High-End Semiconductor Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 41.57 Billion |

| Market Size (2030) | USD 85.11 Billion |

| Growth Rate (2025 - 2030) | 15.41% CAGR |

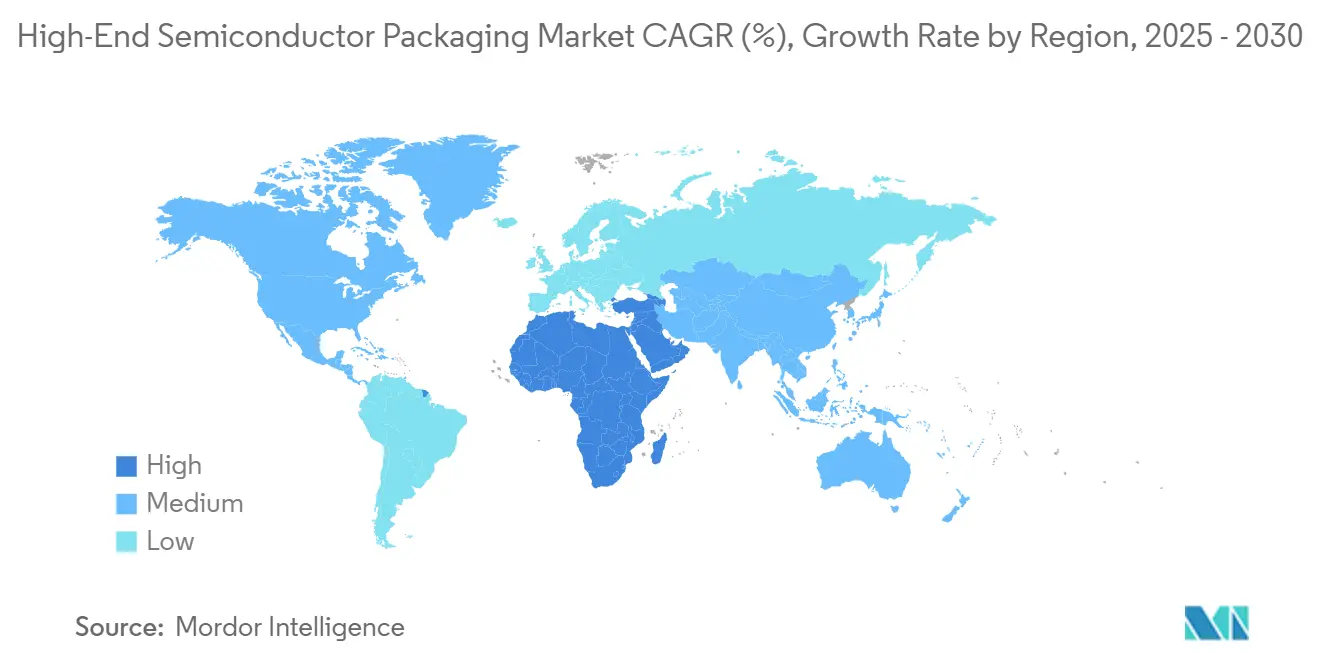

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

High-End Semiconductor Packaging Market Analysis by Mordor Intelligence

The high-end semiconductor packaging market size reached USD 41.57 billion in 2025 and is forecast to reach USD 85.11 billion by 2030, advancing at a 15.41% CAGR. Robust capital flows toward heterogeneous integration, surging AI accelerator demand, and substrate innovations together reinforce a strong growth trajectory. Foundry vertical integration amplifies competitive pressure on traditional outsourced assembly and test (OSAT) vendors while improving time-to-market for AI chips. Sub-5 nm migration by smartphone and automotive system-on-chip (SoC) suppliers fuels incremental volume for fan-out and silicon interposer platforms. Regional policy incentives, from the U.S. CHIPS Act to Europe’s APECS hub, are reshaping supply-chain geography, prompting multinational firms to diversify advanced packaging footprints. Meanwhile, substrate shortages and thermal-density limits temper near-term capacity ramps but simultaneously open opportunities for toolmakers and materials specialists that mitigate these bottlenecks.

Key Report Takeaways

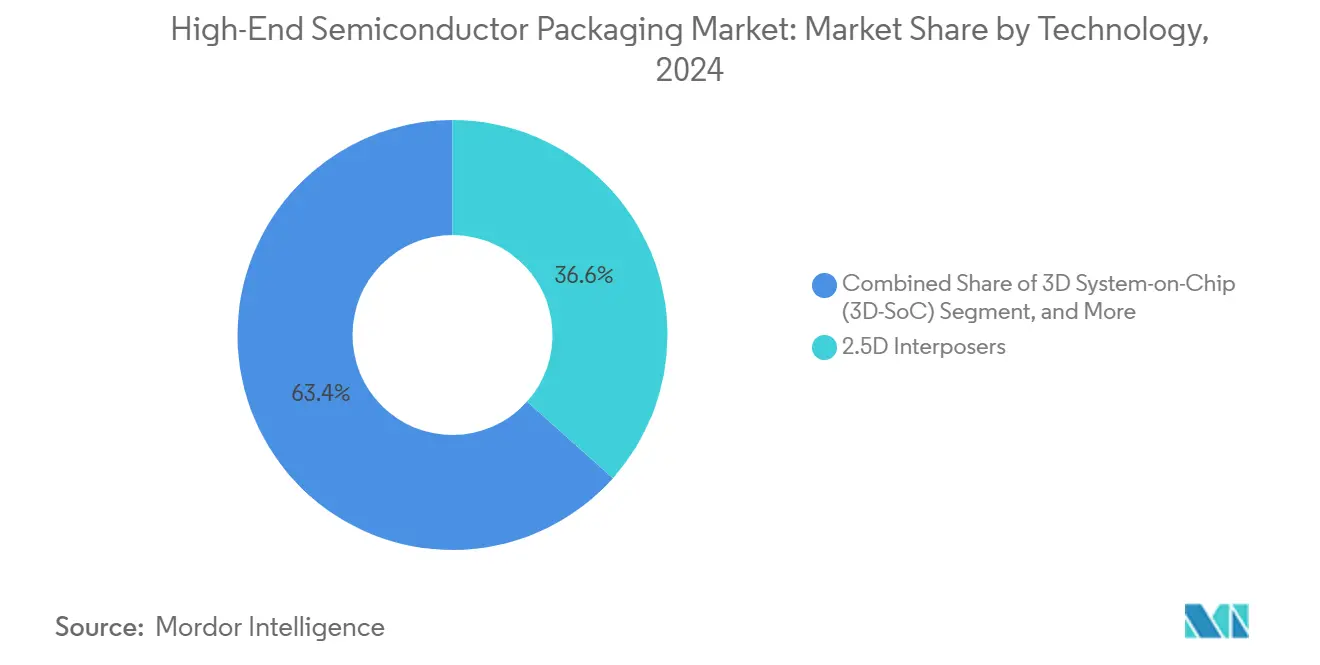

- By technology, 2.5 D interposers led with 36.60% revenue share in 2024, whereas 3 D System-on-Chip is projected to advance at a 16.64% CAGR through 2030.

- By packaging platform, flip-chip ball-grid-array dominated with 43.20% of 2024 sales, while panel-level packaging is set to climb at a 16.84% CAGR to 2030.

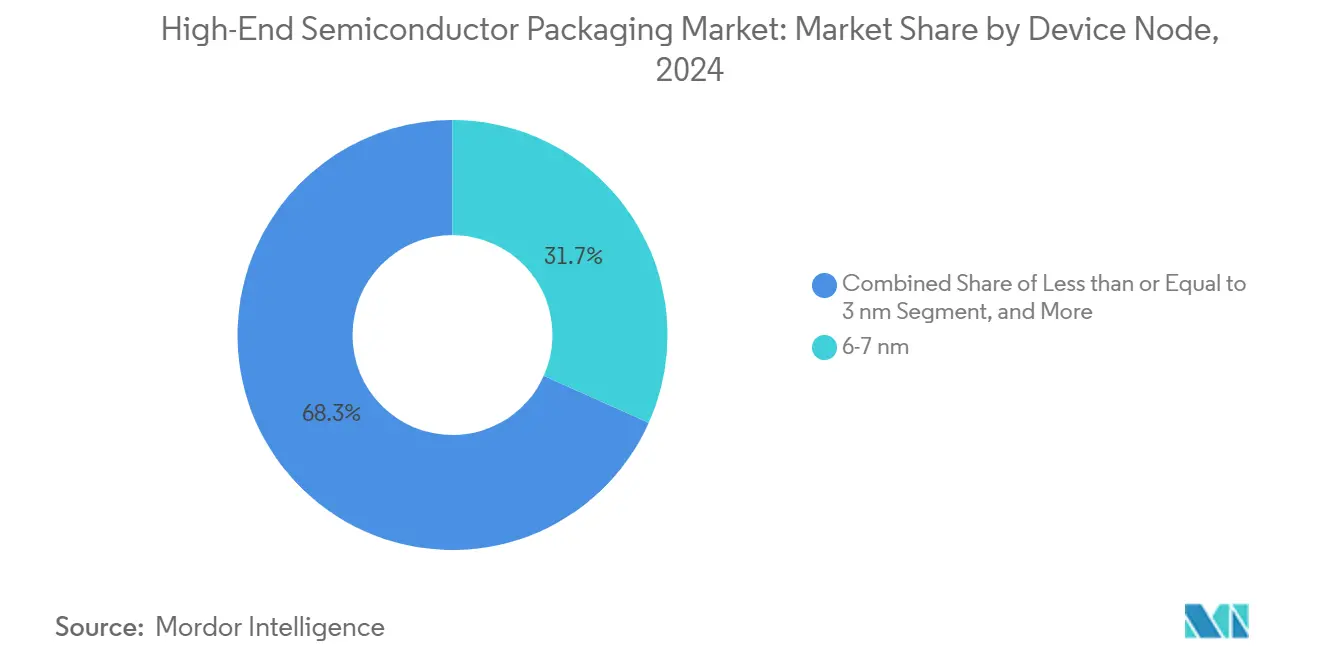

- By device node, the 6-7 nm tier captured 31.70% market share in 2024, yet sub-3 nm packages are forecast to post the fastest 18.24% CAGR through 2030.

- By end user, consumer electronics accounted for 29.30% of 2024 revenue, whereas automotive and ADAS applications are expanding at a 17.85% CAGR to 2030.

- By geography, Asia-Pacific held 59.30% of 2024 turnover, but the Middle East and Africa region is expected to register the quickest 18.63% CAGR through 2030.

Global High-End Semiconductor Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for AI/ML accelerators | +4.20% | Global, concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Smartphone migration to advanced nodes | +3.10% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Heterogeneous integration road-maps of IDMs/OSATs | +2.80% | Global, led by Taiwan and South Korea | Long term (≥ 4 years) |

| Adoption of chip-lets for LEO satellite payloads | +1.40% | North America and Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Growth of Chip-on-Wafer-on-Substrate (CoWoS-R) for HPC reticles | +2.60% | Asia-Pacific dominance, North America demand | Short term (≤ 2 years) |

| Government-funded 'More-than-Moore' pilot lines in Europe | +1.30% | Europe, with technology transfer to global markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for AI/ML Accelerators

Hyperscale data-center operators pivot to multi-die AI processors that fuse >1,000 W compute tiles with stacked high-bandwidth memory, driving an unprecedented requirement for advanced thermal and power delivery inside the high-end semiconductor packaging market.[1]TSMC, “Advanced Packaging Technology Platform,” tsmc.com Capacity for CoWoS and similar interposer platforms remains tight, elevating packaging lead-times to critical-path status for AI product launches. Foundries leveraging system-on-wafer concepts promise 10× memory bandwidth over current GPUs, further intensifying thermal engineering challenges. Vendors that master warpage control, micro-bump reliability, and liquid-coolable substrates gain pricing power as they enable hyperscalers to meet rollout schedules. Consequently, packaging capability is now viewed by system architects as a primary determinant of AI training cost and time.

Smartphone Migration to Advanced Nodes

Premium smartphone chipmakers are transitioning toward 3 nm and 2 nm production nodes, but rising wafer cost forces parallel advances in fan-out wafer-level and embedded bridge packaging to deliver performance within cost envelopes.[2]IEEE, “Advanced Semiconductor Packaging Technologies for AI Applications,” ieeexplore.ieee.org Chinese handset brands accelerate adoption of domestic OSAT services following capacity acquisitions such as JCET’s USD 624 million expansion, localizing value chains, and balancing geopolitical risk. Power-budget gains derived from finer nodes translate into longer battery life and richer on-device AI experiences; however, the tighter pitch requires redistribution layers with sub-2 µm line-and-space and ultra-thin dielectrics. Equipment suppliers innovating in polymer chemistries and plasma etch achieve a competitive advantage by enabling high volume yields at these geometries.

Heterogeneous Integration Road-maps of IDMs/OSATs

Industry frontrunners embrace chiplet architectures that combine analog, digital, RF, and memory tiles inside a single advanced package to circumvent cost and yield constraints of monolithic SoCs.[3]Intel Corporation, “Foveros 3D Packaging Technology,” intel.com This evolution expands addressable content for the high-end semiconductor packaging market as die-to-die interconnect density scales toward 1 Tb/s per millimeter. Government-backed open-access hubs in Europe lower the barrier for smaller design houses to adopt chiplets, increasing ecosystem diversity. Standardization efforts such as Bunch-of-Wires (BoW) and UCIe reduce integration risk and accelerate design cycles, increasing volume for both organic and silicon interposers. The long-term upside is a broader customer base for premium packaging services outside the traditional top-ten semiconductor vendors.

Growth of CoWoS-R for HPC Reticles

CoWoS-R integrates logic dies with HBM stacks on silicon interposers engineered for >10 TB/s bandwidth, a cornerstone for high-performance computing road-maps at cloud providers. TSMC channeling 10-20% of its USD 38-42 billion 2025 capex toward new interposer lines signals confidence in the multi-die AI future demand.[4]TSMC, “Advanced Packaging Technology Platform,” tsmc.com Nevertheless, shortages in T-glass and ABF substrates stretch lead times beyond six months, compelling GPU vendors to align launch calendars with packaging availability. Equipment makers able to boost via-fill throughput and plasma clean uniformity see rising orders as fabs chase yield improvements. The medium-term scenario suggests double-digit pricing premiums for interposer capacity, elevating gross margins for suppliers that scale first.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating capital intensity | -2.80% | Global, most acute in advanced manufacturing regions | Long term (≥ 4 years) |

| Yield management complexity beyond 5 nm | -2.10% | Asia-Pacific and North America leading-edge fabs | Medium term (2-4 years) |

| Sub-strate supply bottlenecks for organic interposers | -1.60% | Global supply chain, concentrated impact in Asia-Pacific | Short term (≤ 2 years) |

| Non-uniform thermal dissipation in 3D-SoC stacks | -1.40% | Global, affecting all high-performance applications | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Capital Intensity

Industry capital intensity climbed from 18% in 2015 to 30% in 2023 and is expected to remain above 30% as next-generation packaging lines require EUV-litho-grade cleanrooms and back-end tools costing hundreds of millions of dollars. Mid-tier OSATs face balance-sheet stress, prompting consolidation or joint ventures with foundries wielding deep pockets. Equipment expenditures now rival front-end fab outlays, with projections exceeding USD 460 billion industry-wide by 2033. Even leading toolmakers such as ASMPT reported 10% revenue contraction in 2024, underscoring the volatility inherent in capex-heavy cycles.[5]ASMPT, “Financial Reports,” asmpt.com In the long term, only geographically diversified players with scale and differentiated process IP can fund successive technology nodes.

Yield Management Complexity Beyond 5 nm

Below 5 nm, each additional die-attach and micro-bump step multiplies potential defect sites, pushing cumulative package yields down sharply. Early 3 nm gate-all-around processes posted <20% yield in pilot runs, intensifying the cost of known-good-die testing. Thermal-cycle-induced stress further aggravates micro-crack propagation in through-silicon vias, demanding advanced reliability screening. Designers increasingly insert redundancy and error-correction logic, incurring area and power trade-offs. OSATs investing in inline X-ray and optical AI inspection tools mitigate yield loss but lift cost per unit, creating headwinds for some volume consumer segments of the high-end semiconductor packaging market.

Segment Analysis

By Technology: 3 D Integration Reshapes Performance Boundaries

2.5 D interposers captured the largest slice of the high-end semiconductor packaging market in 2024 as design houses prioritized proven yield and manufacturability at volume. The technology fuses logic and HBM dies with a moderate thermal penalty, supporting multi-terabit per second bandwidth in GPUs and FPGAs. By contrast, the 3D System-on-Chip segment, though smaller, is projected to clock the fastest 16.64% CAGR, underpinned by AI inference use cases in cloud and edge appliances that require co-located logic and memory stacks. As these architectures mature, vendors are optimizing die-to-die communication protocols to alleviate vertical signaling latency, accelerating broader adoption.

Interposer demand boosts revenue visibility for substrate suppliers, but mounting ABF lead-time risk has propelled interest in glass and silicon-based interposers. Meanwhile, 3D stacked-memory packages broaden the addressable base for high-bandwidth memory vendors, reinforcing scale economies. Embedded-bridge methods like Intel EMIB achieve die-to-die pitch <55 µm without full interposer complexity, offering a lower-cost entry point for heterogeneous integration. Within the high-end semiconductor packaging market size for this segment, process control innovations-especially hybrid bonding align accuracy-remain primary differentiators.

Note: Segment shares of all individual segments available upon report purchase

By Packaging Platform: Panel-Level Manufacturing Gains Momentum

Flip-chip ball-grid-array held 43.20% of the high-end semiconductor packaging market share in 2024, thanks to an entrenched manufacturing base and well-documented reliability metrics. Continued growth in server CPUs and GPU tiles sustains volumes even as alternative platforms emerge. Panel-level packaging (PLP) rides a 16.84% CAGR through 2030 because larger substrate form factors permit more dies per carrier, lowering cost per unit for mobile and IoT SoCs. Samsung’s pilot lines already process 600 mm glass panels, outpacing 300 mm wafer throughput and threatening traditional wafer-level economics.

PLP adoption is constrained by edge-warpage and die-placement accuracy challenges, compelling equipment vendors to refine vacuum-chuck and vision-alignment systems. System-in-Package solutions extend to automotive radar modules, integrating antennas and power management ICs to trim board area. In mobile devices, wafer-level chip-scale packages meet z-height mandates and cost goals, preserving demand momentum. As the high-end semiconductor packaging market evolves, manufacturers increasingly run mixed-platform fabs to align each design’s cost, performance, and reliability envelope.

By Device Node: Sub-3 nm Adoption Accelerates Despite Challenges

The 6-7 nm node range represented 31.70% of the high-end semiconductor packaging market in 2024, serving as the volume sweet spot where lithography costs and yields are relatively mature. However, the pursuit of leadership performance shifts incremental growth toward the sub-3 nm node, forecast to log an 18.24% CAGR to 2030. Early adopters include cloud AI accelerators and flagship smartphone chipsets that absorb a higher cost per transistor for a competitive advantage.

Process convergence drives demand for copper hybrid bonding and backside power delivery in packages, complicating thermal extraction. The 4-5 nm node remains attractive for cost-optimized premium handsets and automotive SoCs, balancing performance against yield risk. Legacy nodes ≥10 nm stay relevant in analog, power management, and some consumer wearables, where advanced packaging-rather than smaller geometry-delivers integration benefits. Standards bodies under IEEE focus on measurement methodologies for ultra-fine pitch interconnect and power integrity, guiding industry best practice at each node regime.

Note: Segment shares of all individual segments available upon report purchase

By End User: Automotive Transformation Drives Growth

Consumer electronics preserved the largest revenue pool at 29.30% in 2024, underpinned by over 1.2 billion smartphone units that each require multiple high-density packages. Device makers embed AI, RF, and PMIC dies inside compact footprints, spurring upticks in fan-out and Si-bridge adoption. Automotive and ADAS demand explodes at 17.85% CAGR as electric vehicles integrate high-resolution sensor fusion and domain controllers needing sub-5 nm logic. Functional safety requirements such as ISO 26262 drive rigorous package-level reliability metrics, favoring vendors with established automotive qualification records.

Telecom infrastructure transitions to 5 G-Advanced and 6 G research create an opportunity for millimeter-wave RF packages with embedded filters and phased-array antennas. Aerospace and defense customers specify radiation-hardened multi-chip modules suited to Low-Earth-Orbit satellites, leveraging chiplets to shorten design refresh cycles. Implantable medical devices adopt hermetic fan-out solutions that reduce volume while enabling wireless power delivery. Together, these segments diversify revenue streams, ensuring the high-end semiconductor packaging market remains resilient against downturns in any single vertical.

Geography Analysis

Asia-Pacific controlled 59.30% of the high-end semiconductor packaging market in 2024, anchored by Taiwan’s foundry leadership, South Korea’s memory expertise, and China’s rapid OSAT build-out. TSMC, ASE Technology, and SPIL co-locate back-end lines next to front-end fabs, compressing cycle time and lowering logistic overhead. Simultaneously, Beijing’s incentives foster a domestic ecosystem targeting 38% of global installed packaging capacity by 2030, though export-control policies add geopolitical uncertainty.

North America concentrates on high-value AI and defense-grade packages, buoyed by USD 52 billion CHIPS funding that subsidizes Amkor’s USD 2 billion Arizona facility and Intel’s Ohio packaging megasite. The region also houses a dense cluster of equipment and materials suppliers, allowing rapid prototyping for next-generation technologies. Europe pursues strategic autonomy through €730 million APECS and €830 million FAMES open-access pilot lines, giving SMEs affordable fabrication slots and seeding a continental chiplet ecosystem.

The Middle East and Africa chart an 18.63% CAGR through 2030, propelled by telecom infrastructure rollouts and sovereign funds investing in semiconductor hubs. Countries such as the United Arab Emirates partner with global OSATs to co-finance pilot lines, targeting regional demand for edge AI modules. South America remains nascent but benefits from consumer-electronics contract manufacturing in Brazil, generating incremental demand for localized test and finish services. The geographic mosaic underscores a shift from pure cost arbitrage toward resilience and national-security considerations.

Competitive Landscape

Foundry encroachment reshapes competitive dynamics inside the high-end semiconductor packaging market. TSMC generated >8% of corporate revenue from advanced packaging in 2024 after channeling upwards of USD 4 billion into CoWoS and system-on-wafer capacity, leveraging process synergies unavailable to pure-play OSATs. Samsung counters via early panel-level packaging milestones and potential alliances, including rumored talks for Intel to acquire a 20% stake in Samsung Foundry to co-develop advanced packages, a move that could diversify Intel’s access to extreme ultraviolet capacity.

ASE Technology retains top OSAT status, posting NTD595.4 billion (USD 18.46 billion) 2024 revenue and investing in multi-die packaging to shield margins from commoditized flip-chip offerings. Amkor Technology complements its Asian footprint with the Arizona site aimed at AI and automotive modules, improving domestic content compliance for U.S. defense and EV customers. JCET’s acquisition of a SanDisk packaging plant for USD 624 million reinforces China’s aspiration to internalize memory module production.

Specialized players command niche leadership: Shin-Etsu and Showa Denko innovate low-Dk dielectrics; Onto Innovation and KLA expand optical-inspection bandwidth for hybrid-bonding lines; and Deca Technologies licenses adaptive patterning to multiple OSATs. Patent filings concentrate on thermally conductive underfill, backside power delivery, and glass-core interposers. Overall, the competitive field rewards firms that pair scale with process leadership and partner ecosystems across materials, design tools, and equipment.

High-End Semiconductor Packaging Industry Leaders

-

Intel Corporation

-

Taiwan Semiconductor Manufacturing Company

-

Advanced Semiconductor Engineering, Inc

-

Samsung Electronics Co. Ltd

-

Amkor Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: The European Commission launched the APECS Chiplet Application Hub with €730 million in funding to accelerate heterogeneous integration R&D.

- March 2025: CEA-Leti coordinated the €830 million FAMES pilot line targeting More-than-Moore specialty packaging.

- February 2025: TSMC unveiled System-on-Wafer technology slated for 2027, delivering 10× current GPU memory bandwidth.

- January 2025: Samsung achieved panel-level packaging milestones ahead of mass production for consumer ICs.

Global High-End Semiconductor Packaging Market Report Scope

Semiconductor packaging is a supportive case that prevents physical damage and corrosion to logic units, silicon wafers, and memory during the final stage of the semiconductor manufacturing procedure. It permits the chip to be connected to a circuit board.

The high-end semiconductor packaging market is segmented by technology (3D SoC, 3D stacked memory, 2.5D interposers, UHD FO, and embedded si bridge), end user (consumer electronics, aerospace and defense, medical devices, telecom and communication, automotive), and geography (North America, Europe, Asia-Pacific, and Rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| 3D System-on-Chip (3D-SoC) |

| 3D Stacked Memory (HBM, HBM-PIM) |

| 2.5D Interposers |

| Ultra-High-Density Fan-Out (UHD-FO) |

| Embedded Si Bridge / EMIB |

| Flip-Chip Ball-Grid-Array (FC-BGA) |

| Wafer-Level Chip-Scale Package (WLCSP) |

| Panel-Level Packaging (PLP) |

| System-in-Package (SiP) |

| Less than or Equal to 3 nm |

| 4-5 nm |

| 6-7 nm |

| Greater than or Equal to 10 nm |

| Consumer Electronics |

| Telecom and 5G Infrastructure |

| Automotive and ADAS |

| Aerospace and Defense |

| Medical Devices |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Technology | 3D System-on-Chip (3D-SoC) | ||

| 3D Stacked Memory (HBM, HBM-PIM) | |||

| 2.5D Interposers | |||

| Ultra-High-Density Fan-Out (UHD-FO) | |||

| Embedded Si Bridge / EMIB | |||

| By Packaging Platform | Flip-Chip Ball-Grid-Array (FC-BGA) | ||

| Wafer-Level Chip-Scale Package (WLCSP) | |||

| Panel-Level Packaging (PLP) | |||

| System-in-Package (SiP) | |||

| By Device Node | Less than or Equal to 3 nm | ||

| 4-5 nm | |||

| 6-7 nm | |||

| Greater than or Equal to 10 nm | |||

| By End User | Consumer Electronics | ||

| Telecom and 5G Infrastructure | |||

| Automotive and ADAS | |||

| Aerospace and Defense | |||

| Medical Devices | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Colombia | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the projected value of the high-end semiconductor packaging market by 2030?

The market is expected to reach USD 85.11 billion by 2030, reflecting a 15.41% CAGR.

Which technology leads current revenue in advanced packaging?

2.5 D interposers hold the top spot with 36.60% market share.

Why are AI accelerators pivotal to packaging demand growth?

They require extreme memory bandwidth and thermal management, making heterogeneous integration a limiting factor for deployment timelines.

How much of global revenue did Asia-Pacific capture in 2024?

Asia-Pacific accounted for 59.30% of total advanced packaging sales.

Which end-user segment is growing the fastest through 2030?

Automotive and ADAS applications are forecast to expand at a 17.85% CAGR as electric vehicles add advanced driver assistance systems.

What capex share is TSMC allocating to advanced packaging in 2025?

The company plans to devote roughly 10-20% of its USD 38-42 billion 2025 capital budget to advanced packaging capacity.

Page last updated on: