Market Overview

| Study Period | 2019 - 2030 |

|---|---|

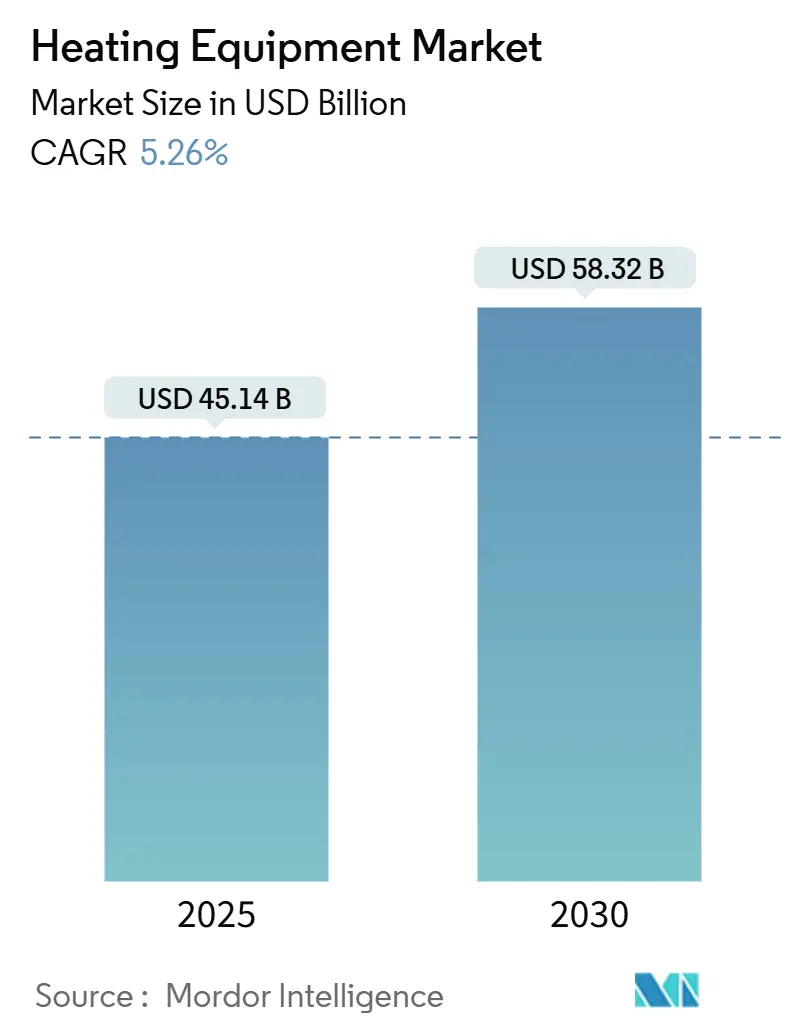

| Market Size (2025) | USD 45.14 Billion |

| Market Size (2030) | USD 58.32 Billion |

| Growth Rate (2025 - 2030) | 5.26% CAGR |

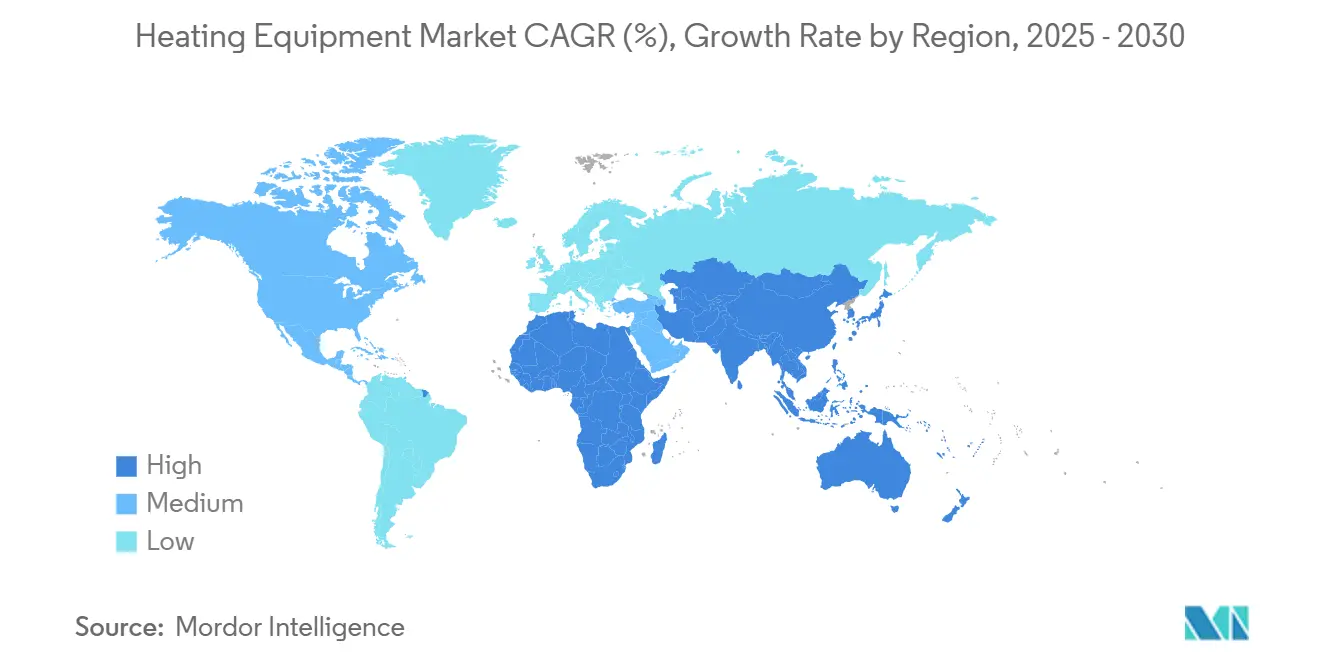

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Heating Equipment Market Analysis by Mordor Intelligence

The global heating equipment market size reached USD 45.14 billion in 2025 and is projected to increase to USD 58.32 billion by 2030, reflecting a 5.26% CAGR over the forecast period. Growing electrification mandates, aggressive carbon-reduction targets, and mounting corporate sustainability commitments are accelerating the adoption of high-efficiency heat pumps while stimulating investment in hydrogen-ready boilers and solar-assisted units. Fortune 500 procurement teams are now specifying heat pump solutions in new facilities to reduce Scope 2 emissions. Additionally, performance-based building codes in Europe and North America are shortening the replacement cycles for outdated fossil-fuel systems. The Asia-Pacific remains the production heartland, yet fast-evolving policy landscapes in the Middle East and Africa are opening up new demand pockets as governments embed energy-efficiency goals within their national diversification agendas. Competitive intensity is moderate: global incumbents pursue economies of scale and vertical integration, while niche innovators focus on high-temperature industrial drying and district-energy applications.

Key Report Takeaways

- By product type, heat pumps led with 43.53% revenue share in 2024; solar-assisted heating units are projected to expand at a 7.32% CAGR through 2030.

- By fuel type, electric systems held 51.54% of the heating equipment market share in 2024, while hydrogen-ready technologies recorded the highest CAGR at 6.42% between 2025 and 2030.

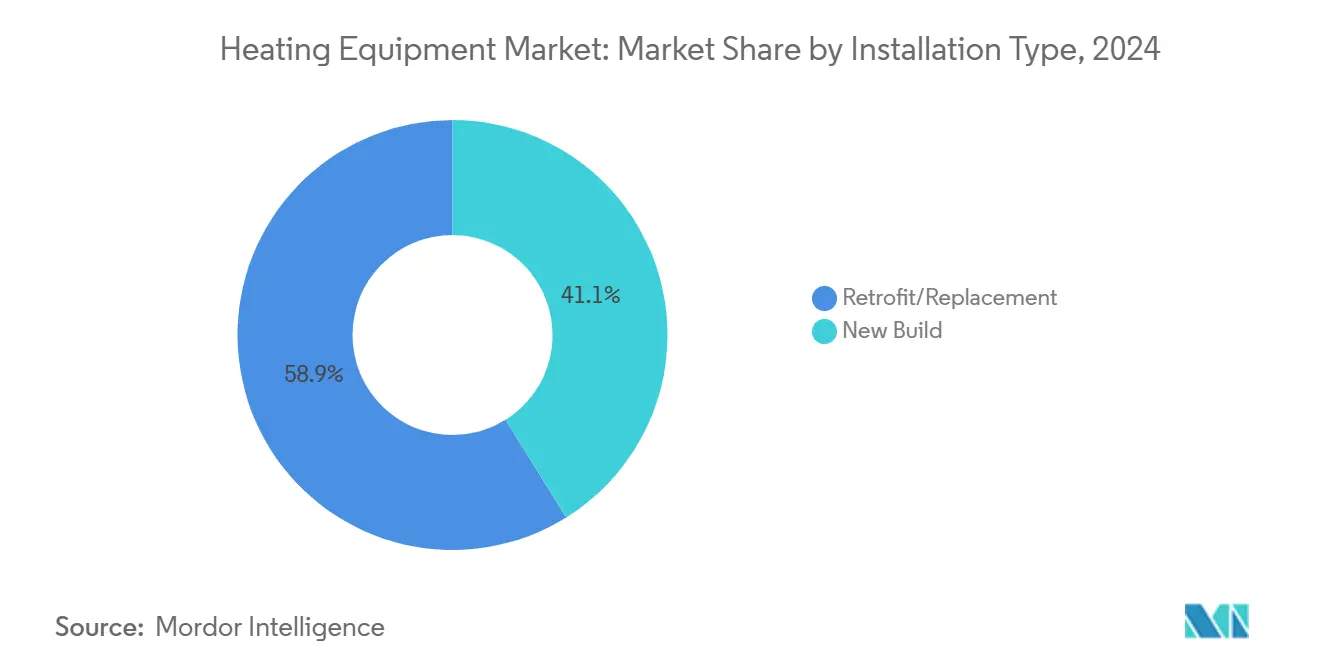

- By installation type, retrofit and replacement accounted for 58.87% of the heating equipment market size in 2024 and are advancing at 6.83% CAGR through 2030.

- By end user, residential applications captured 61.64% share in 2024; industrial users post the strongest CAGR at 7.87% to 2030.

- By geography, the Asia-Pacific region dominated with 38.9% share in 2024, whereas the Middle East and Africa region is expected to grow at 8.01% CAGR through 2030.

Global Heating Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification push in cold-climate retrofits | +1.2% | North America and Europe; spillover to Asia-Pacific | Medium term (2-4 years) |

| Carbon-neutral corporate campuses | +0.8% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Gas-phase heat pump innovations | +0.6% | Asia-Pacific core, expanding to North America/Europe | Long term (≥ 4 years) |

| Performance-based building codes | +0.9% | Europe and North America; early Asia-Pacific uptake | Medium term (2-4 years) |

| Waste-heat integration in district energy | +0.7% | Europe and select North American cities | Long term (≥ 4 years) |

| Green-hydrogen blending pilots | +0.4% | Europe and select Middle East markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Electrification Push in Cold-Climate Retrofit Programs

Utility-funded incentives in the northern United States and Canada made cold-climate heat pumps financially attractive for low-income households in 2024.[1] U.S. Department of Energy, “Biden Administration Announces USD 4.3 Billion in Home Energy Rebates,” energy.govAdvanced inverter compressors keep coefficients of performance above 2.0 at −15 °C, closing historic performance gaps with resistance heaters. Coordinated neighborhood upgrades achieve peak-load smoothing via demand-response software that staggers compressor starts. Savings from avoided natural-gas infrastructure renewals help utilities fund rebate pools, while homeowners report 30% lower annual heating costs relative to legacy oil furnaces. [2]California Public Utilities Commission, “CPUC Addresses Grid Capacity Challenges from Building Electrification,” cpuc.ca.govThe resulting demand surge strengthens the heating equipment market and prompts manufacturers to expand their regional assembly plants to reduce lead times.

Carbon-Neutral Corporate Campuses Demand On-Site Heat Pumps

Large multinationals invested more than USD 2 billion in campus electrification in 2024, driven by net-zero roadmaps and investor pressure. High-capacity ground-source arrays now supply space heating, domestic hot water, and process heat from a single loop, boosting overall site energy productivity by up to 50%. Procurement teams specify seasonal performance factors above 4.0, even in temperate zones, pushing R&D toward ultra-efficient refrigerant blends. Heat-pump systems often integrate with rooftop photovoltaics and behind-the-meter batteries to minimize grid imports, thereby reinforcing the business case through demand-charge reduction. These corporate projects showcase replicable design templates that shorten engineering cycles for midmarket adopters.

Gas-Phase Heat Pump Innovations for High-Temperature Industrial Drying

Breakthrough working-fluid chemistries lifted output temperatures beyond 150 °C, enabling deployment in food, textile, and pharmaceutical dryers previously locked into natural-gas burners. [3]International Energy Agency, “Heat Pumps in Industry,” iea.org Japanese suppliers invested USD 800 million to commercialize units delivering up to 200 °C process heat with 30-50% energy savings. Early installations in Nordic plants powered by 95% renewable electricity cut Scope 1 emissions by nearly 70%. As reliability data grows, Southeast Asian and North American manufacturers are issuing requests for proposals that could triple the addressable segment by 2027.

Performance-Based Building Codes Accelerating Boiler Replacement

The 2024 revision of the European Union's Energy Performance of Buildings Directive obliges commercial properties to meet stringent energy-intensity ceilings, best served by heat pumps.[4]European Parliament, “Buildings: MEPs Back Deal to Cut Energy Consumption and Emissions,” europarl.europa.euNon-compliant owners face escalating fines, turning equipment upgrades into risk-mitigation spend rather than optional payback plays. U.S. municipalities, from Boston to Seattle, mirror this policy through local ordinances pegged to carbon ceilings, effectively phasing out stand-alone boilers. Certification schemes such as LEED and BREEAM award premium credits for electrified heating, lifting property values, and funneling institutional capital toward compliant assets.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-capacity bottlenecks | -0.3% | North America and Europe urban cores | Short term (≤ 2 years) |

| Skilled-labor shortages | -0.5% | Global; acute in North America and Europe | Medium term (2-4 years) |

| Volatile nickel pricing | -0.4% | Global; high impact in Asia-Pacific hubs | Short term (≤ 2 years) |

| Fragmented residential rebate administration | -0.2% | North America; secondary in Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Grid-Capacity Bottlenecks in Electrified Neighborhoods

California utilities experienced over 200 upgrade delays in 2024 due to clustered heat-pump rollouts that pushed distribution transformers beyond their capacity. Peak winter loads jumped 3-4 kW per household, prompting emergency demand-response pilots that cycle compressors against temperature-setback allowances. Short-term mitigation relies on thermal storage tanks and smarter inverters, but substation reinforcement remains unavoidable, resulting in additional capital outlays that dampen installation rates. Similar pinch points emerged in London, Amsterdam, and Toronto, underscoring the need for grid planning that aligns with decarbonization timelines.

Skilled-Labor Shortages for Multi-Technology Retrofits

HVAC Excellence estimates a 35% gap in technicians versed in refrigerant handling, electrical integration, and digital controls required for modern heat pumps. Average project schedules stretched by four weeks in 2024 as contractors queued limited crews across multiple sites. Wage inflation pushed labor costs up by 18%, eroding some rebate benefits for end consumers. Manufacturers now sponsor accelerated training programs and ship pre-charged, quick-connect modules to cut job-site complexity. Nevertheless, labor scarcity remains the single biggest execution risk for large-scale retrofit portfolios through 2027.

Segment Analysis

By Product Type: Heat Pumps Consolidate Market Leadership

Heat pumps accounted for 43.53% of the heating equipment market share in 2024, driven by their superior seasonal performance and generous policy incentives. The heating equipment market size for heat pumps is projected to widen further as inverter technology, variable-speed compressors, and low-GWP refrigerants close efficiency gaps even in severe cold climates. Solar-assisted units, although representing a smaller base, are tracking a 7.32% CAGR, fueled by falling photovoltaic module prices and improved thermal storage media. Consumers in Europe and Japan are increasingly favoring hybrid arrangements that pair a primary heat pump with a compact resistance element or a condensing gas boiler for added resiliency during polar vortex episodes. Meanwhile, furnace shipments remain stable in gas-rich North American states, but tighter methane leak regulations could shift replacements toward electric alternatives. Boilers continue to serve European commercial buildings, where legacy hydronic loops allow for straightforward heat-pump drop-ins. Advanced anti-corrosion coatings now extend heat-exchanger life beyond 15 years, a pivotal criterion in life-cycle cost analyses.

Manufacturers integrate IoT sensors that feed cloud analytics for predictive maintenance, reducing unplanned downtime and supporting service-as-a-subscription models. This data feedback loop informs iterative design improvements, enhancing coefficient of performance and enabling remote firmware upgrades without service visits. The synergy of hardware and software magnifies differentiation potential, especially in a heating equipment market that increasingly rewards total cost of ownership over sticker price. As proof-of-concept solar-thermal and photovoltaic hybrids demonstrate levelized heat costs below USD 20 per MWh in select Mediterranean sites, product-type diversification may accelerate beyond the forecast window.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Fuel Type: Electrification Dominates but Hydrogen Gains Traction

Electric systems accounted for 51.54% of the heating equipment market share in 2024, driven by the penetration of renewables and policy-backed net-zero targets. The heating equipment market size for electric units benefits from coefficients of performance exceeding 3.5, resulting in operational savings when grid carbon intensity is below 400 g CO₂/kWh. Green-hydrogen-ready models, advancing at a 6.42% CAGR, represent strategic hedges for large facilities anticipating a hydrogen economy once electrolyzer costs dip below USD 2/kg. Natural-gas appliances persist where pipeline infrastructure is entrenched and carbon pricing remains modest, but regulatory uncertainty deters new investments in boilers.

Oil-fired systems are often the only option, except in remote Canadian or Nordic locales where electricity prices spike during winter peaks. Biomass boilers maintain niche adoption in rural European districts, leveraging abundant forestry residues, though particulate-emissions controls add CAPEX. Risk assessments of future carbon pricing, grid capacity, and fuel price volatility increasingly drive fuel-type decisions. By 2030, analysts expect electric and hydrogen-ready units, combined, to account for a share of over 65%, underscoring an irreversible shift toward low-carbon vectors.

By Installation Type: Retrofit Segment Accelerates Equipment Turnover

Retrofit and replacement projects accounted for 58.87% of all installations in 2024, as aging boiler fleets in Europe and North America neared the end of their service life. The segment’s 6.83% CAGR is driven by regulatory incentives and disincentives, ranging from utility rebates to carbon taxes that compress payback periods to under six years. The heating equipment market size attached to retrofits is further lifted by add-on services such as load calculations, electrical upgrades, and post-installation performance verification. Off-the-shelf retrofit kits enable straightforward swaps in constrained mechanical rooms, reducing labor hours by 30% compared to bespoke solutions.

New-construction demand, though smaller in volume, often dictates cutting-edge specifications that later filter into the retrofit domain. Passive-house envelopes in Germany and net-zero codes in California mandate low-temperature heating loops that favor air-to-water heat pumps paired with low-mass radiators. Retrofit complexity escalates in multifamily towers where vertical distribution stacks limit pipe rerouting, prompting interest in decentralized micro-heat-pump modules. Financing models such as energy-service agreements transfer upgrade costs to third parties, easing capital constraints for condominium boards and public-housing authorities.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By End User: Industrial Facilities Post the Fastest Growth Curve

Residential buyers still accounted for 61.64% of 2024 shipments, supported by government rebates and consumer preference for all-electric homes. However, industrial customers are on a sharper ascent with a 7.87% CAGR as carbon-border adjustment mechanisms target embedded emissions in exported goods. Food processors and pharmaceutical plants are now piloting closed-loop water-to-water heat pumps that deliver 120-150 °C process heat, thereby slashing gas consumption and aligning with science-based targets. For commercial buildings, predictable refurbishment cycles help maintain steady demand; institutional investors typically replace aging boilers with heat pumps when occupancy falls below 80% during renovation schedules.

Industrial adoption accelerates as life-cycle cost models reflect the volatility of natural gas prices and the reputational risk associated with carbon-intensive production. Scalable skid-mounted heat-pump containers enable phased retrofits, thereby mitigating downtime in continuous process lines. The residential segment, especially in the Asia-Pacific region’s emerging middle-class suburbs, remains volume-centric and price-sensitive. To penetrate this bracket, suppliers roll out compact monobloc units with pre-filled refrigerant, cutting installation time by half and sidestepping license requirements in jurisdictions with stringent F-gas handling rules.

Geography Analysis

The Asia-Pacific region maintained a dominant 38.9% share of the heating equipment market in 2024, driven by China’s large-scale manufacturing and Japan’s technological leadership in variable-speed compressors. Regional authorities align building electrification targets with industrial policy goals, funneling low-interest loans to domestic producers and safeguarding supply chains for compressors and inverters. Growth is underpinned by rising disposable incomes and stricter urban air-quality mandates that discourage the use of coal boilers. Meanwhile, South Korea’s Green Remodeling Initiative subsidizes heat-pump retrofits in small and mid-sized enterprises, broadening the addressable base beyond residential buyers.

Middle East and Africa posted the fastest regional CAGR at 8.01%, reflecting energy-efficiency clauses embedded in Saudi Arabia’s Vision 2030 and the UAE’s Estidama Pearl Rating System. Warm-climate heat pumps that switch seamlessly between cooling and heating now undercut chiller-boiler combinations in terms of life-cycle cost, even in grids still dominated by natural gas. African markets are pivoting as electrification rates improve. Kenya’s Last-Mile Connectivity Project expanded grid access to 75% of households in 2024, opening pathways for entry-level air-source heat pumps. Financing hurdles persist, but multilateral banks increasingly back pay-as-you-save schemes targeting schools and hospitals.

Europe and North America exhibit mature, replacement-driven dynamics. The European Commission’s REPowerEU initiative incentivizes 30 million additional heat-pump installations by 2030, a move accelerated by geopolitical gas-supply disruptions. North American momentum is anchored in the U.S. Inflation Reduction Act’s 30% tax credit and state-level Building Performance Standards that penalize high emissions. Regional disparities remain: California mandates all-electric new homes from 2026, while the U.S. Midwest retains a diversified fuel mix shaped by abundant shale gas. Canada’s Greener Homes Grant tilts the balance in favor of cold-climate air-source units, proved feasible down to −25 °C.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

Global incumbents, such as Daikin Industries, Carrier Global, and Robert Bosch, uphold technological leadership through billion-dollar R&D budgets and vertically integrated compressor lines. They leverage economies of scale to undercut smaller rivals in commodity segments while commanding premiums in advanced inverter models. Regional specialists fill white spaces: Swedish player NIBE dominates geothermal heat pumps in Nordic retrofit projects, whereas U.S. startup Gradient targets window-mounted units for multifamily applications. Patent filings in low-GWP refrigerants and microchannel heat exchangers climbed 23% year-over-year in 2024, indicating an innovation race that could reshape supplier hierarchies.

Ecosystem partnerships are proliferating as heating equipment converges with distributed energy resources. Siemens pairs its building-automation platform with multiple heat-pump brands to offer turnkey demand-response services, monetizing grid flexibility. Digital twins enable predictive maintenance agreements where uptime guarantees become contractual obligations, shifting revenue toward recurring service streams. Mergers and acquisitions accelerate: Carrier’s USD 1.2 billion purchase of a European hydronic specialist expands its retrofit footprint, while Trane Technologies’ district-heating win in Saudi Arabia signals appetite for large-scale integrated projects. Commodity pressures linger due to nickel price volatility, but suppliers partially hedge through long-term purchase contracts and alloy-substitution R&D.

Heating Equipment Industry Leaders

-

Robert Bosch GmbH

-

Daikin industries ltd

-

Carrier Global Corporation

-

Trane Technologies plc

-

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- October 2025: Daikin Industries announced a USD 500 million expansion of heat-pump production in Texas targeting weather-resilient, inverter-driven units.

- September 2025: Carrier Global completed a USD 1.2 billion acquisition of a European hydronic heat-pump manufacturer to deepen retrofit offerings.

- August 2025: Bosch Thermotechnology introduced hydrogen-ready commercial boilers compatible with 20% hydrogen blends and future full conversion.

- July 2025: Trane Technologies secured a USD 300 million district-heating contract for a Saudi smart-city development featuring integrated heat pumps.

Global Heating Equipment Market Report Scope

Heating Equipment comprises any equipment designed, utilized, and intended to be used for supplying heat to a structure.

The Global Heating Equipment Market Report is Segmented by Product Type (Heat Pumps, Furnaces, Unitary Heaters, Boilers, and Solar Assisted Heating Units), Fuel Type (Electric, Natural Gas, Oil, Biomass and Bio-Derived, and Hydrogen-Ready), Installation Type (New Build, and Retrofit/Replacement), End User (Residential, Commercial, and Industrial), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Heat Pumps |

| Furnaces |

| Unitary Heaters |

| Boilers |

| Solar Assisted Heating Units |

By Fuel Type

| Electric |

| Natural Gas |

| Oil |

| Biomass and Bio-Derived |

| Hydrogen-Ready |

By Installation Type

| New Build |

| Retrofit/Replacement |

By End User

| Residential |

| Commercial |

| Industrial |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Rest of Africa | ||

| By Product Type | Heat Pumps | ||

| Furnaces | |||

| Unitary Heaters | |||

| Boilers | |||

| Solar Assisted Heating Units | |||

| By Fuel Type | Electric | ||

| Natural Gas | |||

| Oil | |||

| Biomass and Bio-Derived | |||

| Hydrogen-Ready | |||

| By Installation Type | New Build | ||

| Retrofit/Replacement | |||

| By End User | Residential | ||

| Commercial | |||

| Industrial | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Spain | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What growth rate is expected for heating equipment through 2030?

The heating equipment market is projected to expand at a 5.26% CAGR between 2025 and 2030.

Which product holds the largest share today?

Heat pumps led the 2024 shipment tally with 43.53% of global sales.

Why are corporates investing in heat-pump campuses?

On-site heat pumps slash Scope 2 emissions and align facilities with public net-zero commitments while reducing long-term energy costs.

Where is regional demand rising fastest?

The Middle East and Africa region is forecast to post an 8.01% CAGR through 2030, outpacing all other geographies.

How are skilled-labor shortages being addressed?

Manufacturers sponsor accelerated training, ship pre-charged modules and deploy remote diagnostics to reduce on-site complexity.

What role will hydrogen play in future heating?

Hydrogen-ready boilers are advancing at a 6.42% CAGR as end users hedge against future low-carbon fuel availability.

Page last updated on: