Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.16 Billion |

| Market Size (2031) | USD 4.26 Billion |

| Growth Rate (2026 - 2031) | 6.17% CAGR |

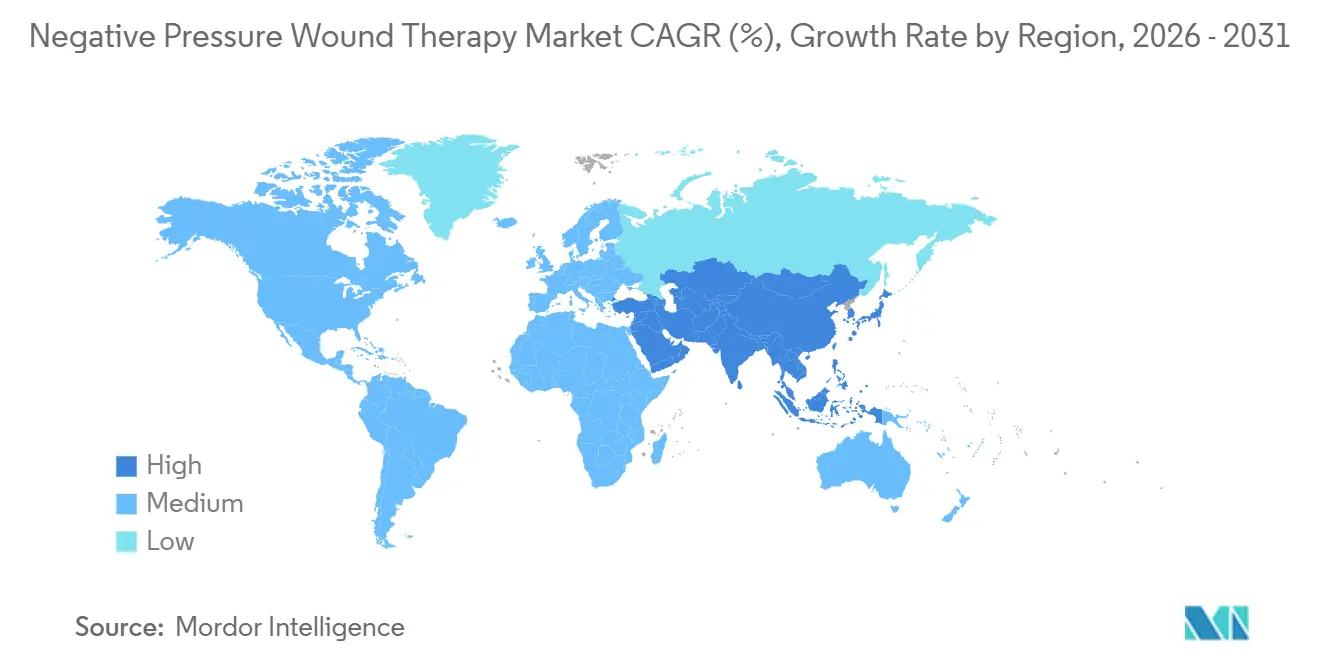

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Negative Pressure Wound Therapy Market Analysis by Mordor Intelligence

