| Study Period | 2020 - 2030 |

| Base Year For Estimation | 2024 |

| Market Size (2025) | USD 2.01 Billion |

| Market Size (2030) | USD 2.84 Billion |

| CAGR (2025 - 2030) | 7.24 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

Major Players*Disclaimer: Major Players sorted in no particular order |

Next Generation Advanced Battery Market Analysis

The Next Generation Advanced Battery Market size is estimated at USD 2.01 billion in 2025, and is expected to reach USD 2.84 billion by 2030, at a CAGR of 7.24% during the forecast period (2025-2030).

The next-generation advanced battery industry is undergoing a significant transformation as manufacturers shift away from traditional lithium-ion technologies toward more innovative solutions. This evolution is driven by the increasing need for higher energy density, improved safety, and more sustainable battery solutions. The industry has witnessed substantial investments in research and development of various technologies, including solid-state, lithium-sulfur battery, and metal-air battery technologies. A notable development in 2023 was Mercedes-Benz's strategic partnership with ProLogium to accelerate the development of solid-state battery technology, demonstrating the industry's commitment to advancing next-generation solutions.

The raw material landscape for next-generation batteries is experiencing notable changes as manufacturers seek alternatives to traditional lithium-ion battery components. The industry is actively exploring materials such as sulfur, which offers potential cost advantages and higher energy density compared to conventional materials. In May 2023, Britishvolt signed a significant agreement with Monbat Group to acquire EAS, an advanced technology battery cell innovator, valued at USD 36 million, highlighting the industry's focus on securing advanced battery technology capabilities and raw material supply chains.

The integration of next-generation batteries with renewable energy systems represents a crucial market development. Advanced energy storage applications are becoming increasingly sophisticated, with new battery technologies playing a vital role in grid stabilization and renewable energy integration. In 2023, Honeywell and FREYR Battery SA formed a strategic partnership for the deployment of next-generation battery cells, with Honeywell committing to purchase 19 GWh of battery cells through 2030 for energy storage applications, demonstrating the growing importance of advanced batteries in the renewable energy sector.

The commercialization landscape is evolving rapidly with numerous strategic partnerships and technological breakthroughs. Major automotive manufacturers and technology companies are increasingly investing in future battery technology to secure their future supply chains and technological advantages. In early 2024, several manufacturers announced plans to commence production of solid-state batteries, with companies like CATL and Toyota making significant progress in their development efforts. These commercial developments are accompanied by increasing collaboration between battery manufacturers, automotive companies, and research institutions, creating a robust ecosystem for innovation and development in the next-generation battery sector.

Next Generation Advanced Battery Market Trends

Increasing Adoption of Renewable Energy Systems and Associated Energy Storage Systems

The rapid expansion of renewable energy infrastructure has created substantial demand for next-generation advanced energy storage systems, particularly for grid-scale energy storage applications. According to the International Renewable Energy Agency, the global renewable energy capacity witnessed remarkable growth from 1,444 gigawatts in 2012 to approximately 3,064 GW in 2021, with solar and wind energy sources accounting for the largest share. This significant increase in renewable power generation has intensified the need for more efficient and reliable energy storage solutions to address intermittency issues inherent to renewable sources. The development of technologies like flow batteries and solid-state batteries is becoming crucial as they offer superior performance characteristics compared to conventional lithium-ion batteries for grid-scale applications.

The evolution of energy storage requirements has led to breakthrough innovations in battery chemistry and design. For instance, in 2023, Honeywell's new flow battery technology demonstrates the industry's push toward more sustainable solutions, offering non-flammable electrolytes and the ability to store and discharge energy for up to 12 hours – a significant improvement over traditional lithium-ion batteries' 4-hour capacity. These next-generation batteries are designed with recyclable components that don't degrade over time, making them particularly attractive for utility-scale renewable energy projects. The technology's ability to integrate seamlessly with renewable power sources while meeting environmental, longevity, and safety objectives has positioned advanced batteries as a critical enabler for the global transition to renewable energy systems.

Understand The Key Trends Shaping This Market

Download PDF

Rising Raw Material Costs and Supply Chain Constraints

The escalating costs and limited availability of traditional battery materials, particularly lithium, have become a significant driver for the development of next-generation advanced batteries. The average lithium carbonate prices have shown dramatic volatility, rising from $5,180 per metric ton in 2010 to $17,000 per metric ton in 2021, highlighting the urgent need for alternative battery technologies that utilize more abundant and cost-effective materials. This price pressure has accelerated research and development into technologies such as sodium-ion batteries, magnesium-ion batteries, and lithium-sulfur batteries, which rely on more readily available resources and potentially offer more sustainable long-term solutions for energy storage needs.

The industry's response to these challenges has manifested in innovative approaches to battery chemistry and design. For example, zinc-manganese oxide batteries and aluminum-air batteries are emerging as promising alternatives, offering the potential for higher energy density while utilizing more abundant materials. The development of these technologies is particularly significant as projections indicate a growing gap between lithium production and demand, with production expected to reach 1,466 thousand metric tons by 2030 while demand is anticipated to surge to 2,114 thousand metric tons in the same year. This widening supply-demand gap has intensified the focus on developing alternative battery technologies that can provide comparable or superior performance while reducing dependence on scarce raw materials.

Growing Electric Vehicle Market and Transportation Electrification

The accelerating transition toward electric vehicles has emerged as a powerful catalyst for the next-generation advanced automotive battery market. Major automotive manufacturers are making substantial commitments to electrification, as evidenced by Honda Motors' announcement of a USD 39.84 billion investment in electrification and software technologies in 2023, including approximately USD 342.65 million allocated for developing all-solid-state battery production lines. These strategic investments reflect the industry's recognition that advanced battery technologies are crucial for achieving the performance, safety, and cost targets necessary for mass EV adoption. The automotive sector's demands for higher energy density, faster charging capabilities, and enhanced safety features are driving innovation in solid-state batteries, lithium-sulfur batteries, and other advanced technologies.

The automotive industry's push toward electrification has been further intensified by ambitious corporate commitments and technological advancements. Nissan's plans to commercialize laminated all-solid-state batteries by 2028, supported by significant research and development investments, exemplify the industry's focus on next-generation battery technologies. These advanced batteries promise substantial improvements in energy density, with some technologies achieving up to 900 Wh/kg, significantly outperforming conventional lithium-ion batteries. The development of aluminum-air batteries, which offer travel ranges comparable to gasoline-powered vehicles and higher energy density than traditional lithium-ion batteries, represents another promising direction for the industry, although broader adoption awaits supportive policy frameworks and increased manufacturer engagement.

Segment Analysis: Technology

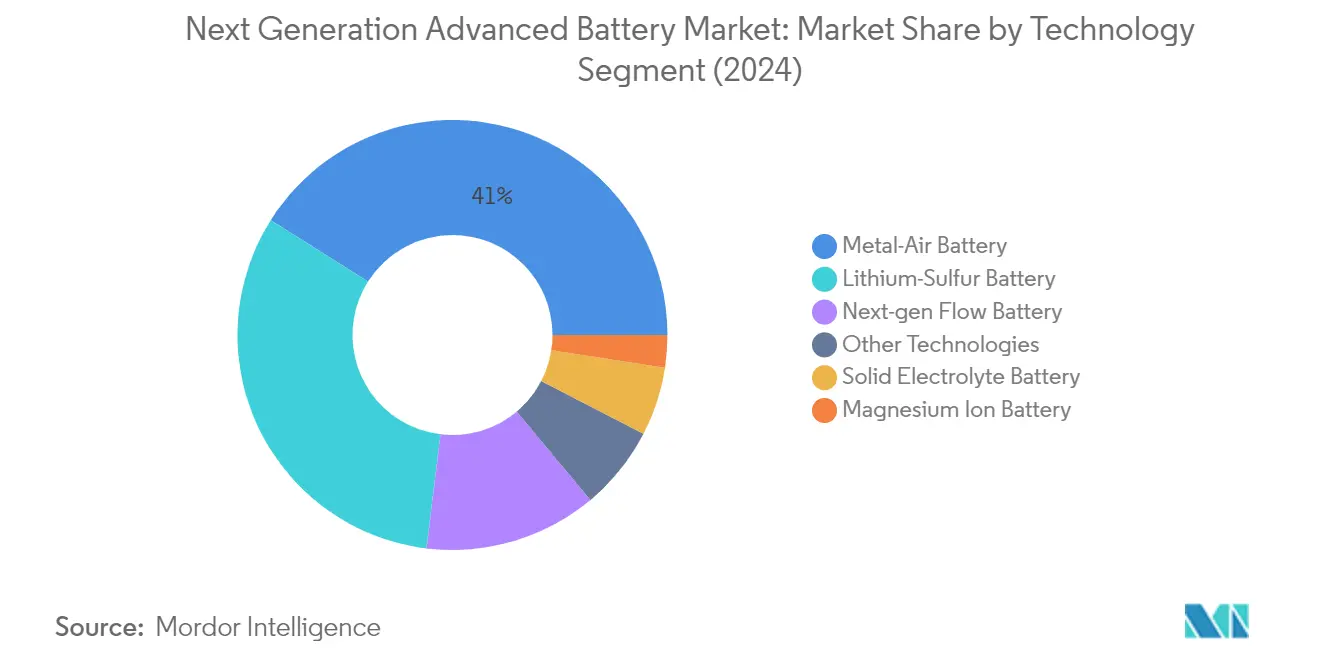

Metal-Air Battery Segment in Next Generation Advanced Battery Market

The metal-air battery segment dominates the next-generation advanced battery market, holding approximately 41% market share in 2024. This significant market position is primarily driven by the segment's superior energy density capabilities and potential applications across various industries. Metal-air batteries, particularly those using metals like zinc and aluminum, have gained substantial traction due to their cost-effectiveness and environmental friendliness. The technology has shown promising results in both stationary energy storage applications and electric vehicle prototypes, with several major manufacturers investing in research and development to overcome current technical challenges such as rechargeability and air electrode stability.

Solid Electrolyte Battery Segment in Next Generation Advanced Battery Market

The solid electrolyte battery segment is emerging as the fastest-growing technology in the next-generation advanced battery market for the period 2024-2029. This remarkable growth is driven by increasing investments from major automotive manufacturers and technology companies in solid-state battery development. The segment's growth is further supported by its superior safety characteristics, higher energy density, and faster charging capabilities compared to conventional lithium-ion batteries. Major automotive manufacturers like Mercedes-Benz and Toyota have announced significant investments in solid-state battery technology, while several technology startups are making breakthrough developments in manufacturing processes and materials.

Remaining Segments in Technology

The other significant segments in the next-generation advanced battery market include lithium-sulfur batteries, next-generation flow batteries, magnesium ion batteries, and various other emerging technologies. Lithium-sulfur batteries have gained attention due to their high theoretical energy density and cost-effectiveness, while next-generation flow batteries are making strides in grid-scale energy storage applications. Magnesium ion batteries represent a promising alternative to lithium-ion technology due to their abundant raw materials and potential for higher energy density. These segments collectively contribute to the diverse technological landscape of the next-generation battery market, each addressing specific market needs and applications.

Segment Analysis: End User

Transportation Segment in Next Generation Advanced Battery Market

The transportation segment dominates the next-generation advanced battery market, commanding approximately 41% market share in 2024. This significant market position is primarily driven by the increasing adoption of electric vehicles (EVs) globally and the growing demand for advanced battery technologies in the automotive sector. Major automotive manufacturers are actively investing in next-generation battery technologies, particularly solid-state batteries and lithium-sulfur batteries, to enhance vehicle performance and range. The segment's dominance is further strengthened by stringent environmental regulations promoting zero-emission vehicles and substantial government initiatives supporting EV adoption across major markets.

Energy Storage Segment in Next Generation Advanced Battery Market

The energy storage segment is emerging as the fastest-growing segment in the next-generation advanced battery market for the period 2024-2029. This remarkable growth is primarily attributed to the increasing integration of renewable energy sources into power grids and the rising demand for efficient advanced energy storage systems. The segment is witnessing significant technological advancements, particularly in flow batteries and solid-state technologies, which offer improved safety, longer lifecycle, and higher energy density compared to conventional batteries. The expansion of utility-scale energy storage projects, coupled with the growing trend of residential and commercial energy storage systems, is further accelerating the segment's growth trajectory.

Remaining Segments in End User Segmentation

The industrial, consumer electronics, and other end users segments collectively play vital roles in shaping the next-generation advanced battery market. The industrial segment is particularly significant in applications such as uninterrupted power supply systems and industrial automation. The consumer electronics segment focuses on developing high-density batteries for portable devices and wearable technology. The other end users segment, which includes medical devices and aerospace applications, contributes to market diversification through specialized battery requirements and innovative applications. These segments continue to drive innovation in battery technology, particularly in areas requiring specific performance characteristics such as miniaturization, safety, and reliability.

Next Generation Advanced Battery Market Geography Segment Analysis

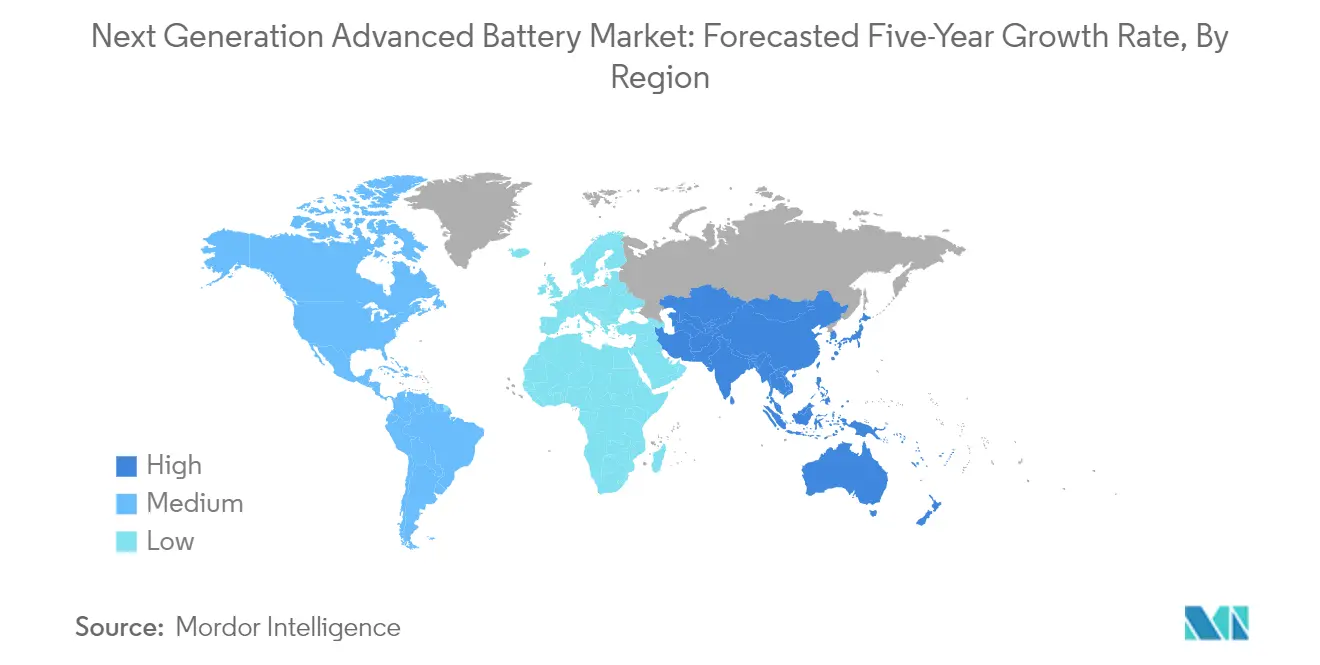

Next Generation Advanced Battery Market in North America

North America represents a significant hub for next-generation battery technology development, commanding approximately 23% of the global market share in 2024. The region's prominence is driven by substantial investments in renewable energy infrastructure and the growing adoption of electric vehicles. The United States leads the regional market with extensive research and development activities in solid-state battery market, lithium-sulfur battery market technologies, and other advanced battery chemistries. The region benefits from a robust ecosystem of battery manufacturers, research institutions, and automotive companies collaborating to advance battery technology. Government support through research grants and environmental policies has created a favorable environment for innovation in battery technology. The presence of major players and strategic partnerships between automotive manufacturers and battery developers has accelerated the commercialization of next-generation batteries. Additionally, the increasing focus on grid-scale energy storage solutions and the transition toward renewable energy sources continues to drive market growth in the region.

Next Generation Advanced Battery Market in Asia-Pacific

Asia-Pacific stands as the largest market for next-generation advanced batteries, demonstrating a robust growth rate of approximately 5% from 2019 to 2024. The region's dominance is primarily attributed to the strong presence of major battery manufacturers and extensive research activities in countries like China, Japan, and South Korea. These nations have established themselves as global leaders in battery technology innovation and production capabilities. The region benefits from advanced manufacturing infrastructure, strong government support for clean energy initiatives, and increasing investments in electric vehicle production. The presence of major automotive manufacturers and their growing focus on electric vehicle development has created substantial demand for advanced battery technologies. Furthermore, the region's commitment to renewable energy integration and grid modernization has spurred the adoption of advanced energy storage solutions, including the sodium-ion battery market. The combination of technological expertise, manufacturing capabilities, and supportive government policies continues to strengthen Asia-Pacific's position in the global market.

Next Generation Advanced Battery Market in Europe

Europe demonstrates strong market potential with an expected growth rate of approximately 7% during the forecast period 2024-2029. The region's market is characterized by aggressive environmental policies and substantial investments in sustainable energy solutions. European countries have shown strong commitment to electric vehicle adoption and renewable energy integration, driving the demand for advanced battery technologies. The presence of major automotive manufacturers and their transition towards electric vehicle production has created a robust ecosystem for battery innovation. The European Battery Alliance and various research initiatives have fostered collaboration between industry players, research institutions, and governments. The region's focus on developing a sustainable battery value chain, from raw materials to recycling, has created a comprehensive framework for market growth. Additionally, the increasing emphasis on energy independence and grid modernization continues to drive investments in the advanced energy storage market.

Next Generation Advanced Battery Market in South America

South America represents an emerging market for next-generation advanced batteries, with significant potential for growth in the coming years. The region's market is primarily driven by increasing adoption of electric vehicles and growing investments in renewable energy infrastructure. Countries like Brazil and Argentina are taking strategic steps to develop their battery technology capabilities, leveraging their natural resources, particularly lithium reserves. The region has witnessed increasing collaboration between international battery manufacturers and local institutions to develop advanced battery technologies. Government initiatives promoting clean energy adoption and sustainable transportation solutions have created a favorable environment for market growth. The growing focus on grid modernization and energy storage solutions, including the flow battery market, has opened new opportunities for advanced battery technologies. Additionally, the region's industrial sector's increasing demand for reliable energy storage solutions continues to drive market development.

Next Generation Advanced Battery Market in Middle East & Africa

The Middle East & Africa region shows promising potential in the next-generation advanced battery market, driven by increasing investments in renewable energy projects and sustainable development initiatives. The region's market is characterized by growing awareness of clean energy solutions and the need for advanced energy storage systems. Countries in the region are actively diversifying their energy portfolios and investing in sustainable technologies, creating opportunities for advanced battery solutions. The increasing focus on smart city development and grid modernization projects has stimulated demand for innovative energy storage solutions. The transportation sector's gradual shift towards electric vehicles, particularly in urban areas, has created new opportunities for advanced battery technologies. Furthermore, the region's industrial sector's growing need for reliable power solutions has expanded the application scope for next-generation batteries. The combination of government initiatives, private sector investments, and increasing environmental awareness continues to drive market development in the region. The metal-air battery market is also gaining traction as part of these advancements.

Get Analysis on Important Geographic Markets

Download PDF

Next Generation Advanced Battery Industry Overview

Top Companies in Next Generation Advanced Battery Market

The next generation advanced battery market features established players like Contemporary Amperex Technology (CATL), GS Yuasa Corporation, Johnson Matthey, LG Energy Solution, and Ilika PLC leading innovation efforts. Companies are heavily investing in research and development of novel technologies like solid-state battery industry, lithium-sulfur batteries, and other advanced battery technology chemistries to achieve higher energy densities and improved safety profiles. Strategic collaborations between battery manufacturers and automotive companies have become increasingly common to accelerate commercialization timelines. Manufacturing capacity expansion, particularly in Europe and Asia, demonstrates the industry's commitment to scaling production capabilities. Companies are also focusing on developing specialized solutions for different applications ranging from electric vehicles to advanced energy storage system market, while simultaneously working on improving the sustainability and cost-effectiveness of their battery technologies.

Dynamic Market with Strong Growth Potential

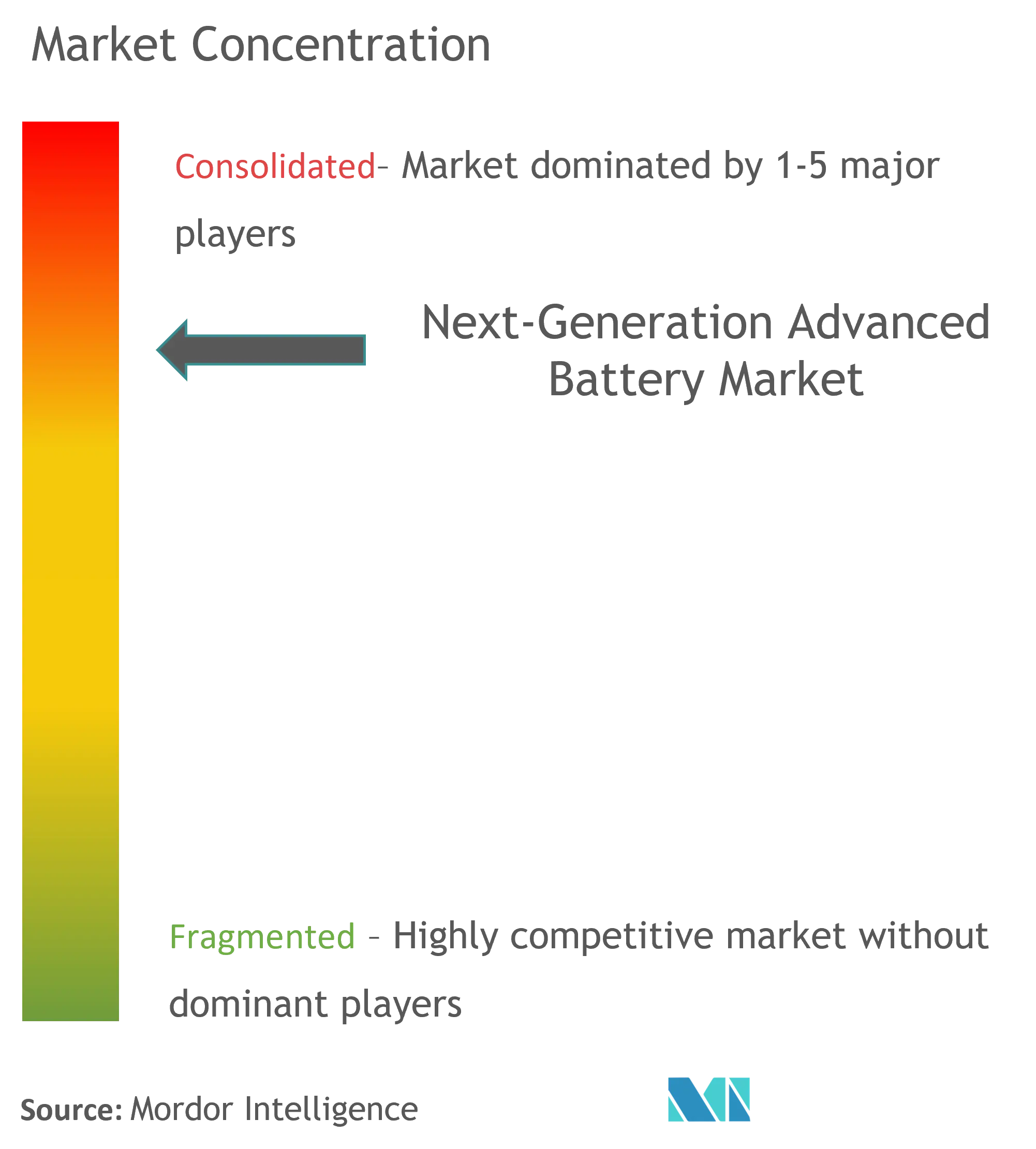

The next generation advanced battery market exhibits a mix of large conglomerates and specialized technology companies, with Asian manufacturers, particularly from China, Japan, and South Korea, maintaining a strong presence. Market consolidation is occurring through strategic acquisitions and partnerships, as evidenced by deals like Britishvolt's acquisition of EAS and Johnson Matthey's purchase of Oxis Energy's assets. These moves indicate a trend toward vertical integration and technology portfolio expansion. The competitive landscape is characterized by significant barriers to entry due to high capital requirements, complex manufacturing processes, and the need for extensive research and development capabilities.

The industry is witnessing increased collaboration between established battery manufacturers and automotive OEMs, research institutions, and technology startups. Companies are forming joint ventures and strategic alliances to share development costs and reduce time-to-market for new battery technologies. The market structure is evolving from a traditionally fragmented landscape to one with more consolidated players who can leverage economies of scale and comprehensive technology portfolios. This transformation is particularly evident in the solid-state battery industry segment, where major players are making substantial investments in research and manufacturing capabilities.

Innovation and Scale Drive Market Success

Success in the next generation advanced battery market requires a balanced approach combining technological innovation with manufacturing scalability. Incumbent players must continue investing in research and development while simultaneously expanding their production capabilities to maintain their competitive edge. Strategic partnerships with automotive manufacturers and energy storage system developers are becoming increasingly crucial for securing long-term market positions. Companies need to focus on developing differentiated products that address specific application requirements while maintaining cost competitiveness through operational efficiency and supply chain optimization.

For new entrants and smaller players, specialization in specific battery technologies or applications offers a pathway to market success. The development of unique intellectual property and novel manufacturing processes can help overcome entry barriers and attract strategic partnerships or investment. Companies must also carefully navigate regulatory requirements, particularly regarding safety standards and environmental compliance. The ability to demonstrate superior performance metrics, such as energy density, charging speed, and cycle life, while maintaining competitive pricing will be critical for gaining market share. Additionally, establishing robust supply chains and securing access to critical raw materials will become increasingly important as the market expands, especially in the context of post-lithium-ion battery advancements.

Next Generation Advanced Battery Market Leaders

-

Contemporary Amperex Technology Co Ltd

-

PolyPlus Battery Co Inc.

-

GS Yuasa Corporation

-

Ilika PLC

-

Johnson Matthey PLC

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Next Generation Advanced Battery Market News

- In February 2022, the US Department of Energy announced that it would provide USD 2.91 billion to boost the production of advanced batteries used in stationary energy storage systems and electric vehicles, as directed by the Bipartisan Infrastructure Law.

- In January 2022, Mercedes-Benz and ProLogium signed a technology cooperation agreement to develop next-generation battery cells. Mercedes Benz plans to go all-electric by 2030. With its solid-state battery R&D and manufacturing know-how, ProLogium is likely to be a strong partner for Mercedes Benz.

Next Generation Advanced Battery Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Technology

- 5.1.1 Solid Electrolyte Battery

- 5.1.2 Magnesium Ion Battery

- 5.1.3 Next-generation Flow Battery

- 5.1.4 Metal-Air Battery

- 5.1.5 Lithium-Sulfur Battery

- 5.1.6 Other Technologies

-

5.2 End User

- 5.2.1 Consumer Electronics

- 5.2.2 Transportation

- 5.2.3 Industrial

- 5.2.4 Energy Storage

- 5.2.5 Other End Users

-

5.3 Geography

- 5.3.1 North America

- 5.3.2 Asia-Pacific

- 5.3.3 Europe

- 5.3.4 South America

- 5.3.5 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Pathion Holding Inc.

- 6.3.2 GS Yuasa Corporation

- 6.3.3 Johnson Matthey PLC

- 6.3.4 PolyPlus Battery Co. Inc.

- 6.3.5 Ilika PLC

- 6.3.6 Sion Power Corporation

- 6.3.7 LG Chem Ltd

- 6.3.8 Saft Groupe SA

- 6.3.9 Contemporary Amperex Technology Co. Ltd

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Next Generation Advanced Battery Industry Segmentation

The advanced next-generation batteries are the upgraded version of existing batteries that have higher efficiency and cheaper unit cost. The Next-Generation advanced battery market is segmented by technology, end user, and geography. By technology, the market is segmented into solid electrolyte battery, magnesium ion battery, next-generation flow battery, metal-air battery, lithium-sulfur batteries, and other technologies. By end user, the market is segmented into consumer electronics, transportation, industrial, energy storage, other end users. The report also covers the market size and forecasts for the solar PV inverters market across major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD million).

| Technology | Solid Electrolyte Battery |

| Magnesium Ion Battery | |

| Next-generation Flow Battery | |

| Metal-Air Battery | |

| Lithium-Sulfur Battery | |

| Other Technologies | |

| End User | Consumer Electronics |

| Transportation | |

| Industrial | |

| Energy Storage | |

| Other End Users | |

| Geography | North America |

| Asia-Pacific | |

| Europe | |

| South America | |

| Middle-East and Africa |

Need A Different Region or Segment?

Customize Now

Next Generation Advanced Battery Market Research FAQs

How big is the Next Generation Advanced Battery Market?

The Next Generation Advanced Battery Market size is expected to reach USD 2.01 billion in 2025 and grow at a CAGR of 7.24% to reach USD 2.84 billion by 2030.

What is the current Next Generation Advanced Battery Market size?

In 2025, the Next Generation Advanced Battery Market size is expected to reach USD 2.01 billion.

Who are the key players in Next Generation Advanced Battery Market?

Contemporary Amperex Technology Co Ltd, PolyPlus Battery Co Inc., GS Yuasa Corporation, Ilika PLC and Johnson Matthey PLC are the major companies operating in the Next Generation Advanced Battery Market.

Which is the fastest growing region in Next Generation Advanced Battery Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Next Generation Advanced Battery Market?

In 2025, the Asia-Pacific accounts for the largest market share in Next Generation Advanced Battery Market.

What years does this Next Generation Advanced Battery Market cover, and what was the market size in 2024?

In 2024, the Next Generation Advanced Battery Market size was estimated at USD 1.86 billion. The report covers the Next Generation Advanced Battery Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Next Generation Advanced Battery Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Next Generation Advanced Battery Market Research

Mordor Intelligence delivers a comprehensive analysis of the next generation energy storage sector. We specialize in emerging technologies, including solid state battery development, sodium ion battery innovations, and flow battery systems. Our extensive research covers breakthrough developments in advanced battery technology. These range from quantum battery concepts to metal air battery solutions. The report PDF is available for immediate download, offering detailed insights into future battery technology trends and advanced automotive battery applications. This is supported by our proven consulting expertise in advanced energy storage markets.

Our analysis encompasses critical developments in lithium sulfur battery technology, advanced lithium battery systems, and emerging post lithium ion battery solutions. The report examines future energy storage possibilities. It includes a detailed analysis of the solid state battery market, sodium ion battery market, and flow battery market dynamics. Stakeholders gain valuable insights into advanced energy storage system implementations. We provide comprehensive coverage of metal air battery market developments and new generation battery innovations. The research offers actionable intelligence on advanced energy storage market trends, enabling informed decision-making across the solid state battery industry landscape.