Market Size of meo satellite Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

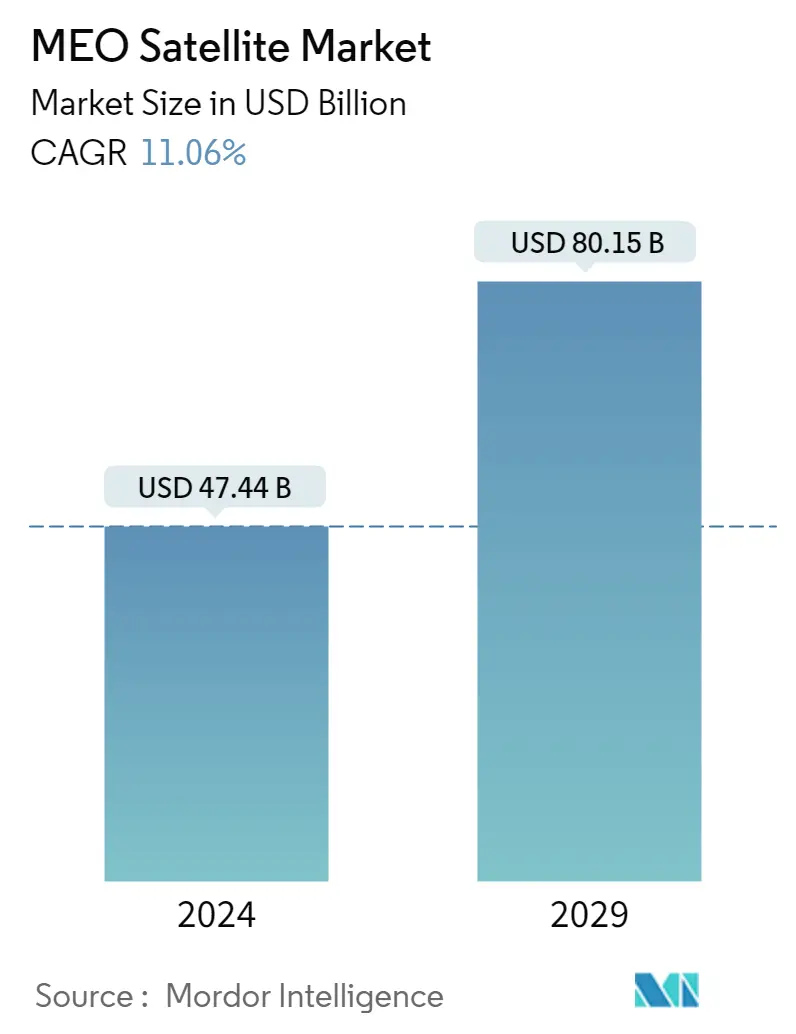

Market Size (2024) | USD 47.44 Billion |

|

|

Market Size (2029) | USD 80.15 Billion |

|

|

Largest Share by Propulsion Tech | Liquid Fuel |

|

|

CAGR (2024 - 2029) | 11.06 % |

|

|

Largest Share by Region | Asia-Pacific |

|

|

Market Concentration | High |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

MEO Satellite Market Analysis

The MEO Satellite Market size is estimated at USD 47.44 billion in 2024, and is expected to reach USD 80.15 billion by 2029, growing at a CAGR of 11.06% during the forecast period (2024-2029).

47.44 Billion

Market Size in 2024 (USD)

80.15 Billion

Market Size in 2029 (USD)

34.97 %

CAGR (2017-2023)

11.06 %

CAGR (2024-2029)

Largest Market by Satellite Mass

61.49 %

value share, above 1000kg, 2022

Large satellites have a higher demand due to their applications, such as satellite radio, communication, remote sensing, planetary security, and weather forecasting.

Largest Market by Propulsion Tech

73.93 %

value share, Liquid Fuel, 2022

Due to its high efficiency, controllability, reliability, and long lifespan, liquid fuel-based propulsion technology is an ideal choice for space missions. It can be used in various orbit classes for satellites.

Largest Market by End User

79.60 %

value share, Commercial, 2022

Increasing usage of MEO satellites for telecommunication services generates the need to deploy advanced communication satellites for commercial purposes thereby the requirement of these satellites has become more relevant.

Largest Market by region

95.56 %

value share, Asia-Pacific, 2022

Government collaborations with private players are emphasizing the growth of MEO Satellite in the Asia-Pacific region. In addition, continuous investments towards the development of these satellites by China and India is also prompting to the increased growth.

Leading Market Player

61.07 %

market share, Lockheed Martin Corporation, 2022

Lockheed Martin is the leading player in the global MEO satellites market. It has a strong product portfolio for military satellites. The company's civil and military customers include USAF, the US Navy, DARPA, NASA, and NOAA. This has facilitated the company in capturing the highest share of the market.

The liquid fuel propulsion system segment leads the market's growth

- A satellite's propulsion system is commonly used to propel a spacecraft into orbit and to coordinate the position of the spacecraft in orbit. Liquid propellants or liquid rockets use rocket engines that use liquid propellants. Gas propellants can also be used but are not common due to their low density and difficulty in applying conventional pumping methods. The liquid fuel propulsion system is the most adopted one of the three propulsion types because of its high density and specific impulse. It is expected to occupy a market share of 73.3% in 2023, which is anticipated to reach 69.5% in 2029.

- Electric propulsion is the second most adopted type of propulsion system, and it is commonly used to hold stations for commercial communication satellites. It is the main propulsion of some space science missions due to its high specific impulses. Northrop Grumman Corporation, Moog Inc., Sierra Nevada Corporation, SpaceX, and Blue Origin are some of the major providers of propulsion systems. The new launch of satellites is expected to accelerate market growth over the forecast period.

- Gas-based propulsion systems that enable movements have been proven efficient and reliable. These include hydrazine systems, other single or twin propulsion systems, hybrid systems, cold/hot air systems, and solid propellants. Typically, these systems are used when strong thrust or rapid maneuvering is required. Therefore, in some cases, gas-based systems continue to be the space propulsion technology of choice when their total impulse capacity is sufficient to meet the mission requirements. Cold gas thrusters are suitable for small satellites because of their low cost and complexity, but they are not ideal for large satellites.

Europe is expected to open new scope of opportunities with significant new product developments in the region

- R&D expenditure on medium Earth orbit (MEO) satellites is an important factor in driving innovation and technology development in the satellite industry. MEO satellites are often used for specialized applications, such as providing global positioning system (GPS) services. As these applications become more critical to society, there may be more R&D investment to improve MEO satellite performance and capabilities.

- The Russian satellite industry is one of the most active and advanced in the world. ISS Reshetnev dominates the MEO satellite market in Russia. ISS Reshetnev is a leading Russian satellite manufacturer responsible for developing and producing most of the country's MEO satellites. ISS Reshetnev's most notable contribution to the MEO satellite market in Russia is its GLONASS series. The GLONASS system is a Russian counterpart to the American GPS system and provides global positioning services to users worldwide. All of these satellites are of the GLONASS series and were manufactured and launched by ISS Reshetnev.

- China has already launched a number of MEO satellites as part of this initiative and is expected to launch many more in the coming years. For instance, during 2017-2022*, 24 navigation and global positioning satellites weighing 800 kg each were placed in MEO for government and military purposes. These satellites were launched by China's Space Technology Research Institute (part of CASC) as part of China's BeiDou Navigation Satellite System (BDS), China's global navigation system. The Asia-Pacific region is expected to dominate during the forecast period.

MEO Satellite Industry Segmentation

Communication, Earth Observation, Navigation, Others are covered as segments by Application. 100-500kg, 500-1000kg, above 1000kg are covered as segments by Satellite Mass. Commercial, Military & Government are covered as segments by End User. Electric, Gas based, Liquid Fuel are covered as segments by Propulsion Tech. Asia-Pacific, Europe, North America are covered as segments by Region.

- A satellite's propulsion system is commonly used to propel a spacecraft into orbit and to coordinate the position of the spacecraft in orbit. Liquid propellants or liquid rockets use rocket engines that use liquid propellants. Gas propellants can also be used but are not common due to their low density and difficulty in applying conventional pumping methods. The liquid fuel propulsion system is the most adopted one of the three propulsion types because of its high density and specific impulse. It is expected to occupy a market share of 73.3% in 2023, which is anticipated to reach 69.5% in 2029.

- Electric propulsion is the second most adopted type of propulsion system, and it is commonly used to hold stations for commercial communication satellites. It is the main propulsion of some space science missions due to its high specific impulses. Northrop Grumman Corporation, Moog Inc., Sierra Nevada Corporation, SpaceX, and Blue Origin are some of the major providers of propulsion systems. The new launch of satellites is expected to accelerate market growth over the forecast period.

- Gas-based propulsion systems that enable movements have been proven efficient and reliable. These include hydrazine systems, other single or twin propulsion systems, hybrid systems, cold/hot air systems, and solid propellants. Typically, these systems are used when strong thrust or rapid maneuvering is required. Therefore, in some cases, gas-based systems continue to be the space propulsion technology of choice when their total impulse capacity is sufficient to meet the mission requirements. Cold gas thrusters are suitable for small satellites because of their low cost and complexity, but they are not ideal for large satellites.

| Application | |

| Communication | |

| Earth Observation | |

| Navigation | |

| Others |

| Satellite Mass | |

| 100-500kg | |

| 500-1000kg | |

| above 1000kg |

| End User | |

| Commercial | |

| Military & Government | |

| Other |

| Propulsion Tech | |

| Electric | |

| Gas based | |

| Liquid Fuel |

| Region | |

| Asia-Pacific | |

| Europe | |

| North America | |

| Rest of World |

MEO Satellite Market Size Summary

The MEO Satellite Market is poised for significant growth, driven by advancements in satellite propulsion systems and increasing demand for navigation and communication services. The market is characterized by the adoption of liquid and electric propulsion systems, with major players like Northrop Grumman Corporation, Moog Inc., and SpaceX leading the charge in technology development. The market's expansion is further supported by substantial R&D investments aimed at enhancing satellite performance and capabilities, particularly in regions like Asia-Pacific, where countries such as China and Russia are actively launching MEO satellites for navigation systems like BeiDou and GLONASS. These satellites, positioned between LEO and GEO orbits, are crucial for global positioning services and are becoming increasingly vital as societal reliance on accurate navigation data grows.

The industry landscape is fairly consolidated, with key players such as China Aerospace Science and Technology Corporation, Information Satellite Systems Reshetnev, Lockheed Martin Corporation, OHB SE, and Thales dominating the market. These companies are at the forefront of developing innovative satellite technologies, as evidenced by recent advancements like Thales Alenia Space's MEOLUT Next for satellite search and rescue. The market's growth trajectory is supported by government expenditures in North America and Europe, which are fostering innovation and development in the space sector. As the demand for MEO satellites continues to rise, driven by their applications in navigation and communication, the market is expected to experience robust growth over the forecast period.

MEO Satellite Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Application

-

1.1.1 Communication

-

1.1.2 Earth Observation

-

1.1.3 Navigation

-

1.1.4 Others

-

-

1.2 Satellite Mass

-

1.2.1 100-500kg

-

1.2.2 500-1000kg

-

1.2.3 above 1000kg

-

-

1.3 End User

-

1.3.1 Commercial

-

1.3.2 Military & Government

-

1.3.3 Other

-

-

1.4 Propulsion Tech

-

1.4.1 Electric

-

1.4.2 Gas based

-

1.4.3 Liquid Fuel

-

-

1.5 Region

-

1.5.1 Asia-Pacific

-

1.5.2 Europe

-

1.5.3 North America

-

1.5.4 Rest of World

-

-

MEO Satellite Market Size FAQs

How big is the MEO Satellite Market?

The MEO Satellite Market size is expected to reach USD 47.44 billion in 2024 and grow at a CAGR of 11.06% to reach USD 80.15 billion by 2029.

What is the current MEO Satellite Market size?

In 2024, the MEO Satellite Market size is expected to reach USD 47.44 billion.