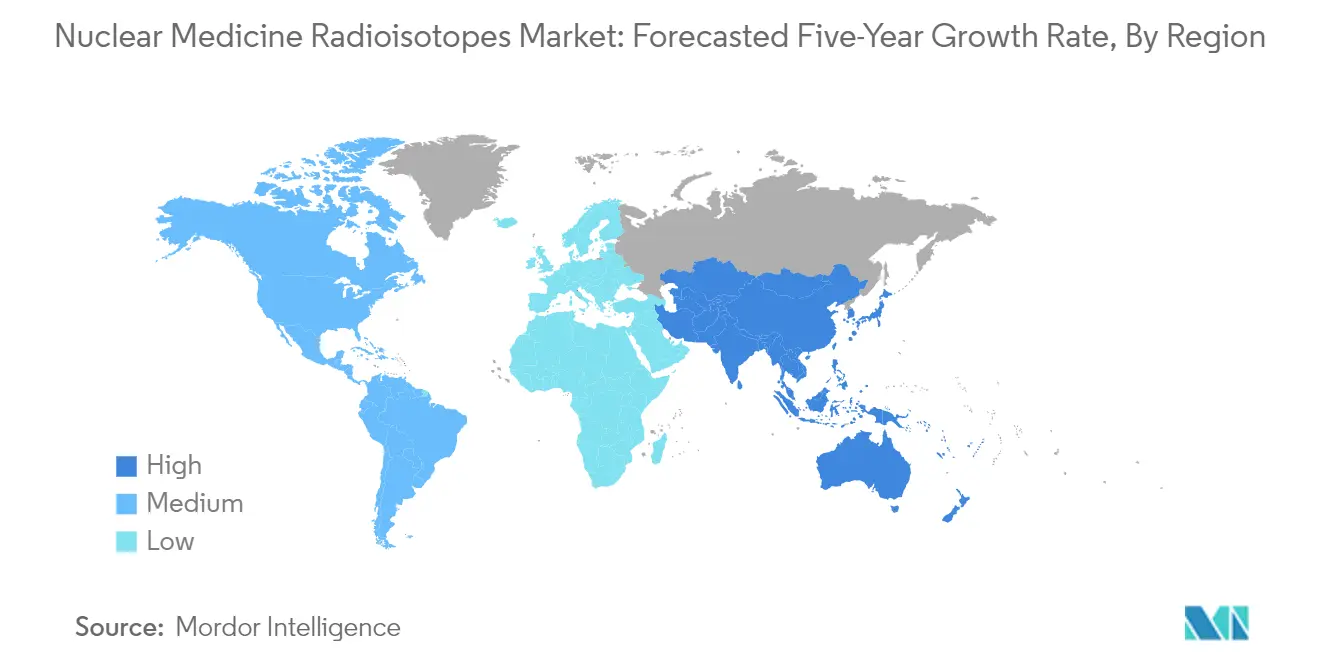

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

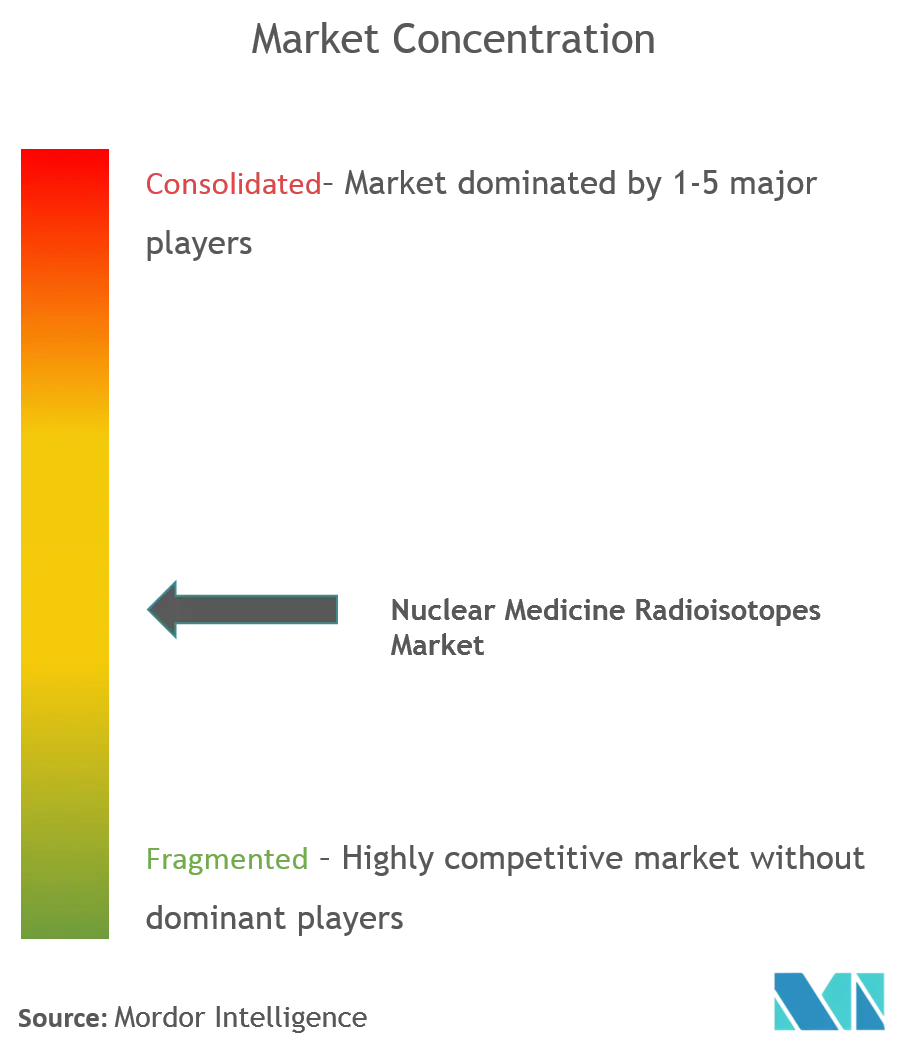

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Nuclear Medicine Radioisotopes Market Analysis

The Nuclear Medicine Radioisotopes Market size is estimated at USD 6.91 billion in 2025, and is expected to reach USD 11.30 billion by 2030, at a CAGR of 10.35% during the forecast period (2025-2030).

The Precision Revolution: Radioisotopes Redefining Treatment Pathways

The integration of radioisotopes into modern medicine represents one of healthcare's most significant advances in precision treatment. These compounds have evolved beyond diagnostic tools to become central in theranostic approaches - where the same isotope can both diagnose and treat disease. This shift has especially impacted oncology, where radioisotopes in medicine now deliver radiation directly to tumor cells while minimizing damage to healthy tissues. A typical radioligand therapy course includes about five doses and costs approximately $250,000 per patient, reflecting both its specialized nature and value. This high price point highlights both the advanced technology involved and the potential for improved clinical outcomes. Clinicians are increasingly using isotopes like Lutetium-177 and Actinium-225 for patients who haven't responded to standard treatments. For healthcare leaders, the key takeaway is straightforward: while radioisotope therapies require significant initial investment, their precision can reduce overall costs by preventing complications and extended hospital stays that come with less targeted approaches. Healthcare systems that develop comprehensive radioisotope capabilities now will be better positioned to offer the precision treatments that patients will increasingly expect as standard care.

The Talent Gap: Addressing Nuclear Medicine's Workforce Challenges

Despite advances in nuclear medicine radioisotopes, a worrying talent shortage threatens the field's continued growth. A clear gender imbalance exists in the workforce - while 55.6% of United States medical school graduates in 2023 were women (up from 47.2% in 2014), women made up only 21.1% of nuclear medicine residents that year. This gap isn't just about diversity; it represents a missed opportunity to bring essential talent into the specialty when demand for radioisotope expertise is growing rapidly. The field faces perception challenges - often seen as technically complex and radiation-focused rather than patient-centered - potentially limiting its appeal across various demographic groups. Healthcare organizations that address this disconnect can gain an advantage by redesigning nuclear medicine training programs to highlight the specialty's unique combination of cutting-edge technology and personalized care. Department leaders should recognize that broadening nuclear medicine's appeal requires more than recruitment efforts; it needs a fundamental shift in how the specialty is presented to medical students and early-career doctors. The clear strategic priority: organizations must work to close this talent gap by showcasing how nuclear medicine careers offer opportunities to pioneer applications of radioisotopes that directly improve patient outcomes.

Value Proposition: Balancing Economic Realities with Clinical Outcomes

The value story of nuclear medicine radioisotopes has shifted from simply being diagnostic tools to becoming essential components in comprehensive care pathways. Health systems are now facing the financial realities of incorporating advanced radioisotopes like Technetium-99m for diagnostics and Lutetium-177 for therapy into regular care protocols. With radioligand therapies costing around $250,000 per patient, healthcare payers and providers must weigh immediate expenses against long-term benefits and quality of life improvements. This value equation is especially important in cardiology, where early, accurate diagnosis using radioisotopes can prevent more expensive interventions later. Forward-thinking healthcare administrators are working with nuclear medicine departments to create economic models that capture both immediate clinical benefits and long-term cost savings from radioisotope-based approaches. These models need to consider the entire patient journey rather than just departmental budgets. For industry players, success requires shifting from focusing on products to emphasizing outcomes - showing not just clinical effectiveness but also economic value. The practical insight for healthcare decision-makers is clear: developing comprehensive value assessment frameworks for radioisotope applications is becoming essential for making smart resource allocation and technology adoption decisions in today's budget-conscious healthcare environment.

Nuclear Medicine Radioisotopes Market Trends

The Silent Epidemic: How Cancer and Cardiac Cases Are Reshaping Nuclear Medicine

The growing prevalence of cancer and cardiac disorders is driving increased demand for nuclear medicine radioisotopes, creating both supply chain challenges and new market opportunities. As populations age and lifestyle-related diseases increase worldwide, healthcare providers need more precise diagnostic tools and targeted therapies. The industry is responding through strategic partnerships, as seen in the February 2025 agreement between Kinectrics and Isotopia for Gadolinium-160 supply to support Terbium-161 production. These collaborations highlight the industry's recognition that reliable radioisotope production infrastructure is essential to meet growing patient needs.The changing clinical landscape has made cardiac imaging and cancer theranostics increasingly important, pushing healthcare providers to adopt more advanced applications of radioisotopes in medicine. Successful healthcare institutions are those implementing comprehensive nuclear medicine programs that integrate both diagnosis and treatment. Companies that invest in diverse, reliable radioisotope supply chains now will have significant advantages as demand grows. The hundreds of clinical trials for radioligand therapies currently conducted by about 75 companies show that the industry is actively developing innovative responses to these health challenges - approaches that will likely create new opportunities for adaptable market participants.

Beyond Diagnostics: Nuclear Medicine's Expanding Treatment Territory

Nuclear medicine is growing beyond its traditional diagnostic role, with therapeutic applications of radioisotopes becoming one of the fastest-growing areas in healthcare. This shift from primarily diagnostic to therapeutic applications has made radioisotopes increasingly important throughout healthcare systems. The industry's innovation is evident in the hundreds of clinical trials for radioligand therapies currently being conducted by approximately 75 companies, showing both the medical potential and business opportunities in these advanced treatments. Forward-looking healthcare providers recognize that building comprehensive nuclear medicine capabilities offers a competitive edge while improving patient outcomes - especially important as healthcare continues to focus on value-based care.The medical uses of radioisotopes now include targeted cancer treatments, neurological disorder therapies, and even infectious disease management - uses that were just theoretical a few years ago. This expansion has led to major infrastructure investments, with companies planning to invest over $25 million per new production facility on both U.S. coasts to ensure reliable supplies and better geographic coverage. For healthcare systems, the key takeaway is clear: developing expertise in nuclear medicine applications now will position them advantageously as treatment approaches continue to evolve. Those who don't build these capabilities risk falling behind clinically and competitively as therapeutic radioisotopes become standard in treatments across more medical conditions.

The Imaging Revolution: SPECT and PET Redefining Patient Care

The increasing use of SPECT and PET imaging represents a major shift in how healthcare providers detect, stage, and monitor diseases - driving demand for specialized radioisotopes across healthcare settings. These advanced imaging technologies have become essential in oncology, neurology, and cardiology, providing detailed molecular insights that conventional imaging cannot offer. The importance of these technologies has driven infrastructure growth, with planned investments exceeding $25 million per new radiopharmaceutical production facility on both U.S. coasts. For healthcare leaders, the message is clear: facilities without access to SPECT and PET capabilities may struggle to remain competitive in specialty care areas.Modern nuclear medicine applications require not just technology investment but also expertise in radioisotope handling, image interpretation, and clinical integration. As treatment decisions are increasingly guided by molecular imaging results, the line between diagnostic and therapeutic radiology continues to blur. The February 2025 partnership between Kinectrics and Isotopia for radioisotope production shows how the industry is responding to these needs through supply chain collaborations. Healthcare providers who gain a competitive edge are those developing smooth clinical pathways that incorporate SPECT and PET insights throughout patient care. This integration requires both technical infrastructure and cross-disciplinary expertise - investments that lead to better clinical outcomes, operational efficiency, and patient satisfaction.

Informed Patients, Evolving Markets: The Awareness Effect

Today's patients come to appointments with significant knowledge about radioisotopes in medicine and radiation-based treatments, changing how providers and patients discuss and decide on treatment options. This increased awareness, driven by online health resources and patient advocacy groups, has changed radiation therapies from feared last resorts to specifically requested options in many cases. The industry is responding to this shift, as shown by the hundreds of clinical trials for radioligand therapies currently conducted by approximately 75 companies - many designed with patient preferences in mind. For healthcare providers, this change means developing better patient education resources and consent processes that respect patients as informed participants in treatment decisions.The effects of increasing patient awareness influence everything from facility design to marketing approaches. Healthcare institutions gaining market share are those being transparent about radiation procedures while highlighting their investments in precision technologies and safety protocols. The strategic partnership between Kinectrics and Isotopia announced in February 2025 represents an industry response to meet both volume demands and quality expectations from increasingly informed patients. For nuclear medicine departments and radiation oncology practices, the key insight is clear: developing good, accessible patient education resources that explain radiation-based diagnostics and treatments creates competitive advantages through improved patient comfort, treatment adherence, and clinical outcomes.

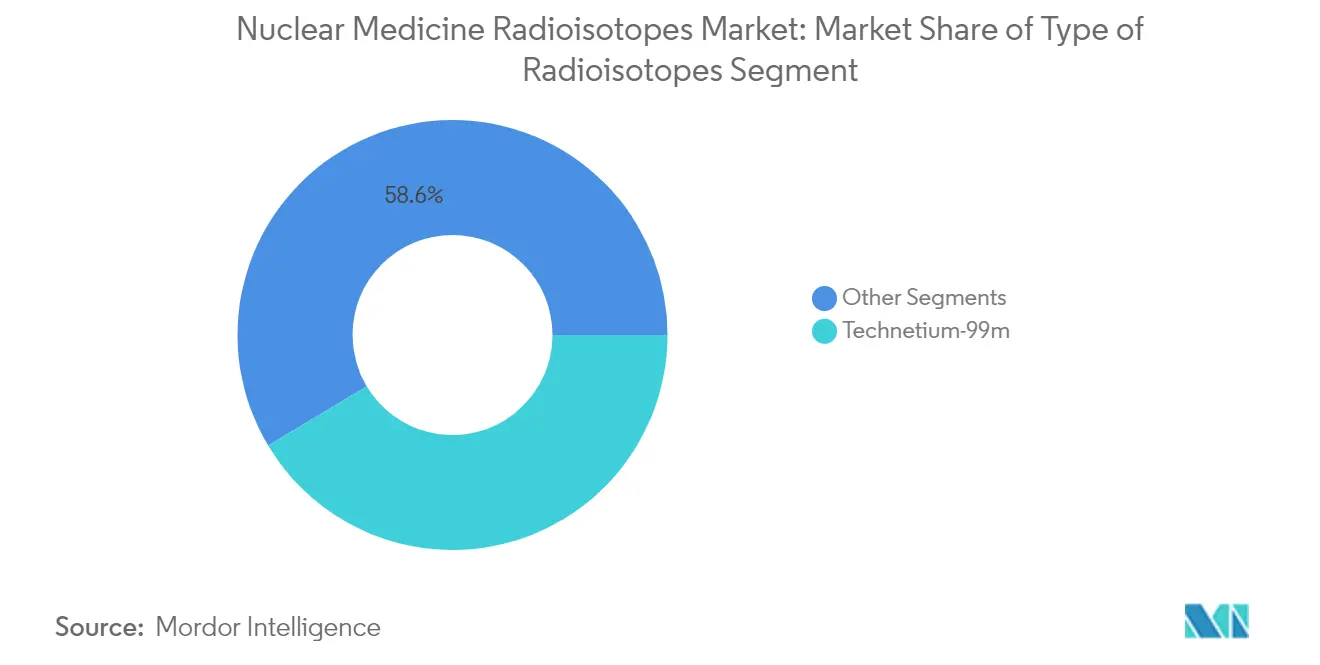

Segment Analysis: Type of Radioisotopes

Technetium-99m: The Cornerstone of Nuclear Diagnostics

Technetium-99m holds a commanding ~41.6% market share in 2025, establishing it as the most widely used radioisotope in medicine. Its popularity stems from practical advantages - a six-hour half-life that balances diagnostic utility with minimal patient radiation exposure. Growing at ~9.37% annually, Tc-99m is expanding faster than the overall market, driven by its versatility across cardiac, bone, and organ imaging applications. Its 140 keV gamma emissions align perfectly with standard SPECT imaging equipment, making it the preferred choice for roughly 80% of nuclear diagnostic procedures. For hospitals and suppliers, Tc-99m offers a reliable foundation that combines established infrastructure with ongoing production innovations - including methods that can yield up to 37 Ci from a single 6-hour irradiation. This balance of clinical effectiveness with operational efficiency explains why Tc-99m remains the backbone of nuclear medicine programs worldwide.

Therapeutic and Specialized Diagnostic Radioisotopes: Opening New Treatment Pathways

Beyond Technetium's diagnostic applications, specialized radioisotopes are creating new treatment options across medicine. Thallium-201 with its 73-hour half-life enables extended cardiac studies, while Iodine-123's 13.2-hour profile is ideal for thyroid assessment. The therapeutic landscape is evolving rapidly through isotopes like Lutetium-177 and Actinium-225 - the latter's 9.92-day half-life providing an optimal window for targeted cancer treatments. Production advances are accelerating this trend, as demonstrated by Nusano's 2025 announcement of a 100-fold increase in Astatine-211 availability. For pharmaceutical developers, these specialized isotopes offer strategic opportunities in precision medicine, though their more complex supply chains create both challenges and entry points for agile producers. The careful selection of isotopes based on decay properties, tissue penetration, and targeting specificity represents a key area for innovation, requiring expertise across physics, chemistry, and clinical medicine.

Segment Analysis: By Application

Cardiology: The Foundation of Nuclear Medicine's Clinical Value

Cardiology applications remain the largest segment in nuclear medicine, representing ~40% of the global nuclear medicine radioisotope market in 2025. This leading position comes from nuclear cardiology's unique ability to provide functional information about heart muscle perfusion, viability, and metabolism that other imaging methods cannot deliver. Thallium-201, with its 73-hour half-life, continues to be essential for evaluating blood flow to the heart and diagnosing coronary artery disease, while newer Technetium-based tracers offer better images with less radiation. Cardiac applications maintain their importance because they're deeply integrated into clinical decision-making for both acute and chronic heart conditions. For radiopharmaceutical companies, cardiology provides a stable revenue base but requires ongoing research to demonstrate advantages over newer imaging alternatives. The next competitive advantage will come from developing radiopharmaceuticals that can identify heart disease before structural changes appear.

Oncology: The Growth Engine of Nuclear Medicine Innovation

Oncology applications are growing fastest in nuclear medicine, with a strong ~11.2% annual growth rate that outpaces the broader market. This expansion comes from combining targeted imaging with therapeutic radioisotopes - creating paired approaches that can both visualize and treat cancers with high precision. The market potential is substantial, as seen with gastroenteropancreatic neuroendocrine tumors, which affect about 18,000 new patients yearly in the United States, with roughly 80% expressing receptors ideal for radiopharmaceutical therapy. The rapid adoption of applications of radioisotopes in oncology reflects a shift from traditional chemotherapy toward targeted treatments that deliver radiation directly to cancer cells while protecting healthy tissue. For drug developers, this presents an opportunity that requires collaboration between radiation specialists and oncology researchers. Companies that can develop integrated systems covering isotope production, chemistry, targeting molecules, and clinical testing will capture significant value by offering complete solutions rather than individual components.

Specialized Clinical Applications: Expanding Nuclear Medicine's Reach

Nuclear medicine is extending beyond its traditional areas into specialized clinical applications that showcase its versatility. Thyroid disorders continue to benefit from Iodine-123 assessment with its 13.2-hour half-life, providing precise measurements of gland function that guide treatment decisions. In neurology, radioisotopes are advancing our understanding of conditions like Parkinson's and Alzheimer's by visualizing molecular targets associated with brain degeneration. Specialized lung applications are also emerging, with V/Q scans using technetium-99m compounds proving valuable for assessing pulmonary vein stenosis by identifying blood flow limitations in cases exceeding 70-80% narrowing. For hospitals and imaging centers, these diverse applications require careful planning of radiopharmacy operations to balance the range of isotopes needed against how frequently they're used. The expanding application landscape also creates opportunities for specialized training programs in these niche but valuable clinical areas. Forward-thinking healthcare providers are building cross-specialty nuclear medicine services that extend beyond traditional boundaries to offer comprehensive diagnostic and treatment capabilities.

Geography Analysis

North America: The Cornerstone of Nuclear Medicine Radioisotope Innovation and Adoption

North America stands as the dominant force in the nuclear medicine radioisotopes market, commanding approximately 42.5% of the global market share in 2025. This regional dominance stems from a robust healthcare infrastructure, substantial R&D investments, and early adoption of advanced diagnostic and therapeutic procedures. The region's leadership position is further cemented by its well-established regulatory frameworks and reimbursement policies that facilitate the integration of radioisotope-based procedures into standard care protocols. In the United States alone, Technetium-99m (Tc-99m), the decay product of molybdenum-99 (Mo-99), is used in over 40,000 medical procedures per day for diagnosing conditions such as heart disease and cancer. The actionable insight for stakeholders is clear: North America continues to serve not just as a revenue center but as the innovation hub where emerging radioisotope applications are likely to gain their first commercial foothold, making it essential for companies to establish and maintain strong regional partnerships and distribution networks to capture value.

United States: The Market Powerhouse Driven by Clinical Excellence and Infrastructure

The United States represents the largest country segment within North America, accounting for the lion's share of the regional nuclear medicine radioisotopes consumption. This market leadership position is built upon the country's extensive network of specialized nuclear medicine facilities, comprehensive reimbursement structures, and continuous technological advancements in both diagnostics and therapeutics. The market is further energized by strategic investment in production facilities, exemplified by Nucleus which has already booked about 50-60% of its Rochester plant's capacity ahead of its operational start, with dose production anticipated to commence in Q3 of 2024. This indicates strong demand for scalable radioligand therapy manufacturing. The key takeaway for industry players is that the U.S. market represents not just volume but also value opportunities—companies that can deliver specialized, high-margin radioisotope solutions while navigating the complex regulatory landscape will find substantial growth potential in this mature but still evolving market.

Canada: Emerging as the Region's Growth Accelerator Through Regulatory Excellence

Canada emerges as the fastest-growing market within North America, demonstrating impressive growth momentum with a remarkable compound annual growth rate in the radioisotopes in medicine segment. This growth trajectory is largely attributable to Canada's strategic investments in radioisotope production capabilities, comprehensive healthcare coverage, and growing specialization in nuclear medicine practices. The country has also established clear and structured regulatory frameworks that simultaneously ensure safety while facilitating innovation—the regulatory criteria specify that in all areas where unsealed nuclear substances are used or stored, non-fixed contamination limits must not exceed 3 Bq/cm² for Class A radionuclides, 30 Bq/cm² for Class B radionuclides, and 300 Bq/cm² for Class C radionuclides. The actionable insight for market participants is that Canada offers a unique combination of growth potential and regulatory predictability, making it an ideal testing ground for new radioisotope applications before broader North American rollout—companies that develop strategic partnerships with Canadian research institutions and healthcare providers position themselves advantageously for regional expansion.

Mexico: Completing North America's Radioisotope Landscape with Accessibility Focus

Mexico completes the North American nuclear medicine radioisotopes landscape by addressing a different market need: expanding access to nuclear medicine procedures for a broader population base. While not matching the market sophistication of its northern neighbors, Mexico represents an important component of the regional market, with growing investments in healthcare infrastructure and increasing adoption of nuclear medicine techniques, particularly in major urban centers. The country's healthcare system is gradually incorporating more advanced diagnostic and therapeutic procedures, creating opportunities for radioisotope suppliers who can tailor their offerings to the specific needs and constraints of emerging markets. The key insight for stakeholders is that Mexico offers unique opportunities for companies willing to adapt their business models to address accessibility and affordability challenges—success here requires not just supplying radioisotopes but also supporting the development of the supporting ecosystem, from equipment maintenance to specialist training. As the applications of radioisotopes in medicine continue to expand, Mexico's market represents the bridge between developed and developing markets within the North American context.

Europe: The Balanced Power in Radioisotope Applications Driven by Clinical Research Excellence

Europe maintains a formidable position in the global nuclear medicine radioisotopes landscape, balancing clinical excellence with regulatory rigor. The region's strength lies in its robust research ecosystem and collaborative approach to advancing radioisotope applications, particularly in oncology and cardiology. European centers have been at the forefront of radioisotope therapy innovation, as evidenced by a multi-center European observational study published in June 2024, which showed that after three cycles of 177Lu-PSMA (prostate-specific membrane antigen) ligand therapy, 77.8% of patients exhibited a prostate specific antigen (PSA) decrease of ≥30%, demonstrating a strong biochemical response. This clinical research excellence translates into practical applications that drive market growth. For industry participants, Europe's value proposition centers on clinical validation—radioisotope products that demonstrate efficacy in European clinical settings gain credibility that translates globally, making strategic partnerships with European research institutions and healthcare providers critical for product development and validation pipelines.

Germany: The European Epicenter for Radioisotope Innovation and Commercialization

Germany establishes itself as the largest country market within Europe's nuclear medicine radioisotopes landscape, driving regional adoption through its combination of research excellence, manufacturing capabilities, and widespread clinical implementation. The country's leadership position was recently reinforced when, on May 3, 2025, Isotopia announced the official commercial launch of Isoprotrace in Germany in partnership with DSD Pharma, marking a notable strategic advancement in the nuclear medicine radioisotopes market. This commercial milestone underscores Germany's role as both an innovation hub and a sophisticated end-user market. The crucial insight for market participants is that Germany serves as the European bellwether for radioisotope products—success in the German market often predicts broader European adoption, making it the ideal testbed for new products and applications. Companies that can navigate Germany's demanding but transparent regulatory environment position themselves advantageously for pan-European expansion.

Rest of Europe: A Diverse Landscape of Opportunity Through Specialized Applications

The remaining European markets collectively represent a mosaic of opportunities for nuclear medicine radioisotope applications, each with distinct characteristics and growth drivers. The United Kingdom leverages its research strengths in developing novel applications, particularly in theranostics, while France maintains a balanced approach between diagnostic and therapeutic applications. Italy and Spain demonstrate growing adoption rates, particularly in oncology applications, as evidenced by multi-center European studies involving 177Lu-PSMA therapy for metastatic castration-resistant prostate cancer patients, which exhibited a median radiographic progression-free survival of 4.4 months. Eastern European markets offer growth potential through improving healthcare infrastructure and increasing access to nuclear medicine procedures. The key insight for market participants is that success in these diverse markets requires a tailored approach—understanding the specific clinical priorities, reimbursement structures, and regulatory nuances of each country enables companies to position their radioisotope products optimally. Investment in local partnerships and market-specific applications development can unlock significant value across these varied European landscapes.

Asia-Pacific: The Emerging Frontier in Radioisotope Applications with Unmatched Growth Momentum

The Asia-Pacific region represents the most dynamic growth story in the global nuclear medicine radioisotopes market, advancing at a remarkable CAGR of approximately 11.8% through 2025. This exceptional growth trajectory is driven by rapidly expanding healthcare infrastructure, increasing prevalence of cancer and cardiovascular diseases, and growing acceptance of nuclear medicine procedures across both developed and developing economies in the region. The market dynamics are shaped by the dual forces of established markets pursuing specialized applications and emerging markets building foundational nuclear medicine capabilities. Companies with global ambitions in the radioisotope space must recognize that Asia-Pacific represents not just future potential but current opportunity—the region's growth rate means that even well-established players need to reassess their geographic priorities, as the next wave of radioisotope innovation and adoption may well be centered in these dynamic markets rather than traditional Western strongholds.

Rest of the World: Emerging Opportunities Through Localized Approaches

The Rest of the World segment, encompassing the Middle East, Africa, and South America, presents a mosaic of emerging opportunities in the nuclear medicine radioisotopes landscape. These regions are characterized by highly variable healthcare infrastructure, with centers of excellence in urban areas contrasting with limited access in rural regions. The Middle East, particularly Gulf Cooperation Council countries, leads adoption through significant healthcare investments and medical tourism initiatives, while Latin American markets demonstrate growing incorporation of nuclear medicine into major healthcare centers. African markets show more limited but developing nuclear medicine capabilities, concentrated in a few countries such as South Africa and Egypt. Companies with truly global ambitions need to recognize that these markets, while currently smaller than the established regions, present significant long-term growth potential—particularly as healthcare systems develop and the applications of radioisotopes in medicine continue to expand beyond traditional uses into new therapeutic areas. Success in these diverse markets requires not just product offerings but comprehensive solutions that address infrastructure limitations, specialist training needs, and sustainable supply chain challenges unique to each region.

Nuclear Medicine Radioisotopes Industry Overview

Strategic Consolidation: Big Pharma's Billion-Dollar Bet on Radiopharmaceuticals

The nuclear medicine radioisotopes market is experiencing a wave of strategic consolidation as pharmaceutical giants stake their claims through high-value acquisitions and partnerships. This competitive repositioning is evident in Eli Lilly's October 2023 acquisition of POINT's pipeline of clinical and preclinical-stage radiotherapeutics for cancer treatment, valued at approximately $1.4 billion. Just months earlier, Genentech entered a $1-billion co-development deal with PeptiDream to advance radiopharmaceuticals. These substantial investments reveal how established players are leveraging their financial muscle to secure promising radioisotopes in medicine technologies while creating entry barriers for smaller innovators. Companies that develop specialized capabilities in radiochemistry and targeted delivery mechanisms will secure dominant positions as the market evolves, forcing mid-sized players to either specialize in niche applications or establish strategic alliances to maintain relevance in this rapidly consolidating landscape.

Supply Chain Mastery: The New Competitive Battleground

Beyond product portfolios, supply chain excellence has emerged as the decisive competitive differentiator in the medical radioisotopes sector, with reliable isotope availability becoming a significant strategic advantage. Industry leader Curium exemplifies this advantage by delivering nuclear medicine solutions to 14 million patients annually, demonstrating operational scale and distribution capabilities that smaller competitors struggle to match. This infrastructure-centered competition is particularly critical for short-lived isotopes like Technetium-99m, where time-sensitive logistics directly translate to market success. Forward-thinking companies are investing in decentralized production facilities, redundant supply networks, and innovative manufacturing technologies to overcome the historical supply vulnerabilities in the radioactive isotopes in medicine field. Organizations that establish end-to-end control from isotope production through final patient delivery will create sustainable competitive advantages that transcend product differentiation, making supply chain resilience the determining factor for market leadership.

Regional Strategy Divergence: Customizing for Global Success

A nuanced regional approach has become essential in the nuclear medicine market as competition diverges along geographic lines, with successful companies developing distinct strategies for mature versus emerging markets. While North America remains the largest market concentration, strategic focus is shifting toward capturing Asia-Pacific's accelerated growth through targeted expansion initiatives. This market bifurcation is prompting companies to balance defending established positions while aggressively expanding in high-growth regions. Leading organizations are establishing regional innovation hubs, forming local partnerships to navigate regulatory hurdles, and developing market-specific product adaptations that address unique healthcare system requirements. The most successful competitors will implement flexible go-to-market models that adapt to regional dynamics while maintaining global scale advantages, recognizing that geographic customization in the application of radioisotopes in medicine has evolved from a secondary consideration to a primary determinant of competitive success.

Nuclear Medicine Radioisotopes Market Leaders

-

NTP Radioisotopes SOC Ltd

-

Bayer AG

-

GE Healthcare

-

Nordion Inc. (Sotera Health Company)

-

Cardinal Health Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Nuclear Medicine Radioisotopes Market News

- Jan 2023: NorthStar Medical Radioisotopes LLC stated that the company has advanced its new technology for non-uranium-based production of the critical medical radioisotope, molybdenum-99 (Mo-99). The proprietary electron accelerator technology of the company successfully produced Mo-99 at its recently completed Accelerator Production facility on its Beloit campus in Wisconsin, United States.

- Mar 2022: Bracco Imaging launched its new subsidiary, Blue Earth Therapeutics, to advance the development of next-generation therapeutic radiopharmaceutical technology for cancer patients.

Nuclear Medicine Radioisotopes Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Rising Burden of Cancer and Cardiac Disorders

- 4.2.2 Widening Applications of Nuclear Medicine

- 4.2.3 Increasing SPECT and PET Applications

- 4.2.4 Increasing Patient Awareness on Radiation and Radiation Therapy

-

4.3 Market Restraints

- 4.3.1 Reimbursement Complications

- 4.3.2 Regulatory Issues

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value - USD)

-

5.1 Type of Radioisotopes

- 5.1.1 Technetium-99m (Tc-99m)

- 5.1.2 Thallium-201 (Tl-201)

- 5.1.3 Iodine (I-123)

- 5.1.4 Fluorine-18

- 5.1.5 Rubidium-82 (Rb-82)

- 5.1.6 Iodine-131 (I-131)

- 5.1.7 Lutetium-177 (Lu-177)

- 5.1.8 Radium-223 (Ra-223) and Alpharadin

- 5.1.9 Actinium-225 (Ac-225)

- 5.1.10 Other Types of Radioisotopes

-

5.2 By Application

- 5.2.1 Oncology

- 5.2.2 Cardiology

- 5.2.3 Thyroid

- 5.2.4 Neurology

- 5.2.5 Other Applications

-

5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Rest of the World

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Bayer AG

- 6.1.2 Bracco SpA

- 6.1.3 Cardinal Health Inc.

- 6.1.4 Curium

- 6.1.5 Lantheus Medical Imaging Inc.

- 6.1.6 GE Healthcare

- 6.1.7 NTP Radioisotopes SOC Ltd

- 6.1.8 Nordion Inc. (Sotera Health Company)

- 6.1.9 NorthStar Medical Radioisotopes

- 6.1.10 Eckert & Ziegler

- 6.1.11 Jubilant Pharma Company (Jubilant DraxImage)

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

**Competitive Landscape Covers - Business Overview, Financials, Products and Strategies, and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Nuclear Medicine Radioisotopes Industry Segmentation

As per the scope of the report, medical radioisotopes are defined as safe radioactive substances that are primarily used in the diagnosis of medical conditions. These radioisotopes, used in a diagnosis, emit gamma rays of energy that are sufficient to escape from the body. The rays also have a short half-life, which is appropriate since the rays can decay as soon as the imaging is completed.

The nuclear medicine radioisotopes market is segmented into by type of radioisotope, application and geography. By type of radioisotopes, the market is segmented as Technetium-99m (Tc-99m), Thallium-201 (Tl-201), Iodine (I-123), Fluorine-18, Rubidium-82 (Rb-82), Iodine-131 (I-131), Lutetium-177 (Lu-177), Radium-223 (Ra-223) and Alpharadin, Actinium-225 (Ac-225), and other types of radioisotopes. By application, the market is segmented as oncology, cardiology, thyroid, neurology, and other applications. The report offers the market size in value terms in USD for all the abovementioned segments.

| Type of Radioisotopes | Technetium-99m (Tc-99m) | ||

| Thallium-201 (Tl-201) | |||

| Iodine (I-123) | |||

| Fluorine-18 | |||

| Rubidium-82 (Rb-82) | |||

| Iodine-131 (I-131) | |||

| Lutetium-177 (Lu-177) | |||

| Radium-223 (Ra-223) and Alpharadin | |||

| Actinium-225 (Ac-225) | |||

| Other Types of Radioisotopes | |||

| By Application | Oncology | ||

| Cardiology | |||

| Thyroid | |||

| Neurology | |||

| Other Applications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Rest of the World | |||

Need A Different Region or Segment?

Customize Now

Nuclear Medicine Radioisotopes Market Research Faqs

How big is the Nuclear Medicine Radioisotopes Market?

The Nuclear Medicine Radioisotopes Market size is expected to reach USD 6.91 billion in 2025 and grow at a CAGR of 10.35% to reach USD 11.30 billion by 2030.

What is the current Nuclear Medicine Radioisotopes Market size?

In 2025, the Nuclear Medicine Radioisotopes Market size is expected to reach USD 6.91 billion.

Which is the fastest growing region in Nuclear Medicine Radioisotopes Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Nuclear Medicine Radioisotopes Market?

In 2025, the North America accounts for the largest market share in Nuclear Medicine Radioisotopes Market.

What years does this Nuclear Medicine Radioisotopes Market cover, and what was the market size in 2024?

In 2024, the Nuclear Medicine Radioisotopes Market size was estimated at USD 6.19 billion. The report covers the Nuclear Medicine Radioisotopes Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Nuclear Medicine Radioisotopes Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Nuclear Medicine Radioisotopes Industry Report

The global nuclear medicine radioisotopes market is experiencing significant growth driven by increasing cancer prevalence, demand for nuclear medicines, and technological advancements. Nuclear medicine radioisotopes are used in diagnostic and therapeutic applications, offering benefits such as non-invasive procedures and lower side effects compared to traditional treatments. Key market segments include diagnostics (technetium-99m, gallium-67, thallium-201, fluorine-18) and therapeutics (rhenium-186, iodine-131, samarium-153, yttrium-90), with applications in cardiology, oncology, thyroid, neurology, and others.

North America leads the market due to advanced healthcare infrastructure and rising chronic diseases, while the Asia-Pacific region shows strong growth potential. The market is competitive, driven by R&D activities, product launches, and increasing healthcare expenditures. Insights into regional markets, including North America, Europe, Asia Pacific, Latin America, and the Middle East and Africa, showcase the broad scope and opportunities within this industry.

The market share and market size are critical factors in understanding the industry's dynamics. An industry analysis reveals that the industry overview and industry report provide valuable insights. The market analysis and market forecast are essential for predicting future trends. The market growth is driven by several factors, including the presence of market leaders and comprehensive market research.

The market trends indicate a positive trajectory, with industry information and industry outlook highlighting the potential for further expansion. Industry reports and industry research are crucial for staying updated with the latest developments. Industry sales, industry size, and industry statistics offer quantitative insights into the market's performance.

The market data and market predictions provide a detailed market review, while market segmentation helps in understanding different market segments. The market value is expected to increase, as indicated by the growth rate and market outlook. Report examples and report PDFs are available for a more detailed analysis. Research companies play a significant role in providing accurate and up-to-date information.