| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| Market Size (2025) | USD 8.91 Billion |

| Market Size (2030) | USD 30.03 Billion |

| CAGR (2025 - 2030) | 27.50 % |

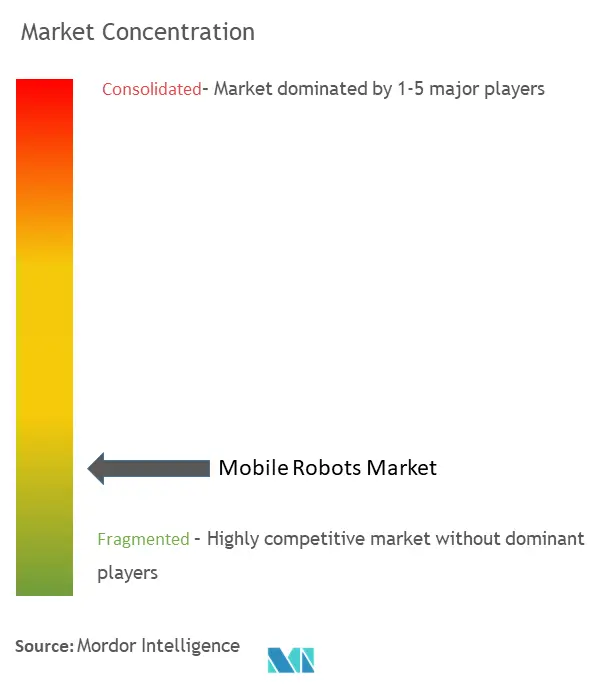

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Mobile Robots Market Analysis

The Mobile Robots Market size is estimated at USD 8.91 billion in 2025, and is expected to reach USD 30.03 billion by 2030, at a CAGR of 27.5% during the forecast period (2025-2030).

The mobile robotics industry is experiencing rapid transformation driven by advancing automation technologies and Industry 4.0 initiatives. Manufacturing facilities worldwide are increasingly adopting sophisticated industrial mobile robots solutions, with South Korea leading global robot density at 1,000 robots per 10,000 employees in the manufacturing sector, followed by Singapore at 670 and Japan at 399. The integration of artificial intelligence, automation, the Internet of Things, and enhanced computing power is enabling the development of next-generation smart factories. These technological convergences are revolutionizing traditional manufacturing processes, allowing for more flexible and efficient production systems while significantly reducing operational complexities.

Navigation technology for mobile robots has evolved substantially, with manufacturers implementing various sophisticated solutions to enhance autonomous operation capabilities. The industry has witnessed a shift from traditional guidance systems to more advanced technologies, with LiDAR sensors commanding a 30.3% market share due to their superior 3D sensing capabilities and ability to operate in challenging lighting conditions. The emergence of hybrid navigation systems, combining cameras with LiDAR technology, is providing enhanced operational accuracy and reliability, enabling autonomous mobile robots to navigate complex warehouse environments more effectively while ensuring safer human-robot collaboration.

Port automation and container handling have emerged as significant growth areas for mobile robots, particularly in seaport terminals where efficiency is paramount. The increasing globalization of trade and rising container volumes have made automated guided vehicles (AGVs) essential for maintaining a competitive advantage in port operations. These unmanned vehicles are revolutionizing container transport between ships and storage locations, significantly reducing vessel dwell time and enhancing operational efficiency. The integration of sophisticated fleet management systems is enabling coordinated movement of multiple robots, optimizing container handling operations and reducing logistical bottlenecks.

The industry is witnessing a significant technological shift with the impending widespread deployment of 5G networks, which is expected to revolutionize mobile robot capabilities. According to industry projections, countries like South Korea, Japan, and the United States are expected to achieve 5G penetration rates of 73%, 68%, and 68% respectively by 2025, creating robust infrastructure for advanced robotics applications. This enhanced connectivity is enabling more sophisticated real-time communication between autonomous mobile robots, allowing for improved coordination in complex environments and enabling the deployment of larger robot fleets. The integration of 5G technology is particularly crucial for applications requiring ultra-reliable, low-latency communication, such as coordinated warehouse operations and manufacturing floor automation.

Mobile Robots Market Trends

Rapid Growth of E-commerce Leading to Warehouse Automation

The exponential growth of e-commerce has fundamentally transformed the retail landscape, creating unprecedented demands on warehouse operations and logistics networks. According to the International Trade Administration, global retail e-commerce sales are projected to reach USD 6,388 billion by 2024, driving warehouses and distribution centers to seek innovative automation solutions. This surge in online shopping has intensified the pressure on fulfillment operations to maintain faster delivery times while managing increasingly complex inventory systems. E-commerce companies are increasingly turning to autonomous mobile robots (AMRs) to improve operational efficiencies in their warehouses and distribution centers, as these mobile robots can effectively handle tasks such as picking, sorting, and transportation of goods.

The warehouse automation trend is evidenced by several major implementations in 2023. For instance, in February 2023, Geek+ and Starlings launched the first robotic fulfillment center in Saudi Arabia, deploying 250 Geek+ robots for both goods-to-person picking and order sorting processes in a 400,000 sq ft facility with storage capacity for over 12 million units. Similarly, in August 2022, global logistics provider Geodis announced plans to deploy 1,000 autonomous mobile robots at facilities worldwide over the next two years, highlighting the industry's commitment to automation. These implementations demonstrate how mobile robots are becoming essential tools for managing the increasing complexity of e-commerce fulfillment operations while maintaining efficiency and accuracy in order processing.

Understand The Key Trends Shaping This Market

Download PDF

Increasing Labor Costs in the Developed Nations

Rising labor costs across developed nations, coupled with widespread worker shortages, are compelling industries to seek automated solutions. According to the US Bureau of Labor Statistics, the average industrial truck and tractor operator salary ranges between USD 34,488 and USD 50,110, with additional costs in benefits, overtime, and vacation time. In the European Union, labor costs have shown significant increases, with hourly labor costs rising by 4.0% in the euro area and 4.4% in the EU in the second quarter of 2022 compared to the previous year. These escalating costs are pushing companies to consider automation as a more cost-effective long-term solution.

The implementation of autonomous mobile robots has demonstrated substantial cost savings and operational benefits for organizations. Operations embracing AMRs and human operation can achieve up to a 30% reduction in labor costs, with some systems realizing up to 100% reductions in certain applications. For instance, in January 2023, DesignFuture Japan, the Japanese arm of Material Bank, deployed 25 Locus AMRs at their distribution facility to deliver high-productivity logistics and order fulfillment, addressing both labor shortage and cost challenges. Additionally, in China, labor costs continue to rise, with 14 regions now having minimum monthly wages exceeding RMB 2,000 (USD 308), including major industrial areas like Beijing, Jiangsu, and Guangdong, further accelerating the adoption of automation solutions in manufacturing and logistics operations by autonomous mobile robot companies.

Segment Analysis: By Product

Autonomous Mobile Robot (AMR) Segment in Mobile Robots Market

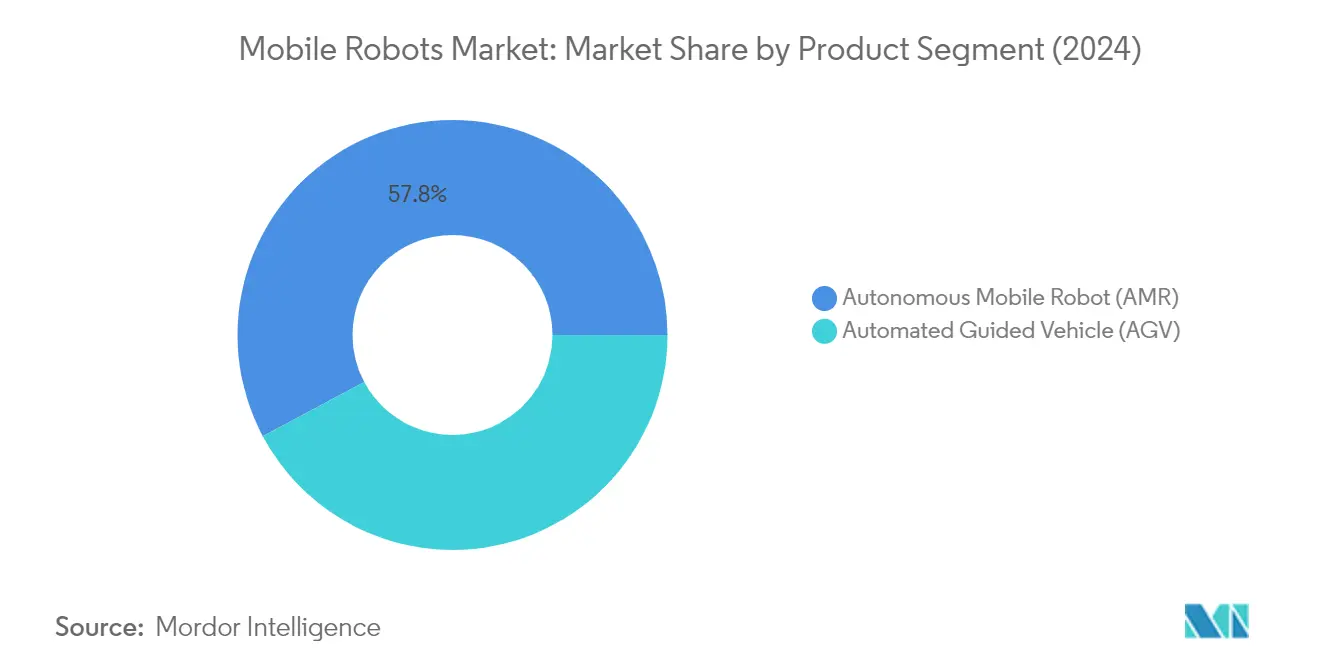

The Autonomous Mobile Robot (AMR) segment has established itself as the dominant force in the global mobile robots market, commanding approximately 58% of the market share in 2024. AMRs have gained significant traction due to their superior flexibility and intelligence compared to traditional AGVs, as they do not require any physical infrastructure such as markers, wires, magnetic strips, or laser targets for navigation. These robots utilize advanced technology to produce accurate maps of their environment and self-navigate to reach their destination. A key differentiating feature of AMRs is their sophisticated obstacle avoidance capability, allowing them to detect obstacles and dynamically adjust their routes to complete designated tasks without human supervision. The segment's growth is particularly driven by their widespread adoption in e-commerce fulfillment centers, manufacturing facilities, and warehouses, where they assist with tasks like locating, picking, and moving inventory, enabling employees to focus on higher-value activities.

Growth Trajectory of AMR Segment in Mobile Robots Market

The Autonomous Mobile Robot (AMR) segment is projected to maintain its impressive growth trajectory with an estimated growth rate of approximately 32% during the forecast period 2024-2029. This remarkable growth is attributed to the segment's continuous technological advancements, particularly in edge AI and machine vision capabilities, which enable AMRs to perform increasingly complex tasks beyond basic material handling. The integration of sophisticated technologies has expanded their application base, with AI and vision solutions enabling automated path findings, obstacle detections, and efficient material delivery optimization. The segment's growth is further fueled by the rising need for flexible automation solutions that can adapt to dynamic work environments, particularly in industries facing labor shortages and increasing pressure for operational efficiency. The ability of AMRs to operate in unstructured environments and their easy integration into existing operations without requiring significant infrastructure changes continues to drive their adoption across various industries.

Segment Analysis: By Form Factor

Unit Load Segment in Mobile Robots Market

The Unit Load segment maintains its dominant position in the mobile robots market, commanding approximately 33% market share in 2024. Unit load mobile robots (ULMR) utilize integrated or attached lifting modules to transport trolleys, racks, or pallets efficiently across facilities. These robots excel in picking and dropping goods at specific locations while adapting working heights for optimal ergonomic benefits. The segment's leadership is attributed to its competitive advantages over alternatives like forklifts, including superior inventory visibility, reduced accidents, enhanced workplace safety, and improved operational efficiency in refrigerated or frozen environments. Unit load systems also eliminate challenges related to manual material misplacement and provide consistent output regardless of operator skill levels, making them particularly valuable in warehouse and manufacturing settings.

Assembly Line Segment in Mobile Robots Market

The Assembly Line segment is experiencing remarkable growth, projected to expand at approximately 30% annually from 2024 to 2029. This accelerated growth is driven by the increasing adoption of robotic assembly lines across various industries, particularly in manufacturing and warehousing operations. Assembly line mobile robots are revolutionizing traditional manufacturing processes by performing repetitive tasks with greater precision and consistency while enabling human workers to focus on more complex, value-adding activities. The segment's growth is further propelled by advancements in human-robot collaboration capabilities, allowing robots to operate seamlessly alongside human workers in assembly operations. These robots can be programmed for multiple tasks and quickly reprogrammed to adapt to changes in production processes, offering unprecedented flexibility in manufacturing environments.

Remaining Segments in Mobile Robots Market by Form Factor

The Tow/Tractor/Tug and Forklift segments complete the mobile robots market landscape, each serving distinct operational needs. Tow/Tractor/Tug robots are designed for pulling multiple trailers simultaneously, making them highly efficient for bulk material movement in manufacturing and logistics environments. These robots can be equipped with various devices to enhance operator ergonomics and minimize non-ergonomic operations. The Forklift segment focuses on autonomous forklift solutions that can handle both floor-to-floor material handling and pallet stacking operations, offering versatility in warehouse operations while maintaining high safety standards and operational efficiency.

Segment Analysis: By Navigation Sensor

Laser/LiDAR Segment in Mobile Robots Market

The Laser/LiDAR segment maintains its dominant position in the mobile robots market, holding approximately 30% market share in 2024. This significant market presence can be attributed to the segment's superior 3D sensing capabilities and ability to operate effectively under challenging lighting conditions. Laser/LiDAR technology enables mobile robots to extend beyond controlled situations with pre-defined tasks and function efficiently in unfamiliar and unpredictable settings. The technology provides a constant stream of high-resolution, 3D information about the robot's surroundings, including precise location data of objects and people. The segment's strength is further enhanced by its dual functionality - while navigation-based LiDAR sensors are primarily used to construct environmental maps, obstacle avoidance LiDAR sensors are integrated into mobile robots' bodies to detect and prevent collisions with approaching objects.

Camera and Hybrid Segment in Mobile Robots Market

The Camera, Hybrid (Camera & LiDAR) and Other segment is experiencing the most rapid growth in the mobile robots market, with an expected growth rate of approximately 29% from 2024 to 2029. This accelerated growth is driven by the increasing adoption of vision solutions that are transforming how Autonomous Mobile Robots (AMRs) operate in various applications, particularly in warehouse management. The integration of advanced vision systems, including Time-of-Flight (ToF) cameras, is revolutionizing warehouse operations by equipping AGVs and AMRs with sophisticated depth-sensing intelligence. These advanced vision systems enable robots to perceive their surroundings and capture depth imaging data, allowing them to undertake business-critical functions with unprecedented accuracy, convenience, and speed. The segment's growth is further propelled by the cost-effectiveness of vision systems compared to traditional navigation methods.

Remaining Segments in Navigation Sensor Market

The mobile robots market's navigation sensor landscape is further complemented by the Reflector and QR Code segments, each offering unique advantages for specific applications. The Reflector-based navigation systems are particularly valued for their ease of installation and rapid deployment capabilities, allowing manufacturers to quickly simulate AGV paths and define routes with minimal effort. Meanwhile, the QR Code navigation system has gained traction due to its cost-effectiveness and ability to store more data than traditional barcode systems, making it particularly suitable for warehouse and logistics applications where precise positioning and navigation are crucial. These segments continue to play vital roles in different industrial settings, offering alternatives that cater to varying operational requirements and budget constraints.

Segment Analysis: By Environment of Operation

Manufacturing Segment in Mobile Robots Market

The manufacturing segment, encompassing automotive, electrical & electronics, food & beverage, chemical & pharmaceuticals, and other industries, holds approximately 53% share of the global mobile robots market in 2024. This dominant position is driven by the increasing adoption of mobile robots across various manufacturing applications to optimize production processes and enhance operational efficiency. The segment's growth is particularly notable in electronics manufacturing, where mobile robots are extensively deployed to reduce waste, improve efficiency, and create safer working environments. The automotive sector, especially with the transition towards electric vehicle production, has emerged as a significant adopter of mobile robots for material handling and assembly line operations. Additionally, the food and beverage industry's increasing automation needs, coupled with the pharmaceutical sector's requirements for precise and contamination-free material handling, have further strengthened the manufacturing segment's market leadership.

Non-Manufacturing Segment in Mobile Robots Market

The non-manufacturing segment, primarily comprising logistics centers, distribution centers, and warehouses, is projected to grow at approximately 29% during 2024-2029, emerging as the fastest-growing segment in the mobile robots market. This exceptional growth is primarily driven by the rapid expansion of e-commerce and the increasing need for efficient warehouse automation solutions. The segment's growth is further accelerated by the rising demand for same-day or next-day delivery services, compelling warehouse operators to invest in autonomous mobile robots for faster order fulfillment and improved operational efficiency. Mobile robots in logistics and warehousing environments are revolutionizing traditional material handling processes by enabling faster order processing, reducing labor costs, and minimizing errors in picking and sorting operations. The ease of deployment compared to conventional automation systems, coupled with the flexibility to scale operations without significant infrastructure modifications, makes mobile robots particularly attractive for warehouse automation applications.

Mobile Robots Market Geography Segment Analysis

Mobile Robots Market in Asia-Pacific (Excluding China)

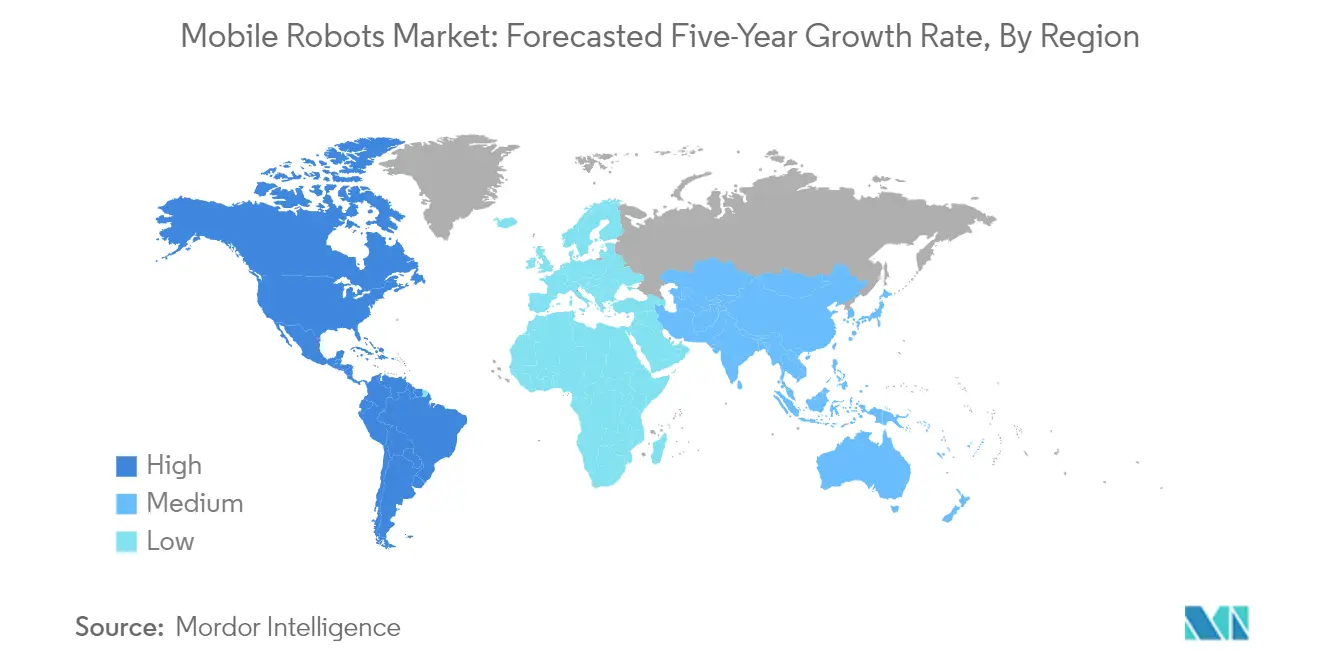

The Asia-Pacific region, excluding China, represents the largest mobile robots market, commanding approximately 32% of the global market share in 2024. The region's dominance is primarily driven by countries like Japan and South Korea, which have emerged as technological powerhouses in robotics and automation. Japan, being a leading manufacturer and consumer of robots, has implemented strategic initiatives like the "New Robot Strategy" aimed at making the country the world's premier robot innovation hub. The strong presence of major electronics and automotive manufacturers in the region has created substantial demand for mobile robots in manufacturing processes. Additionally, the region's progressive stance on Industry 4.0 adoption, particularly in countries like South Korea with its Third Basic Plan on Intelligent Robots, has fostered an environment conducive to mobile robot deployment. The integration of advanced technologies such as artificial intelligence and IoT in manufacturing processes has further accelerated the adoption of mobile robots across various industries.

Mobile Robots Market in China

China's mobile robots market is poised for exceptional growth, projected to expand at approximately 31% annually from 2024 to 2029. The country's remarkable growth trajectory is underpinned by its Made in China 2025 initiative, which prioritizes high-tech manufacturing and robotics development. The Chinese market has witnessed substantial investments from both domestic and international players, with numerous robotic companies benefiting from significant funding increases. The country's commitment to industrial automation is evident through various government-backed programs and initiatives aimed at modernizing manufacturing facilities. The rapid expansion of e-commerce and increasing labor costs have driven warehousing and logistics companies to adopt automated solutions, particularly in urban areas. Furthermore, China's position as home to some of the world's most advanced manufacturing facilities has created an ideal environment for mobile robot deployment, with domestic companies increasingly focusing on developing innovative autonomous solutions.

Mobile Robots Market in United States

The United States maintains a strong position in the mobile robots market, driven by its robust manufacturing sector and early adoption of Industry 4.0 technologies. The country's emphasis on warehouse automation and logistics optimization has created significant opportunities for mobile robot deployment. American manufacturers are increasingly implementing autonomous mobile robots to address labor shortages and improve operational efficiency. The automotive industry, being one of the largest adopters of mobile robots, continues to drive market growth through its transition toward electric vehicle production. The country's strong focus on research and development, coupled with the presence of leading robotics companies and technology innovators, has fostered an environment of continuous innovation in mobile robot technologies. Additionally, the growing emphasis on workplace safety and the need for contactless operations has accelerated the adoption of mobile robots across various industries.

Mobile Robots Market in Europe

Europe's mobile robots market is characterized by its strong focus on technological innovation and industrial automation, particularly in countries like Germany, which serves as a major hub for robotics development. The region's commitment to Industry 4.0 initiatives has created a favorable environment for mobile robot adoption across various sectors. The presence of major automotive manufacturers and their increasing focus on automated production processes has been a significant driver for market growth. European countries have also demonstrated strong support for robotics research and development through various funding programs and initiatives. The region's emphasis on sustainable manufacturing practices has led to increased adoption of energy-efficient mobile robots. Furthermore, the growing e-commerce sector and the need for efficient warehouse automation have created new opportunities for mobile robot deployment across the region.

Mobile Robots Market in Other Countries

The mobile robots market in other regions, particularly in the Middle East and Africa, demonstrates varying levels of adoption and growth potential. Countries in the Middle East, especially the United Arab Emirates and Saudi Arabia, are making significant strides in embracing robotics and automation technologies through various government initiatives and investments. The UAE's Fourth Industrial Revolution Program and Saudi Arabia's growing e-commerce sector are creating new opportunities for mobile robot deployment. While the African continent currently shows relatively lower adoption rates, there is growing interest in automated solutions, particularly in the manufacturing and logistics sectors. These regions are gradually developing their technological infrastructure and implementing policies to support the adoption of advanced automation solutions. The increasing focus on diversifying economies and modernizing industrial sectors in these regions suggests potential for future growth in the mobile robots market.

Get Analysis on Important Geographic Markets

Download PDF

Mobile Robots Industry Overview

Top Companies in Mobile Robots Market

The mobile robots market features prominent players like KION, JBT, Elettic80, Geek+, and Toyota among the market leaders. These mobile robot companies demonstrate strong product innovation through continuous development of advanced autonomous mobile robots (AMRs) and automated guided vehicles (AGVs) with enhanced navigation capabilities, payload capacities, and intelligent features. Operational agility is evidenced through rapid deployment capabilities, flexible automation solutions, and the ability to integrate with existing warehouse management systems. Strategic moves in the industry are characterized by partnerships with system integrators, technology companies, and end-users to expand market reach and enhance solution offerings. Companies are actively expanding their geographical presence through distribution networks, regional offices, and manufacturing facilities across North America, Europe, and Asia Pacific to better serve local markets and provide localized support.

Diverse Players Shape Dynamic Market Structure

The mobile robots market exhibits a mix of global conglomerates and specialized robotics companies competing for market share. Large industrial automation companies like Omron, Daifuku, and Toyota leverage their established presence, comprehensive product portfolios, and strong financial resources to maintain market positions. Meanwhile, specialized players like Mobile Industrial Robots, Fetch Robotics, and Geek+ focus exclusively on mobile robotics technology, bringing agility and targeted innovation to the market. The industry is experiencing ongoing consolidation through strategic acquisitions, as evidenced by Teradyne's acquisition of Mobile Industrial Robots and AutoGuide Mobile Robots, demonstrating the trend of larger companies acquiring specialized technology providers.

The market structure is characterized by intense competition driving continuous innovation and product development. Companies are forming strategic alliances and partnerships to enhance their technological capabilities and expand their market reach. The emergence of robotics-as-a-service (RaaS) business models is reshaping competitive dynamics by lowering barriers to entry for end-users and creating new opportunities for service-oriented providers. Regional players are gaining prominence in their local markets through specialized knowledge of local requirements and strong customer relationships, while global players leverage their international presence and comprehensive solution offerings.

Innovation and Adaptability Drive Future Success

Success in the autonomous mobile robot market increasingly depends on companies' ability to deliver innovative, flexible solutions that address evolving customer needs. Incumbents must focus on developing advanced technologies like artificial intelligence, machine learning, and enhanced navigation systems to maintain their competitive edge. Companies need to strengthen their service and support networks while expanding their integration capabilities with various warehouse management systems and other automation technologies. The ability to offer customizable solutions, quick deployment options, and comprehensive after-sales support will be crucial for maintaining market position and capturing new opportunities.

Market contenders can gain ground by focusing on specific industry verticals or applications where they can develop specialized expertise and differentiated solutions. The development of user-friendly interfaces, simplified implementation processes, and flexible pricing models will be essential for attracting new customers and expanding market share. Companies must also prepare for potential regulatory changes regarding autonomous systems and safety standards, while maintaining strong cybersecurity measures to protect connected robotic systems. Success will depend on building strong partnerships with technology providers, system integrators, and end-users while maintaining the agility to adapt to rapidly changing market conditions and customer requirements.

Mobile Robots Market Leaders

-

Teradyne Inc. (Mobile Industrial Robots ApS (MIR))

-

Fetch Robotics

-

JASCI LLC

-

Aethon Inc.

-

KION Group AG

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Mobile Robots Market News

- March 2023 - OTTO Motors introduced OTTO 600, an advanced AMR designed for heavy-duty environments, capable of handling payloads up to 600 kg (1,322 lb).

- March 2023 - ForwardX Robotics launched its new autonomous forklift, Apex C1500-L, which features higher payload capacity and compatibility with both GMA and Euro pallets.

Mobile Robots Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitutes

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Industry Value Chain Analysis

- 4.4 Impact of Macro Trends on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Rapid Growth of E-commerce Leading to Warehouse Automation

- 5.1.2 Increasing Labor Costs in the Developed Nations

-

5.2 Market Restraints

- 5.2.1 High Capital Requirements and Connectivity Issues

6. MARKET SEGMENTATION

-

6.1 By Product

- 6.1.1 Automated Guided Vehicle (AGV)

- 6.1.2 Autonomous Mobile Robot (AMR)

-

6.2 By Form Factor

- 6.2.1 Forklifts

- 6.2.2 Tow/Tractor/Tug

- 6.2.3 Unit Load

- 6.2.4 Assembly Line

-

6.3 By Navigation Sensor

- 6.3.1 Reflector

- 6.3.2 QR Code

- 6.3.3 Laser/LiDAR

- 6.3.4 Camera, Hybrid (Camera & LiDAR) and Other navigation sensors

-

6.4 By Environment of Operation

- 6.4.1 Manufacturing (Automotive, Electrical & Electronics, Food & Beverage, Chemical & Pharmaceuticals and Other Environments of Operation)

- 6.4.2 Non-Manufacting (Logistics Centers/Distribution Centers/Warehouses)

-

6.5 By Geography***

- 6.5.1 United States

- 6.5.2 Europe

- 6.5.3 Asia

- 6.5.4 China

- 6.5.5 Australia and New Zealand

- 6.5.6 Latin America

- 6.5.7 Middle East and Africa

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles*

- 7.1.1 Teradyne Inc (Mobile Industrial Robots ApS (MIR))

- 7.1.2 Fetch Robotics

- 7.1.3 JASCI LLC

- 7.1.4 Aethon Inc.

- 7.1.5 KION Group AG

- 7.1.6 SCOTT TECHNOLOGY LIMITED

- 7.1.7 Murata Machinery Ltd

- 7.1.8 Toyota Material Handling US

- 7.1.9 John Bean Technologies (JBT) Corporation

- 7.1.10 6 River Systems Inc

- 7.1.11 inVia Robotics Inc.

- 7.1.12 IAM Robotics LLC

- 7.1.13 GreyOrange Pte Ltd

- 7.1.14 Clearpath Robotics Inc.

- 7.1.15 Geek+ Inc

- 7.1.16 Omron Corporation

- 7.1.17 Daifuku Co. Ltd

8. VENDOR RANKING ANALYSIS

9. INVESTMENT ANALYSIS

10. FUTURE OUTLOOK

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' and Latin America and Middle East and Africa will be considered together as 'Rest of the World'

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Mobile Robots Industry Segmentation

Mobile robots are autonomous or semi-autonomous machines designed to move around in their environment without needing a fixed base or external guidance. They frequently have sensors, cameras, and other equipment to perceive and interact with their surroundings and are controllable via onboard computers or remote control.

The mobile robots market is segmented by product (automated guided vehicle (AGV), autonomous mobile robot (AMR)), by form factor (forklift, tow tractor, tug, unit load, assembly line), by navigation sensor (reflector, QR code, laser/liDAR, camera, hybrid (camera & LiDAR)), by the environment of operation (manufacturing (automotive, electrical & electronics, food & beverage, chemical & pharmaceuticals), non-manufacturing (logistics centers/distribution centers/warehouses), and geography (United States, China, Europe, Asia-Pacific (excluding China), and the Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the segments.

| By Product | Automated Guided Vehicle (AGV) |

| Autonomous Mobile Robot (AMR) | |

| By Form Factor | Forklifts |

| Tow/Tractor/Tug | |

| Unit Load | |

| Assembly Line | |

| By Navigation Sensor | Reflector |

| QR Code | |

| Laser/LiDAR | |

| Camera, Hybrid (Camera & LiDAR) and Other navigation sensors | |

| By Environment of Operation | Manufacturing (Automotive, Electrical & Electronics, Food & Beverage, Chemical & Pharmaceuticals and Other Environments of Operation) |

| Non-Manufacting (Logistics Centers/Distribution Centers/Warehouses) | |

| By Geography*** | United States |

| Europe | |

| Asia | |

| China | |

| Australia and New Zealand | |

| Latin America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Mobile Robots Market Research Faqs

How big is the Mobile Robots Market?

The Mobile Robots Market size is expected to reach USD 8.91 billion in 2025 and grow at a CAGR of 27.5% to reach USD 30.03 billion by 2030.

What is the current Mobile Robots Market size?

In 2025, the Mobile Robots Market size is expected to reach USD 8.91 billion.

Who are the key players in Mobile Robots Market?

Teradyne Inc. (Mobile Industrial Robots ApS (MIR)), Fetch Robotics, JASCI LLC, Aethon Inc. and KION Group AG are the major companies operating in the Mobile Robots Market.

What years does this Mobile Robots Market cover, and what was the market size in 2024?

In 2024, the Mobile Robots Market size was estimated at USD 6.46 billion. The report covers the Mobile Robots Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Mobile Robots Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Mobile Robots Market Research

Mordor Intelligence, a leading AMR research company, provides a comprehensive analysis of the mobile robotics market through detailed industry research and consulting services. Our extensive coverage includes industrial mobile robots, autonomous mobile robots, and various mobile robot platforms. This analysis offers stakeholders crucial insights into market dynamics. The report thoroughly examines the evolving landscape of mobile robot technology. It highlights developments in automated mobile robots and their applications across diverse industries.

The report offers invaluable insights for stakeholders in the mobile robots ecosystem. It focuses particularly on the market for mobile robots in healthcare and hospitality sectors and the professional service mobile robots market. Our analysis covers prominent autonomous mobile robot companies and their technological innovations. This information is available in an easy-to-read report PDF format for download. The research provides a detailed examination of mobile robotics software developments, mobile robot investment trends, and emerging opportunities in the mobile logistics robot market. This enables businesses to make informed strategic decisions based on robust market intelligence.