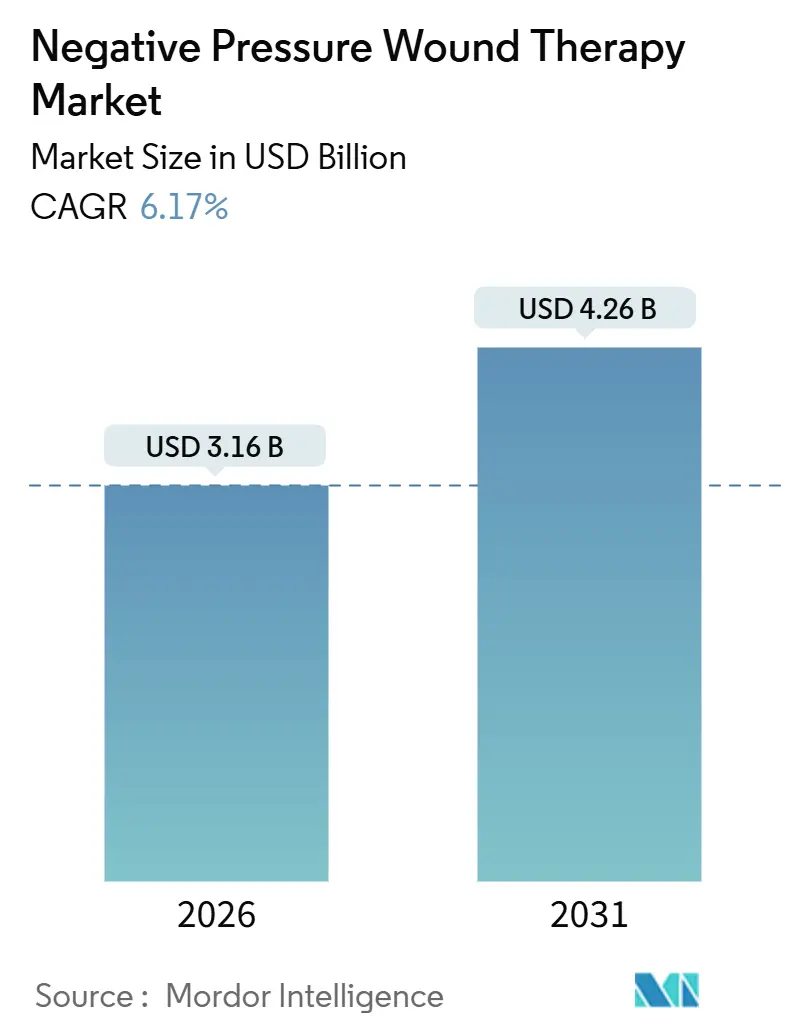

The negative pressure wound therapy market size stands at USD 3.16 billion in 2026 and is projected to reach USD 4.26 billion by 2031, advancing at a 6.17% CAGR. Device miniaturization, broader reimbursement, and integration of digital monitoring turn what was once an inpatient therapy into a home-care staple, while rising diabetic-foot and venous-leg ulcer prevalence keeps overall demand on an upward trajectory. Portable single-use pumps that operate for seven days on one charge appeal to ambulatory surgical centers keen to avoid cross-contamination, and the same design helps humanitarian teams stabilize complex wounds during evacuation. North America remains the revenue anchor thanks to Medicare’s refined coverage for high-risk incisions, yet Asia-Pacific delivers the fastest incremental growth as China and India fund rural wound-care programs. Competitive focus has shifted from price cuts to data capture, with smart pumps that transmit pressure consistency and exudate volume now winning hospital tenders.[1]Centers for Medicare & Medicaid Services, “Local Coverage Determination (LCD) L33821,” cms.gov

Key Report Takeaways

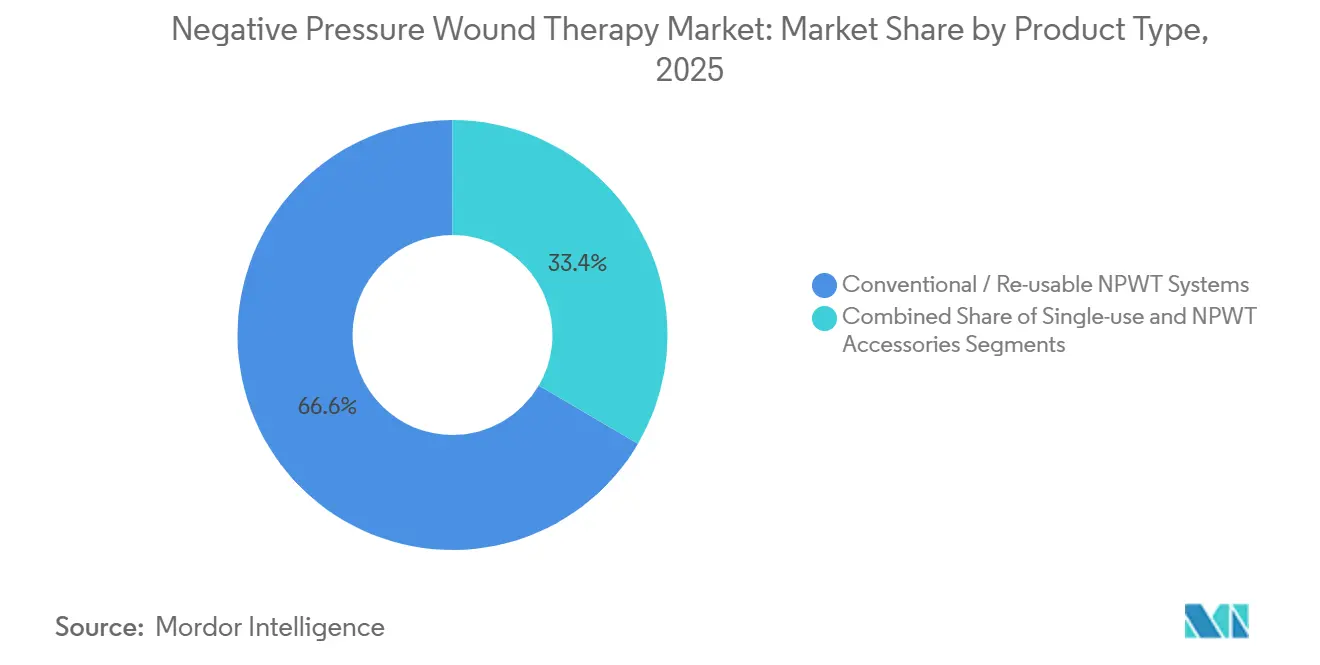

- By product type, conventional reusable systems held 66.56% of negative pressure wound therapy market share in 2025, while single-use systems are forecast to grow at a 9.62% CAGR to 2031.

- By mode of delivery, portable pumps led with 58.63% share in 2025 and are projected to expand at a 9.13% CAGR through 2031.

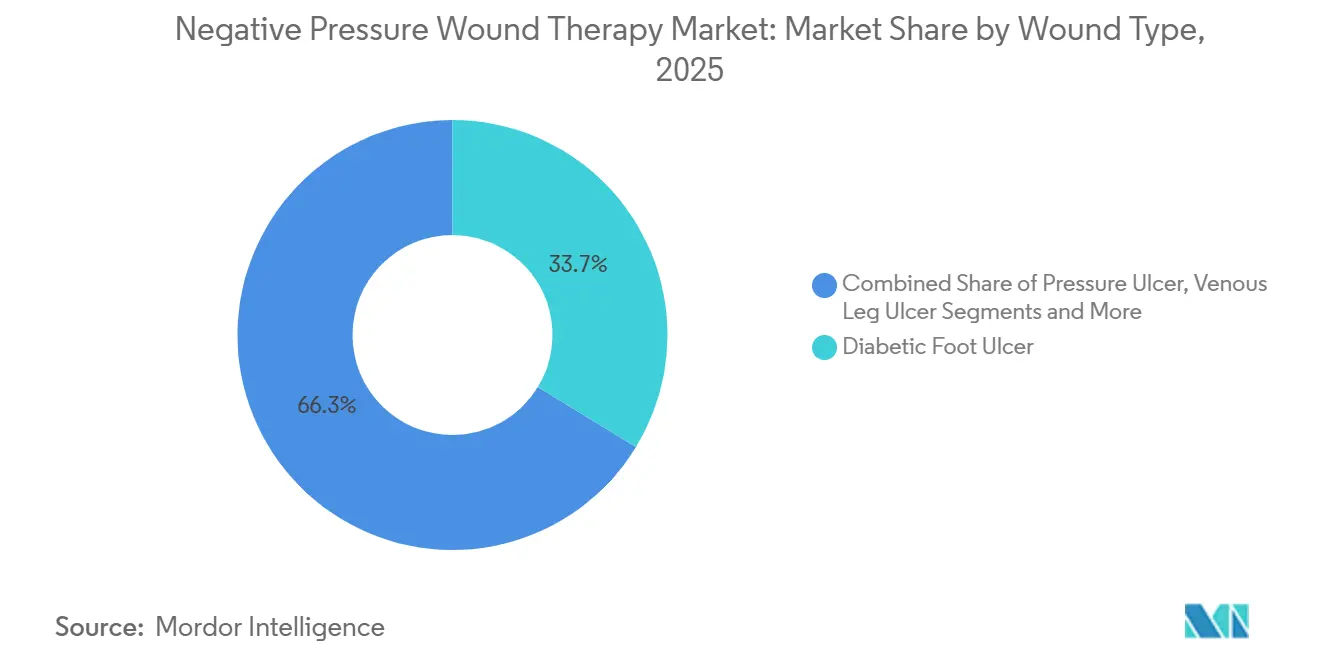

- By wound type, diabetic foot ulcers captured 33.72% share of the negative pressure wound therapy market size in 2025, whereas burn wounds are set to post the fastest 8.45% CAGR between 2026 and 2031.

- By end user, hospitals accounted for 53.81% of revenue in 2025, while home-care settings are advancing at a 10.64% CAGR to 2031.

- By geography, North America commanded 39.61% share in 2025; Asia-Pacific records the highest projected 8.72% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Negative Pressure Wound Therapy Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing incidence of traumatic & chronic wounds | +1.4% | Global with focus on North America and EU-5 | Medium term (2-4 years) |

| Growing diabetic-foot & venous-leg ulcer prevalence | +1.6% | Global, strongest in India, China, and the Middle East | Long term (≥ 4 years) |

| Continuous technological innovation in NPWT pumps | +1.1% | North America and core EU, spill-over to APAC urban centers | Short term (≤ 2 years) |

| Wider reimbursement in the U.S. & EU-5 | +0.9% | North America and Western Europe | Medium term (2-4 years) |

| Integration with digital wound-monitoring platforms | +0.7% | North America, Germany, and the UK | Short term (≤ 2 years) |

| Humanitarian & military field adoption surge | +0.5% | Conflict zones and disaster-prone regions worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Incidence of Traumatic & Chronic Wounds

Road traffic injuries kill 1.35 million people every year, and survivors often present with complex soft-tissue trauma that heals faster under consistent negative pressure.[2]World Health Organization, “Road Traffic Injuries Key Facts,” who.intPressure ulcers affect up to 3 million U.S. residents yearly and create a USD 20 billion cost burden that payers aim to cut with early NPWT deployment. Populations over 65 now make up a growing share of OECD countries, and impaired healing in this cohort pushes clinicians toward therapies that accelerate granulation. Surgical site infections appear in 2%-5% of inpatient procedures, convincing surgeons to apply prophylactic negative pressure to clean, closed incisions after the FDA expanded labeling in 2024. Trauma centers in Ukraine and Gaza documented a 40% rise in complex extremity wounds during 2024, and field surgeons routinely requested portable NPWT units to avoid secondary amputations.

Growing Diabetic-Foot & Venous-Leg Ulcer Prevalence

The International Diabetes Federation counted 537 million adults living with diabetes in 2024, and an estimated 6.3% suffered at least one foot ulcer.[3]International Diabetes Federation, “IDF Diabetes Atlas 10th Edition,” idf.orgRecurrence rates reach 40% within one year and 65% within five, turning each patient into a repeat consumer of dressings and pumps. Venous leg ulcers occur in 1% of adults in developed economies and respond well to NPWT when compression therapy alone fails. Amputations tied to diabetes rose 15% in the United States between 2020 and 2024, prompting wider Medicare coverage for home-care negative pressure applications. India’s national non-communicable disease program earmarked USD 150 million in 2024 to subsidize NPWT consumables in public hospitals, signaling long-term demand growth.

Continuous Technological Innovation in NPWT Pumps

Smith & Nephew’s 100-gram PICO system lets patients remain mobile and cut hospital stay by 2.3 days on average. Real-time pressure sensors issue alerts when therapeutic levels drop below −80 mmHg, preventing unnoticed interruptions. Solventum’s Prevena Restor, cleared in 2024, integrates antimicrobial dressings that release silver ions, lowering infection risk to below 3%. Lithium-ion batteries now power pumps for up to ten days, a leap from the 48-hour ceiling common five years ago. Canister-free single-use devices absorb exudate into superabsorbent polymers and trim episode costs up to 40% compared with reusable kits that require sterilization.

Wider Reimbursement in the U.S. & EU-5

Medicare’s LCD L33821 revision in 2024 extended coverage to high-risk incisions, doubling the pool of eligible patients without imposing new cost ceilings. Private insurers quickly mirrored the change, which moved wound management from inpatient to outpatient sites. Germany’s Federal Joint Committee authorized home-care reimbursement tied to weekly teleconsults, creating a playbook that France and Italy still assess. Reimbursement per week averages USD 150 under Medicare but can exceed USD 300 in commercial plans, leaving room for manufacturers to bundle consumables profitably. Policy inertia in southern Europe keeps hospital utilization dominant, yet competitive pressure may force harmonization.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High device & therapy costs | −0.8% | Emerging markets in APAC, Latin America, and MEA | Long term (≥ 4 years) |

| Procedural complications (bleeding, infection) | −0.5% | Global, higher risk in resource-limited settings | Medium term (2-4 years) |

| Uncertain reimbursement for single-use systems | −0.4% | India, Brazil, South Africa | Medium term (2-4 years) |

| Disposal regulations for NPWT waste | −0.3% | EU and select U.S. states such as California and New York | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Device & Therapy Costs

Capital prices for reusable pumps range from USD 8,000 to USD 15,000, and four weeks of disposables can add USD 2,500, a sum that exceeds annual health spending per capita in many low-income countries. Leasing contracts ease capital outlay but lock hospitals into single-vendor ecosystems for up to five years. Single-use kits cost USD 400-800 each and remain unaffordable for self-pay patients in rural India even after subsidies. Cost-effectiveness studies show a 20% episode-of-care saving when NPWT replaces extended inpatient treatment, but hospitals rarely capture that benefit directly.

Procedural Complications (Bleeding, Infection)

A 2024 Journal of Wound Care study covering 1,200 patients reported a 3.2% bleeding rate rising to 7% in post-cardiac surgery cases. The FDA’s MAUDE database listed 142 adverse events tied to negative pressure units in the same year, including 18 foam fragment retentions that required surgical retrieval. Pain scores of 6-8 during dressing removal push 12% of home-care patients to discontinue therapy prematurely. Better clinician training and advanced dressings that incorporate antimicrobial layers help mitigate, but risk perception still slows adoption in risk-averse facilities.

Segment Analysis

By Product Type: Disposables Gain on Infection Control

Reusable pumps retained 66.56% share of the negative pressure wound therapy market in 2025, favored by hospitals that amortize capital over seven years and value adjustable pressure settings. Single-use disposables are on course for a 9.62% CAGR to 2031 as ambulatory surgical centers elevate infection-control protocols. These facilities like the fact that every kit arrives sterile and leaves with the patient, eliminating re-processing. Accessories such as dressings, drapes, and canisters form a steady consumable stream that shields revenue when capital budgets tighten. Proprietary connectors ensure brand loyalty because rival dressings will not fit the pump head. Disposables flourish where payers cover the higher per-episode cost to avoid cross-contamination claims, a trend most apparent in the United States.

Reusable platforms stay relevant in trauma centers that cycle one pump across multiple high-exudate wounds each day, keeping per-patient costs low. Competition intensifies as smaller firms leverage the FDA’s 510(k) route to launch niche devices within nine months, undercutting multinationals on price without sacrificing core functionality. The negative pressure wound therapy industry now watches whether European payers will follow U.S. malpractice trends that favor disposables despite the waste burden.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Mode of Delivery: Portability Unlocks Home Discharge

Portable devices captured 58.63% of delivery-mode revenue in 2025 and aim for a 9.13% CAGR through 2031 as payers shift costs from hospital beds to home settings. Weighing under 500 grams and running silently at 45 decibels, modern pumps permit patients to sleep comfortably and walk freely, which improves compliance. Battery endurance of up to ten days reduces caregiver visits for recharging.

Stationary pumps remain indispensable in intensive care units where wound exudate can exceed 200 mL per hour and instillation cycles demand precise fluid management. Medicare reimburses both modes equally, but commercial insurers often require portable systems for post-discharge coverage. Manufacturers differentiate on alarm logic and cloud connectivity rather than suction power, signaling that software now drives procurement. Portable pumps therefore set the tone for home-care business models, while stationary units find a stable niche in high-acuity wards. The negative pressure wound therapy market now hinges on whether remote monitoring can convince lagging payers that home care delivers outcomes equal to inpatient treatment.

By Wound Type: Burn Wounds Surge on Field Protocols

Diabetic foot ulcers represented 33.72% share in 2025, reflecting the global diabetes burden. Burn cases will grow fastest at 8.45% CAGR as military guidelines and humanitarian protocols name NPWT first-line therapy for injuries exceeding 20% surface area.

Pressure ulcers and venous leg ulcers account for consistent, longer-duration revenue streams but show slower unit growth because preventive pressure-redistribution surfaces are improving. Traumatic and surgical wounds form a diverse group that values NPWT’s flexibility across varying depths and contamination levels. Burn-focused pumps that handle high moisture vapor and temperature fluctuations emerge as a distinct sub-segment. Providers appreciate that negative pressure wound therapy market size for burn care can expand without cannibalizing diabetic-foot share because demand drivers differ. Clinical endorsements continue to substitute anecdotal evidence, moving burned tissue treatment from optional to standard practice across both military and civilian protocols. The negative pressure wound therapy industry hence sees burn care as the next frontline application.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Home Care Outpaces Hospitals

Hospitals still controlled 53.81% of revenue in 2025, but home-care agencies register the fastest 10.64% CAGR to 2031. Early discharge reduces daily costs from USD 2,000 to USD 200 and frees capacity for higher-acuity admissions. Journal of the American College of Surgeons data show an 18% lower readmission rate when post-operative wounds are managed with home-based NPWT.

Ambulatory surgical centers adopt single-use kits to avoid sterilization overhead and potential cross-contamination litigation. Long-term care facilities deploy NPWT selectively for severe pressure ulcers, reserving pumps for cases where faster closure justifies expense. Home-care expansion depends on device logistics, patient education, and telemonitoring reimbursement; turnkey supplier programs now bundle all three to secure exclusivity agreements. The segment’s trajectory suggests that negative pressure wound therapy market share will keep tilting toward community settings as remote monitoring evidence accumulates. Large health systems must therefore align surgical discharge protocols with payer policies to avoid revenue loss while still meeting quality benchmarks.

Geography Analysis

North America contributed 39.61% of global revenue in 2025, anchored by predictable Medicare rules and brisk FDA clearance cycles that encourage product refreshes every two years. The 2024 expansion of LCD L33821 to high-risk incisions swelled the eligible patient base overnight. Canada lags the United States because provincial funding differs; Ontario reimburses home-care NPWT, but Alberta confines coverage to inpatient use. Mexico’s private hospitals attract medical tourists from the United States, boosting imports of portable pumps that meet Joint Commission standards. Rural North American regions still see patchy access, and the Indian Health Service only started funding NPWT units for tribal facilities in 2024, indicating room for growth.

Europe’s uptake remains uneven. Germany reimburses home use provided weekly teleconsults document progress, driving the region’s highest per-capita utilization. The UK’s NHS lists NPWT on its formulary but restricts indications through local commissioning groups. France demands prior authorization, which delays therapy initiation by weeks. Italy and Spain face fiscal constraints and reserve NPWT for teaching hospitals. EU Regulation 2017/745 raised compliance costs, causing smaller domestic suppliers to exit and concentrate share with multinationals, which could reshape competitive dynamics if reimbursement harmonizes.

Asia-Pacific posts the swiftest 8.72% CAGR to 2031. China’s Healthy China 2030 program funds county-level wound-care clinics, while India’s National Health Mission subsidizes consumables in 150 district hospitals. Japan’s elderly population would support demand, yet low reimbursement rates slow adoption outside university centers. South Korea broadened coverage to post-operative wounds in 2024 and saw device sales jump 35% year on year. Australia reimburses consumables but not pumps, leading hospitals to favor reusable models. Southeast Asian countries such as Indonesia rely on humanitarian donations, showing latent potential once payer frameworks mature.

South America’s growth is led by Brazil, where private insurers reimburse NPWT, but SUS still excludes single-use kits, splitting the market. Argentina’s inflation deters importers, limiting access to high-margin private clinics. Chile added NPWT for diabetic-foot ulcers under FONASA in 2024, but budget strain limits rollout. Currency stability and domestic production approvals, like ANVISA’s 2024 nod for Brazilian-made consumables, will determine whether the region moves from niche to mainstream adoption.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Smith & Nephew, Solventum, and Mölnlycke combine for roughly half share, yet the negative pressure wound therapy market remains open to niche entrants. Incumbents lock customers into proprietary consumables that require specific connectors or dressings, ensuring recurring income even after capital sales plateau.

New players exploit the faster 510(k) route to release lighter pumps with novel form factors, such as Genadyne’s 150-gram wearable device. ConvaTec’s 2024 purchase of the Avelle portfolio shows strategic pivot toward single-use kits ahead of anticipated infection-control mandates. Product differentiation now rests on embedded sensors and analytics dashboards rather than suction capacity. Solventum filed a 2024 patent for multi-lumen dressings with pressure transducers, signaling continued investment in data-rich disposables. Supply-chain resilience also matters; Mölnlycke’s European manufacturing footprint gives hospitals a hedge against trans-Pacific shipping delays. Moderate concentration allows regional specialists to thrive, though reimbursement-driven price compression may accelerate consolidation.

Negative Pressure Wound Therapy Industry Leaders

ConvaTec Inc.

Smith & Nephew plc

Mölnlycke Health Care AB

Solventum

Medela AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: New Horizon Medical Solutions acquired Applied Tissue Technologies, adding a transparent NPWT device and micro-grafting kit to its wound-care portfolio.

- December 2025: Solventum completed the acquisition of Acera Surgical, expanding its offering with fully engineered regenerative materials.

- December 2025: An international panel released consensus guidelines on closed-incision NPWT with reticulated open-cell foam dressings, underscoring unique features of Solventum’s Prevena system.

- October 2025: Cork Medical introduced the Nisus One NPWT pump, designed to simplify workflows and lower costs across hospital, long-term care, and home-care environments.

Global Negative Pressure Wound Therapy Market Report Scope

As per the scope of the report, negative-pressure wound therapy (NPWT) is a therapeutic technique that uses a suction dressing to remove excess exudate and promote healing in acute or chronic wounds and second and third-degree burns.

The Negative Pressure Wound Therapy Market is segmented by Product Type, Mode of delivery, wound type, end user, and geography. By Product Type, the market is segmented by Conventional/Re-usable Systems, Single-use/Disposable Systems, and Accessories. By Mode of Delivery, the market is segmented into Portable and Stand-alone/Stationary. By Wound Type, the market is segmented by Diabetic Foot Ulcer, Pressure Ulcer, Venous Leg Ulcer, Burn Wounds, Traumatic & Surgical Wounds, Other. By End User, the market is segmented into Hospitals, Ambulatory Surgical Centers, Home-care, and Other. By Geography, the market is segmented into North America, Europe, Asia-Pacific, MEA, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

By Product Type

| Conventional / Re-usable NPWT Systems | |

| Single-use / Disposable NPWT Systems | |

| NPWT Accessories | Canisters |

| Dressings & Drapes | |

| Tubing & Connectors |

By Mode of Delivery

| Portable Systems |

| Stand-alone / Stationary Systems |

By Wound Type

| Diabetic Foot Ulcer |

| Pressure Ulcer |

| Venous Leg Ulcer |

| Burn Wounds |

| Traumatic & Surgical Wounds |

| Other Wound Types |

By End User

| Hospitals |

| Ambulatory Surgical Centers |

| Home-care Settings |

| Other End Users |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Conventional / Re-usable NPWT Systems | |

| Single-use / Disposable NPWT Systems | ||

| NPWT Accessories | Canisters | |

| Dressings & Drapes | ||

| Tubing & Connectors | ||

| By Mode of Delivery | Portable Systems | |

| Stand-alone / Stationary Systems | ||

| By Wound Type | Diabetic Foot Ulcer | |

| Pressure Ulcer | ||

| Venous Leg Ulcer | ||

| Burn Wounds | ||

| Traumatic & Surgical Wounds | ||

| Other Wound Types | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Home-care Settings | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the projected value of the negative pressure wound therapy market in 2031?

The market is expected to reach USD 4.26 billion by 2031, reflecting a 6.17% CAGR from 2026.

Which product segment is growing fastest within negative pressure wound therapy?

Single-use disposable systems are forecast to expand at a 9.62% CAGR as surgical centers prioritize infection control.

Why are portable NPWT pumps gaining share?

Advances in battery life and weight reduction enable safe home discharge, lowering daily treatment costs from USD 2,000 to USD 200.

How does reimbursement affect adoption in emerging markets?

Limited or delayed funding for single-use devices in India, Brazil, and South Africa slows uptake despite clinical need.

Which wound type shows the highest growth outlook?

Burn wounds carry the highest 8.45% CAGR because military and humanitarian protocols now list NPWT as first-line therapy.

What digital features are most valued in modern NPWT pumps?

Real-time pressure monitoring and cloud-based adherence reports help providers meet value-based care metrics while reducing complications.