| Study Period | 2019 - 2030 |

| Market Volume (2025) | 98.55 Million tonnes |

| Market Volume (2030) | 116.43 Million tonnes |

| CAGR | 3.39 % |

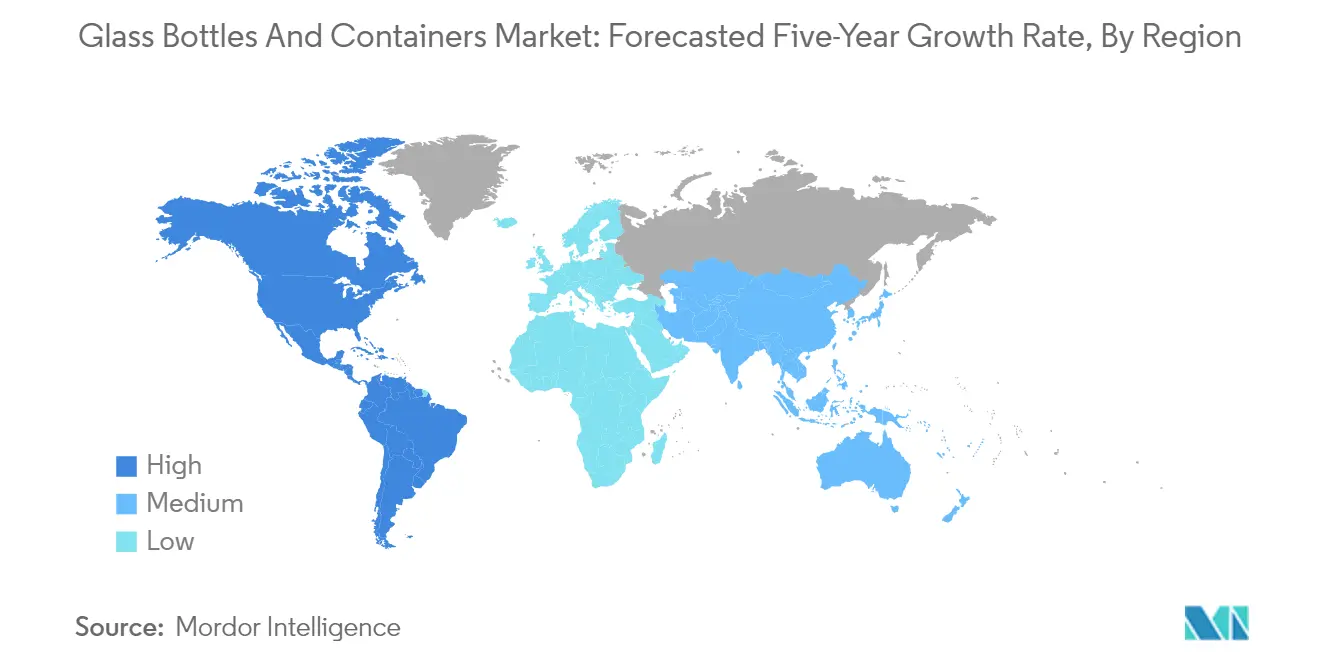

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

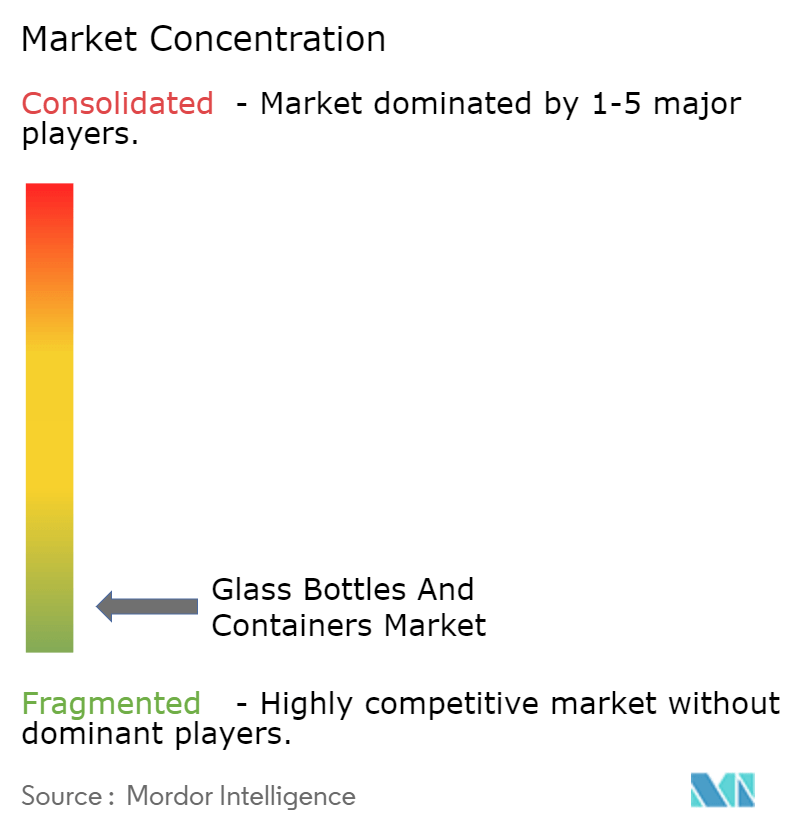

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Glass Bottles and Containers Market Analysis

The Glass Bottles and Containers Market size in terms of shipment volume is expected to grow from 98.55 million tonnes in 2025 to 116.43 million tonnes by 2030, at a CAGR of 3.39% during the forecast period (2025-2030).

The glass packaging industry is increasingly shaped by the global focus on sustainability and environmentally conscious practices. Glass, as a material, offers a compelling value proposition due to its recyclability and reusability, aligning seamlessly with the growing demand for eco-friendly glass packaging solutions. Regulatory initiatives, particularly in regions such as the European Union, are accelerating this shift by setting ambitious recycling targets for the container glass industry. For example, the EU has established a goal of achieving a 70% recycling rate for glass packaging by 2025, with an increase to 75% by 2030. Collaborative efforts like the Close the Glass Loop initiative further underscore this commitment, aiming for a 90% post-consumer glass container collection rate by 2030.

Within this market, notable trends such as the premiumization of products and the preference for transparent packaging are emerging as key drivers. Glass is often perceived as a premium material, making it a favored choice in industries like cosmetics and spirits, where quality and luxury are paramount. For instance, high-end fragrance and skincare brands frequently opt for glass packaging due to its aesthetic appeal and sustainable attributes. Furthermore, the inherent transparency of glass resonates with consumer preferences for visible and trustworthy packaging, particularly in the food and beverage sectors. Innovations in glass bottle manufacturing, including lightweighting and enhanced production techniques, are addressing traditional challenges such as weight and fragility, thereby broadening its applicability.

The dynamics of the glass bottle industry are influenced by the intersection of sustainability imperatives and specific industry requirements. The global emphasis on reducing carbon footprints and enhancing recycling rates is fostering the adoption of glass packaging, while sector-specific demands in areas like food, beverages, and healthcare are driving innovation. For example, the U.S. domestic glass container industry showcases robust production and consumption patterns, reflecting its integral role in these markets. Additionally, the aesthetic and functional advantages of glass are propelling its use in premium product segments. Collectively, these factors illustrate the market's evolution and its alignment with both consumer expectations and industry trends.

Glass Bottles and Containers Market Industry Segmentation

Growing Demand from Food and Beverage Industry

The food and beverage industry continues to be a cornerstone in driving the demand for glass bottles and containers. Glass bottle packaging is highly valued in this sector for its ability to preserve the taste and quality of its contents, making it a preferred choice for both manufacturers and consumers. The rising consumption of beverages, particularly in the alcoholic segment such as wine and spirits, has been a significant contributor to the growth of the glass beverage bottles market. Additionally, the food industry relies heavily on glass jars and bottles for packaging a variety of products, further amplifying demand.

Moreover, the preference for glass packaging is not solely functional but also strategic. Its aesthetic appeal and premium perception align with the branding objectives of many food and beverage companies, enhancing the consumer experience. Glass's inert nature ensures it does not interact with its contents, offering a safe and reliable glass packaging solution. As the food and beverage industry continues to expand, the demand for glass bottle packaging solutions is poised to grow, underscoring its critical role in this market.

Understand The Key Trends Shaping This Market

Download PDF

Sustainability and Recyclability Initiatives Moving Packagers and Consumer Brands to Glass Packaging

Sustainability and recyclability are increasingly shaping the packaging decisions of manufacturers and consumers alike. Glass packaging, being 100% recyclable and reusable without quality degradation, is emerging as a leading choice for environmentally conscious glass packaging solutions. This trend aligns with the rising consumer demand for sustainable options and the corporate social responsibility commitments of many organizations. For instance, the European Union has set ambitious recycling targets for glass packaging, aiming to significantly enhance recycling rates by 2030. This regulatory push is accelerating the shift towards glass as a sustainable alternative to less eco-friendly materials.

Industry and governmental initiatives further bolster this transition. Programs like the Close the Glass Loop partnership aim to achieve high post-consumer glass container collection rates by 2030, promoting a circular economy. These efforts not only reduce waste but also conserve resources, as recycled glass can be efficiently repurposed into new containers. The focus on sustainability is driving innovation within the glass packaging industry, fostering advancements in recycling processes and the integration of recycled materials in production. This momentum is expected to persist, positioning sustainability and recyclability as pivotal drivers of growth in the glass bottles and containers market.

Glass Bottles and Containers Market Trends

Beverages Glass Bottles and Containers Market Analysis

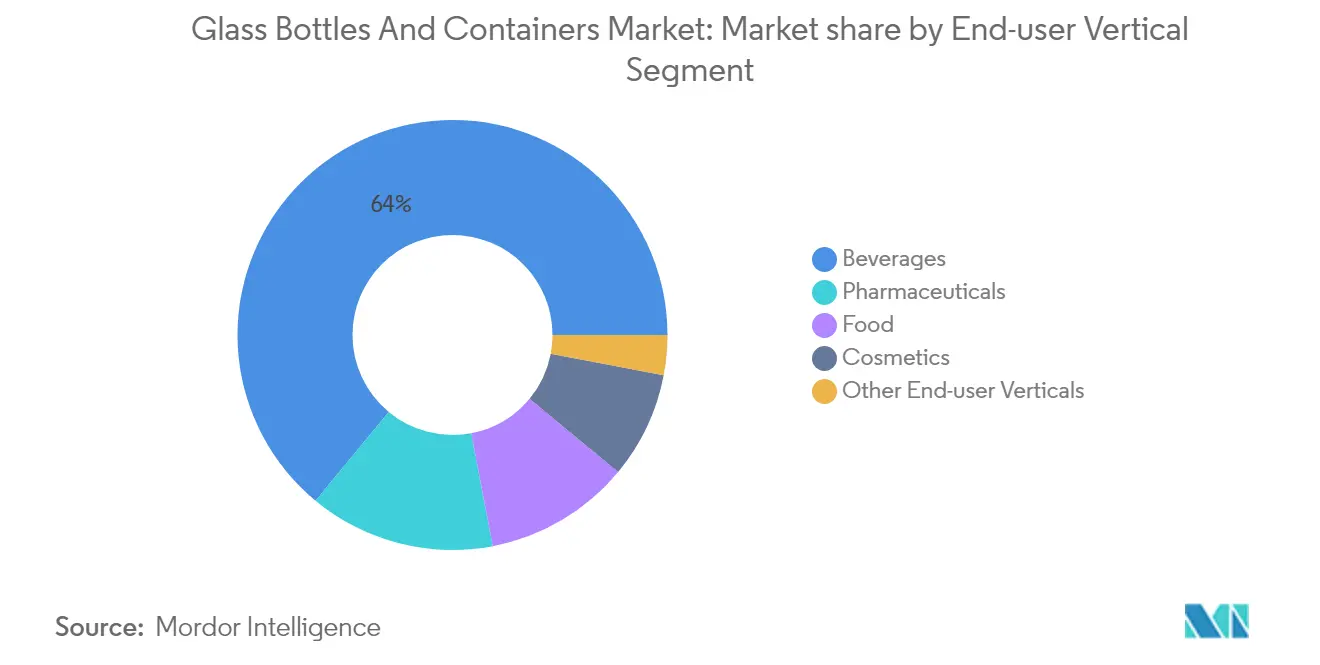

The beverages segment is the largest in the glass bottles and containers market, accounting for approximately 64% of the global market share. This dominance is driven by the extensive use of glass beverage bottles in both alcoholic and non-alcoholic beverages due to their ability to preserve the taste, aroma, and quality of the contents. Glass bottles are particularly favored in the alcoholic beverage industry, including wine and beer, as they provide UV protection and maintain the integrity of the product. The segment benefits from the increasing consumer preference for sustainable and eco-friendly glass bottle packaging solutions, as glass is recyclable and reusable. Additionally, the premiumization trend in the beverage industry has led to a higher demand for aesthetically appealing and high-quality glass packaging. Innovations in lightweight glass bottle production have also contributed to reducing transportation costs and environmental impact. As a result, the beverages segment continues to lead the market, setting benchmarks for quality and sustainability.

Glass Bottles And Containers Market Geography Segment Analysis

North America Glass Bottles And Containers Market Analysis

North America plays a pivotal role in the global glass bottle industry and glass container industry, driven by its advanced manufacturing capabilities and high consumer demand across various sectors. The region's market is characterized by a strong emphasis on sustainability, with increasing adoption of recyclable and reusable glass packaging solutions. Key growth drivers include the robust demand from the food and beverage industry, particularly for alcoholic beverages and premium products, as well as the pharmaceutical sector's reliance on glass packaging for its superior barrier properties. Trends indicate a shift towards lightweight glass containers and innovations in design to cater to evolving consumer preferences. Additionally, the region benefits from a well-established supply chain and significant investments in technological advancements, ensuring its competitive edge in the bottle industry.

United States Glass Bottles And Containers Market Analysis

The United States is projected to hold approximately 77% of the North American glass bottles and containers market share in 2024. This significant share underscores the country's pivotal role as a leader in glass bottle manufacturing and the production and consumption of glass packaging, driven by its robust food and beverage, pharmaceutical, and personal care industries. Key growth drivers include increasing consumer preference for sustainable and recyclable glass packaging solutions, alongside the rising demand for premium alcoholic beverages and pharmaceutical products. Notable trends include the adoption of innovative glass bottle packaging designs and the expansion of refillable and reusable glass bottle systems, reflecting a shift towards environmental sustainability. Additionally, the United States benefits from a well-established supply chain and domestic production capabilities, ensuring its continued dominance in the glass bottle industry.

Canada Glass Bottles And Containers Market Analysis

Canada plays a pivotal role in the glass bottle industry, characterized by its robust manufacturing capabilities and significant export activities. The market is driven by factors such as increasing urbanization, rising disposable incomes, and a growing preference for sustainable and premium glass packaging solutions. Notable trends include the adoption of glass packaging in the alcoholic beverage sector and the increasing demand for eco-friendly and recyclable materials. Additionally, strategic acquisitions and investments in the Canadian market underscore its importance as a hub for innovation and growth in the glass packaging industry. These dynamics position Canada as a key player in the global glass packaging landscape, with opportunities for further expansion and development.

Europe Glass Bottles And Containers Market Analysis

Europe plays a pivotal role in the glass bottle industry and glass container industry, characterized by its advanced recycling systems and strong emphasis on sustainability. The region's focus on eco-friendly glass packaging solutions is driven by stringent environmental regulations and consumer preferences for sustainable products. Key growth drivers include the increasing demand for glass packaging in the food and beverage industry, as well as innovations in glass bottle manufacturing technologies that enhance product quality and design. Trends in Europe highlight a shift towards circular economy practices, with significant investments in recycling infrastructure and the adoption of hybrid furnaces to reduce carbon emissions. Additionally, the region's established industries, such as wine and cosmetics, continue to rely heavily on glass packaging, further solidifying its importance in the global market.

United Kingdom Glass Bottles And Containers Market Analysis

The United Kingdom plays a pivotal role in the glass bottle industry, driven by its strong emphasis on sustainability and recycling. The market has experienced approximately 4% CAGR growth from 2019 to 2024, reflecting its robust development. Key growth drivers include the increasing consumer preference for sustainable glass packaging and the government's initiatives to enhance recycling infrastructure. Trends such as the exclusion of glass bottles from the Deposit Return Scheme (DRS) and the rise in consumer spending on beverages packaged in glass highlight the market's dynamic nature. Additionally, the UK's glass packaging industry has made significant strides in decarbonization and energy efficiency, further solidifying its position as a leader in sustainable glass packaging solutions.

Germany Glass Bottles And Containers Market Analysis

Germany plays a pivotal role in the glass bottles and containers market, being a leader in sustainability and recycling initiatives. The market in Germany has experienced approximately 3% CAGR from 2019 to 2024, driven by the country's advanced recycling systems and strong demand for eco-friendly glass packaging solutions. Notably, Germany's deposit return scheme for glass containers achieves a remarkable 98% return rate, showcasing the nation's commitment to environmental sustainability. Trends in the market include the adoption of hybrid furnaces by glass container manufacturers to reduce CO2 emissions and the increasing preference for glass packaging in the beverage sector due to its ability to preserve product quality. Additionally, strategic acquisitions and investments in innovative technologies are further strengthening Germany's position in the global glass packaging industry.

France Glass Bottles And Containers Market Analysis

France plays a pivotal role in the glass bottle manufacturing industry, being a leading producer of premium beverages such as champagne and cognac, which demand high-quality glass packaging. The market is driven by the country's strong emphasis on sustainability, as evidenced by initiatives like the introduction of a glass bottle deposit system to reduce plastic waste and promote recycling. Trends in the French market include a growing preference for reusable glass containers and significant investments in modernizing glass production facilities. Additionally, the cosmetics industry in France, known for its premium products, heavily relies on glass packaging to enhance product appeal and maintain quality. These factors collectively underscore France's strategic importance in the global glass packaging industry.

Italy Glass Bottles And Containers Market Analysis

Italy plays a pivotal role in the wine glass bottles market, primarily driven by its strong association with the wine and food industries, which are integral to Italian culture and economy. The country's emphasis on high-quality, sustainable glass packaging solutions aligns with the global trend towards eco-friendly materials, further bolstering the demand for glass containers. Notable growth drivers include the increasing preference for glass due to its inert nature and recyclability, as well as innovations in lightweight and recycled glass bottle production. Trends such as the adoption of advanced glass bottle manufacturing technologies and the expansion of production capacities by key players underscore the market's dynamic nature. Additionally, Italy's commitment to recycling and sustainability initiatives enhances its position as a leader in environmentally conscious glass packaging solutions.

Spain Glass Bottles And Containers Market Analysis

Spain plays a pivotal role in the glass bottle industry, driven by its robust food and beverage industry and a growing emphasis on sustainable glass packaging solutions. The market is propelled by increasing consumer demand for eco-friendly and health-conscious packaging options, alongside advancements in glass manufacturing technologies that enhance design and functionality. Notable trends include the adoption of innovative production techniques and the integration of renewable energy sources in manufacturing processes, as evidenced by collaborations like that of Verallia Group and Mahou San Miguel. Additionally, the pharmaceutical sector's expansion and the government's support for technological advancements in industries such as wine production further stimulate market growth. Challenges such as rising energy costs and supply chain disruptions are being addressed through strategic investments and partnerships, ensuring the market's resilience and adaptability.

Poland Glass Bottles And Containers Market Analysis

Poland plays a pivotal role in the European glass bottle industry, characterized by its robust manufacturing capabilities and strategic geographical location. The market is driven by the increasing demand for sustainable glass packaging solutions, particularly in the beverage and cosmetics industries, where glass is preferred for its inert and recyclable properties. Recent trends highlight the adoption of innovative technologies, such as sustainable glass furnaces, which aim to reduce emissions and enhance energy efficiency. Additionally, regulatory measures, including bans on single-use plastics and the introduction of deposit systems for glass bottles, are fostering a shift towards environmentally friendly packaging. These factors, combined with Poland's active participation in European glass industry initiatives, underscore its importance in shaping the future of sustainable packaging solutions.

Russia Glass Bottles And Containers Market Analysis

The glass bottles and containers market in Russia plays a pivotal role in the packaging industry, driven by the country's robust food and beverage sectors and its strategic emphasis on import substitution policies. Key growth drivers include the increasing demand for sustainable and eco-friendly packaging solutions, coupled with the rising consumption of beverages and pharmaceuticals requiring glass packaging. Recent trends highlight a shift towards localized production due to geopolitical factors, fostering innovation and self-reliance within the industry. Additionally, the market is witnessing advancements in glass manufacturing technologies aimed at enhancing efficiency and reducing environmental impact. These dynamics underscore the market's resilience and its adaptation to evolving economic and regulatory landscapes.

Asia Glass Bottles And Containers Market Analysis

The Asia glass bottles and containers market plays a pivotal role in the global packaging industry, driven by its extensive manufacturing capabilities and growing consumer base. The region's market growth is fueled by increasing demand for sustainable and eco-friendly glass packaging solutions, particularly in the food and beverage and pharmaceutical sectors. Notable trends include the adoption of innovative glass designs and the resurgence of returnable and reusable glass bottles, which align with environmental sustainability goals. Additionally, the rising consumption of alcoholic and non-alcoholic beverages in countries like India and China significantly contributes to the market's expansion. The market's evolution is further supported by advancements in glass manufacturing technologies and the increasing preference for premium glass packaging solutions.

China Glass Bottles And Containers Market Analysis

China plays a pivotal role in the global glass bottle industry, driven by its robust manufacturing capabilities and significant domestic demand. The country's expanding middle class and urbanization are key growth drivers, leading to increased consumption of beverages and pharmaceuticals, which heavily rely on glass packaging. Trends such as the rising preference for premium glass packaging and eco-friendly materials are shaping the market, with innovations in design and functionality gaining traction. Additionally, partnerships between beverage and packaging companies are fostering market growth, as seen in recent collaborations targeting younger demographics. The market in China is projected to grow at a CAGR of approximately 5% from 2024 to 2029, reflecting its dynamic and evolving nature.

India Glass Bottles And Containers Market Analysis

India plays a pivotal role in the glass bottle manufacturing industry, driven by its large population and growing demand across various sectors such as beverages, pharmaceuticals, and food packaging. The market is significantly influenced by the increasing consumption of alcoholic beverages, with glass being the preferred material due to its ability to preserve the quality of the contents. Additionally, the rise in demand for non-alcoholic beverages and the adoption of sustainable glass packaging solutions further bolster the market's growth. Trends such as the resurgence of returnable glass bottles and innovations in ready-to-drink alcoholic products highlight the dynamic nature of the Indian market. The market is projected to grow at a CAGR of approximately 7% from 2024 to 2029, reflecting robust demand and evolving consumer preferences.

Japan Glass Bottles And Containers Market Analysis

Japan is projected to account for approximately 6% of the global glass bottles and containers market in 2024. The Japanese market is characterized by its emphasis on sustainability and innovation, with a strong focus on reducing plastic waste and promoting eco-friendly glass packaging solutions. Key drivers include government regulations, such as the 2022 law to reduce single-use plastics, which have encouraged the adoption of glass as a sustainable alternative. Trends in the market highlight the increasing use of glass packaging in beverage and food packaging, supported by its recyclability and safety for food storage. Additionally, collaborations between companies and recycling initiatives are fostering a circular economy, further solidifying Japan's role as a leader in sustainable packaging solutions.

South Korea Glass Bottles And Containers Market Analysis

South Korea plays a pivotal role in the glass bottle industry within the Asia-Pacific region, driven by its robust beverage industry and cultural emphasis on traditional alcoholic beverages like Soju. The market's growth is fueled by increasing demand for sustainable glass packaging solutions and the rising consumption of beverages, both alcoholic and non-alcoholic. Notable trends include the adoption of eco-friendly glass packaging and the influence of South Korea's vibrant drinking culture, which promotes the use of glass bottles for premium beverages. Additionally, the market is witnessing a shift towards innovative designs and lightweight glass containers to cater to consumer preferences and environmental concerns. These factors collectively position South Korea as a significant contributor to the regional glass packaging industry.

Australia and New Zealand Glass Bottles And Containers Market Analysis

The glass bottles and containers market in Australia and New Zealand is characterized by its robust demand across diverse sectors, including beverages, pharmaceuticals, and food packaging, driven by the regions' emphasis on sustainability and premium product presentation. Key growth drivers include the increasing consumer preference for eco-friendly glass packaging solutions and the rising demand for high-quality glass containers in the alcoholic and non-alcoholic beverage industries. Notable trends include the adoption of innovative manufacturing techniques to enhance the durability and aesthetic appeal of glass products, as well as the integration of recycled materials to align with environmental goals. Additionally, the market is witnessing a shift towards lightweight glass packaging to reduce transportation costs and carbon footprint. These factors collectively underscore the strategic importance of the glass bottles and containers market in supporting the sustainable packaging initiatives of Australia and New Zealand.

Middle East and Africa Glass Bottles And Containers Market Analysis

The Middle East and Africa region plays a pivotal role in the global glass bottle industry, driven by its unique combination of abundant raw material availability and a growing demand for sustainable glass packaging solutions. Key growth drivers include increasing urbanization and disposable income levels, which fuel the demand for packaged food and beverages, as well as the region's strategic focus on sustainability and recycling initiatives. Notable trends include the rising adoption of glass packaging in the food and beverage sector, supported by its superior preservation qualities and environmental benefits. Additionally, the region's glass manufacturing industry benefits from low energy costs and significant investments in production capacity expansions, enhancing its competitive edge. These factors collectively position the Middle East and Africa as a dynamic and evolving market for glass bottles and containers.

United Arab Emirates Glass Bottles And Containers Market Analysis

The United Arab Emirates plays a pivotal role in the glass bottle industry within the Middle East due to its strategic location and robust economic framework. The market is driven by increasing demand in sectors such as pharmaceuticals, personal care, and beverages, supported by the UAE's focus on sustainability and innovation. Notable trends include the adoption of eco-friendly glass packaging solutions and the rising preference for glass over plastic due to environmental concerns. Additionally, government initiatives like the Dubai Industrial Strategy 2050 aim to bolster industrial growth, further enhancing the market's potential. The UAE's emphasis on high-quality standards and its position as a trade hub amplify its significance in the regional market.

Saudi Arabia Glass Bottles And Containers Market Analysis

Saudi Arabia plays a pivotal role in the glass bottle industry due to its strategic position as a hub for trade and its robust industrial base. The market is driven by increasing consumer preferences for sustainable glass packaging solutions, supported by government regulations promoting eco-friendly materials over plastics. Trends indicate a growing demand for glass packaging in sectors such as beverages, pharmaceuticals, and cosmetics, fueled by rising disposable incomes and a shift towards premium products. Additionally, the country's initiatives to diversify its economy and enhance local manufacturing capabilities further bolster the market's growth. The emphasis on recycling and sustainability aligns with global trends, positioning Saudi Arabia as a key player in the regional glass packaging industry.

South Africa Glass Bottles And Containers Market Analysis

South Africa plays a pivotal role in the glass bottle industry due to its robust manufacturing capabilities and strategic position in the region. The market is driven by increasing demand from the beverage industry, particularly for alcoholic and non-alcoholic beverages, as well as growing sustainability initiatives promoting glass recycling. Notable trends include investments in production facilities, such as the expansion of Ardagh Group's capacity, and partnerships like Heineken's acquisition of local breweries, which enhance regional production and export potential. Additionally, the versatility and eco-friendly nature of glass packaging make it a preferred choice for food preservation and beverage storage, aligning with consumer preferences for sustainable and high-quality packaging solutions. South Africa's advancements in glass recycling and production efficiency further solidify its position as a key player in the global glass packaging industry.

Latin America Glass Bottles And Containers Market Analysis

The Latin America glass bottles and containers market is characterized by its dynamic growth and diverse applications across industries such as food and beverages, pharmaceuticals, and cosmetics. Brazil, as the largest market in the region, benefits from significant investments in sustainable glass production facilities, driven by the beverage and pharmaceutical sectors. Mexico, with its strong tradition in alcoholic beverages, has seen a surge in demand for glass containers, supported by its advanced glass manufacturing capabilities. Argentina's market is bolstered by its robust food and beverage industry, alongside government initiatives to enhance local glass production. The rest of Latin America, including countries like Chile and Colombia, is witnessing growth due to increasing consumer preference for environmentally friendly packaging and the expansion of the food and beverage sector. Across the region, trends such as the adoption of lightweight glass for reduced CO2 emissions and the use of innovative designs in glass packaging are shaping the market. The recyclable nature of glass and its alignment with sustainability goals further enhance its appeal, positioning the Latin American market as a key player in the global glass packaging industry.

Brazil Glass Bottles And Containers Market Analysis

Brazil plays a pivotal role in the glass bottle industry within Latin America, driven by its robust industrial base and expanding end-user industries. The country's market is bolstered by significant investments in sustainable glass production facilities, such as those by Ambev and Ardagh Group, which aim to enhance manufacturing capabilities and promote circular packaging solutions. Trends indicate a growing preference for environmentally friendly and recyclable packaging, aligning with global sustainability goals. Additionally, the pharmaceutical sector's expansion in Brazil further propels the demand for glass containers, given their suitability for preserving product integrity. These factors, combined with Brazil's strategic position in the region, underscore its importance in shaping the future of the glass packaging industry.

Mexico Glass Bottles And Containers Market Analysis

Mexico plays a pivotal role in the glass bottle industry, driven by its robust manufacturing capabilities and significant demand from industries such as beverages, pharmaceuticals, and cosmetics. The country's traditional production of alcoholic beverages, including tequila and beer, significantly contributes to the demand for glass packaging. Trends indicate a growing preference for sustainable and recyclable materials, positioning glass as a favored choice due to its eco-friendly properties. Additionally, advancements in manufacturing technologies and investments in capacity expansion by major players are enhancing production efficiency and meeting rising demand. However, challenges such as supply shortages and increasing raw material costs are influencing market dynamics, prompting industries to explore alternative packaging solutions.

Argentina Glass Bottles And Containers Market Analysis

Argentina plays a pivotal role in the glass bottle industry within Latin America, driven by its robust food and beverage industry and increasing demand for sustainable glass packaging solutions. The market is bolstered by the growing preference for glass packaging due to its recyclability and inert properties, making it ideal for preserving the quality of consumables. Key trends include the rise in demand for glass containers in the cosmetics and pharmaceutical sectors, supported by investments in local production facilities. Additionally, the government's initiatives to enhance domestic manufacturing capabilities and the increasing adoption of eco-friendly practices among consumers are significant growth drivers. The market is also witnessing a shift towards innovative and aesthetically appealing glass packaging designs, catering to the evolving preferences of end-users.

Glass Bottles and Containers Market Overview

Top Companies in the Glass Bottles and Containers Market

- O-I Glass, Inc.

- Vidrala SA

- Ardagh Group S.A.

- Vetropack Holding SA

- PGP Glass Private Limited

- Verallia SA

- Wiegand-glas GmbH

- Stoelzle Oberglas GmbH

- Gaasch Packaging

- Beatson Clark

- Vitro SAB de CV

- Schott AG

- Glassworks International Limited

- Gerresheimer AG

- Middle East Glass Manufacturing Co.

- Berlin Packaging LLC

- BA Glass Group

- Verescence France SASU

- SGD S.A.

- Saverglass Group

The glass bottles and containers market is characterized by a focus on product innovation and operational efficiency. Glass bottle manufacturers are developing lightweight and sustainable glass solutions to meet environmental goals and reduce costs. Strategic collaborations and partnerships are being leveraged to enhance technological capabilities and expand market reach. Expansion efforts are concentrated on increasing production capacity and entering emerging markets to capture growing demand.

Market Characteristics: Consolidation and Global Presence

The glass bottle manufacturing industry is dominated by a mix of global conglomerates and regional specialists. Major players like O-I Glass, Ardagh Group, and Verallia have a strong presence across multiple regions, while smaller companies focus on niche markets. The industry exhibits moderate consolidation, with leading firms holding significant market shares. Mergers and acquisitions are prevalent, aimed at achieving scale, technological advancements, and geographic expansion.

Vertical integration is a notable trend, with companies investing in raw material supply chains to ensure stability and cost control. Sustainability is a key focus, with investments in recycling and eco-friendly production methods. Regulatory pressures related to environmental standards are influencing innovation in energy-efficient manufacturing and sustainable product development.

Future Success Factors: Innovation and Sustainability Focus

To maintain or grow market share, glass bottle manufacturers must prioritize innovation and sustainability. Investments in advanced glass bottle manufacturing technologies and the development of lightweight, durable glass products are critical. Contenders can differentiate by targeting niche markets or offering unique design solutions. Strong customer relationships in key sectors like beverages and pharmaceuticals are essential.

The risk of substitution by alternative materials such as plastics and aluminum remains a challenge. Emphasizing glass's recyclability and premium appeal can mitigate this threat. Regulatory developments, particularly concerning emissions and recycling, will shape the competitive landscape. Companies that proactively adopt low-carbon technologies and circular economy practices will be better positioned for future success.

Glass Bottles and Containers Market News

-

O-I Glass, Inc.

-

Ardagh Group S.A.

-

Vetropack Holding SA

-

PGP Glass Private Limited

-

Vidrala SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Container Glass Market News

- September 2024: Ardagh Glass Packaging-North America, a division of Ardagh Group, has unveiled a new line of craft beverage bottles, expanding its portfolio of American-made offerings. These 12-ounce glass bottles, crafted in the United States, come in three vibrant colors: emerald green, flint (clear), and amber (brown). Available for direct purchase from AGP-North America, these bottles are produced using high-quality, 100% recyclable glass. Notably, the glass can be recycled endlessly without any degradation in purity or quality, as emphasized by the company.

- February 2024: O-I Glass has debuted its inaugural eco-designed 75 cl bottle tailored for the wine industry. This bottle's carbon footprint and its journey towards carbon neutrality have received validation from the Carbon Trust, a renowned climate consultancy. Weighing in at 390g and crafted using 82% recycled glass, the Estampe bottle boasts a carbon footprint of 249g of CO2 equivalent. This marks a 25% reduction in carbon emissions when juxtaposed with traditional 500g bottles. Furthermore, its sleek and contemporary design has garnered an impressive 84% purchasing intent among consumers.

Glass Bottles and Containers Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Export-Import Data of Container Glass

- 4.3 Industry Standard and Regulation For Container Glass Use For Packaging

- 4.4 Raw Material Analysis and Material Consideration For Packaging

- 4.5 Sustainability Trends For Glass Packaging

- 4.6 Container Glass Furnace and Location

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growing Demand from Food and Beverage Industry

- 5.1.2 Sustainability and Recyclability Initiatives Are Expanding End-Users Demand For Glass Packaging

-

5.2 Market Restraints

- 5.2.1 High Carbon Footprint due to Glass Manufacturing

- 5.2.2 Operation and Logistical Concerns

- 5.3 Trade Scenario - Analysis of the Historical and Current Export-Import Paradigm For Container Glass Industry

6. MARKET SEGMENTATION

-

6.1 By End-user Vertical

- 6.1.1 Bevarages

- 6.1.1.1 Alcoholic (Qualitative Analysis to be Provided)

- 6.1.1.1.1 Beer and Cider

- 6.1.1.1.2 Wine and Spirits

- 6.1.1.1.3 Other Alcoholic Beverages

- 6.1.1.2 Non-Alcoholic (Qualitative Analysis to be Provided)

- 6.1.1.2.1 Carbonated Soft Drinks

- 6.1.1.2.2 Milk

- 6.1.1.2.3 Water and Other Non-alcoholic Beverages

- 6.1.2 Food

- 6.1.3 Cosmetics

- 6.1.4 Pharmaceutical (Excluding Vials and Ampoules)

- 6.1.5 Other End-user Verticals

-

6.2 By Geography*

- 6.2.1 North America

- 6.2.1.1 United States

- 6.2.1.2 Canada

- 6.2.2 Europe

- 6.2.2.1 France

- 6.2.2.2 Germany

- 6.2.2.3 Italy

- 6.2.2.4 United Kingdom

- 6.2.2.5 Spain

- 6.2.2.6 Poland

- 6.2.2.7 Russia

- 6.2.2.8 Denmark

- 6.2.2.9 Sweden

- 6.2.2.10 Belgium

- 6.2.2.11 Czech Republic

- 6.2.2.12 Netherlands

- 6.2.2.13 Ukraine

- 6.2.2.14 Austria

- 6.2.2.15 Hungary

- 6.2.3 Asia

- 6.2.3.1 China

- 6.2.3.2 India

- 6.2.3.3 Japan

- 6.2.3.4 Thailand

- 6.2.3.5 Australia and New Zealand

- 6.2.3.6 South Korea

- 6.2.3.7 Indonesia

- 6.2.3.8 Vietnam

- 6.2.4 Middle East and Africa

- 6.2.4.1 United Arab Emirates

- 6.2.4.2 Saudi Arabia

- 6.2.4.3 Egypt

- 6.2.4.4 Kuwait

- 6.2.4.5 South Africa

- 6.2.4.6 Nigeria

- 6.2.4.7 Morocco

- 6.2.5 Latin America

- 6.2.5.1 Brazil

- 6.2.5.2 Mexico

- 6.2.5.3 Colombia

- 6.2.5.4 Chile

- 6.2.5.5 Argentina

- 6.2.5.6 Uruguay

- 6.2.5.7 Ecuador

7. COMPETITIVE LANDSCAPE

-

7.1 Company Profiles

- 7.1.1 O-I Glass, Inc.

- 7.1.2 Vidrala SA

- 7.1.3 Ardagh Group S.A.

- 7.1.4 Vetropack Holding SA

- 7.1.5 PGP Glass Private Limited

- 7.1.6 Verallia SA

- 7.1.7 Wiegand-glas GmbH

- 7.1.8 Stoelzle Oberglas GmbH

- 7.1.9 Gaasch Packaging

- 7.1.10 Beatson Clark

- 7.1.11 Vitro SAB de CV

- 7.1.12 Schott AG

- 7.1.13 Glassworks International Limited

- 7.1.14 Gerresheimer AG

- 7.1.15 Middle East Glass Manufacturing Co.

- 7.1.16 Berlin Packaging LLC

- 7.1.17 BA Glass Group

- 7.1.18 Verescence France SASU

- 7.1.19 SGD S.A.

- 7.1.20 Saverglass Group

- *List Not Exhaustive

8. REGION WISE ANALYSIS OF MAJOR FURNACE SUPPLIER TO THE CONTAINER GLASS PLANTS (North America, Asia-Pacific, Europe, Middle East and Africa and Latin America)

9. FUTURE OUTLOOK OF THE MARKET

**Subject to Availability

***In the final report, Asia, Australia, and New Zealand will be studied together as 'Asia Pacific' andand the Rest of Europe, the Rest of Asia, the Rest of the Middle East and Africa, and the rest of Latin America will be studied as separate segments.

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Glass Bottles and Containers Market Leaders

Glass containers market tracks the demand of glass packaging containers and bottles across the end-users industries including beverage, food, pharmaceutical, cosmetics and others. Glass containers are majorly used in the alcoholic and non-alcoholic beverage industry due to their ability to maintain chemical inertness and sterility and non-permeability.

The Container Glass market is segmented by end-user vertical (beverages [alcoholic (beer and cider, wine & spirits, and other alcoholic beverages] and non-alcoholic [carbonated soft drinks, milk, and water and other non-alcoholic beverages]), food, cosmetics, pharmaceutical, and other end-user verticals) and by geography (North America [United States and Canada], Europe [France, Germany, Italy, United Kingdom, Spain, Poland, Russia, Nordic and Rest of Europe], Asia-Pacific [China, India, Japan, Thailand, New Zealand and Australia, South Korea, Indonesia, Vietnam, and Rest of Asia -Pacific], Middle East and Africa [United Arab Emirates, Saudi Arabia, Egypt, Kuwait, South Africa, Nigeria, Morocco, and Rest of Middle East and Africa] and Latin America [Brazil, Mexico, Colombia, Chile, Argentina, and Rest of Latin America]). The market sizes and forecasts are provided in terms of consumption volume (tonnes) for all the above segments.

| By End-user Vertical | Bevarages | Alcoholic (Qualitative Analysis to be Provided) | Beer and Cider | |

| Wine and Spirits | ||||

| Other Alcoholic Beverages | ||||

| Non-Alcoholic (Qualitative Analysis to be Provided) | Carbonated Soft Drinks | |||

| Milk | ||||

| Water and Other Non-alcoholic Beverages | ||||

| Food | ||||

| Cosmetics | ||||

| Pharmaceutical (Excluding Vials and Ampoules) | ||||

| Other End-user Verticals | ||||

| By Geography* | North America | United States | ||

| Canada | ||||

| Europe | France | |||

| Germany | ||||

| Italy | ||||

| United Kingdom | ||||

| Spain | ||||

| Poland | ||||

| Russia | ||||

| Denmark | ||||

| Sweden | ||||

| Belgium | ||||

| Czech Republic | ||||

| Netherlands | ||||

| Ukraine | ||||

| Austria | ||||

| Hungary | ||||

| Asia | China | |||

| India | ||||

| Japan | ||||

| Thailand | ||||

| Australia and New Zealand | ||||

| South Korea | ||||

| Indonesia | ||||

| Vietnam | ||||

| Middle East and Africa | United Arab Emirates | |||

| Saudi Arabia | ||||

| Egypt | ||||

| Kuwait | ||||

| South Africa | ||||

| Nigeria | ||||

| Morocco | ||||

| Latin America | Brazil | |||

| Mexico | ||||

| Colombia | ||||

| Chile | ||||

| Argentina | ||||

| Uruguay | ||||

| Ecuador | ||||

Need A Different Region or Segment?

Customize Now

Glass Bottles and Containers Market Research FAQs

How big is the Glass Bottles And Containers Market?

The Glass Bottles And Containers Market size is expected to reach 98.55 million tonnes in 2025 and grow at a CAGR of 3.39% to reach 116.43 million tonnes by 2030.

What is the current Glass Bottles And Containers Market size?

In 2025, the Glass Bottles And Containers Market size is expected to reach 98.55 million tonnes.

Which is the fastest growing region in Glass Bottles And Containers Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Glass Bottles And Containers Market?

In 2025, the Europe accounts for the largest market share in Glass Bottles And Containers Market.

What years does this Glass Bottles And Containers Market cover, and what was the market size in 2024?

In 2024, the Glass Bottles And Containers Market size was estimated at 95.21 million tonnes. The report covers the Glass Bottles And Containers Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Glass Bottles And Containers Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Glass Bottles and Containers Market Industry Report

Statistics for the 2025 Glass Bottles and Containers market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Glass Bottles and Containers analysis includes a market forecast outlook for 2025 to 2030 and historical overview. Get a sample of this industry analysis as a free report PDF download.