Market Overview

| Study Period | 2019 - 2030 |

|---|---|

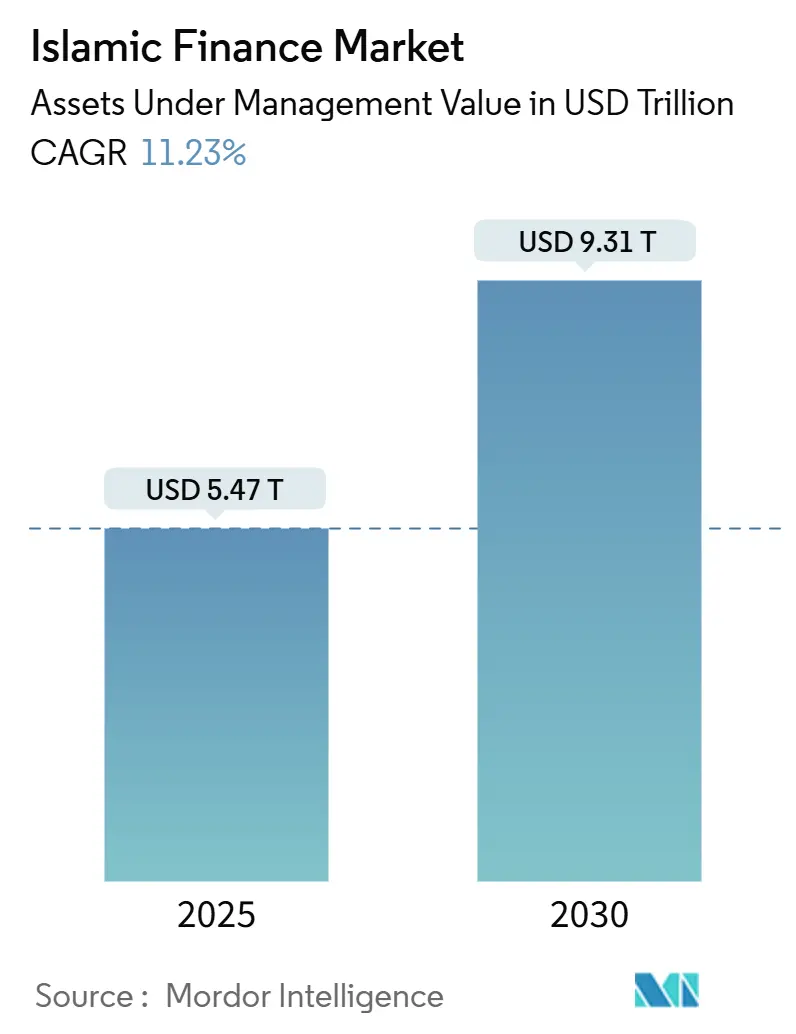

| Market Size (2025) | USD 5.47 Trillion |

| Market Size (2030) | USD 9.31 Trillion |

| Growth Rate (2025 - 2030) | 11.23% CAGR |

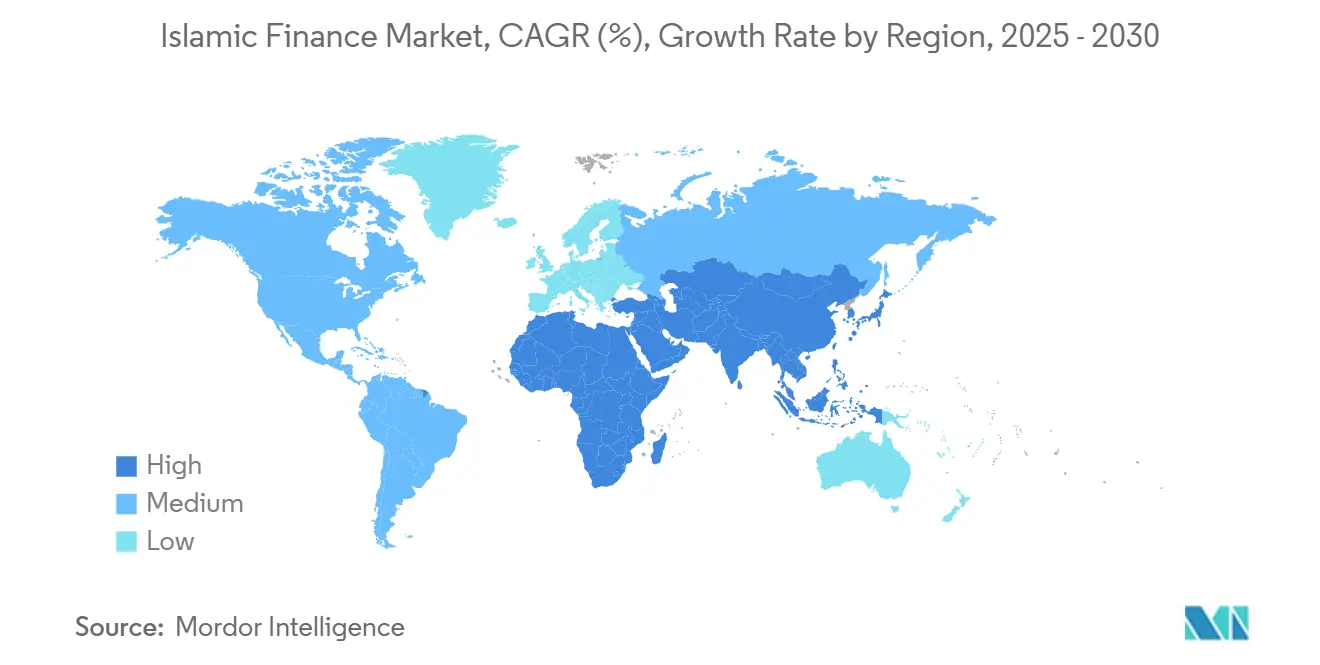

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East and Africa |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Islamic Finance Market Analysis by Mordor Intelligence

The Islamic finance market reached USD 5.47 trillion in 2025 and is on course to advance to USD 9.31 trillion by 2030, implying a sturdy 11.23% CAGR. Solid population growth in Muslim-majority countries, wider investor appetite for ethical assets, and steady government action to harmonize regulations support this trajectory. Growth benefits from swelling sovereign wealth fund allocations to Sharia-compliant products, the roll-out of Vision 2030 infrastructure programs in the Gulf, and Asia-Pacific’s digital banking leap that draws Generation Z users to mobile Islamic platforms. New blockchain-enabled sukuk and tokenized asset structures lower issuance costs, while rising ESG or green sukuk issuance links the sector to mainstream sustainable-finance mandates. Climate-risk exposure among asset-heavy Gulf banks and cybersecurity gaps in digital Islamic banks remain the chief headwinds.

Key Report Takeaways

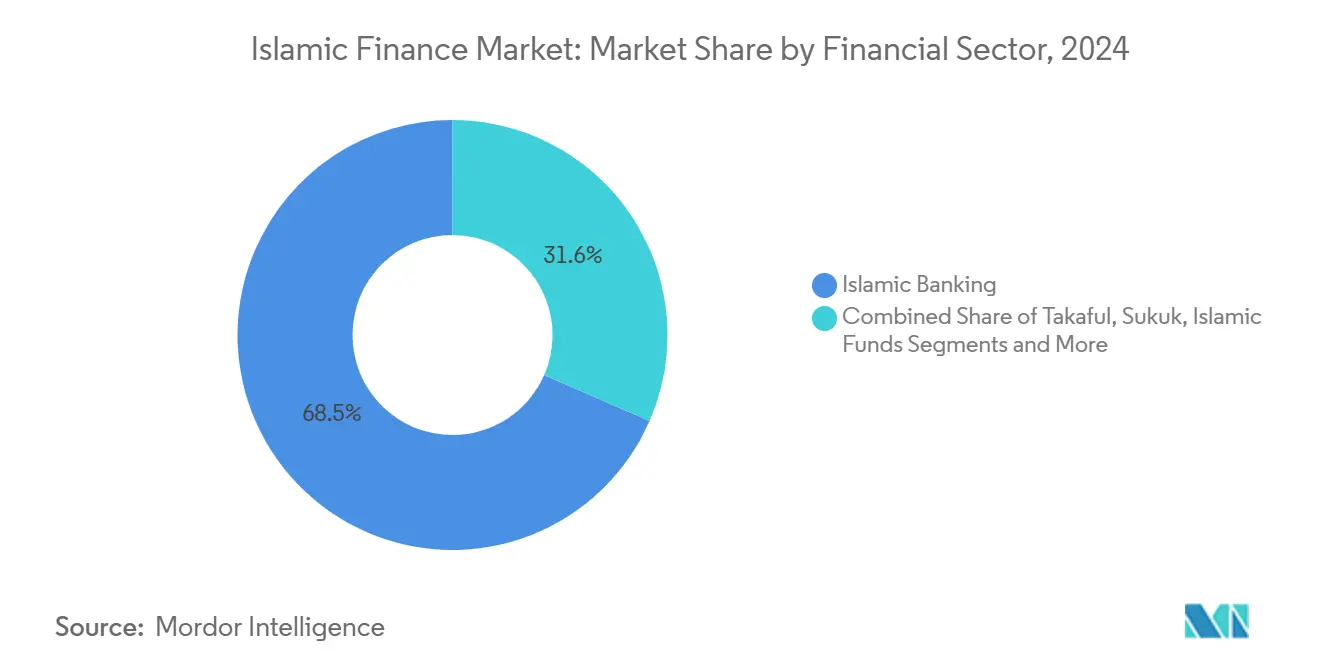

- By financial sector, Islamic banking led with 68.45% of the Islamic finance market share in 2024; Takaful is projected to expand at a 14.78% CAGR through 2030.

- By customer type, businesses accounted for 57.32% of the Islamic finance market size in 2024, while the retail segment is forecasted to grow at 12.89% CAGR to 2030.

- By geography, the Middle East & Africa commanded 61.94% share of the Islamic finance market in 2024; Asia-Pacific is expected to post a 13.28% CAGR between 2025 and 2030.

Global Islamic Finance Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Muslim affluence & demand for Sharia-compliant products | +2.8% | GCC, Indonesia, Malaysia | Long term (≥ 4 years) |

| Government policy pushes & regulatory harmonization | +2.1% | Middle East & Asia-Pacific | Medium term (2–4 years) |

| Surge in ESG/green sukuk issuance | +1.9% | Malaysia & UAE lead | Medium term (2–4 years) |

| Cross-border Islamic fintech platforms opening micro-investment pools | +1.4% | Asia-Pacific spill-over to MEA | Short term (≤ 2 years) |

| Blockchain-enabled tokenized sukuk lowering issuance costs | +1.2% | GCC core, Malaysia & Indonesia | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Rising Muslim Affluence & Demand for Sharia-Compliant Products

Higher disposable income is steering Muslim consumers toward sophisticated wealth management, sukuk, and private-market products delivered via digital channels. In Indonesia, Bank Syariah Indonesia’s net profit climbed 33% in 2024, mirroring growing middle-class demand. The UAE seeks to lift Islamic banking assets to AED 2.56 trillion by 2031, reinforcing Gulf leadership. Malaysia’s EPF Shariah savings produced returns between 5.5% and 6.5% in 2024, confirming the asset class’s competitive yield. The UK-based platform Mnaara now channels private-market exposure to Sharia-conscious investors, underscoring the globalization of Islamic wealth solutions. Demand is equally visible in North America and continental Europe, where ESG motives align with faith-based mandates.

Government Policy Pushes & Regulatory Harmonization

National strategies are accelerating sector penetration. Pakistan’s Federal Shariat Court ordered a full transition to Islamic banking by December 2027, the most sweeping conversion mandate in modern finance. Saudi Arabia’s Financial Sector Development Program aims to license new digital banks and broaden sukuk supply to sustain a debt-to-GDP ceiling of 22.1%. The UAE’s Higher Shari'ah Authority is working toward standardization to trim compliance costs for cross-border deals. In Malaysia, Bank Negara’s rules have long balanced innovation with prudence, keeping domestic Islamic lenders competitive. Unified standards foster scale economies and smoother capital flows across the Islamic finance market.

Surge in ESG/Green Sukuk Issuance

Global sukuk issuance witnessed significant growth in 2024, with green sukuk capturing about 10% of the market and recording the fastest growth[1]World Bank, “Global Sukuk Market 2024 Overview,” World Bank, worldbank.org. Indonesia’s sovereign green sukuk and the UAE’s AED 1 trillion sustainable-finance target signal deep public-sector engagement. Corporate demand is evident in Cenomi Centers’ USD 1.39 billion sustainability-linked murabaha facility with social and carbon targets. UBS research estimates total sukuk outstanding at USD 867 billion in Q1 2024, reflecting a broader investor base. Coming Basel III climate disclosures will sharpen transparency and should lift issuance appetite.

Cross-Border Islamic Fintech Platforms Opening Micro-Investment Pools

Islamic DeFi protocols, though still below USD 50 million in total value locked, reveal vast headroom inside a USD 3.5 trillion ethical-finance universe. Wahed Invest’s digital model illustrates scalable Sharia robo-advice as the MSCI World Islamic Index tracked positive momentum through 2024. Indonesia’s Bank Aladin reached 3.2 million users by mid-2024 on the back of fully Sharia-compliant digital banking[2]The Asian Banker, “Bank Aladin Reaches 3.2 Million Users,” The Asian Banker, theasianbanker.com. Investors such as Fintactics and Arbah Capital launched a USD 40 million Saudi fund to back early-stage Islamic fintechs. These platforms enlarge retail access across the Islamic finance market by lowering entry barriers.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Shariah standards across jurisdictions | -1.8% | Global cross-border | Long term (≥ 4 years) |

| Shortage of certified Shariah scholars & risk professionals | -1.2% | Worldwide, emerging markets acute | Medium term (2–4 years) |

| Cyber-security vulnerabilities in digital Islamic banks/fintechs | -0.9% | Asia-Pacific & GCC hubs | Short term (≤ 2 years) |

| Climate-stress exposure of asset-heavy Islamic banks | -0.7% | GCC focused | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Fragmented Shariah Standards Across Jurisdictions

Lack of global alignment inflates compliance costs and blunts product scalability. Draft AAOIFI Standard 62, which would shift sukuk from asset-based to asset-backed, has seen deadlines extended amid industry debate[3]White & Case LLP, “AAOIFI Draft Shariah Standard 62 Explained,” White & Case, whitecase.com. Divergent adherence rates to AAOIFI rules create uneven playing fields and investor confusion. Malaysia’s model of embedding Sharia guidance into IFRS is one potential pathway, but it relies on deep collaboration with the IASB. Multinational Islamic banks must therefore juggle multiple rulings, hampering the Islamic finance market’s global integration.

Shortage of Certified Shariah Scholars & Risk Professionals

Demand for dual-skilled talent in fiqh and modern finance outstrips supply, constraining product development cycles. In Bangladesh, limited Sharia governance expertise contributed to liquidity bottlenecks in 2024, slowing sector growth. AI deployment in Islamic banking introduces fresh compliance questions that require scholarly oversight, widening the competence gap. While universities and professional bodies are scaling programs, the talent pipeline will lag market expansion for years.

Segment Analysis

By Financial Sector: Banking Dominance Amid Takaful Acceleration

Islamic banking contributed 68.45% to the Islamic finance market size in 2024, underscoring its centrality in deposit mobilization and credit creation. Steady corporate demand and scale advantages enable banks to sustain net-profit expansion, as Kuwait Finance House reported KD 482.9 million profit in Q3 2024, a 4.6% increase[4]Kuwait Finance House, “Q3 2024 Financial Results,” Kuwait Finance House, kfh.com. Meanwhile, the Takaful segment is projected to grow at 14.78% CAGR to 2030, the fastest clip in the Islamic finance market. Consolidation, such as the Dar Al Takaful–National Takaful merger, positions players to achieve economies of scale and richer digital servicing. Elevated awareness of protection needs after the pandemic and product bundling with Islamic mortgages further spur uptake. Capital-market segments follow: sukuk outstanding could eclipse USD 875 billion in 2024, while ESG-themed funds gain traction on institutional mandates.

Insurance scale-ups strengthen balance-sheet diversity as Takaful Malaysia’s revenue climbed to RM 862.5 million in Q2 FY 2024. Product customization to cater to SME workers and gig-economy earners widens the customer funnel. On the capital markets side, issuers such as Saudi Electricity, Malaysia’s sovereign, and Dubai real-estate developers use sukuk to tap long-dated liquidity at competitive spreads, anchoring the Islamic finance industry’s funding ecosystem. Funds focusing on renewable-energy sukuk and social-housing projects signal alignment with UN SDGs, an observation that draws global institutional investors seeking both yield and impact allocation.

Note: Segment shares of all individual segments are available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Customer Type: Business Segment Leadership with Retail Momentum

Businesses accounted for 57.32% of the Islamic finance market size in 2024 as corporates tapped Sharia-compliant revolving credit, trade finance, and sukuk to fund expansion. GCC banks reported double-digit loan growth, with Saudi lenders raising loan balances 14.4% in 2024. Retail, however, is projected to advance at 12.89% CAGR through 2030, reflecting mobile-first product roll-outs that ease account opening and micro-investment. Generation Z’s preference for speed and security over traditional religiosity shifts marketing messages toward lifestyle value propositions. Digital onboarding and biometric authentication cut processing time, further boosting adoption.

Mobile Hajj-saving wallets, buy-now-pay-later offerings, and Sharia robo-advisers make personal finance easier to navigate, encouraging first-time investors. Bank Muamalat aims to double bancassurance volumes by 2025 through protected mutual fund tie-ups. At the corporate end, sukuk-backed infrastructure financing in the Gulf and Southeast Asia sustains the pipeline of project finance, keeping the Islamic finance industry anchored to real-economy assets. Together, these trends showcase an increasingly balanced customer mix.

Geography Analysis

The Middle East & Africa retained 61.94% share of the Islamic finance market in 2024, propelled by UAE ambitions to reach AED 2.56 trillion in Islamic banking assets by 2031. Saudi Arabia’s top banks raised net profit by 13.5% in FY 2024 as Vision 2030 programs boosted credit demand. Sovereign wealth funds recycle oil receipts into sukuk and private-market vehicles, deepening liquidity. Nigeria, South Africa, and Egypt together issued USD 3.045 billion of sukuk in 2024, illustrating a new African appetite. Yet climate transition risk looms large for asset-heavy Gulf lenders, prompting early exploration of green-financing frameworks.

Asia-Pacific, the fastest-growing region, is expected to log a 13.28% CAGR from 2025 to 2030 as Indonesia’s merged Bank Syariah Indonesia climbs toward a global top-ten scale and opens international branches. Malaysia’s CIMB Islamic lifted profit before tax 26.4% year-on-year in Q3 2024, demonstrating mature market profitability. Pakistan’s planned system-wide Sharia transition could inject fresh momentum if execution hurdles such as sovereign debt restructuring are addressed. Regional regulators nurture fintech sandboxes, pushing the Islamic finance market toward mass-adoption stages.

