Hydropower Market Size

| Study Period | 2020 - 2030 |

| Market Volume (2025) | 1.41 terawatt |

| Market Volume (2030) | 1.49 terawatt |

| CAGR | 1.02 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Hydropower Market Analysis

The Hydropower Market size is estimated at 1.41 terawatt in 2025, and is expected to reach 1.49 terawatt by 2030, at a CAGR of 1.02% during the forecast period (2025-2030).

The hydropower industry continues to evolve as a cornerstone of global renewable energy infrastructure, with significant technological advancements and policy developments shaping its trajectory. Hydropower remains a dominant force in the renewable energy landscape, representing approximately 40% of installed capacity and 50% of electricity generation in North America, highlighting its crucial role in regional power systems. The industry is witnessing a shift toward the modernization of existing facilities, with many countries focusing on upgrading aging hydropower infrastructure rather than developing new large-scale projects. This trend is particularly evident in developed markets where optimal sites for large hydropower installations are already utilized.

The market is experiencing a notable transition toward smaller-scale hydropower projects and pumped storage hydropower facilities, particularly in mature markets. The global small hydropower potential stands at approximately 229 GW, presenting significant opportunities for development in regions with untapped resources. Feed-in tariffs supporting small hydropower development are now present in 50 countries worldwide, demonstrating strong policy support for this segment. This shift is driven by environmental considerations and the need for more distributed power generation systems that can better integrate with other renewable energy sources.

Technological innovation is revolutionizing the hydropower sector, with advanced digital solutions and automation systems being implemented to enhance operational efficiency and reduce maintenance costs. Major infrastructure projects are incorporating cutting-edge technologies, as exemplified by recent developments such as the Wudongde Hydropower Station in China and the approval of the Snowy Hydro 2.0 project in Australia. These projects showcase the industry's commitment to implementing state-of-the-art solutions that optimize hydropower generation while minimizing environmental impact.

The industry is witnessing a significant geographical shift in development focus, with emerging markets taking the lead in new project implementations. Africa presents particularly promising opportunities, with only 11% of its technical hydropower potential currently utilized, representing the highest percentage of untapped potential globally. This untapped potential, combined with increasing energy demands in developing regions, is driving substantial investments in new hydropower infrastructure. The sector is also seeing increased interest in hybrid projects that combine renewable hydropower with other renewable energy sources, creating more resilient and flexible power generation systems.

Hydropower Market Trends

Growing Investment in Large-Scale Hydropower Projects

The hydropower market is experiencing substantial momentum driven by significant capital investments in new projects and hydropower infrastructure modernization. According to the International Renewable Energy Agency, global investment in hydropower reached USD 7.55 billion in 2022, demonstrating a strong commitment to hydroelectric development. This investment trend is further evidenced by major project announcements, such as Drax Group PLC's USD 616 million investment in the Cruachan power station in May 2022, which aims to add 600 MW of underground pumped storage hydropower capacity. The scale of these investments reflects growing confidence in hydroelectric power as a reliable renewable energy source and its ability to meet increasing electricity demands.

Recent developments in 2023 have further reinforced this investment trend, with significant projects being announced across various regions. For instance, in May 2023, China's National Development and Reform Commission (NDRC) approved the construction of a new hydropower plant in the Xizang Autonomous Region with capital backing of approximately USD 8.43 billion, projected to generate over 11.28 billion kilowatt-hours annually. Similarly, India's approval of a USD 3.9 billion investment for the 2,880 MW Dibang hydropower project in February 2023 demonstrates the continuing commitment to large-scale hydropower development. These investments are particularly focused on developing both conventional hydroelectric dams and pumped storage facilities, which are crucial for meeting peak electricity demands and ensuring grid stability.

Shift Towards Clean Energy Sources

The global imperative to reduce carbon emissions and transition to cleaner energy sources has emerged as a significant driver for hydropower market growth. Large-scale hydropower facilities have become increasingly attractive as they can generate substantial amounts of clean electricity while providing the flexibility to meet fluctuating power demands throughout the day. This advantage is particularly valuable as countries worldwide establish ambitious clean energy targets and phase out fossil fuel-based power generation. For example, China's commitment to achieving carbon neutrality by 2060 and its target to peak coal consumption by 2025 has directly contributed to increased investment and development in hydropower infrastructure.

The reliability and scalability of hydropower as a clean energy source have made it an essential component of national renewable energy strategies. Unlike intermittent renewable sources such as wind and solar, large-scale hydropower facilities can be easily turned on and off, making them more dependable for meeting peak electricity demands. This operational flexibility, combined with the ability to store energy through pumped storage systems, positions hydropower as a crucial enabler of the clean energy transition. The technology's ability to provide both baseload power and grid stabilization services has made it particularly valuable for countries seeking to reduce their dependence on fossil fuels while maintaining energy security.

Supportive Government Policies and Regional Cooperation

Government policies and regional cooperation initiatives have emerged as crucial drivers for hydropower market development, particularly in regions with significant untapped potential. The implementation of supportive regulatory frameworks and cross-border energy trade agreements has created favorable conditions for hydropower development. For instance, the Lao government's strategic plan to export around 20,000 MW of electricity to neighboring countries by 2030 has catalyzed the development of multiple hydropower projects, including plans to complete 12 hydropower dam projects with a combined capacity of 1,950 MW. These initiatives demonstrate how government support can facilitate both domestic energy security and regional economic integration through hydropower development.

The establishment of long-term energy policies and investment frameworks has provided the stability needed for large-scale hydropower projects, which typically require significant capital investment and extended construction periods. Governments are increasingly recognizing hydropower's role in achieving multiple policy objectives, including energy security, climate change mitigation, and economic development. This recognition has led to the implementation of various support mechanisms, such as streamlined permitting processes, investment incentives, and power purchase agreements, which have collectively enhanced the attractiveness of hydropower investments. The coordination between different government agencies and regional authorities has also improved project implementation efficiency and reduced development risks.

Extensive Untapped Hydropower Potential

The significant untapped hydropower potential across various regions continues to drive market expansion and investment opportunities. Many countries, particularly in Southeast Asia and developing regions, possess substantial unexploited hydropower resources that could be developed to meet growing energy demands. The technical feasibility of these untapped resources, combined with advancing hydropower technology and construction methods, has made previously challenging projects more viable. This potential extends beyond large-scale projects to include opportunities for modernizing existing hydropower infrastructure and developing new pumped storage facilities to support grid stability.

The development of untapped hydropower resources is particularly significant in regions experiencing rapid economic growth and urbanization. These areas require reliable and scalable power generation solutions that can support industrial development while maintaining environmental sustainability. The ability to develop hydropower projects of varying scales, from large conventional dams to run-of-river installations, provides flexibility in matching power generation capabilities with local needs and geographical conditions. Furthermore, the modernization of aging hydropower infrastructure in developed markets presents additional opportunities for capacity expansion and efficiency improvements, contributing to the overall growth of the hydropower sector.

Segment Analysis: Size

Large Hydropower Segment in Global Hydropower Market

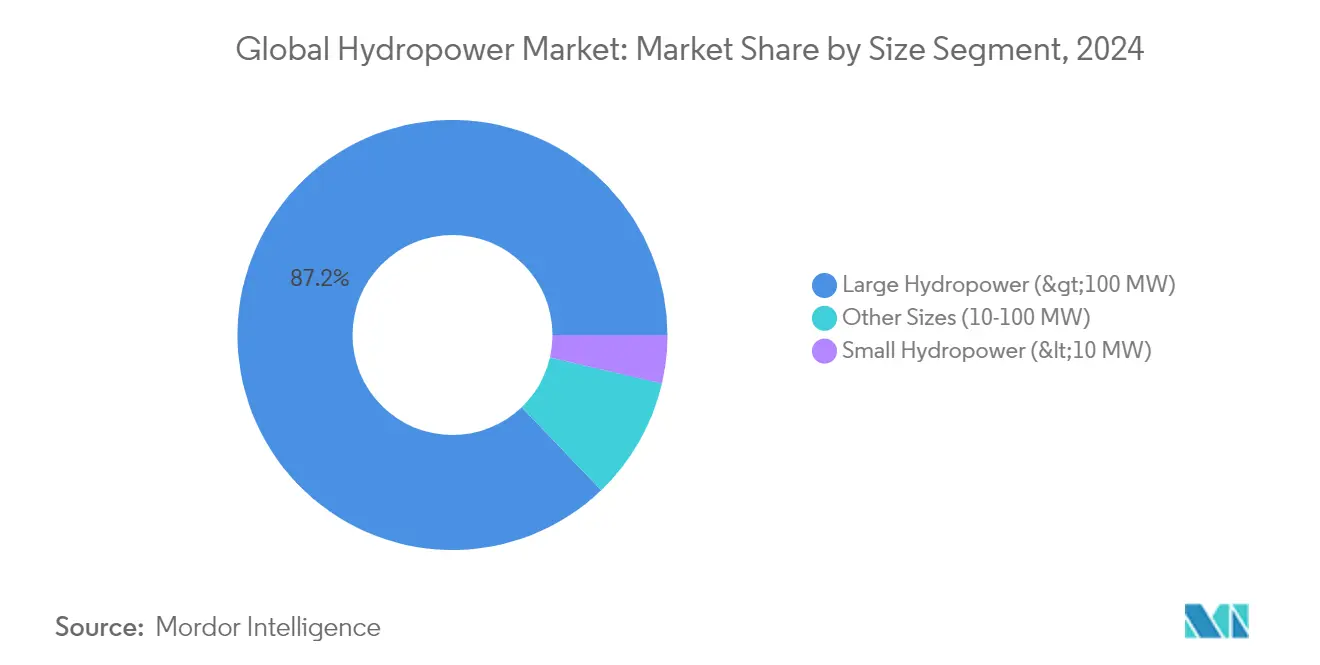

Large hydropower installations, with capacities exceeding 100 MW, continue to dominate the global hydropower market, accounting for approximately 87% of the total installed capacity in 2024. This segment's dominance is primarily driven by its ability to generate massive amounts of electricity at low operational costs, especially for large urban centers. The levelized cost of energy (LCOE) for large-scale hydropower projects at high-performing sites can be as low as USD 0.020/kWh, making it one of the most cost-effective renewable energy sources. Countries like China, Brazil, the United States, Canada, India, and Japan remain the major players in large-scale hydropower generation, with several significant projects under development or expansion.

Small Hydropower Segment in Global Hydropower Market

The small hydropower segment, comprising installations below 10 MW capacity, is experiencing rapid growth in the hydropower market from 2024-2029. This growth is primarily driven by increasing government support through feed-in tariffs (FITs) and other incentive schemes across various regions. The segment's expansion is particularly notable in Asia-Pacific, where countries are actively developing their small hydropower potential. The segment benefits from lower environmental impact, reduced construction costs, and faster implementation timelines compared to large hydropower projects. Additionally, small hydropower projects are often exempt from forest and land clearance requirements in many countries, making them more attractive for development in environmentally sensitive areas.

Remaining Segments in Size Segmentation

The medium-scale hydropower segment (10-100 MW) serves as a crucial bridge between large and small hydropower installations, particularly well-suited for medium urban population centers. This segment offers a balanced approach, providing significant power generation capacity while maintaining relatively lower environmental impacts compared to large-scale projects. Medium-scale hydropower plants have become increasingly important in regions like Asia-Pacific, Europe, and North America, where they help diversify the hydropower portfolio and provide flexible power generation options for grid stability.

Hydropower Market Geography Segment Analysis

Hydropower Market in North America

North America represents a mature and well-established hydropower market, accounting for approximately 15% of global installed capacity in 2024. The region's hydropower infrastructure is characterized by a mix of large-scale facilities and pumped storage projects, with significant installations across the United States and Canada. The market benefits from extensive river systems, particularly in the Pacific Northwest and Quebec regions, which provide ideal conditions for hydroelectric generation. Technological advancements in modernizing aging infrastructure and upgrading existing facilities have become key focus areas for market participants. The region's regulatory framework strongly supports renewable energy development, with hydropower playing a crucial role in achieving clean energy targets. Market dynamics are influenced by factors such as grid reliability requirements, increasing demand for renewable energy storage solutions, and the need for flexible power generation to complement other renewable sources. The emphasis on environmental protection and indigenous rights considerations continues to shape new project developments and existing facility operations.

Hydropower Market in Europe

Europe's hydropower market has demonstrated steady development, recording approximately 8% growth from 2019 to 2024. The region's market is characterized by a strong focus on modernizing existing facilities and developing pumped storage capabilities to support grid stability. Countries like Norway, Turkey, and France lead the regional market with substantial installed capacities and continued investment in infrastructure development. The European market distinguishes itself through its advanced technological implementations and strong focus on environmental sustainability in hydropower operations. Integration with other renewable energy sources has become a key priority, with hydropower facilities increasingly serving as flexible power generation assets. The region's regulatory framework emphasizes sustainable development practices and cross-border power trading capabilities. Market participants are actively investing in digitalization and automation technologies to enhance operational efficiency and grid integration capabilities. The region's commitment to carbon neutrality continues to drive investment in hydropower infrastructure, particularly in small-scale and pumped storage projects.

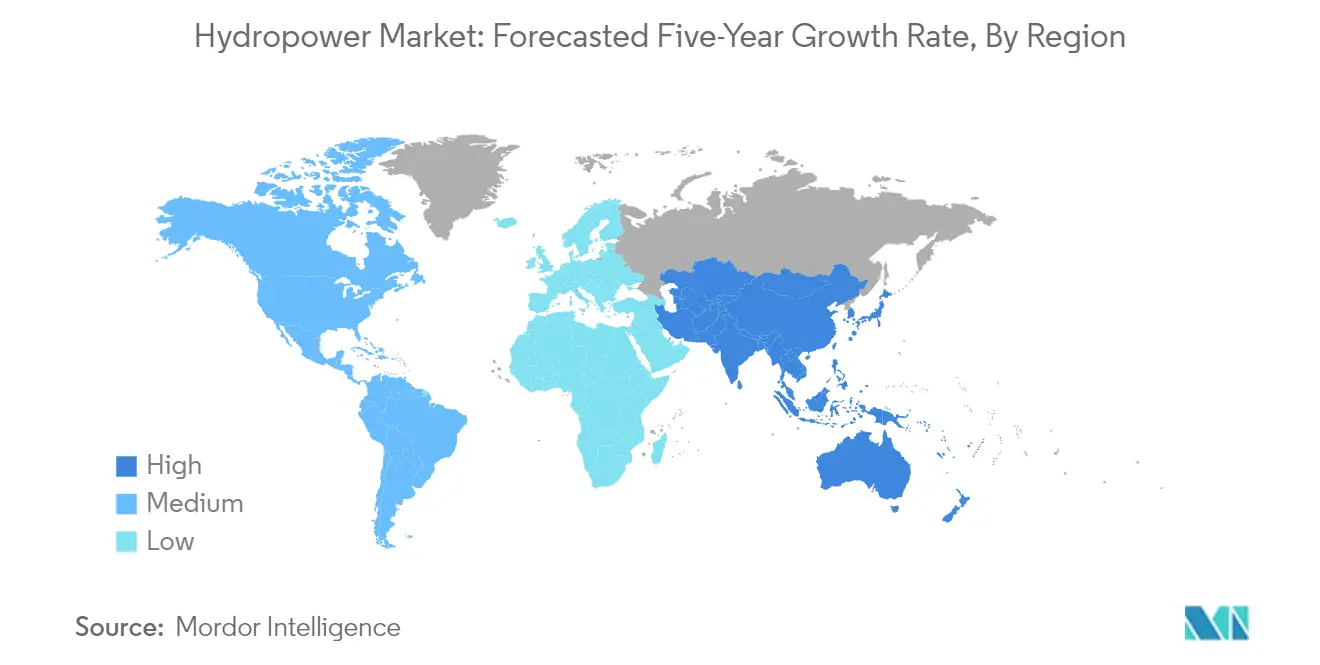

Hydropower Market in Asia-Pacific

The Asia-Pacific region maintains its position as the global leader in hydropower development, with projections indicating approximately 2% annual growth from 2024 to 2029. The region's market is characterized by significant investments in large-scale projects, particularly in countries like China, India, and Southeast Asian nations. Infrastructure development continues to be driven by rapid urbanization, increasing electricity demand, and strong government support for renewable energy initiatives. The market demonstrates a balanced approach between developing new large-scale projects and promoting small hydropower installations for rural electrification. Technological innovation focuses on improving efficiency and reducing environmental impact, with increased attention to sustainable development practices. Regional cooperation in cross-border hydropower projects has become increasingly important, particularly in the Mekong River region. The market benefits from strong government support through favorable policies and investment incentives, while also addressing environmental and social considerations in project development.

Hydropower Market in South America

South America's hydropower market continues to evolve as a crucial component of the region's energy infrastructure, with Brazil leading the development landscape. The region benefits from abundant water resources and favorable geographical conditions for hydroelectric generation. Market development is characterized by a balanced approach between large-scale projects and smaller installations to serve remote communities. Environmental considerations and indigenous community rights play a significant role in project planning and development. The region's market demonstrates an increasing focus on modernizing existing facilities while carefully expanding capacity through new projects. Integration with other renewable energy sources has become a key priority to ensure grid stability and reliable power supply. The market shows strong potential for future growth, supported by increasing electricity demand and government commitments to renewable energy development.

Hydropower Market in Middle East & Africa

The Middle East and Africa region represents an emerging hydropower market with significant untapped potential in the global hydropower landscape. The market is characterized by varying levels of development across different countries, with notable progress in nations like Ethiopia and Angola. Development focuses on both large-scale projects for urban centers and smaller installations for rural electrification. Regional cooperation in river basin management has become increasingly important for sustainable market development. The market benefits from increasing investment in infrastructure development and growing recognition of hydropower's role in achieving renewable energy targets. Technological advancement focuses on adapting solutions to local conditions while ensuring sustainable development practices. The region demonstrates strong potential for future growth, supported by increasing electricity demand and government initiatives to expand renewable energy capacity.

Hydropower Industry Overview

Top Companies in Hydropower Market

The global hydropower market features prominent players like General Electric, Siemens AG, Andritz AG, Voith GmbH, China Yangtze Power, RusHydro, EDF, and Iberdrola SA leading the industry through continuous innovation and strategic expansion. These hydropower companies are increasingly focusing on digitalization and automation solutions to enhance operational efficiency and plant performance, with particular emphasis on predictive maintenance and smart monitoring systems. The industry witnesses regular collaborations between equipment manufacturers and utility companies to develop advanced hydropower technology and modernize existing hydropower infrastructure. Companies are expanding their geographical presence through strategic partnerships and joint ventures, particularly in emerging markets with untapped hydropower potential. Environmental sustainability and regulatory compliance remain key drivers of product development and operational strategies, with companies investing heavily in research and development to minimize ecological impact while maximizing power generation efficiency.

Market Structure Shows Strong Regional Leadership

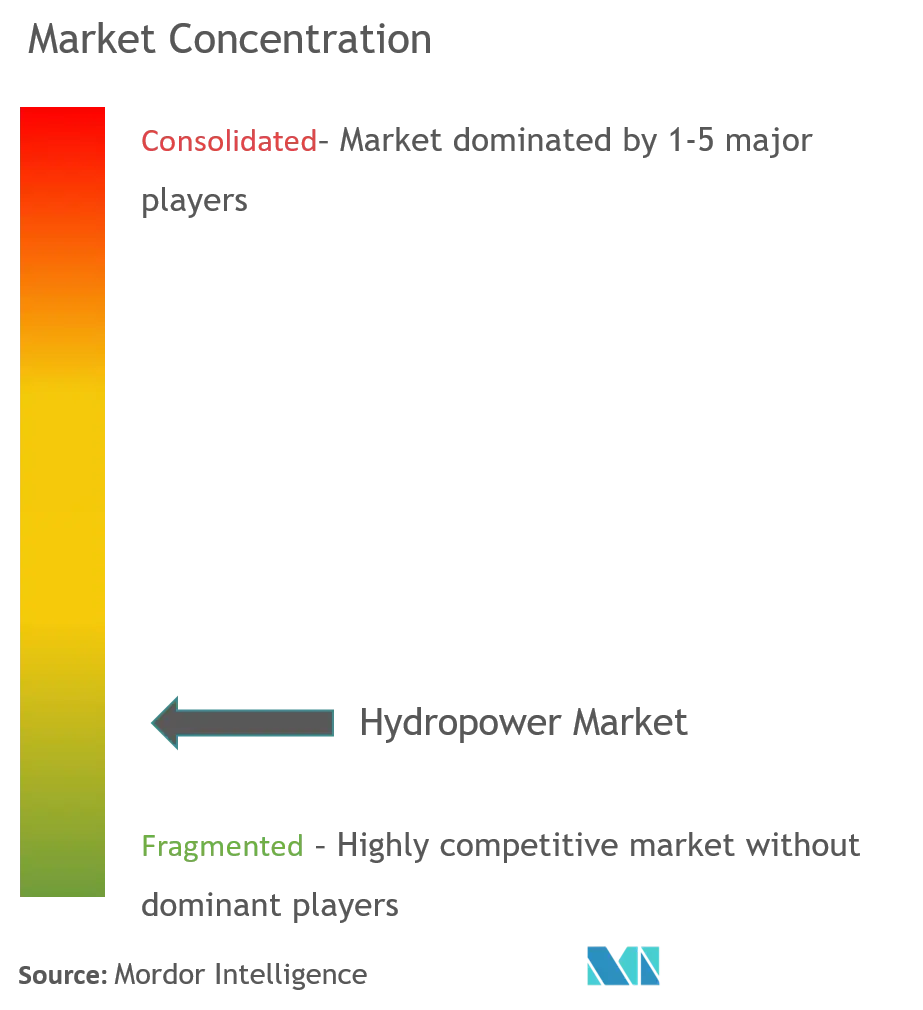

The hydropower market exhibits a unique structure characterized by both global technology providers and regional operators, with different players dominating various segments of the value chain. Equipment manufacturers like GE and Siemens operate globally, providing comprehensive solutions from turbines to digital systems, while regional utilities like China Yangtze Power and RusHydro maintain strong local market positions through their extensive operational expertise and government relationships. The market demonstrates moderate consolidation in hydropower equipment manufacturing but remains relatively fragmented in terms of hydropower generation and operation, particularly in developing regions where state-owned enterprises play significant roles.

The industry has witnessed significant merger and acquisition activity, particularly focused on technology acquisition and market expansion. Major conglomerates are acquiring specialized hydropower technology firms to enhance their digital capabilities and modernize their product offerings. Joint ventures and strategic partnerships have become increasingly common, especially in emerging markets where local knowledge and government relationships are crucial for project development. The trend toward consolidation is particularly evident in the small and medium-sized hydropower segment, where larger companies are acquiring regional players to expand their portfolio and geographical presence.

Innovation and Sustainability Drive Future Success

For established players to maintain and expand their market share, a multi-faceted approach combining technological innovation, operational excellence, and strategic partnerships is essential. Companies must invest in developing advanced digital solutions and automation technologies while maintaining strong relationships with government entities and utilities. The ability to offer comprehensive solutions that address environmental concerns while maximizing operational efficiency will become increasingly important. Market leaders need to focus on developing flexible and scalable solutions that can adapt to varying project sizes and local conditions, while also maintaining strong after-sales service networks.

New entrants and challenger companies can gain ground by focusing on specialized market segments or geographical regions where they can build a strong local presence and expertise. Success factors include developing cost-effective solutions for small and medium-sized projects, establishing strategic partnerships with established players for technology access, and building strong relationships with local stakeholders. The regulatory environment continues to evolve with increasing emphasis on environmental protection and social impact, requiring companies to demonstrate strong compliance capabilities and sustainable practices. The concentration of end-users in the utility sector necessitates long-term relationship building and strong track records in project delivery and operational reliability.

Hydropower Market Leaders

-

GE Renewable Energy

-

Siemens Energy AG

-

Andritz AG

-

Voith GmbH & Co. KGaA

-

PJSC RusHydro

*Disclaimer: Major Players sorted in no particular order

Hydropower Market News

- May 2023: Satluj Jal Vidyut Nigam (SJVN) of India has been granted permission by Nepal to develop a second hydropower project in the country. Currently, the firm is developing a 900-MW Arun-III hydroelectric project located on the Arun River in Eastern Nepal. This project is scheduled to be completed in 2024. Investment Board Nepal (IBN) has approved to build of the 669 MW Lower Arun hydropower project in eastern Nepal.

- December 2022: China announced the completion of its second-largest hydropower facility, the Baihetan hydropower plant, on the upstream branch of the Yangtze River. This facility will be equipped with 16 one-GW turbines.

Hydropower Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Installed Capacity and Forecast in GW, till 2029

4.3 Recent Trends and Developments

4.4 Government Policies and Regulations

4.5 Market Dynamics

4.5.1 Drivers

4.5.1.1 Rising Demand for Reliable Electricity

4.5.1.2 Increasing Government Support for Hydropower Gneeration

4.5.2 Restraints

4.5.2.1 Negative Environmental Consequences of Hydropower Projects

4.6 Supply Chain Analysis

4.7 Porter's Five Forces Analysis

4.7.1 Bargaining Power of Suppliers

4.7.2 Bargaining Power of Consumers

4.7.3 Threat of New Entrants

4.7.4 Threat of Substitutes Products and Services

4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Size

5.1.1 Large Hydropower (Greater Than 100 MW)

5.1.2 Small Hydropower (Smaller Than 10 MW)

5.1.3 Other Sizes (10-100 MW)

5.2 Geography

5.2.1 North America

5.2.1.1 United States

5.2.1.2 Canada

5.2.1.3 Rest of North America

5.2.2 Europe

5.2.2.1 Germany

5.2.2.2 France

5.2.2.3 United Kingdom

5.2.2.4 Rest of Europe

5.2.3 Asia-Pacific

5.2.3.1 China

5.2.3.2 India

5.2.3.3 Japan

5.2.3.4 South Korea

5.2.3.5 Rest of Asia-Pacific

5.2.4 South America

5.2.4.1 Brazil

5.2.4.2 Argentina

5.2.4.3 Rest of South America

5.2.5 Middle East and Africa

5.2.5.1 Saudi Arabia

5.2.5.2 United Arab Emirates

5.2.5.3 South Africa

5.2.5.4 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 GE Renewable Energy

6.3.2 Siemens Energy AG

6.3.3 Andritz AG

6.3.4 Voith GmbH & Co. KGaA

6.3.5 China Yangtze Power Co. Ltd

6.3.6 PJSC RusHydro

6.3.7 Électricité de France SA (EDF)

6.3.8 Iberdrola SA

- *List Not Exhaustive

6.4 Market Ranking/Share Analysis

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

7.1 Emerging Technological Trends Aimed at Increasing Hydropower Generation

Hydropower Industry Segmentation

Hydropower is one of the largest and oldest renewable energy sources, and it uses the natural flow of moving water to produce electricity. Hydropower is also applied as half of an energy storage system known as pumped-storage hydroelectricity. It is an alternative source of electricity production for fossil fuels as it doesn't directly produce carbon emissions.

The hydropower market is segmented by type and geography. By type, the market is segmented into large hydropower (greater than 100 MW), small hydropower (smaller than 10 MW), and other sizes (10-100 MW). The report also covers the size and forecasts of the power market across major regions. For each segment, the market sizing and forecasts have been done based on installed capacity in terawatts (TW).

| Size | |

| Large Hydropower (Greater Than 100 MW) | |

| Small Hydropower (Smaller Than 10 MW) | |

| Other Sizes (10-100 MW) |

| Geography | |||||||

| |||||||

| |||||||

| |||||||

| |||||||

|

Hydropower Market Research FAQs

How big is the Hydropower Market?

The Hydropower Market size is expected to reach 1.41 terawatt in 2025 and grow at a CAGR of 1.02% to reach 1.49 terawatt by 2030.

What is the current Hydropower Market size?

In 2025, the Hydropower Market size is expected to reach 1.41 terawatt.

Who are the key players in Hydropower Market?

GE Renewable Energy, Siemens Energy AG, Andritz AG, Voith GmbH & Co. KGaA and PJSC RusHydro are the major companies operating in the Hydropower Market.

Which is the fastest growing region in Hydropower Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Hydropower Market?

In 2025, the Asia Pacific accounts for the largest market share in Hydropower Market.

What years does this Hydropower Market cover, and what was the market size in 2024?

In 2024, the Hydropower Market size was estimated at 1.40 terawatt. The report covers the Hydropower Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Hydropower Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Hydropower Market Research

Mordor Intelligence provides a comprehensive analysis of the hydropower industry. We leverage extensive expertise in both renewable hydropower and hydropower technology research. Our detailed examination spans the complete spectrum, from large hydropower installations to micro hydropower and mini hydropower systems. This includes an analysis of pumped storage hydropower facilities. The report offers an in-depth look at hydropower infrastructure, hydroelectric facility operations, and hydropower generation capabilities. We pay particular attention to the water turbine and hydro turbine technologies used in modern hydropower plant installations.

Stakeholders across the hydropower market can benefit from our actionable insights. These insights are available in an easy-to-download report PDF format that examines global hydropower market dynamics. The analysis covers hydropower equipment specifications, profiles of water power companies, and emerging trends in hydro power development. Our research supports decision-making for hydroelectric power investments. It covers opportunities in the small hydropower market as well as developments in the large-scale hydropower generation market. The report provides valuable insights into water energy utilization, hydraulic power systems, and advancing hydropower technology. This enables stakeholders to optimize their market strategies and operational efficiency.