Market Size of Nuclear Imaging Industry

| Study Period | 2019 - 2029 |

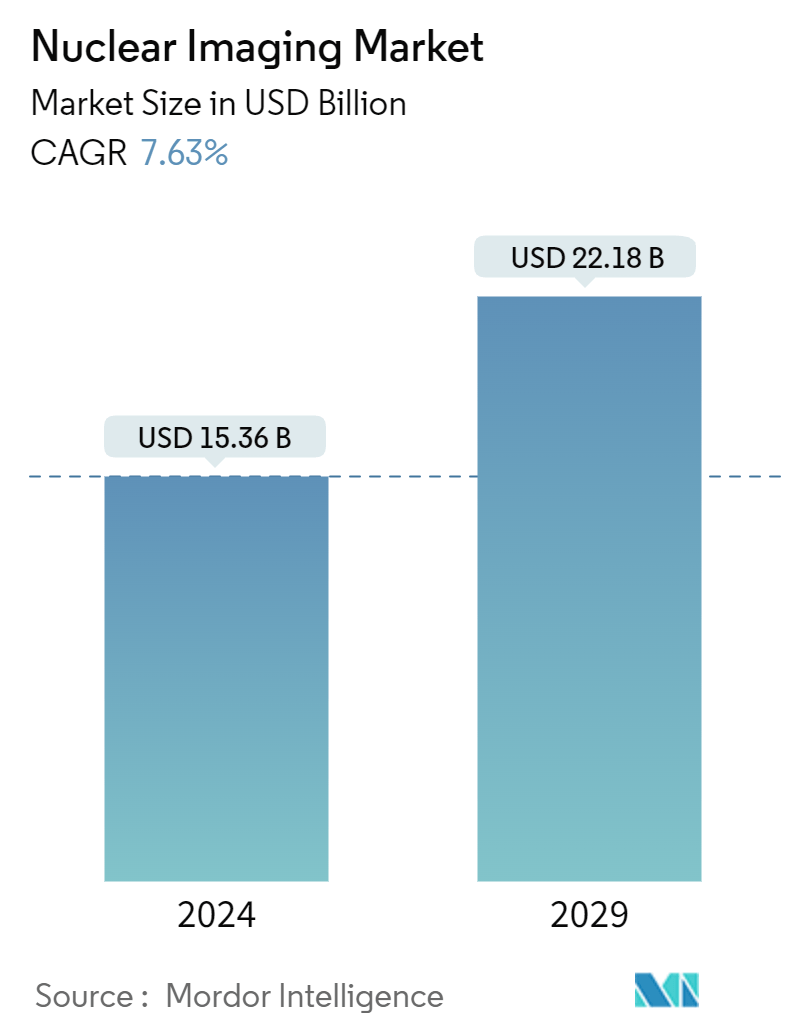

| Market Size (2024) | USD 15.36 Billion |

| Market Size (2029) | USD 22.18 Billion |

| CAGR (2024 - 2029) | 7.63 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Nuclear Imaging Market Analysis

The Nuclear Imaging Market size is estimated at USD 15.36 billion in 2024, and is expected to reach USD 22.18 billion by 2029, growing at a CAGR of 7.63% during the forecast period (2024-2029).

The Nuclear Imaging Market was moderately impacted due to the pandemic. The operation of reactors has been largely classified as an essential service, given its criticality. Therefore, Nuclear Reactors were not shut down during the lockdown. For instance, under Section 71 of the Labour Act 66 of 1995 in South Africa, its SAFARI-1 Reactor remained operational during the lockdown enforced in the country post-March 2020.

However, according to an article published in Seminar in Nuclear Medicine in June 2021, the number of Nuclear Studies, Nuclear Cardiac Imaging, and Oncology Positron Emission Tomography/Computed Tomography decreased in March and April 2020 due to the rise of COVID-19 cases and deaths as reported by the Centers for Disease Control and Prevention (CDC). The study further stated that procedures increased from June 2020 to February 2021 as COVID-19 cases declined. Thus, COVID-19 has slightly impacted the Nuclear Imaging Market with delays in clinical studies, postponement of various surgeries and imaging procedures, an increase in Teleradiology, and several staff-related limitations. However, since the lockdown restrictions were lifted, the industry has been recovering well.

Over the last two years, the market recovery has been led by the high prevalence of chronic diseases. Patients' hospital visits for imaging diagnosis increased as the restrictions were relaxed, and so the Medical Imaging Industry saw a major surge in diagnostics and treatment. This is expected to promote the market's growth in the next few years.

Certain factors that are propelling the growth of the market include technological advancements, increasing diagnostic applications in various diseases, such as cancer and cardiovascular diseases, government support, and a shift from standalone imaging to Hybrid Imaging Systems modalities. For instance, according to the Breast Cancer Factsheet Now 2021, around 55,000 women and 370 men in the United Kingdom are diagnosed with breast cancer every year. Breast cancer has claimed the lives of an estimated 600,000 people in the United Kingdom. This figure is expected to climb to 1.2 million by 2030. Moreover, the growing prevalence of heart diseases is expected to propel the growth of the market. As stated by the American Heart Association 2021 Journal, it is estimated that by 2035, more than 130 million adults in the United States will have some type of heart disease. Thus, the growing prevalence of chronic diseases such as cancer and cardiac diseases is expected to increase demand for early and effective diagnosis, thereby boosting the growth of the Nuclear Imaging Market over the forecast period.

Technological advancements in the Medical Nuclear Imaging System Market have always been challenging to practitioners in terms of how best to optimize them in patient care. Over the past few years, scientists, researchers, and technologists have been able to bring Hybrid Imaging Systems into clinical practice, in which two or even more standalone diagnostic imaging modalities are combined. Some of those multimodality imaging systems include PET/CT, SPECT/CT, PET/MRI, and PET/SPECT/CT. For instance, in October 2022, Spectrum Dynamics announced its newest development in digital Nuclear Medicine Imaging capability to image high-energy isotopes using solid-state detector technology in a 3600-CZT-based, wide-bore SPECT/CT configuration. This functionality is available in the new VERITON-CT 400 Series Digital SPECT/CT scanners, enabling total body, brain, heart, and other imaging applications. With such advances in Nuclear Imaging, the market studied is expected to grow significantly over the forecast period.

The key players are working on many strategic initiatives such as mergers, acquisitions, collaborations, partnerships, and product launches. For instance, in January 2021, Koninklijke Philips NV and Rennes University Hospital signed a five-year innovation and technology partnership to support PET diagnostics, interventional imaging, patient monitoring, and management, among other things. Additionally, in March 2021, GE Healthcare launched StarGuide in the United Kingdom, a next-generation SPECT/CT system that uses the latest digital technologies to help clinicians improve patient outcomes in bone procedures, cardiology, neurology, oncology, and other specialties.

According to the factors mentioned above, such as the growing prevalence of chronic diseases and technological advances in Nuclear Medicine Imaging, the market studied is anticipated to witness growth over the forecast period. However, regulatory issues and a lack of reimbursement may restrain the market's growth.

Nuclear Imaging Industry Segmentation

As per the scope of the report, nuclear medicine imaging procedures are non-invasive, with the exception of intravenous injections, and are usually painless medical tests that help physicians diagnose and evaluate medical conditions. These imaging scans use radioactive materials called radiopharmaceuticals or radiotracers. These radiopharmaceuticals are used in diagnosis and therapeutics. They are small substances that contain a radioactive substance that is used in the treatment of cancer and cardiac and neurological disorders.

The global nuclear imaging market is expected to register a CAGR of 7.63% during the forecast period. The global nuclear imaging market is segmented by product (equipment and radioisotope (SPECT radioisotopes (Technetium-99m (TC-99m), Thallium-201 (TI-201), Gallium (Ga-67), Iodine (I-123), and other SPECT radioisotopes) and PET radioisotopes (Fluorine-18 (F-18), Rubidium-82 (RB-82), and other PET radioisotopes))), application (SPECT applications (cardiology, neurology, thyroid, and other SPECT applications) and PET applications (oncology, cardiology, neurology, and other PET applications)), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (USD million) for the above segments.

| By Product | ||||||||||||||

| Equipment | ||||||||||||||

|

| By Application | ||||||

| ||||||

|

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Nuclear Imaging Market Size Summary

The nuclear imaging market is poised for significant growth over the forecast period, driven by technological advancements and the increasing prevalence of chronic diseases such as cancer and cardiovascular conditions. The market experienced a moderate impact due to the COVID-19 pandemic, with delays in clinical studies and imaging procedures. However, the industry has shown resilience and is recovering as restrictions have eased, leading to a surge in diagnostic and treatment activities. The shift from standalone to hybrid imaging modalities, such as PET/CT and SPECT/CT, has been a key factor in the market's expansion. These advancements have been supported by strategic initiatives from major players, including partnerships and product launches, which have further bolstered the market's growth prospects.

North America is expected to dominate the nuclear imaging market, attributed to technological innovations, a robust healthcare infrastructure, and a high incidence of cancer and cardiovascular diseases. The region's growth is also supported by the introduction of new radiopharmaceuticals and molecular imaging techniques. The competitive landscape is characterized by the presence of major players like Bracco Imaging SpA, Curium, and GE Healthcare, who are actively engaging in strategic collaborations and geographic expansions. These efforts, coupled with the increasing demand for early and effective diagnostics, are anticipated to drive the market's growth, despite potential challenges such as regulatory issues and reimbursement limitations.

Nuclear Imaging Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Rise in Prevalence of Cancer and Cardiac Disorders

-

1.2.2 Increase in Technological Advancements

-

1.2.3 Growth in Applications of Nuclear Medicine and Imaging

-

-

1.3 Market Restraints

-

1.3.1 Regulatory Issues

-

1.3.2 Lack of Reimbursement

-

-

1.4 Industry Attractiveness - Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD Million)

-

2.1 By Product

-

2.1.1 Equipment

-

2.1.2 Radioisotope

-

2.1.2.1 SPECT Radioisotopes

-

2.1.2.1.1 Technetium-99m (TC-99m)

-

2.1.2.1.2 Thallium-201 (TI-201)

-

2.1.2.1.3 Gallium (Ga-67)

-

2.1.2.1.4 Iodine (I-123)

-

2.1.2.1.5 Other SPECT Radioisotopes

-

-

2.1.2.2 PET Radioisotopes

-

2.1.2.2.1 Fluorine-18 (F-18)

-

2.1.2.2.2 Rubidium-82 (RB-82)

-

2.1.2.2.3 Other PET Radioisotopes

-

-

-

-

2.2 By Application

-

2.2.1 SPECT Applications

-

2.2.1.1 Cardiology

-

2.2.1.2 Neurology

-

2.2.1.3 Thyroid

-

2.2.1.4 Other SPECT Applications

-

-

2.2.2 PET Applications

-

2.2.2.1 Oncology

-

2.2.2.2 Cardiology

-

2.2.2.3 Neurology

-

2.2.2.4 Other PET Applications

-

-

-

2.3 Geography

-

2.3.1 North America

-

2.3.1.1 United States

-

2.3.1.2 Canada

-

2.3.1.3 Mexico

-

-

2.3.2 Europe

-

2.3.2.1 Germany

-

2.3.2.2 United Kingdom

-

2.3.2.3 France

-

2.3.2.4 Italy

-

2.3.2.5 Spain

-

2.3.2.6 Rest of Europe

-

-

2.3.3 Asia-Pacific

-

2.3.3.1 China

-

2.3.3.2 Japan

-

2.3.3.3 India

-

2.3.3.4 Australia

-

2.3.3.5 South Korea

-

2.3.3.6 Rest of Asia-Pacific

-

-

2.3.4 Middle East and Africa

-

2.3.4.1 GCC

-

2.3.4.2 South Africa

-

2.3.4.3 Rest of Middle East and Africa

-

-

2.3.5 South America

-

2.3.5.1 Brazil

-

2.3.5.2 Argentina

-

2.3.5.3 Rest of South America

-

-

-

Nuclear Imaging Market Size FAQs

How big is the Nuclear Imaging Market?

The Nuclear Imaging Market size is expected to reach USD 15.36 billion in 2024 and grow at a CAGR of 7.63% to reach USD 22.18 billion by 2029.

What is the current Nuclear Imaging Market size?

In 2024, the Nuclear Imaging Market size is expected to reach USD 15.36 billion.