Market Overview

| Study Period | 2020 - 2031 |

|---|---|

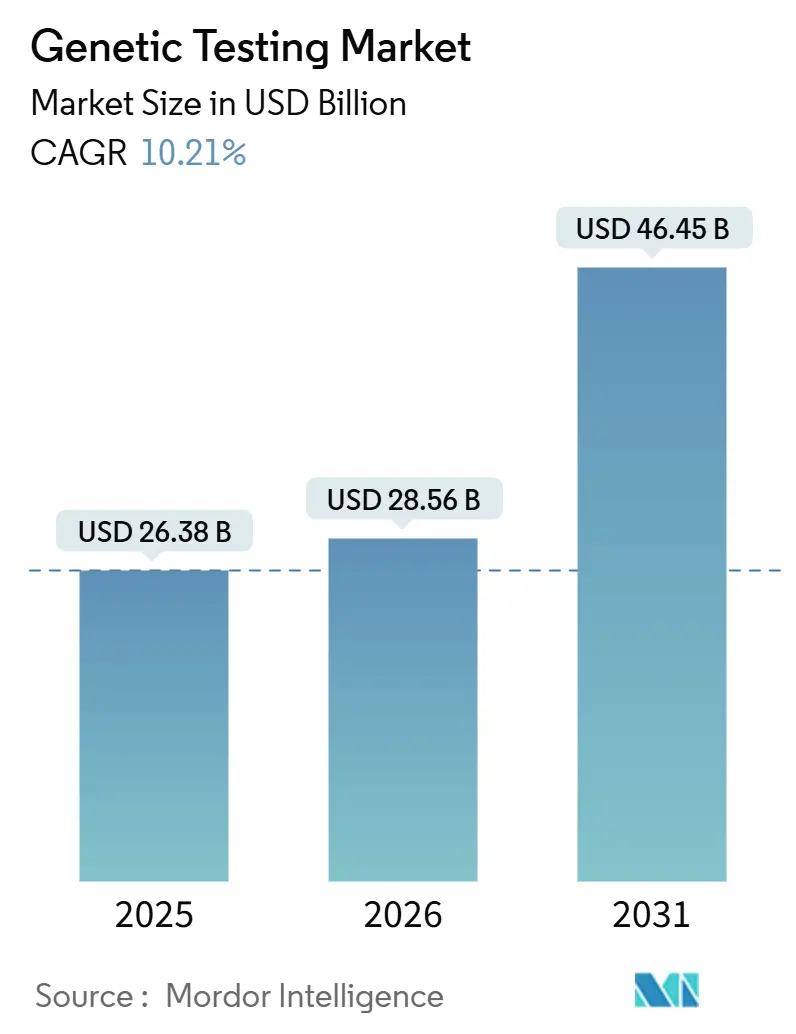

| Market Size (2026) | USD 28.56 Billion |

| Market Size (2031) | USD 46.45 Billion |

| Growth Rate (2026 - 2031) | 10.21% CAGR |

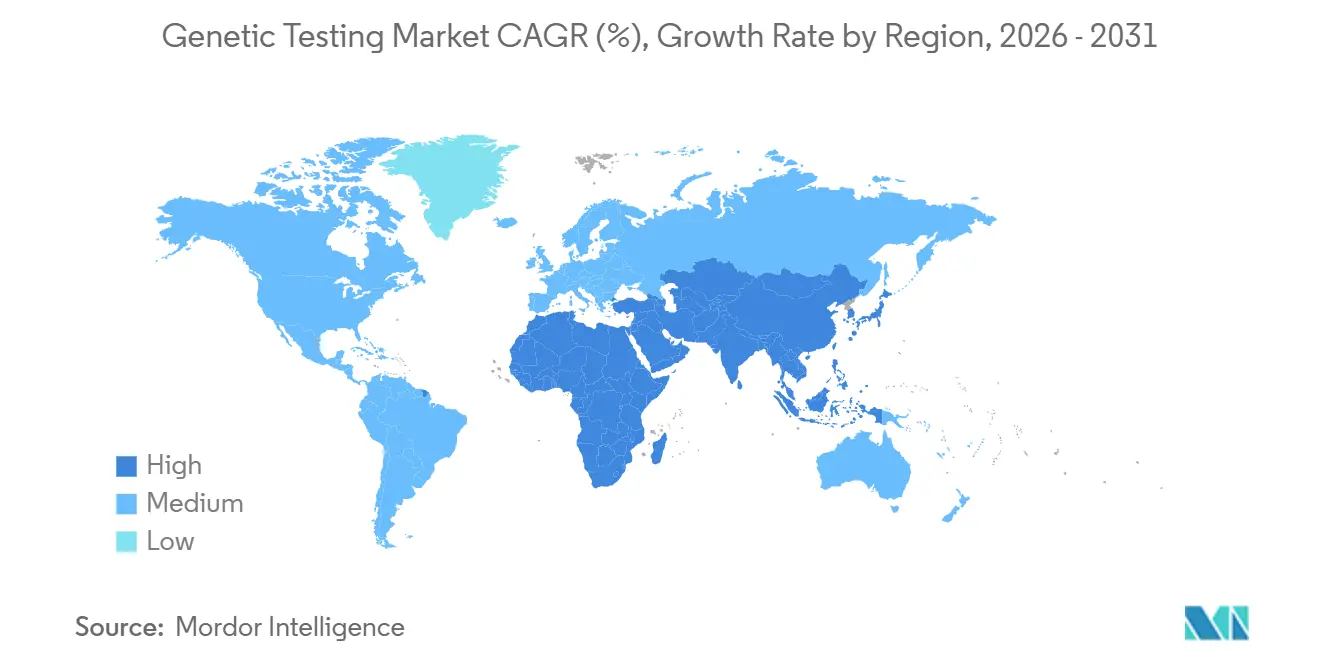

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

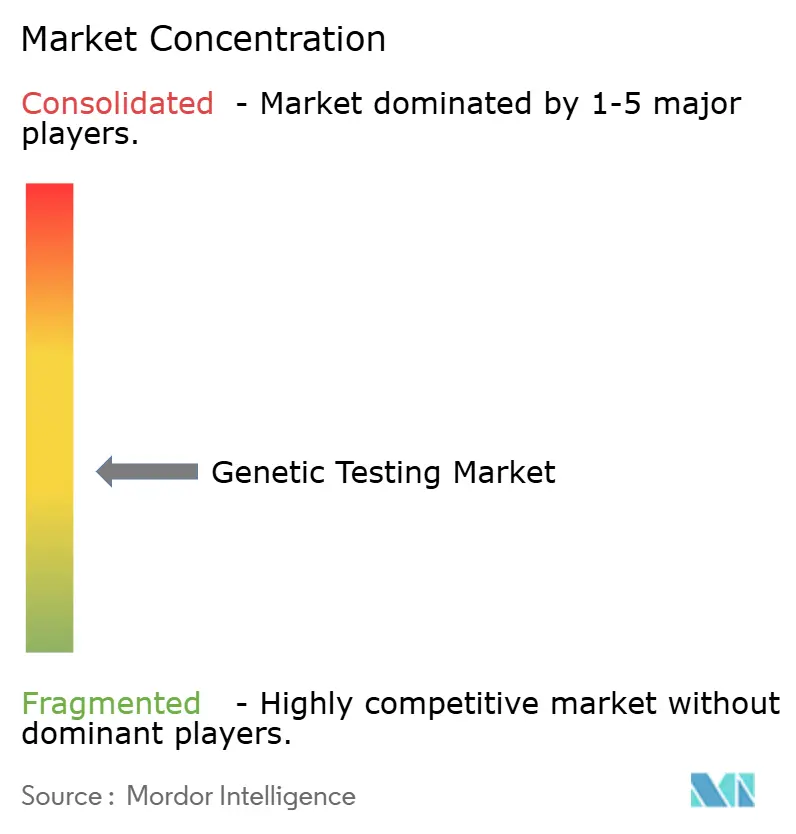

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Genetic Testing Market Analysis by Mordor Intelligence

The Genetic Testing Market size is expected to increase from USD 26.38 billion in 2025 to USD 28.56 billion in 2026 and reach USD 46.45 billion by 2031, growing at a CAGR of 10.21% over 2026-2031.

Mainstream reimbursement for multigene panels, whole-genome sequencing costs that will dip below USD 100 after 2027, and employer-funded genomic wellness programs are scaling demand in the genetic testing market. Non-invasive prenatal testing (NIPT) and newborn screening mandates in 30 U.S. states add steady volume, while FDA-cleared liquid-biopsy pathways from 2024 onward accelerate oncology adoption. Cloud-based AI interpretation platforms such as Illumina DRAGEN on Microsoft Azure now compress analysis from weeks to hours, enabling same-visit clinical decisions. Rapid payer uptake, falling sequencing costs, and real-time analytics collectively keep the genetic testing market on a double-digit growth trajectory.

Key Report Takeaways

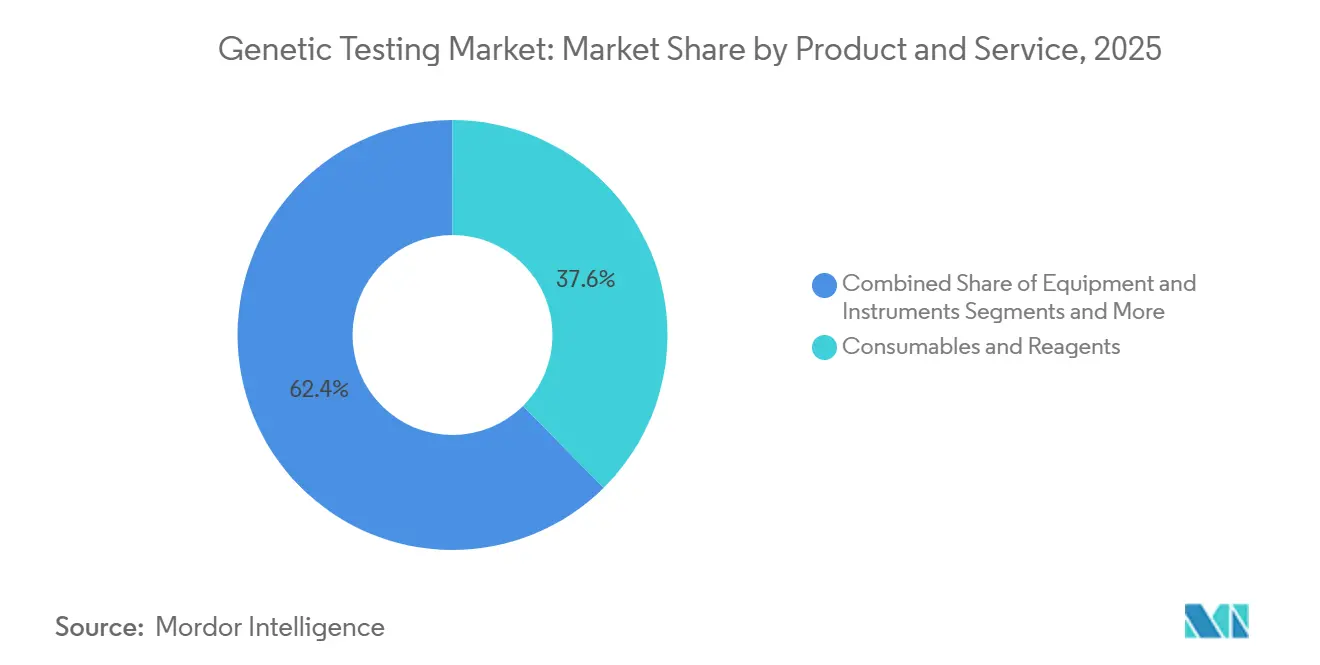

- By product & service, consumables and reagents led with 37.57% revenue share in 2025, whereas software and services are projected to post a 14.57% CAGR through 2031.

- By test type, prenatal and newborn assays held 36.25% of the 2025 genetic testing market share, while carrier screening is expected to grow at 13.34% CAGR to 2031.

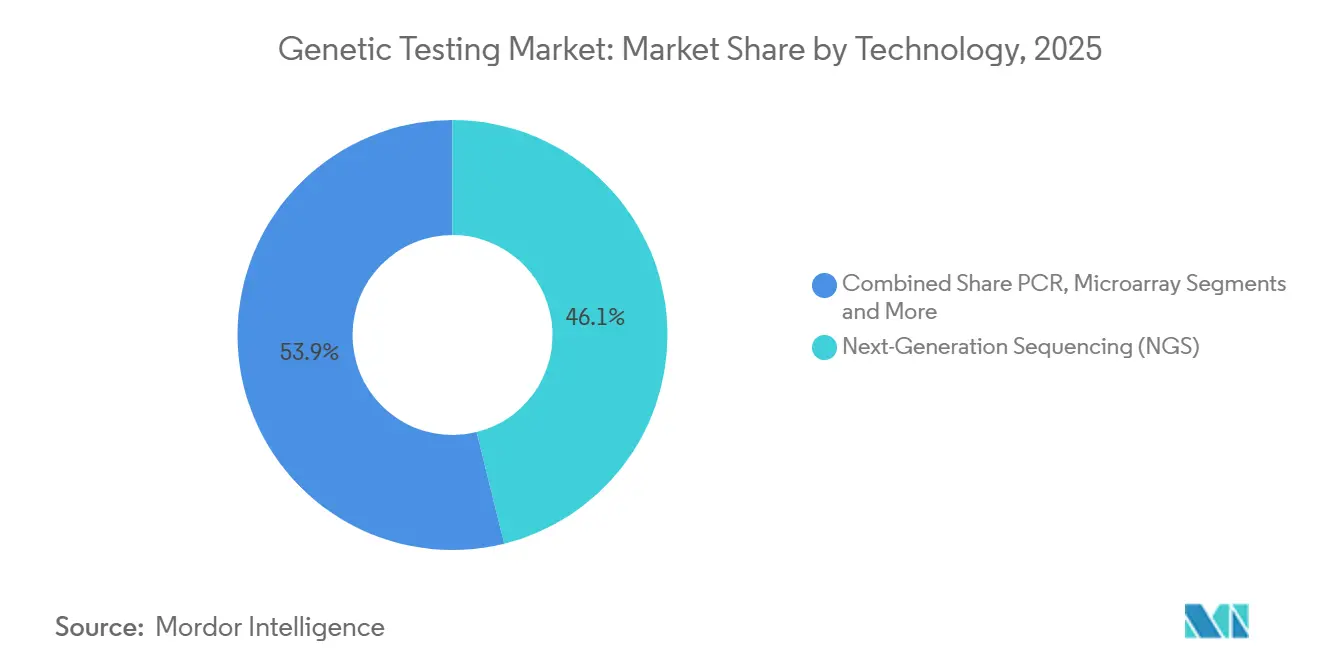

- By technology, next-generation sequencing captured 46.13% of 2025 revenue and will continue expanding at a 12.67% CAGR through the forecast window.

- By application, genetic disease diagnosis commanded 39.63% of 2025 revenue, yet oncology leads growth with a 13.88% CAGR to 2031.

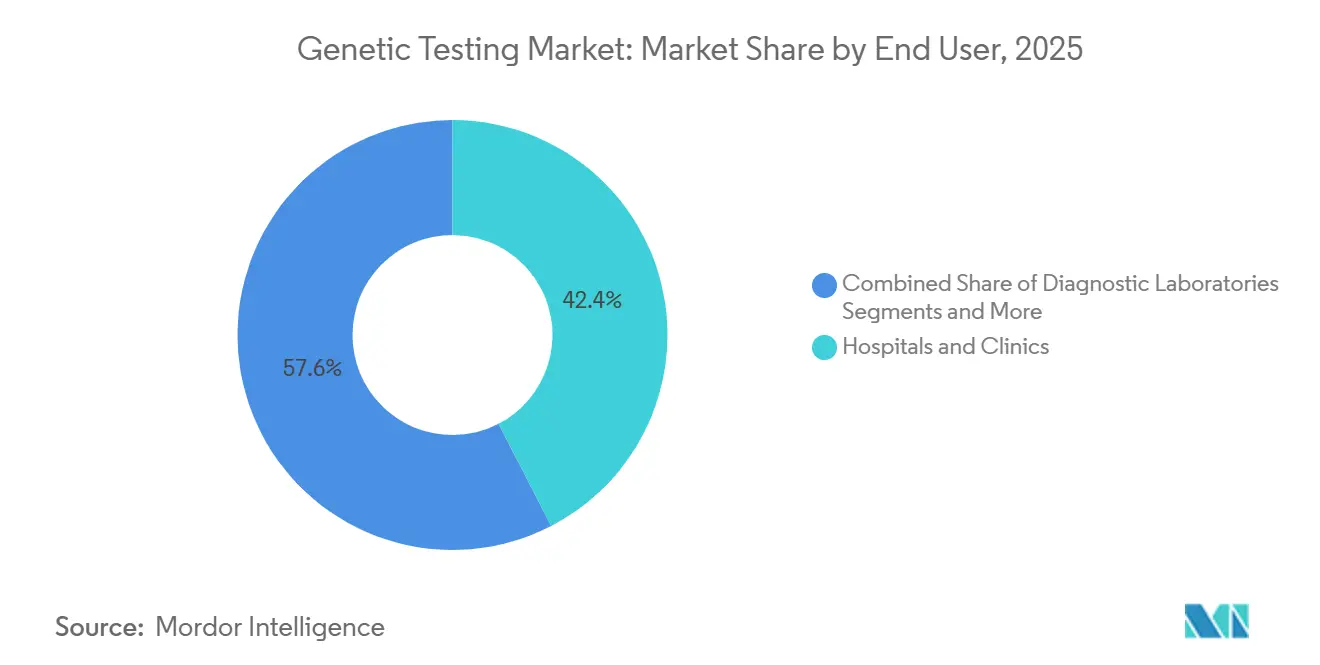

- By end user, hospitals and clinics accounted for 42.41% in 2025, whereas research and academic institutes will register a 12.21% CAGR.

- By geography, North America held 43.13% in 2025, while Asia-Pacific is poised for a 12.63% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Genetic Testing Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Adoption of NIPT & Newborn Screening | +1.8% | North America, Europe, APAC core | Short term (≤ 2 years) |

| Mainstream Insurance Coverage for Multigene Panels | +2.1% | North America, Western Europe | Medium term (2-4 years) |

| Falling NGS Cost to Less Than USD 100/Whole Genome (Post-2027) | +1.5% | Global | Long term (≥ 4 years) |

| Cloud-Based AI Genomic Interpretation Ecosystems | +1.3% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Liquid-Biopsy-Ready Regulatory Pathways | +1.6% | North America, Europe, Japan | Short term (≤ 2 years) |

| Employer-Sponsored Genomic Wellness Benefits Surge | +1.2% | North America, select APAC markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Adoption of NIPT & Newborn Screening

Commercial payers in the United States covered NIPT for trisomies 13, 18, and 21 without prior authorization by 2025, lifting penetration above 80%.[1]UnitedHealthcare Editorial Team, “Prior Authorization Requirements for Non-Invasive Prenatal Testing,” UnitedHealthcare Provider, uhcprovider.com Thirty states simultaneously expanded newborn panels to 35 core conditions, boosting demand for Natera Panorama and PerkinElmer platforms. Updated American College of Obstetricians and Gynecologists guidance designated NIPT as a first-tier option for all pregnancies in 2024, removing risk-based barriers.[2]ACOG Advocacy Team, “Non-Invasive Prenatal Testing,” American College of Obstetricians and Gynecologists, acog.org The shift converted prenatal testing from niche to universal coverage, shortening reimbursement cycles and enabling direct-to-consumer channels. China began reimbursing NIPT in tier-1 cities in 2025, yet rural provinces remain self-pay, creating uneven adoption.

Mainstream Insurance Coverage for Multigene Panels

Medicare added BRCA1/2, PALB2, and ATM to its hereditary cancer panel coverage in 2024, aligning with NCCN guidelines. Commercial payers followed by reimbursing 25- to 80-gene panels for eligible members, pushing Myriad MyRisk and Invitae volumes up 40% year-over-year. Average panel reimbursement settled near USD 250, down steeply from historical levels, making proactive testing financially attractive to payers focused on avoiding late-stage cancer costs. Germany still limits BRCA testing to post-diagnosis use, curbing preventive uptake.

Falling NGS Cost below USD 100/Genome

Illumina’s NovaSeq X Plus reached USD 200 per genome in 2024, and the firm projects sub-USD 100 pricing by 2028 as chemistry and throughput improve.[3]Illumina Newsroom, “Illumina's Revolutionary NovaSeq X Exceeds 200th Order Milestone in First Quarter 2023,” Illumina Investor Relations, investor.illumina.com Competing releases from Complete Genomics and BGI are targeting the same benchmark in 2025. Lower costs enable population-scale projects such as the NHS Genomic Medicine Service, which sequenced 500,000 genomes by 2025 and reported actionable findings in 25% of participants. India’s 10,000-genome pilot launched in 2025 at sub-USD 500 per sample, illustrating the democratization of sequencing.

Cloud-Based AI Genomic Interpretation Ecosystems

Illumina DRAGEN on Microsoft Azure cut variant calling from 24 hours to 30 minutes in 2025, supporting same-day neonatal results. Nvidia Clara Parabricks lowers compute costs by 60% versus CPU pipelines, letting regional labs rent capacity instead of buying servers. The FDA released draft guidance on AI-driven genomic software in 2024, clarifying compliance pathways for cloud platforms. Interoperability hurdles persist because proprietary data formats require middleware for seamless EHR integration in resource-constrained sites.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-Border Data Sovereignty Restrictions | -0.9% | Global, acute in EU & China | Short term (≤ 2 years) |

| Skilled Genetic Counselor Shortage Bottlenecks | -0.7% | Global, severe in emerging markets | Medium term (2-4 years) |

| Patchy Reimbursement in Emerging Economies | -1.1% | APAC (ex-Japan), MEA, South America | Long term (≥ 4 years) |

| NGS Chip Supply-Chain Dependency on 2 Fabs | -0.6% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cross-Border Data Sovereignty Restrictions

The EU Health Data Space regulation effective May 2025 mandates EU server residency for genomic data, fragmenting multinational datasets. China’s rules likewise require domestic storage and government approval for sharing human genetic material abroad, limiting global collaboration. These policies raise compliance costs as labs must maintain separate infrastructures and navigate conflicting consent frameworks, delaying cross-border assay launches.

Skilled Genetic Counselor Shortages

Only about 7,000 certified counselors serve a global testing volume topping 10 million annually. The American Board of Genetic Counseling graduated 400 professionals in 2025, far short of demand. Tele-counseling expands reach, yet reimbursement remains patchy, especially across U.S. Medicaid programs. Emerging economies such as India have fewer than 50 counselors, forcing labs to rely on clinicians who lack bandwidth for in-depth guidance, thereby prolonging test ordering and elevating misinterpretation risk.

Segment Analysis

By Product & Service: Software Scales Interpretation Bottlenecks

Consumables and reagents held 37.57% of 2025 revenue, reinforcing their role as the consumable backbone of the genetic testing market. Software and services, however, will advance at a 14.57% CAGR to 2031 as interpretation rather than sequencing becomes the primary bottleneck. The genetic testing market size for software offerings is projected to widen as laboratories shift from high-capex servers to cloud subscriptions billed below USD 50,000 per year. EU IVDR rules that require CE-marked interpretation software further drive migration away from in-house pipelines. Equipment sales face semiconductor delays that stretch instrument lead times to a year, but reagent purchases remain recurring and predictable.

Recurring revenue models improve vendor cash flows while lowering startup costs for mid-tier labs. Each NovaSeq X shipped in 2025 consumes roughly USD 1 million in reagents annually at full utilization, creating annuity-like sales for Illumina. Software vendors monetize variant databases through tiered analytics, enabling community hospitals to run pan-cancer panels without dedicated bioinformaticians. Genetic testing industry players offering bundled counseling, interpretation, and billing support gain a competitive edge with payers that assess total episode cost.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Test Type: Carrier Screening Extends Beyond Ancestry-Based Panels

Prenatal and newborn assays accounted for 36.25% in 2025, yet carrier screening is poised to grow at 13.34% CAGR as guidelines shift toward pan-ethnic panels. The genetic testing market size for carrier screening will broaden because expanded menus now cover over 400 conditions, replacing earlier Ashkenazi-focused offerings. Diagnostic testing remains high-volume but faces price pressure as exome sequencing displaces single-gene assays. Predictive panels continue to benefit from Medicare and commercial payer coverage, although uptake among unaffected adults remains modest due to privacy concerns despite GINA protections.

Expanded carrier screening surged after ACMG recommended universal panels in 2024. Adoption among fertility clinics rose 50% in 2025 for Natera Horizon. Payers, however, increasingly demand evidence of negative targeted tests before approving exome claims, a dynamic that pushes patients through stepwise testing. Pharmacogenomic panels advance at roughly 10% CAGR, but lack of EHR decision support slows physician adoption. Direct-to-consumer ancestry tests saw contraction in 2024 as privacy concerns drove 23andMe to pivot away from therapeutics and cut staff.

By Technology: NGS Dominates While Long-Read Platforms Enter Clinics

Next-generation sequencing captured 46.13% of technology revenue in 2025 and is expected to retain double-digit growth. Cost declines and multi-gene flexibility make NGS the default for oncology and rare disease diagnostics. Polymerase chain reaction retains niches in high-throughput single-gene testing, while microarray use contracts as NIPT supplants it in prenatal care. Cytogenetic techniques and FISH remain standard for certain hematologic disorders due to rapid turnaround and established reimbursement.

Long-read sequencing moved from research to clinics when Pacific Biosciences Revio cut per-genome costs to USD 1,000 in 2024. Oxford Nanopore’s MinION devices, deployed in field outbreaks, underscore NGS versatility in infectious disease surveillance. Guardant360 CDx and similar assays exemplify NGS utility in liquid biopsy, reducing tissue-based turnaround from 14 days to 7 days. The genetic testing market share for NGS will therefore expand as both short- and long-read platforms climb clinical adoption curves.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Oncology Surpasses Genetic Disease Diagnosis in Growth Pace

Genetic disease diagnosis topped 39.63% in 2025, yet oncology testing is projected to register a 13.88% CAGR, the highest among applications. Liquid biopsy assays tap large addressable populations; Medicare coverage for Natera Signatera in colorectal and breast cancer scaled eligible patients tenfold in 2024. Early detection tests such as Exact Sciences Cologuard Plus broaden screening beyond colonoscopy.

Reproductive health remains robust but is nearing saturation in developed markets, shifting future growth to emerging regions where reimbursement is debuting. Direct-to-consumer wellness testing declined as consumer trust eroded. Pharmacogenomics lags because clinical decision support integration into EHRs is incomplete, though over 300 drug labels carry FDA pharmacogenomic guidance.

By End User: Research Institutes Lead Population Genomics

Hospitals and clinics generated 42.41% of 2025 revenue by embedding genetic services into integrated care pathways. Diagnostic laboratories face squeezed margins as payers negotiate bundled pricing and hospitals repatriate testing. Research and academic institutes, however, will post a 12.21% CAGR thanks to population genomics projects such as the U.S. All of Us, which enrolled 500,000 participants by 2025.

Hospital systems like Mayo Clinic embed pharmacogenomics into e-prescribing, automatically flagging gene-drug interactions for prescriptions such as warfarin. Research campuses, led by the Broad Institute, sequenced 100,000 genomes in 2025 alone, fueling demand for high-throughput services. Laboratories lacking capital for IVDR compliance are expected to consolidate, redirecting market share to better-funded research centers and large hospital groups.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

North America retained 43.13% of 2025 revenue in the genetic testing market and will rise at 9.8% CAGR through 2031. Medicare and major insurers reimburse hereditary cancer, NIPT, and liquid biopsy assays, while employers broaden genomic wellness benefits. The FDA cleared 12 genetic tests in 2024, cutting approval cycles from 18 to 9 months under its Precision Medicine Initiative. Canada reimburses DPYD genotyping in Ontario and British Columbia, whereas Mexico remains largely self-pay, restricting access to urban private facilities.

Asia-Pacific is forecast to log a 12.63% CAGR, underpinned by China’s national sequencing infrastructure and India’s expanding diagnostics network. BGI runs the world’s largest sequencing hub, processing over 1 million samples monthly and launching a USD 100 genome service in 2025. Japan reimburses comprehensive genomic profiling for advanced cancer; India’s leading chains offer NIPT at USD 300, one-third U.S. prices. South Korea added BRCA testing in 2024, and Australia reimburses pharmacogenomics for thiopurine drugs at AUD 150 (USD 100).

Europe reshapes the laboratory landscape. Germany reimburses hereditary cancer panels at EUR 1,500 (USD 1,650); the U.K. NHS sequenced 100,000 cancer genomes with 30% actionable findings. France invested EUR 670 million (USD 737 million) in its Genomic Medicine Plan. Middle East and Africa will grow at an 11% CAGR, led by the UAE’s plan to sequence 1 million Emirati genomes by 2030. South America advances at a 10.5% CAGR, with Brazil’s Fleury and Dasa introducing hereditary panels at BRL 3,000 (USD 600).

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The genetic testing market remains moderately fragmented; the top five firms command roughly 40% of global revenue. Illumina dominates sequencing instruments with over 70% installed NGS base, although price pressure emerges from BGI and Pacific Biosciences. LabCorp’s 2024 purchase of Invitae created an end-to-end testing, counseling, and data analytics platform. Guardant Health’s liquid biopsy delivers seven-day turnaround, appealing to oncologists needing rapid therapy decisions.

Oxford Nanopore’s portable sequencers open point-of-care niches, exemplified by Médecins Sans Frontières’ deployment for tuberculosis drug resistance profiling. FDA Breakthrough Device designations favored incumbents; six of eight 2024 designations went to major players such as Roche and Exact Sciences. Robust patent portfolios like Illumina’s 1,000-plus sequencing claims raise barriers for entrants. Upcoming IVDR enforcement in Europe is expected to spur acquisitions of smaller labs unable to afford compliance upgrades.

Genetic Testing Industry Leaders

Illumina Inc.

F Hoffmann-La Roche AG

Thermo Fisher Scientific Inc

QIAGEN

Myriad Genetics

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Zydus Lifesciences and Myriad Genetics agreed to introduce MyRisk hereditary cancer and related assays across India.

- October 2025: Gene Solutions partnered with AMPATH to open an advanced genomics lab in Hyderabad, expanding NGS access.

- September 2025: Mass General Brigham launched a polygenic cardiovascular risk panel developed with Broad Clinical Labs.

- July 2025: Bupa debuted Medication Check DNA testing, finding 99% of participants carried variants affecting common drugs.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the genetic testing market as all clinical and direct-to-consumer tests that analyze human DNA or chromosomes to detect, confirm, or predict disease-associated variants, delivered through kits, instruments, and interpretation services across healthcare settings and at-home channels.

Scope exclusion: animal genetics, toxicology assays, and pure research-only sequencing reagents are not covered.

Segmentation Overview

- By Product & Service

- Consumables and Reagents

- Equipments and Instruments

- Software and Services

- By Test Type

- Diagnostic

- Prenatal & Newborn

- Predictive & Presymptomatic

- Carrier

- Pharmacogenomic

- By Technology

- Next-Generation Sequencing (NGS)

- Polymerase Chain Reaction (PCR)

- Microarray

- Cytogenetic / FISH

- Other Technologies

- By Application

- Oncology

- Genetic Disease Diagnosis

- Reproductive Health

- Ancestry & DTC Wellness

- Others

- By End User

- Hospitals & Clinics

- Diagnostic Laboratories

- Research & Academic Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed laboratory directors, genetic counselors, payor policy specialists, and test kit distributors across North America, Europe, and Asia Pacific. These discussions clarified real-world average selling prices, sample-throughput constraints, and the timing of guideline updates, enabling us to true up assumptions drawn from secondary material.

Desk Research

We started with public datasets from bodies such as the WHO Human Genomics Program, the U.S. National Human Genome Research Institute, Eurostat's health statistics, and Japan's MHLW test reimbursement files, which outline procedure volumes and national fee schedules. Trade association portals, such as the American Clinical Laboratory Association and Asia Pacific Society of Human Genetics, helped us map lab capacity and regulatory milestones. Company 10-Ks, investor decks, and peer-reviewed journals provided pricing shifts and technology adoption cues. Select proprietary feeds from D&B Hoovers and Dow Jones Factiva supplied revenue splits and M&A trails. The sources cited illustrate our desk work and are not exhaustive; many additional references aided data checks and context building.

Market-Sizing & Forecasting

A top-down model reconstructs global spend from national test reimbursement outlays, private pay volumes, and average consumer kit prices, which are then cross-checked with selective bottom-up estimates drawn from major supplier revenues and sampled hospital purchase data. Key variables include newborn screening rates, oncology companion-diagnostic penetration, declining whole-genome sequencing cost curves, direct-to-consumer kit shipments, and country-specific payer coverage rules. Multivariate regression links these indicators to spending trajectories, after which scenario analysis adjusts for regulatory or pricing shocks. Data gaps in supplier roll-ups are bridged using weighted regional proxies vetted through expert calls.

Data Validation & Update Cycle

Outputs pass a three-layer analyst review: variance checks against independent health-expenditure series, anomaly flags routed back to interviewees, and supervisory sign-off. Reports refresh each year, and material events, such as abrupt reimbursement cuts, trigger interim model updates before client delivery.

Why Mordor's Genetic Testing Baseline Earns Trust

Published estimates often diverge because firms pick different inclusion rules, pricing bases, and refresh cadences. Decision-makers therefore meet a wide spread of numbers when comparing reports.

Key gap drivers for this market include whether non-clinical ancestry kits are counted, how oncology panel ASP erosion is modeled, and if currency conversions lock at prior-year averages. Mordor applies a consistent DNA-based test scope, updates exchange rates at every refresh, and folds real-time ASP feedback from labs, yielding a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 21.79 B | Mordor Intelligence | - |

| USD 37.32 B | Global Consultancy A | Includes veterinary genetics and assumes flat ASPs |

| USD 17.21 B | Industry Publication B | Excludes direct-to-consumer kits; uses 2023 exchange rates |

| USD 14.25 B | Regional Consultancy C | Models test uptake solely from oncology demand; omits newborn screening |

The comparison shows how wider or narrower scopes, legacy currency locks, and single-segment focus inflate or deflate totals. By grounding estimates in clearly stated definitions, live pricing inputs, and annually refreshed variables, Mordor Intelligence offers a dependable starting point for strategic planning.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large was the genetic testing market in 2026?

The genetic testing market size reached USD 28.56 billion in 2026 and is projected to rise sharply through 2031.

What CAGR is expected through 2031?

The market is set to expand at a 10.21% CAGR, supported by payer coverage, falling sequencing costs, and AI-driven analysis.

Which technology dominates current revenue?

Next-generation sequencing led with 46.13% of 2025 revenue and continues to outpace other methods with a 12.67% CAGR.

Why is oncology the fastest-growing application?

Liquid biopsy approvals and minimal residual disease monitoring fuel a 13.88% CAGR, overtaking traditional genetic disease diagnostics.

Which region is forecast to grow the fastest?

Asia-Pacific is poised for a 12.63% CAGR, propelled by large-scale initiatives in China and expanded lab networks in India.