Market Overview

| Study Period | 2021 - 2031 |

|---|---|

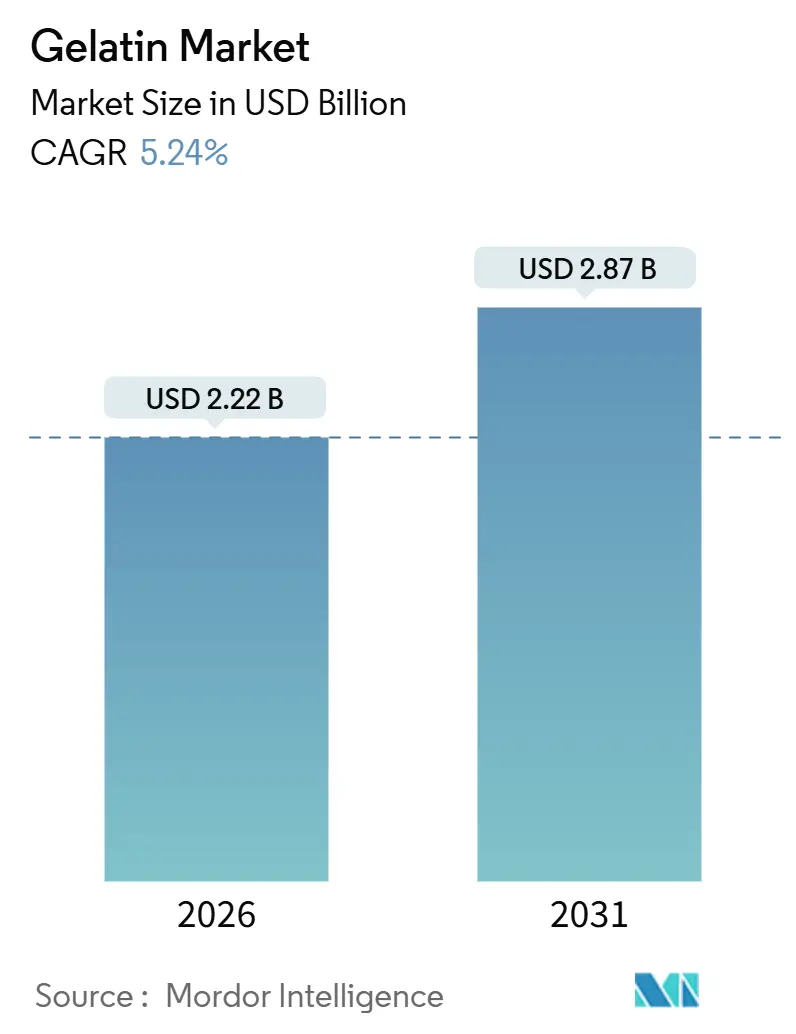

| Market Size (2026) | USD 2.22 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 5.24% CAGR |

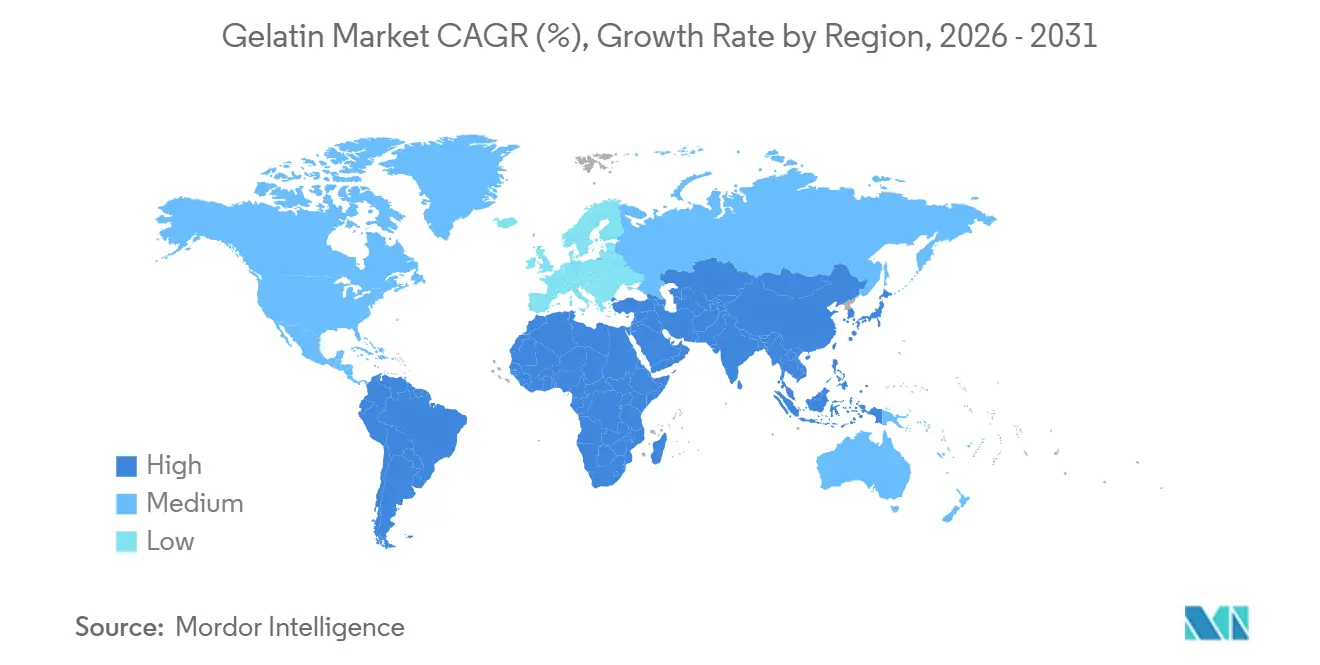

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Gelatin Market Analysis by Mordor Intelligence

The gelatin market, valued at USD 2.22 billion in 2026 and projected to reach USD 2.87 billion by 2031 at a CAGR of 5.24%, is driven by its functional relevance, broad applicability across industries, and alignment with health, wellness, and clean-label trends. The market's growth is further supported by the increasing focus on preventive healthcare and functional nutrition. Gelatin plays a pivotal role in capsules, gummies, and protein-enriched products due to its proven bioavailability, versatility, and strong consumer acceptance. Furthermore, its widespread use in food, pharmaceuticals, and cosmetics highlights its adaptability and expanding demand across diverse applications. Ongoing advancements in extraction, purification, and customization technologies have significantly enhanced consistency, safety, and application-specific performance, enabling gelatin to meet stringent quality standards and effectively cater to evolving consumer needs and preferences.

Key Report Takeaways

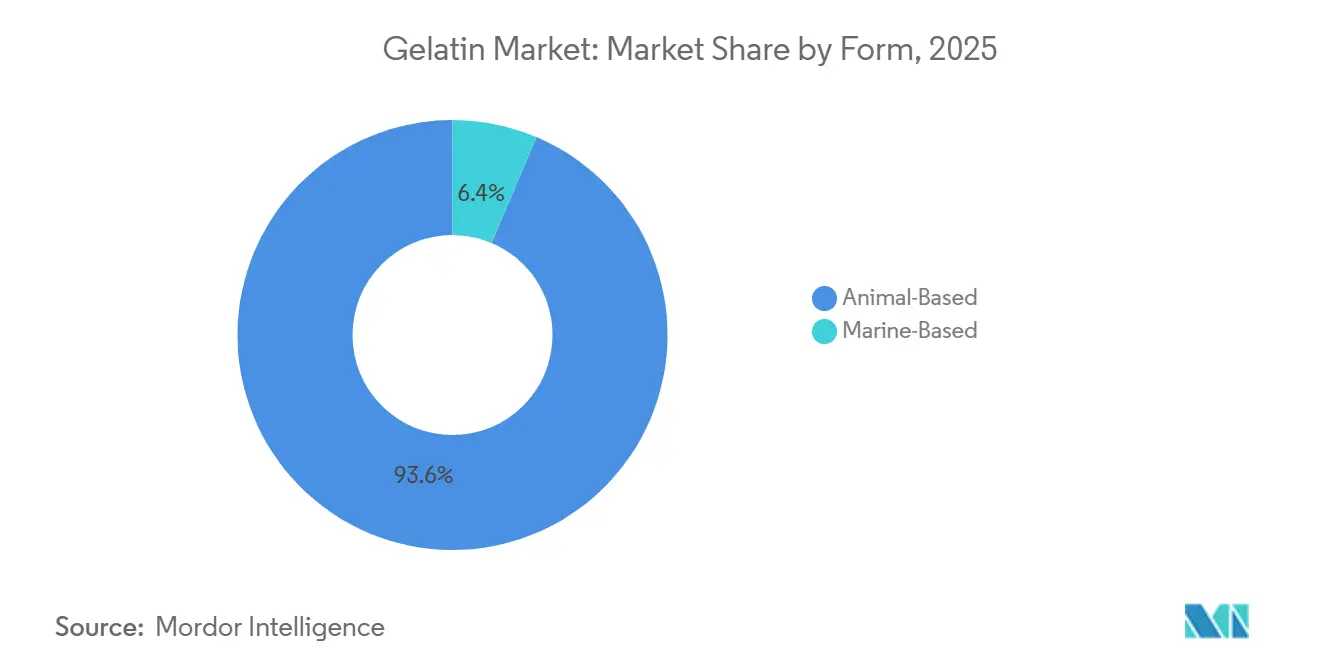

- By form, animal-based gelatin accounted for 93.61% of volume in 2025, whereas marine variants are projected to climb at a 7.54% CAGR to 2031.

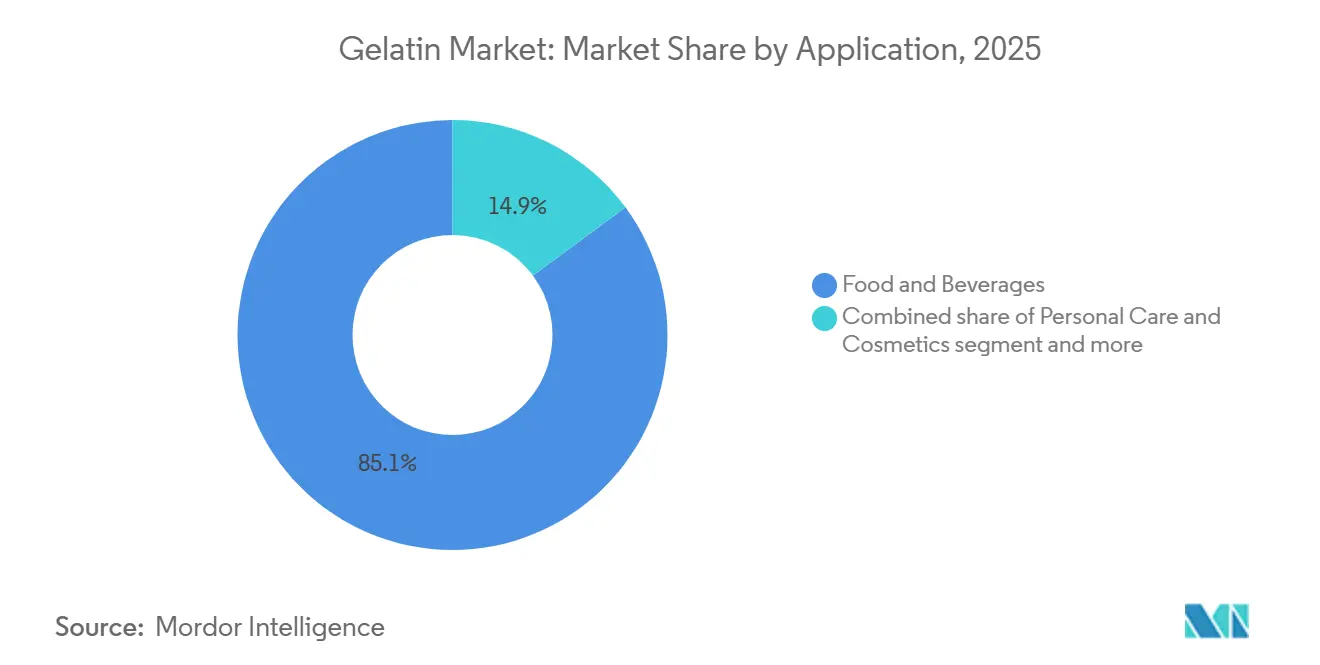

- By application, the food and beverage segment held 85.12% of the gelatin market share in 2025; personal care and cosmetics are expanding at a 6.35% CAGR through 2031.

- By geography, Asia-Pacific commanded 34.66% of revenue in 2025 and is set to grow at a 5.67% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Gelatin Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for functional and nutraceutical products | +1.8% | Global, with concentration in North America and Asia-Pacific | Medium term (2-4 years) |

| Technological advancements in extraction and processing | +1.2% | Europe and North America, spillover to Asia-Pacific | Long term (≥4 years) |

| Clean-label and natural ingredient preference | +1.0% | North America and Europe | Short term (≤2 years) |

| Rising use of gelatin in pharmaceutical capsules | +1.5% | Asia-Pacific core, expansion in Middle East and Africa | Medium term (2-4 years) |

| Growth of convenience and ready-to-eat food products | +0.9% | Asia-Pacific and South America | Short term (≤2 years) |

| Customization of gelatin grades for end-use applications | +0.7% | Global, led by Europe and North America | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing demand for functional and nutraceutical products

The growing demand for functional and nutraceutical products is a key driver of the gelatin market. Gelatin is increasingly evolving from a conventional food texturizer to a value-added functional ingredient, aligning with trends in preventive health and wellness. Its collagen-derived amino acid profile, rich in glycine, proline, and hydroxyproline, offers widely recognized benefits for joint health, bone strength, muscle recovery, skin elasticity, and gut health, making it highly suitable for nutraceutical formulations. This has led to its increased use in dietary supplements, gummies, capsules, powders, and ready-to-consume functional formats, where gelatin functions both as an active protein source and a delivery system. In nutraceutical capsules and softgels, gelatin's excellent film-forming properties, rapid dissolution, and high bioavailability ensure efficient nutrient absorption, reinforcing its preference over alternative encapsulation materials. Furthermore, gelatin's versatility in formulation, compatibility with diverse active ingredients, and ability to meet clean-label and sustainability demands strengthen its position as a preferred choice in the nutraceutical industry.

Technological advancements in extraction and processing

Technological advancements in extraction and processing are a significant driver of the gelatin market. Continuous innovation has improved yield efficiency, functional performance, consistency, and the application versatility of gelatin across various end-use industries. Enhancements in controlled acid and alkaline pretreatment methods, enzymatic hydrolysis, and precision filtration have enabled manufacturers to produce gelatin with more uniform bloom strength, viscosity, clarity, and thermal stability, meeting the increasingly stringent requirements of food, pharmaceutical, and biomedical applications. Advanced processing technologies also provide tighter control over molecular weight distribution, facilitating the development of application-specific gelatin grades. From a production perspective, automation, real-time quality monitoring, and improved purification systems have reduced contamination risks while enhancing traceability and batch-to-batch consistency—critical factors for pharmaceutical and medical-grade gelatin. These technological advancements have also enabled the efficient utilization of diverse raw materials, supporting product differentiation and ensuring regulatory compliance across regions.

Clean-label and natural ingredient preference

The preference for clean-label and natural ingredients is a significant driver of the gelatin market. Manufacturers in the food, nutraceutical, and personal care industries are increasingly focusing on ingredients that are recognizable, minimally processed, and perceived as natural by consumers. Gelatin benefits from this trend as it is derived from natural collagen sources and is widely regarded as a familiar, label-friendly alternative to synthetic stabilizers, thickeners, and film-forming agents. Clean-label positioning has become a key factor in product differentiation, with brands reformulating to eliminate artificial additives while maintaining texture, stability, and sensory quality, areas where gelatin provides inherent functional benefits. In the personal care and cosmetics sector, this trend is particularly evident. Consumers increasingly associate natural ingredients with safety, skin compatibility, and long-term wellness, driving the use of gelatin in skincare, haircare, masks, and beauty supplements. This behavior is supported by consumer data; for example, according to NSF International, 74% of consumers in 2024 considered organic ingredients important in personal care products, highlighting the rising demand for naturally derived components [1]Source: NSF International, "74% of Consumers Consider Organic Ingredients", nsf.org.

Rising use of gelatin in pharmaceutical capsules

The increasing use of gelatin in pharmaceutical capsules is a significant driver of the gelatin market, supported by its essential role in drug delivery systems. Gelatin is widely regarded as the preferred material for hard and soft capsules due to its excellent film-forming properties, mechanical strength, predictable dissolution, and high bioavailability. These characteristics are crucial for ensuring dosage accuracy and therapeutic effectiveness. Pharmaceutical manufacturers prioritize gelatin capsules because they enable efficient encapsulation of a broad range of active pharmaceutical ingredients (APIs). This demand is further bolstered by gelatin’s established regulatory acceptance, safety profile, and compatibility with automated capsule-filling technologies, which reduce formulation risks and expedite product commercialization. For example, according to the Office of Economic Complexity, China exported approximately USD 12.2 billion worth of pharmaceutical products in 2024, underscoring the scale of capsule production and export-driven pharmaceutical manufacturing [2]Source: Office of Economic Complexity [OEC], "Pharmaceutical products in China", oec.world. As capsule-based dosage forms remain dominant in oral drug delivery due to their convenience and patient preference, the growth of the global pharmaceutical supply chain continues to drive sustained, high-volume demand for gelatin.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Allergen and health safety risks | -0.6% | Global, acute in North America and Europe | Short term (≤2 years) |

| Supply chain vulnerability | -0.9% | Global, acute in Asia-Pacific and South America | Short term (≤2 years) |

| Competition from plant-based and synthetic alternatives | -1.3% | North America and Europe, emerging in Asia-Pacific | Medium term (2-4 years) |

| Limited functionality in certain applications | -0.5% | Global, with emphasis on technical food applications | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Allergen and health safety risks

Allergen and health safety risks remain a significant restraint for the gelatin market, driven by concerns related to source traceability, disease transmission, and allergenic potential. Despite advancements in processing standards and stringent regulatory controls that have substantially reduced these risks, legacy perceptions continue to impact acceptance in sensitive applications such as pharmaceuticals, infant nutrition, and medical products, where safety standards are particularly stringent. Additionally, marine-based gelatin may require fish-allergen labeling, creating challenges in formulation and packaging for food and nutraceutical manufacturers seeking to uphold allergen-free claims. These challenges highlight the pressing need for continuous innovation in processing technologies, the integration of advanced traceability systems, and enhanced industry collaboration to effectively address safety concerns, foster greater consumer confidence, and ensure compliance with increasingly rigorous regulatory frameworks and shifting market dynamics.

Supply Chain Vulnerability

Supply chain vulnerability poses a significant restraint in the gelatin market due to the industry's reliance on animal-derived raw materials and complex upstream processing networks. Gelatin production depends on a consistent supply of bovine hides, porcine skins, and fish by-products, making it highly susceptible to factors such as livestock disease outbreaks, fluctuations in slaughter rates, regulatory changes, and shifts in meat processing practices. Disruptions, including animal health crises or modifications in veterinary and food safety regulations, can abruptly limit raw material availability, directly impacting gelatin production, lead times, and overall market stability. Additionally, the geographic concentration of slaughterhouses and rendering facilities creates logistical dependencies, increasing exposure to transportation bottlenecks, cross-border trade restrictions, and regional supply chain inefficiencies. These vulnerabilities highlight the critical importance of adopting diversified sourcing strategies, improving supply chain transparency, and leveraging technological advancements to enhance resilience and ensure uninterrupted production.

Segment Analysis

By Form: Marine Variants Gain Despite Animal Dominance

Animal-based gelatin is projected to dominate with a 93.61% market share in 2025, driven by its functional advantages, established industrial reliance, regulatory familiarity, and mature supply chains. Animal-based gelatin offers superior gelling strength, thermo-reversibility, film-forming capability, emulsification, and controlled melt-in-mouth properties. These characteristics are challenging for plant-based or synthetic alternatives to replicate at scale. Such functional benefits are particularly critical in pharmaceutical applications, where precise dissolution rates, mechanical strength, and bioavailability are essential, positioning animal-based gelatin as the industry standard. Additionally, its widespread availability, cost-effectiveness, and adaptability across diverse applications further solidify its dominance in various end-use industries. The segment also benefits from its long-standing acceptance in food and beverage applications, where its unique textural and stabilizing properties are indispensable.

Marine-based gelatin, anticipated to grow at a 7.54% CAGR through 2031, is gaining traction due to its unique sourcing benefits, regulatory acceptance in sensitive markets, and increasing adoption in high-value applications. Although it currently holds a smaller market share compared to animal-based gelatin, the segment is supported by a growing focus on sustainability and by-product utilization. Marine gelatin capitalizes on waste streams from the seafood processing industry, aligning well with circular economy principles. Furthermore, its lower allergenicity, compatibility with dietary restrictions such as halal and kosher certifications, and potential for innovation in premium applications enhance its appeal in niche but expanding consumer segments. The rising demand for clean-label and eco-friendly products further strengthens the growth prospects of marine-based gelatin in the global market.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Food Dominance Masks Cosmetics Surge

Food and beverage applications are projected to account for 85.12% of gelatin consumption in 2025, underscoring gelatin's essential role in both mainstream and specialty food formulations. Its dominance in this segment is attributed to its multifunctional properties, including gelling, thickening, stabilizing, emulsifying, and foaming capabilities. These attributes are challenging to replicate without compromising product quality. In confectionery products such as gummies, jellies, marshmallows, and chewy candies, gelatin provides elasticity, chewiness, clarity, and a melt-in-the-mouth texture, which are critical to product identity and consumer satisfaction. Additionally, gelatin's compatibility with clean-label trends and its natural origin further enhance its appeal in the food and beverage industry.

The personal care and cosmetics segment is expected to grow at a CAGR of 6.35% through 2031. Gelatin is increasingly utilized in this sector for its film-forming, moisture-retention, texture-enhancing, and conditioning properties, making it suitable for skincare creams, face masks, hair care products, and nail treatments. Its collagen-derived amino acid profile supports claims related to skin elasticity, hydration, hair strength, and anti-aging benefits, aligning with the global trend toward functional beauty and beauty-from-within concepts. This growth is further supported by increasing consumer interest in premium and routine personal care products, particularly in developed markets. For example, according to the Office for National Statistics (UK), consumer spending on personal care in the United Kingdom reached approximately GBP 41.9 billion in 2024, highlighting the robust and sustained demand in a key mature market [3]Source: Office for National Statistics (UK), "Consumer spending on personal care in the United Kingdom", ons.gov.uk. Furthermore, the rising preference for sustainable and ethically sourced ingredients in cosmetics is driving innovation and expanding gelatin's applications in this segment.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

Geography Analysis

In 2025, Asia-Pacific accounted for 34.66% of gelatin revenue and is projected to grow at a CAGR of 5.67% through 2031, establishing itself as the most influential regional market. This dominance is attributed to the region's large-scale manufacturing capabilities, diverse applications, and export-oriented pharmaceutical ecosystem. China plays a pivotal role with its extensive production of hard and soft gelatin capsules, catering to both domestic and international pharmaceutical markets. This is supported by advanced technical expertise and standardized production processes. Additionally, India is emerging as a significant growth driver due to the rapid expansion of nutraceuticals, dietary supplements, and functional foods, where gelatin is extensively used in capsules, gummies, and protein-enriched formulations.

Europe is solidifying its position as a key gelatin market, driven by its robust pharmaceutical, biomedical, and premium food industries. The region exhibits high utilization of gelatin in capsules, medical devices, wound care, and specialty nutrition, supported by stringent quality standards that highlight gelatin's safety and performance. Europe also leads in the development of marine-based and specialty gelatin, addressing dietary, religious, and sustainability concerns. Furthermore, demand for gelatin in high-end confectionery, dairy desserts, and clean-label food formulations continues to grow. This combination of regulatory compliance, innovation-driven demand, and premium applications reinforces Europe's role as a high-value gelatin market.

North America, South America, and the Middle East and Africa (MEA) collectively contribute to gelatin market growth through application-specific demand in pharmaceutical capsules and functional foods. This growth is supported by ongoing product innovation and increasing consumer interest in protein and wellness solutions. South America benefits from its strong livestock industry, ensuring a steady supply of raw materials for gelatin production, which supports its use in food processing and pharmaceuticals. In the Middle East and Africa, gradual market expansion is driven by rising demand for Halal-compliant gelatin, pharmaceutical formulations, and packaged foods, particularly in Gulf countries and urban African markets.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The gelatin market is moderately concentrated, with a limited number of large, vertically integrated manufacturers dominating the landscape. These companies possess strong technological capabilities and extensive global distribution networks. Key players in the market include Darling Ingredients Inc., Gelita AG, Nitta Gelatin NA Inc., SAS Gelatines Weishardt, and Italgelatine SpA. Their competitive advantage stems from long-standing customer relationships across food, pharmaceutical, nutraceutical, and biomedical applications, combined with deep formulation expertise and consistent quality assurance. These factors create significant entry barriers for new competitors.

Vertical integration is the primary competitive strategy in the gelatin market. Leading manufacturers focus on controlling upstream raw material procurement to address challenges such as price volatility, quality inconsistencies, and supply disruptions related to bovine hides and porcine skins. By integrating processes such as sourcing slaughterhouse by-products, processing, and downstream gelatin manufacturing, companies ensure traceability, regulatory compliance, and stable input availability. These factors are particularly critical for pharmaceutical and medical-grade gelatin production. This strategy also enables manufacturers to optimize cost structures, maintain consistent bloom strength and functional performance, and efficiently meet customer-specific requirements. Consequently, vertically integrated players benefit from stronger negotiating power and greater operational resilience compared to smaller, non-integrated producers.

White-space opportunities are emerging in the premiumization of marine-based gelatin, presenting a strategic growth avenue within the competitive landscape. While animal-based gelatin continues to dominate, increasing demand for Halal, Kosher, allergen-sensitive, and sustainability-focused ingredients is driving interest in marine-based gelatin products. Premium offerings are characterized by enhanced purity, improved sensory attributes, traceability to sustainable fisheries, and suitability for high-value applications such as nutraceuticals, cosmetics, and biomedical uses. Companies that invest in advanced marine extraction technologies, branding, and application-specific innovations are well-positioned to capture additional value.

Gelatin Industry Leaders

-

Darling Ingredients Inc.

-

Gelita AG

-

Nitta Gelatin NA Inc.

-

SAS Gelatines Weishardt

-

Italgelatine SpA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- December 2025: Gelken has undertaken extensive production upgrades to deliver a consistent supply of high-quality fish gelatin and bovine gelatin. These improvements are designed to uphold consumer safety and maintain ingredient integrity for international product launches.

- May 2025: Darling Ingredients Inc. announced the signing of a non-binding term sheet with Tessenderlo Group to merge the collagen and gelatin segments of their businesses into a new entity named Nextida, without requiring any cash or initial investment from either party.

- September 2024: Gelita presented its new brands at CPHI Milan, showcasing its advanced controlled release portfolio of performance products specifically designed for superior softgels.

- May 2024: Nitta Gelatin initiated a project in Kochi, Kerala, to establish a new collagen peptide plant aimed at addressing the growing global demand for health ingredients.

Global Gelatin Market Report Scope

Gelatin is a natural, water-soluble protein obtained through the partial hydrolysis of collagen, which is primarily sourced from animal connective tissues.

The gelatin market is segmented based on form, application, and geography. Based on form, the market is segmented into animal-based and marine-based. Based on the application, the market is segmented into personal care and cosmetics, food and beverages, dietary supplements, pharmaceuticals, and others. The food and beverages are further subsegmented into bakery, beverages, confectionery, dairy and dairy alternative products, RTE/RTC food products, and others. Based on geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and the Middle East and Africa.

The report provides market size and forecasts in both value (USD) and volume (tons) for all the mentioned segments.

By Form

| Animal-Based |

| Marine-Based |

By Application

| Personal Care and Cosmetics | |

| Food and Beverages | Bakery |

| Beverages | |

| Confectionery | |

| Dairy and Dairy Alternatives Products | |

| RTE/RTC Food Products | |

| Others | |

| Dietary Supplements | |

| Pharmaceuticals | |

| Others |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Form | Animal-Based | |

| Marine-Based | ||

| By Application | Personal Care and Cosmetics | |

| Food and Beverages | Bakery | |

| Beverages | ||

| Confectionery | ||

| Dairy and Dairy Alternatives Products | ||

| RTE/RTC Food Products | ||

| Others | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Market Definition

- End User - The Protein Ingredients Market operates on a B2B basis. Food, Beverages, Supplements, Animal Feed, and Personal Care & Cosmetic manufacturers are considered to be end-consumers in the market studied. The scope excludes manufacturers buying liquid/dry whey to be used for application as a binding agent or thickener or other non-protein applications.

- Penetration Rate - Penetration Rate is defined as the percentage of Protein-Fortified End User Market Volume in the Overall End User Market Volume.

- Average Protein Content - Average protein content is the average protein content present per 100 g of product manufactured by all end-user companies considered under the scope of this report.

- End User Market Volume - End-user market volume is the consolidated volume of all types and forms of end-user products in the country or region.

| Keyword | Definition |

|---|---|

| Alpha-lactalbumin (α-Lactalbumin) | It is a protein that regulates the production of lactose in the milk of almost all mammalian species. |

| Amino acid | It is an organic compound that contains both amino and carboxylic acid functional groups, which are required for the synthesis of body protein and other important nitrogen-containing compounds, such as creatine, peptide hormones, and some neurotransmitters. |

| Blanching | It is the process of briefly heating vegetables with steam or boiling water. |

| BRC | British Retail Consortium |

| Bread improver | It is a flour-based blend of several components with specific functional properties designed to modify dough characteristics and give quality attributes to bread. |

| BSF | Black Soldier Fly |

| Caseinate | It is a substance produced by adding an alkali to acid casein, a derivative of casein. |

| Celiac disease | Celiac disease is an immune reaction to eating gluten, a protein found in wheat, barley, and rye. |

| Colostrum | It is a milky fluid that’s released by mammals that have recently given birth before breast milk production begins. |

| Concentrate | It is the least processed form of protein and has a protein content ranging from 40-90% by weight. |

| Dry protein basis | It refers to the percentage of "pure protein" present in a supplement after the water in it is completely removed through heat. |

| Dry whey | It is the product resulting from drying fresh whey which has been pasteurized and to which nothing has been added as a preservative. |

| Egg protein | It is a mixture of individual proteins, including ovalbumin, ovomucoid, ovoglobulin, conalbumin, vitellin, and vitellenin. |

| Emulsifier | It is a food additive that facilitates the blending of foods that are immiscible with one another, such as oil and water. |

| Enrichment | It is the process of addition of micronutrients that are lost during the processing of the product. |

| ERS | Economic Research Service of the USDA |

| Extrusion | It is the process of forcing soft mixed ingredients through an opening in a perforated plate or die designed to produce the required shape. The extruded food is then cut to a specific size by blades. |

| Fava | Also known as Faba, it is another word for yellow split beans. |

| FDA | Food and Drug Administration |

| Flaking | It is a process in which typically a cereal grain (like corn, wheat, or rice) is broken down into grits, cooked with flavors and syrups, and then pressed into flakes between cooled rollers. |

| Foaming agent | It is a food ingredient that makes it possible to form or maintain a uniform dispersion of a gaseous phase in a liquid or solid food. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Fortification | It is the deliberate addition of micronutrients that are not found in them naturally or which are lost during processing, to improve a food product's nutritional value. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Gelling agent | It is an ingredient that functions as a stabilizer and thickener to provide thickening without stiffness through the formation of gel. |

| GHG | Greenhouse Gas |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Hemp | It is a botanical class of Cannabis sativa cultivars grown specifically for industrial or medicinal use. |

| Hydrolysate | It is a form of protein manufactured by exposing the protein to enzymes that can partially break the bonds between the protein's amino acids and break down large, complicated proteins into smaller pieces. Its processing makes it easier and quicker to digest. |

| Hypoallergenic | It refers to a substance that causes fewer allergic reactions. |

| Isolate | It is the purest and most processed form of protein which has undergone separation to obtain a pure protein fraction. It typically contains ≥ 90% of protein by weight. |

| Keratin | It is a protein that helps form hair, nails, and the outer layer of skin. |

| Lactalbumin | It is the albumin contained in milk and obtained from whey. |

| Lactoferrin | It is an iron‑binding glycoprotein that is present in the milk of most mammals. |

| Lupin | It is the yellow legume seeds of the genus Lupinus. |

| Millenial | Also known as Generation Y or Gen Y, it refers to the people born from 1981 to 1996. |

| Monogastric | It refers to an animal with a single-compartmented stomach. Examples of monogastric include humans, poultry, pigs, horses, rabbits, dogs, and cats. Most monogastric are generally unable to digest much cellulose food materials such as grasses. |

| MPC | Milk protein concentrate |

| MPI | Milk protein isolate |

| MSPI | Methylated soy protein isolate |

| Mycoprotein | Mycoprotein is a form of single-cell protein, also known as fungal protein, derived from fungi for human consumption. |

| Nutricosmetics | It is a category of products and ingredients that act as nutritional supplements to care for skin, nails, and hair natural beauty. |

| Osteoporosis | It is a medical condition in which the bones become brittle and fragile from loss of tissue, typically as a result of hormonal changes, or deficiency of calcium or vitamin D. |

| PDCAAS | Protein digestibility-corrected amino acid score (PDCAAS) is a method of evaluating the quality of a protein based on both the amino acid requirements of humans and their ability to digest it. |

| Per-capita consumption of animal protein | It is the average amount of animal protein (such as milk, whey, gelatin, collagen, and egg proteins) that is readily available for consumption by each person in an actual population. |

| Per-capita consumption of plant protein | It is the average amount of plant protein (such as soy, wheat, pea, oat, and hemp proteins) that is readily available for consumption by each person in an actual population. |

| Quorn | It is a microbial protein manufactured using mycoprotein as an ingredient, in which the fungus culture is dried and mixed with egg albumen or potato protein, which acts as a binder, and then is adjusted in texture and pressed into various forms. |

| Ready-to-Cook (RTC) | It refers to food products that include all of the ingredients, where some preparation or cooking is required through a process that is given on the package. |

| Ready-to-Eat (RTE) | It refers to a food product prepared or cooked in advance, with no further cooking or preparation required before being eaten. |

| RTD | Ready-to-Drink |

| RTS | Ready-to-Serve |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Softgel | It is a gelatin-based capsule with a liquid fill. |

| SPC | Soy protein concentrate |

| SPI | Soy protein isolate |

| Spirulina | It is a biomass of cyanobacteria that can be consumed by humans and animals. |

| Stabilizer | It is an ingredient added to food products to help maintain or enhance their original texture, and physical and chemical characteristics. |

| Supplementation | It is the consumption or provision of concentrated sources of nutrients or other substances that are intended to supplement nutrients in the diet and is intended to correct nutritional deficiencies. |

| Texturant | It is a specific type of food ingredient that is used to control and alter the mouthfeel and texture of food and beverage products. |

| Thickener | It is an ingredient that is used to increase the viscosity of a liquid or dough and make it thicker, without substantially changing its other properties. |

| Trans fat | Also called trans-unsaturated fatty acids or trans fatty acids, it is a type of unsaturated fat that naturally occurs in small amounts in meat. |

| TSP | Textured soy protein |

| TVP | Textured vegetable protein |

| WPC | Whey protein concentrate |

| WPI | Whey protein isolate |

Need More Details on Market Definition?

Ask a Question

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms

Get More Details On Research Methodology

Download PDF