Europe fills a niche as a structuring hub for USD-denominated sukuk, leveraging English law and deep capital markets expertise. The London Stock Exchange remains a listing venue of choice, while Gatehouse Bank extended Sharia home-finance through a £550 million deal with ColCap UK, lifting its portfolio past £1.2 billion. ING’s maiden USD 750 million sukuk for Turkey’s wealth fund underscores broader European involvement. Tailored tax relief in the UK on Islamic home-purchase plans eliminates previous frictions, pointing to a stable pipeline of retail products.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Competitive intensity is on the rise as digital-first entrants chip away at incumbent market share. Kuwait Finance House posted USD 1.58 billion profit in Q3 2024, supported by diversified product lines and expansion into Turkey after the Ahli United Bank acquisition. In parallel, Ruya’s 2025 launch of virtual-asset investment via mobile marks the Islamic finance market’s first cryptocurrency-linked retail product. Saudi Awwal Bank paired with HSBC to adopt AI-driven treasury tools, highlighting partnerships as a route to rapid capability building.

Banks pour capital into artificial intelligence chatbots, biometric onboarding, and predictive credit analytics. Bank Syariah Indonesia’s AI chatbot reduced average query resolution time to under two minutes, lifting customer satisfaction. Blockchain pilots on secondary sukuk trading plan to shrink settlement from two days to near-real time, freeing capital. Yet regulation remains fluid; AAOIFI Standard 62 could tilt the advantage to issuers flexible enough to structure asset-backed sukuk. Mergers such as Dar Al Takaful and National Takaful reveal a quest for scale and digital-investment headroom.

White-space opportunities include Sharia-compliant wealth management for mass-affluent customers, green-hydrogen project finance, and cross-border e-wallet remittances. Fintech startups backed by Saudi venture funds deploy micro-investing apps that blend ESG screening with profit-rate optimization, widening retail participation in the Islamic finance market. At the upper end, sovereign funds increasingly allocate to private equity and infrastructure inside Sharia wrappers, propping up deal flow for specialist managers.

Islamic Finance Industry Leaders

-

Al Rajhi Bank

-

Dubai Islamic Bank

-

Kuwait Finance House

-

Qatar Islamic Bank

-

Maybank Islamic

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Ruya launched virtual-asset investment services including Bitcoin via its mobile app, the first Islamic bank to do so, in partnership with Fuze.

- February 2025: Cenomi Centers secured SR 5.25 billion (USD 1.39 billion) sustainability-linked murabaha financing.

- December 2024: Bank Muamalat Indonesia launched Reksa Dana Syariah Terproteksi Insight Terproteksi Syariah IX, tapping 78.5% year-on-year AUM growth.

- November 2024: Bank Muamalat Indonesia became the first fully Sharia-compliant custodian bank licensed by OJK.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Islamic finance market as the aggregate value of assets, liabilities, and fee-based services that pass a recognized Sharia supervisory board, covering Islamic banking deposits and loans, sukuk outstanding, takaful contributions, Sharia-compliant investment funds, and other licensed Islamic financial institutions. According to Mordor Intelligence, figures are reported in current U.S. dollars and span more than seventy jurisdictions.

Scope Exclusions: We exclude unregulated crypto tokens lacking formal Sharia certification, as well as informal peer-to-peer lending circles.

Segmentation Overview

- By Financial Sector

- Islamic Banking

- Takaful (Islamic Insurance)

- Sukuk (Islamic Bonds)

- Islamic Funds

- Other Islamic Financial Institutions (OIFIs)

- By Customer Type

- Retail Consumers

- Businesses

- By Region

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- Kuwait

- Bahrain

- Oman

- Egypt

- Nigeria

- Rest of Middle East and Africa

- Asia-Pacific

- Malaysia

- Indonesia

- Pakistan

- Bangladesh

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Rest of Europe

- Rest of the World

- Middle East and Africa

Detailed Research Methodology and Data Validation

Primary Research

We conducted structured interviews with Sharia scholars, treasury heads at GCC and Southeast Asian banks, and Islamic fintech founders to validate certification practices, asset-mix shifts, and product-rollout timelines. Follow-up surveys with institutional investors and takaful managers sharpened assumptions on average ticket sizes and regional growth triggers.

Desk Research

We compiled macro-economic indicators, banking statistics, and Islamic capital-market bulletins from sources such as the Islamic Financial Services Board, IMF Financial Access Survey, and national sukuk prospectuses. Additional context on fintech adoption and ESG sukuk pipelines was gathered from leading academic journals, respected business dailies, and central-bank monetary reports. Our team also tapped Dow Jones Factiva for company filings and Questel for patent trends on blockchain-enabled settlement. This listing is illustrative; many more references informed data collection and validation.

Market-Sizing & Forecasting

Our model starts with a top-down asset reconstruction built from central-bank Islamic windows, sukuk registries, and takaful gross written premiums. It then corroborates totals with sampled balance-sheet roll-ups and average-spread analysis. Key variables like Muslim population growth, oil-price-linked liquidity, cross-border sukuk issuance volume, digital account penetration, and regulatory capital buffers feed a multivariate regression with scenario analysis. Bottom-up provider checks adjust any gaps, especially in emerging jurisdictions where disclosure remains thin.

Data Validation & Update Cycle

Modeled outputs pass three analyst reviews, where variance thresholds trigger re-contact of field sources. Reports refresh annually, and extraordinary events such as major policy shifts or large default episodes lead to interim updates. A final analyst pass ensures clients receive the latest view.

Why Mordor's Islamic Finance Baseline Commands Market Confidence

Published estimates often diverge because firms choose different asset buckets, convert currencies on different dates, and refresh models at uneven intervals.

Key gap drivers include whether sukuk are recorded at par or market value, if off-balance-sheet mudarabah pools are counted, and how fintech-related fee income is imputed before growth is compounded.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 5.47 Trn (2025) | Mordor Intelligence | |

| USD 5.98 Trn (2024) | Global Consultancy A | Combines conventional bank Islamic windows and applies year-end FX averages that inflate totals. |

| USD 5.00 Trn (2025) | Trade Journal B | Omits family takaful assets and uses a single growth factor without granular product validation. |

The comparison shows that Mordor analysts ground forecasts in verifiable regulatory filings, reconcile product-level detail, and refresh data soon after fiscal releases, giving decision-makers a balanced, transparent baseline they can trace and replicate.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current size of the Islamic finance market?

The Islamic finance market reached USD 5.47 trillion in 2025 and is projected to rise to USD 9.31 trillion by 2030.

Which region is growing fastest in Islamic finance?

Asia-Pacific leads with a forecast 13.28% CAGR for 2025-2030, driven by Indonesia’s digital banking and Malaysia’s fintech ecosystem.

Which segment shows the highest growth potential?

Takaful insurance is forecasted to expand at 14.78% CAGR, outpacing banking and fund-management segments.

How important are ESG considerations in Islamic finance?

Green sukuk already accounts for 10% of global sukuk issuance and is expanding quickly as investors align Sharia compliance with sustainability objectives.

What are the main challenges facing the industry?

Fragmented Sharia standards, talent shortages in certified scholars, cyber-security risks in digital platforms, and climate-stress exposure among Gulf banks are the key restraints.

Are digital assets compatible with Islamic banking?

Banks such as Ruya have introduced Sharia-compliant virtual-asset services, indicating growing acceptance when transparency and asset-backing conditions are met.

Page last updated on: