Market Overview

| Study Period | 2019 - 2030 |

|---|---|

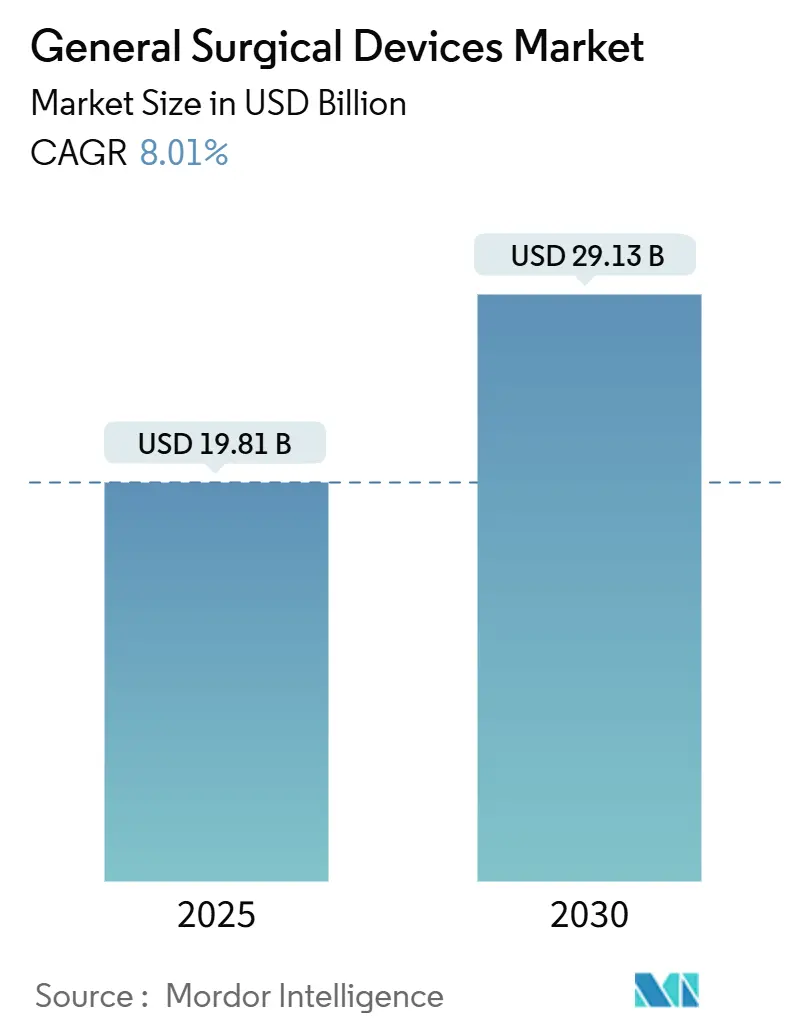

| Market Size (2025) | USD 19.81 Billion |

| Market Size (2030) | USD 29.13 Billion |

| Growth Rate (2025 - 2030) | 8.01% CAGR |

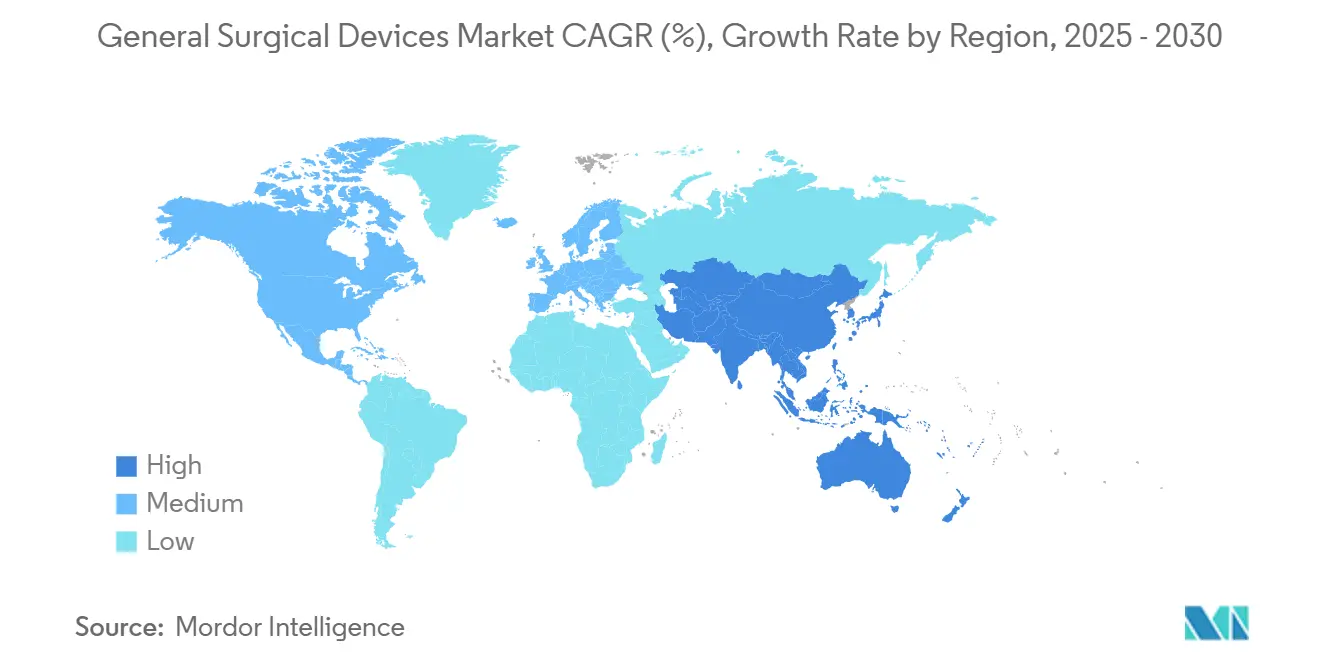

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

General Surgical Devices Market Analysis by Mordor Intelligence

The general surgical devices market size is estimated at USD 19.81 billion in 2025, and is expected to reach USD 29.13 billion by 2030, at a CAGR of 8.01% during the forecast period (2025-2030). Momentum comes from rising surgical volumes, accelerated adoption of minimally invasive techniques, and continuous product innovation aimed at shortening recovery times and lowering complication rates. North America leads the general surgical devices market thanks to advanced infrastructure and favorable reimbursement, while Asia-Pacific is advancing fastest as governments scale hospital capacity and private operators add ambulatory sites. Disposable supplies retain dominance because infection-control rules favor single-use tools, yet rapid gains in robotic platforms illustrate the industry’s pivot toward precision. Competitive intensity is increasing as large conglomerates defend their share against focused entrants bringing niche technologies to market.

Key Report Takeaways

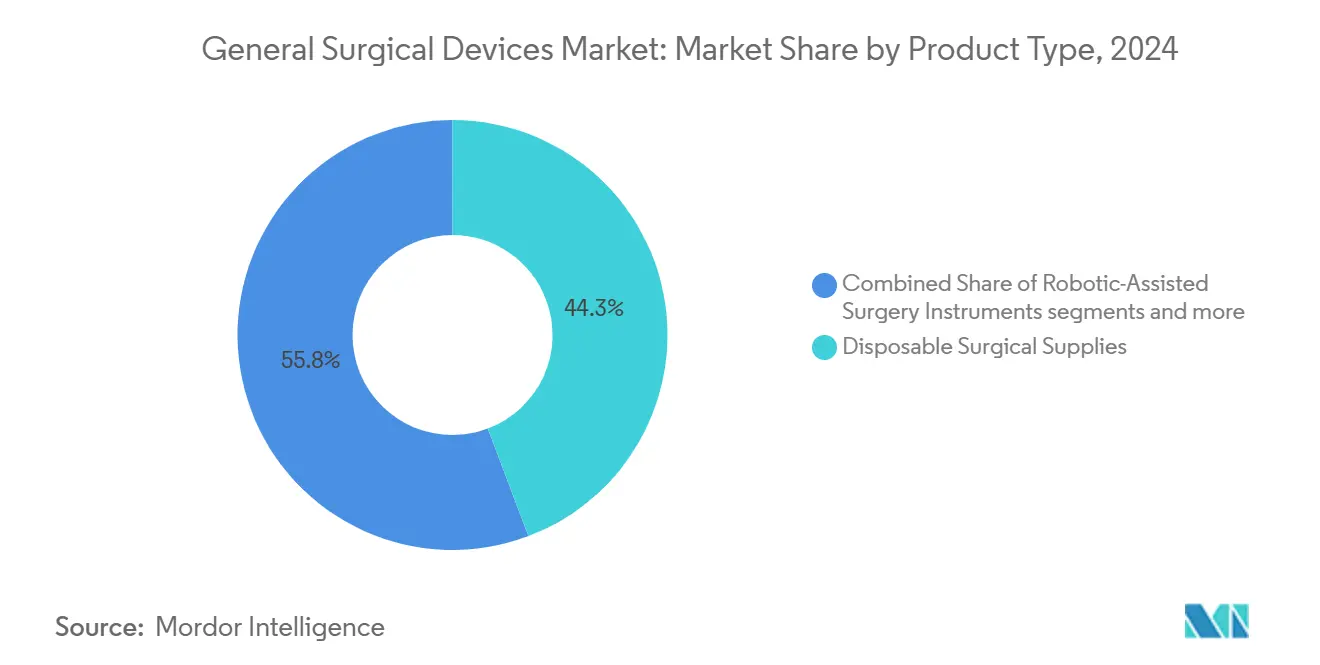

- By product type, disposable surgical supplies held 44.25% of the general surgical devices market share in 2024; robotic-assisted surgery instruments are forecast to grow at an 11.12% CAGR through 2030.

- By application, orthopedic accounted for a 19.35% slice of the general surgical devices market size in 2024, while cardiology is poised to register a 10.23% CAGR between 2025 and 2030.

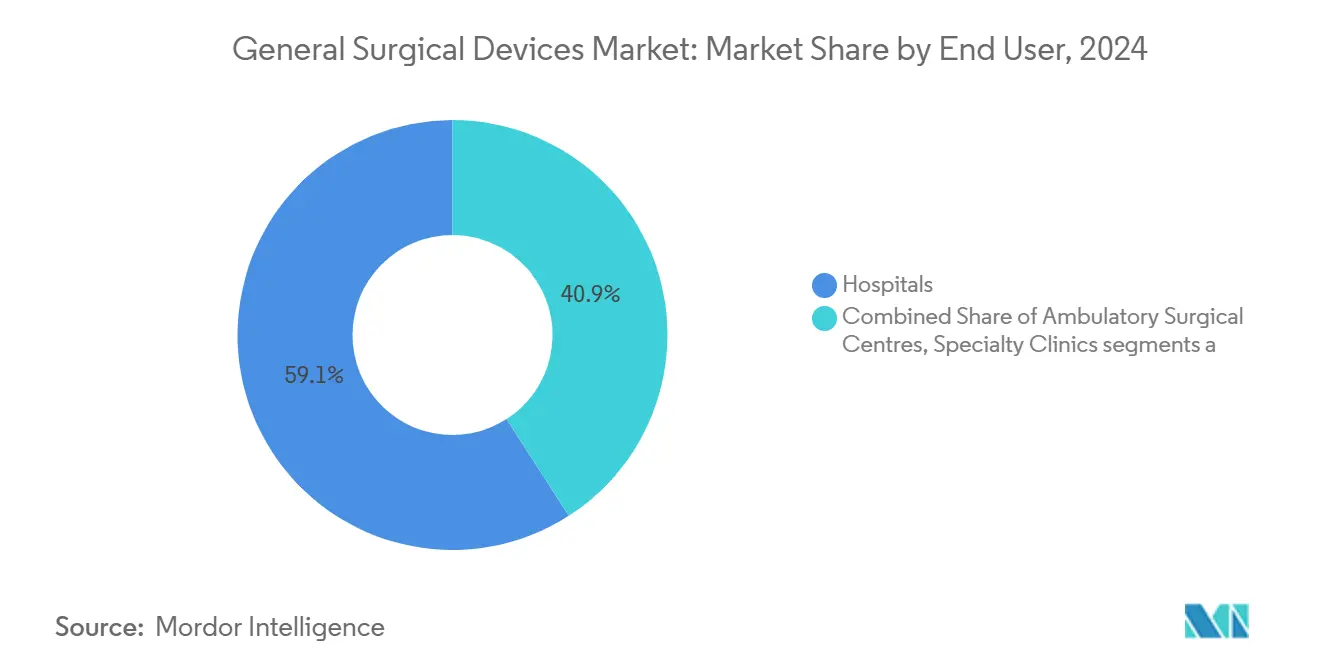

- By end user, hospitals commanded 59.05% revenue in 2024; ambulatory surgical centers are advancing at a 9.34% CAGR through 2030.

- By geography, North America captured 37.97% of the general surgical devices market share in 2024; Asia-Pacific is growing at a 10.77% CAGR over the forecast horizon.

Global General Surgical Devices Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global surgical procedure volume | Adoption of minimally invasive surgery | Worldwide, highest in North America & Europe | Short term (≤ 2 years) |

| Adoption of minimally invasive surgery | +1.8% | Global, early uptake in developed markets | Medium term (2-4 years) |

| Technological advances in energy-based tools | +1.2% | Concentrated in North America | Medium term (2-4 years) |

| Expanding healthcare infrastructure & spending | +1.5% | Asia-Pacific, Latin America, Middle East | Long term (≥ 4 years) |

| Surge in ambulatory surgical centers | +1.7% | North America, expanding to Europe & Asia-Pacific | Short term (≤ 2 years) |

| Increasing preference for single-use and sterile devices | +1.3% | Global, with highest impact in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Minimally invasive surgery adoption accelerates across specialties

Robotic navigation systems, specialized access ports, and refined imaging together help surgeons reduce tissue trauma, which in turn lowers length of stay by 2-3 days and halves the time patients need before returning to work. Orthopedics illustrates the shift as 68% of eligible procedures in 2024 already used MIS, and Stryker’s Mako SmartRobotics platform cut intra-operative force by 43%. Cardiovascular, gynecology, and neurosurgery specialties show comparable trajectories as device makers add single-port or catheter-based solutions that fit existing workflows. The economic upside strengthens the case: lowering readmissions and freeing beds help hospitals meet value-based payment targets, which further stimulates procurement of MIS-compatible systems. Collectively, these factors will keep the general surgical devices market on a robust expansion path as health systems continue replacing open approaches with keyhole alternatives.

AI Integration Transforms Surgical Decision-Making and Outcomes

Artificial intelligence now supports pre-operative planning, intra-operative guidance, and post-operative monitoring. FastGlioma, a University of Michigan–UCSF model, identified residual brain tumor tissue with 92% accuracy and reduced miss rates from 25% to 3.8%.[1]Source: ScienceDaily Staff, “In 10 Seconds, an AI Model Detects Cancerous Brain Tumor Often Missed During Surgery,” sciencedaily.com Predictive engines such as MySurgeryRisk outperform conventional assessments, cutting complication incidence by up to 30%. Hospitals using these tools see fewer ICU days, and payers note cost avoidance; thus, AI is moving from pilot projects into routine procurement line-items. As algorithms migrate onto consoles and endoscopes, vendors differentiate through data pipelines rather than purely mechanical features yet another evolution that underpins sustained demand in the general surgical devices market.

Energy-based Devices Evolve Beyond Vessel Sealing

Hybrid ultrasonic-radiofrequency handpieces now sense tissue impedance in real time and auto-tune energy delivery, which minimizes thermal spread near nerves or ducts. The U.S. FDA’s decision to reclassify ultrasound cyclodestructive devices to Class II underscores regulatory confidence in safety profiles.[2]Source: U.S. Food and Drug Administration, “Ophthalmic Devices; Reclassification of Ultrasound Cyclodestructive Device,” federalregister.gov Broader acceptance encourages surgeons to adopt these intelligent tools for delicate thyroid, prostate, and colorectal procedures, enlarging addressable volumes inside the general surgical devices market.

Ambulatory Surgical Centers Reshape Care Delivery Models

The rapid expansion of ambulatory surgical centers (ASCs) is fundamentally altering the surgical care delivery landscape. The segment growth is driven by cost efficiency, ASCs can perform procedures at 35-50% lower cost compared to hospital outpatient departments and enhanced patient experience, with shorter wait times and reduced infection risks. The ASC boom is catalyzing innovation in surgical devices, with manufacturers developing products specifically tailored to the ambulatory setting. These include more compact and portable equipment, single-use instruments that eliminate reprocessing requirements, and integrated surgical systems that reduce setup time and staff requirements.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance costs | -1.6% | Strongest in emerging economies | Medium term (2-4 years) |

| Stringent regulatory approval pathways | -1.2% | North America & Europe | Medium term (2-4 years) |

| Shortage of trained surgeons | -1.0% | Emerging markets in Asia-Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Supply-chain disruptions | -1.4% | Global, with higher impact in regions dependent on imports | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Maintenance Costs

Advanced robotics and imaging suites require investments that can exceed USD 2 million per operating room, a hurdle for facilities in middle-income countries where paybacks stretch beyond standard budgeting cycles. Service contracts, software upgrades, and disposables compound total cost of ownership, dampening uptake despite clear clinical benefits. Consequently, value-engineered systems and pay-per-use models are gaining traction as vendors attempt to keep the general surgical devices market accessible across income tiers.

Regulatory Harmonization Gains Momentum Globally

The FDA's amendment of the Quality System (QS) regulation to align with international standards for device quality management systems marks a significant step toward global regulatory harmonization FDA. This shift, effective February 2026, aims to reduce redundant compliance activities for manufacturers operating in multiple markets while maintaining rigorous safety standards. The move is particularly significant for innovative surgical device manufacturers, who often face delays in global commercialization due to divergent regulatory requirements.

Segment Analysis

By Product Type: Disposables Hold Sway While Robotics Redefines Precision

Disposable surgical supplies generated the largest revenue share in 2024 as infection-control protocols favored single-use drapes, trocars, and blades. Their 44.25% command of the general surgical devices market size underscores hospital preference for standardization when tracking nosocomial infection metrics. Segment growth nevertheless converges toward mid-single-digit rates because sustainability efforts encourage selective reusability in low-risk cases, a nuance reshaping procurement guidelines without dislodging disposables from top position.

Robotic-assisted instruments, though smaller in absolute dollars, are set to outpace every other category through 2030, riding an 11.12% CAGR. Systems tailored for hip revision, partial knee, and soft-tissue work broaden indications and shorten learning curves. As throughput improvements offset capital outlays, administrators increasingly view robotics as productivity tools rather than prestige purchases. This dynamic points to sustained momentum for the general surgical devices market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Orthopedics Leads, Cardiology Accelerates

Orthopedic interventions accounted for 19.35% of the general surgical devices market share in 2024, anchored by high procedure counts for knee, hip, and spine. The ROSA Shoulder System’s first-in-human robotic shoulder replacement at Mayo Clinic showcases how innovation penetrates new joints.[3]Source: Zimmer Biomet Holdings Inc., “Zimmer Biomet Announces Successful Completion of World’s First Robotic-Assisted Shoulder Replacement Surgery with ROSA Shoulder System,” investor.zimmerbiomet.com Such milestones strengthen surgeon confidence and spur procurement even in community hospitals, ensuring orthopedics keeps its pole position during the forecast period.

Cardiology is the fastest climber, set to post a 10.23% CAGR as pulsed-field ablation, drug-coated balloons, and real-time mapping catheters enter mainstream use. Boston Scientific’s U.S. launch of the FARAPULSE System and Medtronic’s FDA-cleared Sphere-9 catheter show incumbents racing to outfit electrophysiology labs with versatile platforms. Expansion of structural heart programs beyond academic centers further enlarges the general surgical devices market size for cardiovascular tools.

By End-user: Hospitals Dominate, ASCs Gain Momentum

Hospitals generated 59.05% of global revenue in 2024, reflecting their breadth of specialties and ability to handle high-acuity cases. Administrative leaders view technology suites as competitive assets that attract referrals; therefore capital allocation remains steady even amid cost-containment debates. Yet reimbursement models increasingly tie payments to outcomes, prompting scrutiny of utilization rates and pushing vendors to offer consumption-based financial packages for the general surgical devices market.

Ambulatory surgical centers (ASCs) occupy the high-growth niche, tracking a 9.34% CAGR as procedures migrate to lower-cost settings. Roughly 6,100 U.S. ASCs treated 3.3 million Medicare beneficiaries in 2024, and procedure counts per beneficiary rose 2.8%.[4]Source: Center for Medicare & Medicaid Services via MedPAC, “Ambulatory Surgical Center Services Databook,” medpac.gov Vendors respond with compact consoles, single-use camera stacks, and portable energy units designed for limited floor space. These purpose-built products swell the overall opportunity pool inside the general surgical devices market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

North America held 37.97% of 2024 revenue, buoyed by high procedure counts, rapid uptake of robotics, and supportive reimbursement. The U.S. benefits from a dense innovation ecosystem, but market saturation in staples and electrosurgery means growth increasingly stems from software-enhanced systems and AI modules. Canada’s push toward value-based care encourages hospitals to track device performance closely, a trend likely to ripple into procurement across the general surgical devices market.

Europe ranks second and maintains steady expansion despite rigorous conformity assessments under the Medical Device Regulation. Germany, the United Kingdom, and France lead adoption, particularly for joint arthroplasty robots and advanced imaging. Southern and Eastern European states are upgrading facilities, creating fresh avenues for mid-priced solutions. Currency fluctuations and budget constraints remain hurdles, but harmonized standards improve cross-border commercialization inside the general surgical devices market.

Asia-Pacific represents the fastest-growing region with a 10.77% CAGR. China invests heavily in county-level hospitals while fostering domestic robotic challengers that aim to lower acquisition costs. Japan’s aging demographic catalyzes spine and cardiac device demand, and India’s private chains expand operating theatre capacity to capture elective orthopedic work. This momentum elevates the region’s contribution to overall general surgical devices market size and heightens competitive jockeying among multinationals and local entrants alike.

Note: Segment shares of all individual segments available upon report purchase

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The marketplace remains moderately concentrated. Medtronic, Johnson & Johnson, and Stryker anchor portfolios that span imaging, stapling, energy, and robotics. Strategic acquisitions remain a primary lever: Stryker bought NICO Corporation, Vertos Medical, and Inari Medical in 2024 to diversify beyond orthopedics. Medtronic’s purchase of Fortimedix Surgical added articulating laparoscopic instruments that complement its Hugo robotic platform. These moves block emergent rivals from capturing lucrative sub-segments and reinforce incumbents’ breadth inside the general surgical devices market.

Specialized entrants emphasize distinctive value propositions. Intuitive Surgical tailors its da Vinci ecosystem for outpatient environments, while Sony prototypes a microsurgery assistant robot aimed at neurovascular tasks. Such focused innovation pressures legacy vendors to iterate faster lest they cede share.

White-space opportunities persist in interventional pulmonology, bariatric endoscopy, and low-weight robotic arms optimized for ASCs. Companies that align novel platforms with pay-per-use financing could disrupt procurement habits, adding competitive dynamism to the general surgical devices market. Intellectual-property portfolios, data analytics, and surgeon-training ecosystems will likely become decisive moats as hardware differentials narrow.

General Surgical Devices Industry Leaders

-

Boston Scientific Corporation

-

B. Braun SE

-

Medtronic PLC

-

Johnson & Johnson (Ethicon, DePuy & Robotics)

-

Stryker Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Johnson & Johnson MedTech completed initial cases with the OTTAVA Robotic Surgical System, marking its first clinical use.

- January 2025: JUNE MEDICAL and Aspen Surgical agreed to distribute the Galaxy II retractor across U.S. hospitals.

- October 2024: Johnson & Johnson MedTech introduced the ECHELON ENDOPATH Staple Line Reinforcement for bariatric, thoracic, and general surgery.

- May 2024: Stereotaxis purchased APT to secure catheter designs tailored to robotics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the general surgical devices market as all handheld or powered instruments, robotic arms, energy-based tools, and single-use supplies that enable physicians to access, cut, cauterize, or close human tissue across open, minimally invasive, and robot-assisted procedures performed in operating rooms and ambulatory surgical centers.

Scope Exclusion: Veterinary surgical kits and large capital imaging systems fall outside this assessment.

Segmentation Overview

- By Product Type

- Minimally Invasive Surgery Instruments

- Robotic-Assisted Surgery Instruments

- Energy-Based Surgery Instruments (RF, Ultrasonic)

- Open Surgery Instruments

- Disposable Surgical Supplies

- Others

- By Application

- Orthopaedic

- Cardiology

- Gynecology nd Urology

- Neurology

- Gastrointestinal

- Others

- By End User

- Hospitals

- Ambulatory Surgical Centres

- Specialty Clinics

- Academic and Research Institutes

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed practicing surgeons, perioperative nurses, supply-chain directors, and regional distributors in North America, Europe, Asia-Pacific, Latin America, and the Middle East. These conversations confirmed real-world average selling prices, the shift toward disposable kits, and early adoption rates of robotic consoles, allowing us to recalibrate secondary inputs and assumptions.

Desk Research

We began by mapping public procedure volumes and spend patterns from tier-1 sources such as the World Health Organization, OECD Health Statistics, the American Hospital Association, and Eurostat; these establish how often major surgeries occur and how device demand scales. Our team then extracted import-export codes for instruments under HS 9018 and 9019 from UN Comtrade, which helps us benchmark global trade flows against production figures.

Patent analytics from Questel, 510(k) clearance files on the FDA MAUDE database, and peer-reviewed journals on laparoscopic and robotic adoption trends supply technology diffusion cues. Company 10-Ks, investor decks, and news feeds accessed through Dow Jones Factiva round out pricing and competitive signals. This list is illustrative, and many other open and paid repositories were tapped for validation and clarification.

Market-Sizing & Forecasting

A top-down construct converts national surgical admissions into addressable device demand through procedure-specific instrument counts, which are then multiplied by blended ASPs and adjusted for reuse cycles. Select bottom-up cross-checks, supplier revenue roll-ups, and sampled ASC purchasing data help us reconcile any variance. Key variables include elective versus emergency surgery mix, installed robotic theater base, average instrument turnover, trade tariff movements, and reimbursement updates.

For forecasting, we apply multivariate regression that links procedure growth, demographic aging, ASC capacity expansion, and ASP inflation, before scenario analysis injects upside or downside around technology uptake. Where bottom-up estimates lack clarity, gap factors derived from primary research bridge the difference.

Data Validation & Update Cycle

Outputs move through anomaly scans, peer review, and senior sign-off. We refresh the model each year, and we issue interim revisions when regulatory approvals, supply shocks, or currency swings create material deviation. Before release, an analyst re-runs the full workbook so clients receive the latest synced view.

Why Our General Surgical Devices Baseline Earns Unmatched Trust

Published figures often differ because publishers choose dissimilar product mixes, pricing ladders, geographic coverage, and update cadences. We acknowledge such spread upfront and show where numbers diverge.

Key gap drivers include whether robotic systems and energy platforms are counted, the breadth of countries modeled, hedged versus spot currency treatment, and the frequency with which fresh hospital procurement data are folded back into the model.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 19.81 B (2025) | Mordor Intelligence | - |

| USD 19.90 B (2025) | Global Consultancy A | Narrower scope on open surgery tools, constant-2023 dollar conversion |

| USD 16.65 B (2025) | Industry Journal B | Excludes robotic platforms, covers only 12 economies, conservative ASP basis |

These comparisons show that while others provide useful snapshots, Mordor's disciplined scope selection, multi-source triangulation, and annual refresh cadence deliver a balanced baseline buyers can rely on.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How is artificial intelligence changing surgical device usage in operating rooms?

AI now guides intra-operative decisions such as tumor margin detection and predicts post-operative complications, helping surgeons improve precision while hospitals cut re-intervention rates.

Why are ambulatory surgical centers important to device manufacturers?

ASCs seek compact, single-use, and quick-setup instruments, so suppliers that redesign robots and energy tools for smaller footprints gain preferred-vendor status in this high-volume care setting.

What role do “intelligent” energy devices play in delicate procedures?

These instruments adjust power delivery in real time based on tissue feedback, minimizing thermal injury near nerves or ducts and expanding minimally invasive options for endocrine and urologic surgeries.

How are leading companies strengthening supply-chain resilience after recent disruptions?

Strategies include dual-sourcing critical electronics, nearshoring assembly lines, and holding larger safety stocks for disposable kits to ensure uninterrupted deliveries to hospitals.

Which regulatory shifts could speed device launches globally?

Alignment of U.S. quality-system rules with ISO standards and expanded FDA fast-track programs are trimming redundant audits and shortening time-to-market for novel surgical technologies.

Page last updated on: