Market Trends of LNG Industry

Liquefaction Sector to Dominate the Market

- In the last decade, there has been a significant rise in industrialization and urbanization, which has resulted in a surge in carbon dioxide and greenhouse gases worldwide. Thus, to reduce carbon and greenhouse gas emissions, governments are promoting the utilization of natural gas in power generation and fuel in vehicles.

- Thus, governments are developing various supportive policies to increase the adoption of CNG and LNG-based vehicles, including providing subsidies and tax exemptions to automobile manufacturers and consumers.

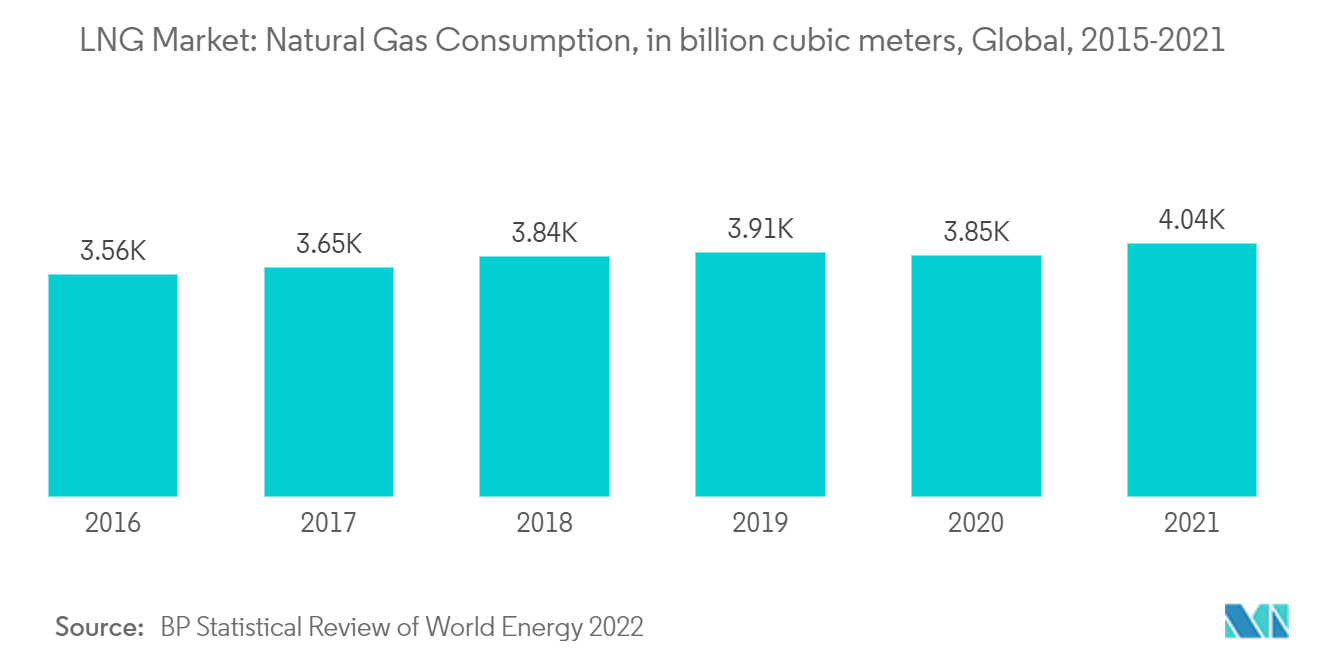

- The growing demand for natural gas across the regions resulted in increased natural gas consumption in the last decade across the globe. For instance, in 2012, natural gas consumption was around 3,319.4 billion cubic meters, which increased by more than 21% in 2021 to about 4,037.5 billion cubic meters.

- According to the World LNG Report 2022, LNG connected 40 importing countries with 19 export markets. The global liquefaction capacity accounted for 459.9 MTPA in 2021 after adding 6.9 MTPA, compared to 20 MTPA the year prior. The great potential for LNG in Africa is significant to the region's development, with 123.9 MTPA of proposed liquefaction waiting for the final investment decision (FID).

- Additionally, PFLNG Dua (1.5 MTPA), Corpus Christi T3 (4.5 MTPA), and Yamal LNG T4 (0.9 MTPA) were the liquefaction projects that came online in 2021. During the first four months of 2022, an additional 12.5 MTPA of liquefaction capacity was added, increasing the total global liquefaction capacity to 472.4 MTPA. Thus, the increasing liquefaction capacity, as well as the establishment of liquefaction projects, are expected to create demand for the liquefaction sector in the forecast period.

- Therefore, based on the above-mentioned factors, the liquefaction sector is expected to dominate the LNG market during the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

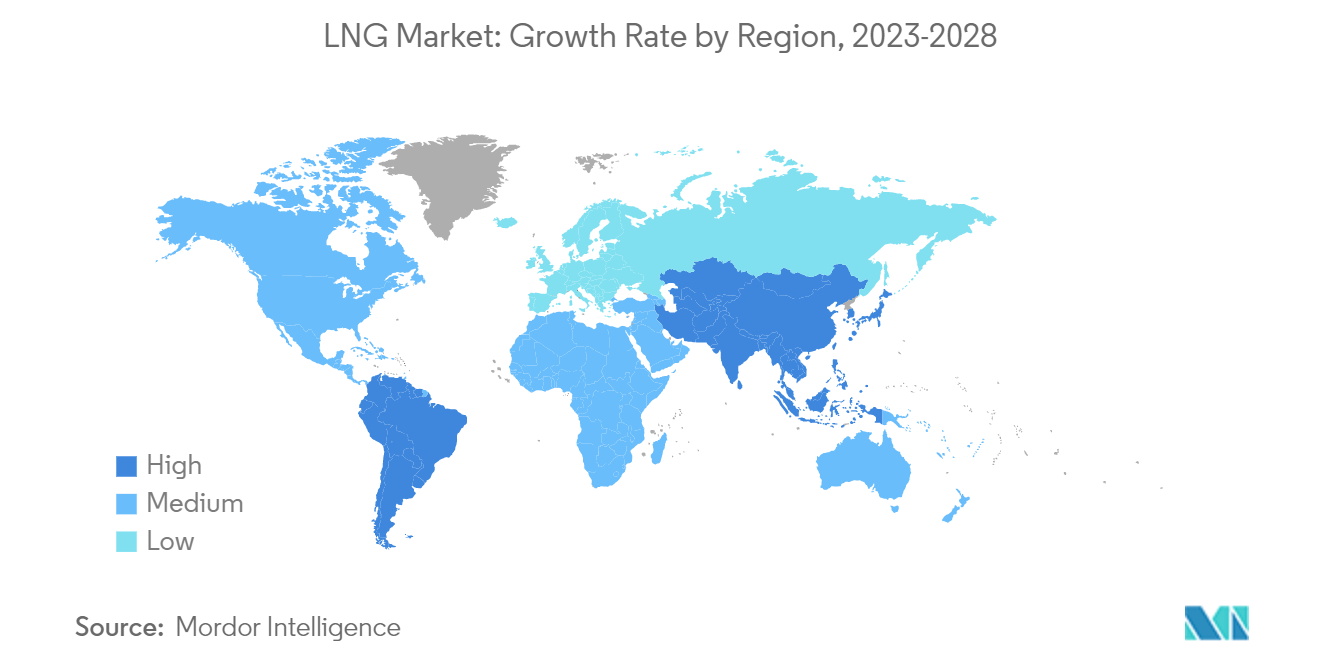

Asia-Pacific to Dominate the Market

- Asia-Pacific continued to be the leading importing region, with a 72% share of global LNG imports last year, up from 69% in 2019. Asian LNG imports grew by 7.7% last year, reaching 371.8 billion cubic meters. Imports rose in all Asia-Pacific countries except Japan, India, Malaysia, and Singapore.

- According to the World LNG Report 2022, the largest exporting region continued to be Asia-Pacific, with a total of 131.2 MT of exports last year, in line with what was exported in 2020.

- China, being the largest LNG importer in Asia-Pacific, experienced the greatest growth in terms of imported volumes, with an annual growth rate of 16.8%, accounting for 109.5 billion cubic meters last year. Additionally, governments also adopted supportive policies for natural gas consumption, which include several LNG projects.

- Furthermore, in February 2023, Jiangsu Huadian Ganyu LNG terminal construction began at Ganyu port in Lianyungang, China's eastern Jiangsu province. The project is included in both the national natural gas development plan and the province's 14th Five-Year Plan, with a designed LNG receiving capacity of 3 million mt/year. The project is one of four LNG-receiving projects approved by the federal government for 2022, with a total capacity of almost 24 million metric tons per year.

- Therefore, based on the above-mentioned factors, Asia-Pacific is expected to dominate the global LNG market during the forecast period.

Get Analysis on Important Geographic Markets

Download PDF