| Study Period | 2021 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 4.00 % |

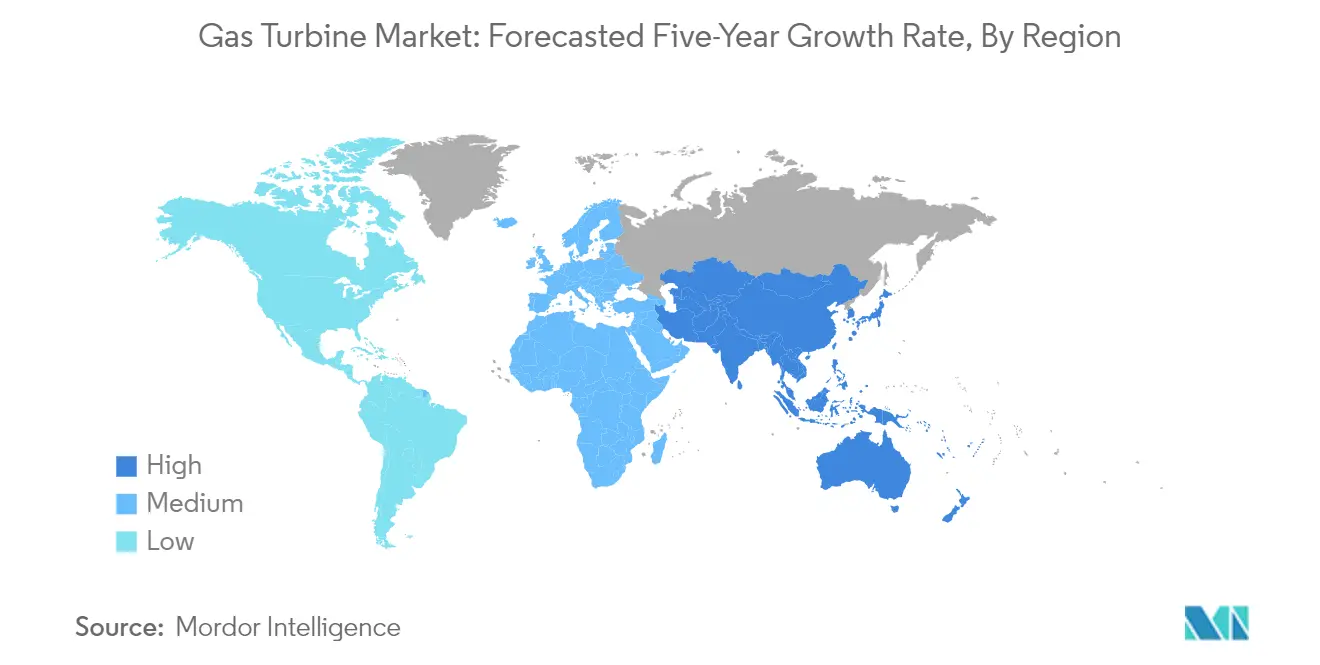

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

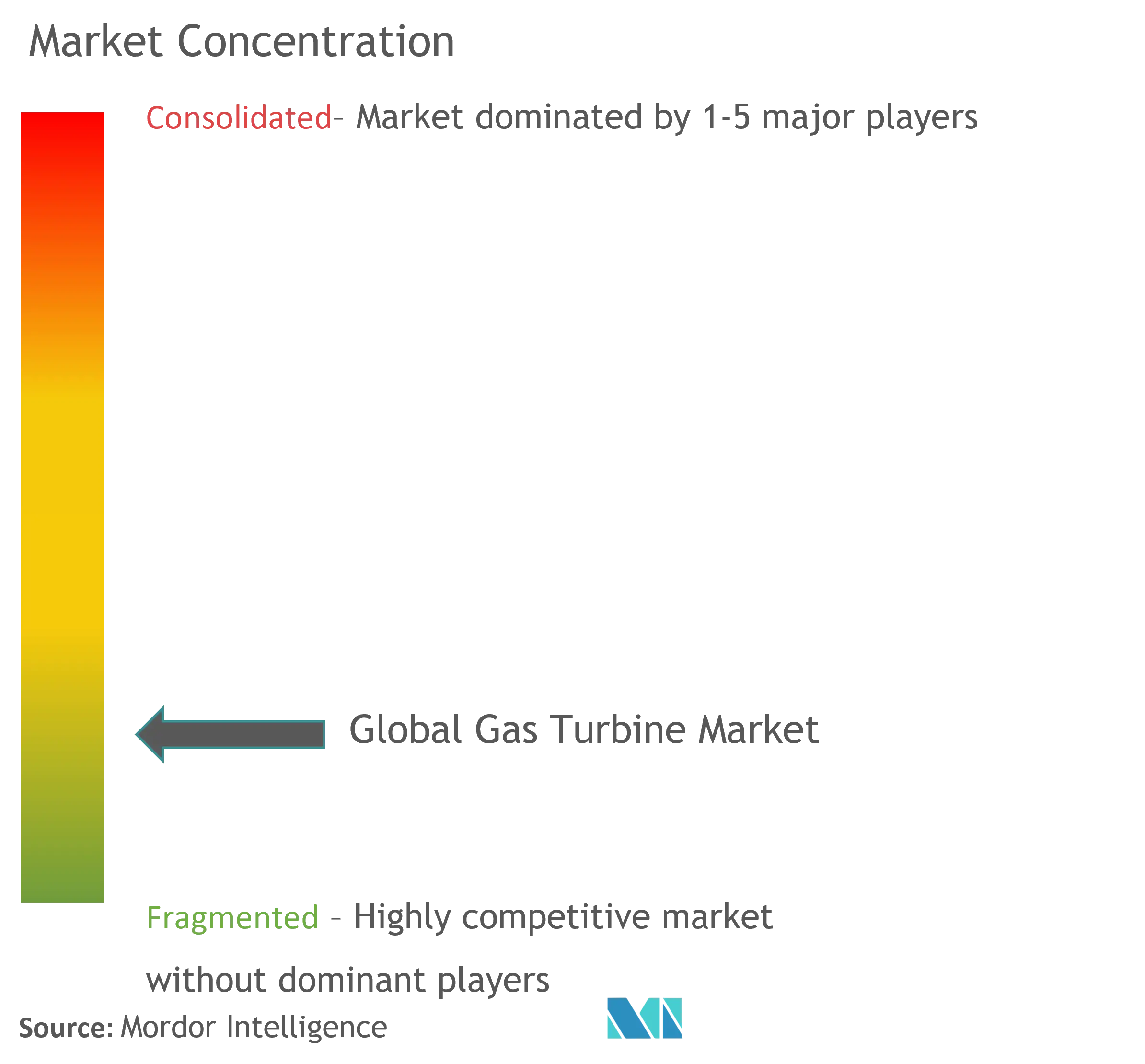

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order |

Gas Turbine Market Analysis

The Gas Turbine Market is expected to register a CAGR of greater than 4% during the forecast period.

The gas turbine industry is experiencing significant transformation driven by global energy transition initiatives and technological advancements. Major energy companies are increasingly investing in advanced gas turbine technologies to improve efficiency and reduce emissions, with manufacturers focusing on developing hydrogen-ready turbines to future-proof their installations. According to the International Energy Agency, gas-fired power generation is projected to increase by approximately 30% (+67 TWh) between 2021 and 2025, supported by various gas development projects and infrastructure expansion. The industry is witnessing a notable shift in investment patterns, with utilities and power producers prioritizing flexible and efficient gas turbine solutions that can complement renewable energy sources.

The market is characterized by substantial infrastructure development and modernization efforts across regions. In March 2023, the German government announced plans to auction off gas power plants to add 17-25 GW of gas-fired power capacity by 2030, demonstrating the continued importance of gas turbines in energy security strategies. The United States is similarly expanding its gas-fired power infrastructure, with plans to build 7.5 GW of new natural gas-fired capacity in 2023, of which 83% will be from combined-cycle plants. These developments reflect the growing recognition of gas turbines as a crucial bridge technology in the energy transition.

Technological innovation in the gas turbine sector is accelerating, with manufacturers focusing on improving efficiency, flexibility, and environmental performance. Advanced materials, digital technologies, and smart monitoring systems are being integrated into modern gas turbines to enhance their operational capabilities. In February 2023, GE announced the modernization of EnergyAustralia's Tallawarra A power plant, showcasing the industry's commitment to upgrading existing infrastructure with state-of-the-art technology. The integration of digital solutions and predictive maintenance capabilities is becoming increasingly important in maximizing turbine performance and reliability.

Regional energy security concerns are reshaping the gas turbine market landscape, particularly in Europe and Asia. Natural gas's role as a reliable power generation source has gained prominence amid energy security discussions, especially in regions seeking to diversify their energy mix. In Saudi Arabia, natural gas generated 269.4 TWh or 67% of total electricity in 2022, highlighting its significance in national energy strategies. The industry is witnessing increased investment in LNG infrastructure and gas-fired power plants, with countries developing more flexible and efficient power generation capabilities to ensure a stable energy supply while meeting environmental objectives.

Gas Turbine Market Trends

Shift from Coal to Natural Gas Turbine-Fired Power Generation Will Be a Major Driver

The global transition from coal to natural gas turbine-fired power generation continues to be a major driver for the gas turbine market, primarily due to its environmental and efficiency advantages. Natural gas burns significantly cleaner than other fossil fuels, producing approximately 30% less carbon dioxide than petroleum and about 45% less than coal for an equivalent amount of energy produced. Gas turbines and combined-cycle power plants are making substantial contributions to reducing greenhouse gas emissions, with combined-cycle facilities achieving efficiency rates approaching 60%, resulting in notably lower pollutant emissions compared to traditional steam-turbine plants of comparable output. This improved efficiency, coupled with stricter environmental regulations worldwide, is compelling power generators to shift away from coal-based generation.

Recent developments and announcements further reinforce this transition trend. In March 2023, the German government unveiled plans to use auctions to ensure the construction of new gas power plants, targeting 25 gigawatts of new gas power capacity by 2030. These plants are designed to provide energy security when renewable energy sources cannot meet demand. Similarly, in April 2023, GE secured a contract from UCED Group for the supply of LM6000 PC Sprint aero-derivative gas turbine to expand the UCED Prostějov reserve power plant, demonstrating the ongoing investment in gas turbine technology. Between 2023 and 2025, approximately 27.3 gigawatts of natural gas turbine-fired power generation capacity is scheduled to come online in the United States alone, highlighting the significant scale of this transition. These developments are supported by the fact that gas turbines can operate with more sustainable fuels such as hydrogen when blended with other fuels, aligning with various countries' long-term decarbonization strategies.

Understand The Key Trends Shaping This Market

Download PDF

Segment Analysis: Capacity

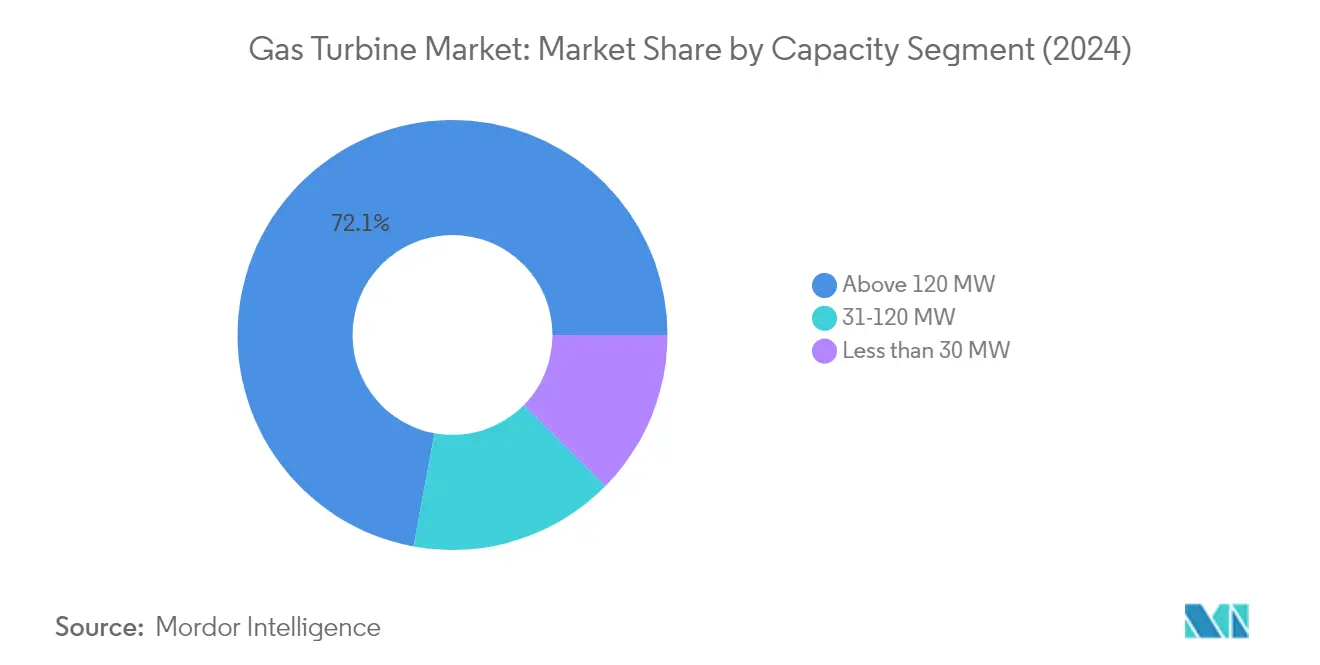

Above 120 MW Segment in Gas Turbine Market

The Above 120 MW segment dominates the global gas turbine market, accounting for approximately 72% of the total gas turbine market share in 2024. These high-capacity gas turbines are widely deployed throughout chemical process industries due to their ability to provide high power output and overall efficiency at relatively reasonable costs. They are extensively utilized in oil refineries and petrochemical plants for generating power during the cracking process. The segment's prominence is particularly evident in power generation plants, where heavy-duty gas turbines above 300 MW demonstrate combined cycle efficiency ranging from 50-70%. These turbines are categorized into different classes, including D/E (75-100 MW range), F-class (150-250 MW range), and the advanced G, H, and J classes, which deliver output exceeding 250 MW with superior efficiency levels of more than 62%.

31-120 MW Segment in Gas Turbine Market

The 31-120 MW segment is projected to experience the fastest growth in the gas turbine market during 2024-2029. This segment's growth is primarily driven by its extensive applications in oil and gas operations, particularly for providing on-site power to offshore platforms, floating production systems, and gas production facilities. These gas turbines are specifically designed to meet the power requirements of remote oil and gas fields, which operate like small isolated cities requiring substantial power generation capabilities. The segment is also witnessing increased adoption in Combined Cycle Gas Turbine (CCGT) plants, where both gas and steam turbines work in tandem to produce up to 50% more electricity from the same fuel compared to traditional simple-cycle plants. The growing trend of aero-derivative gas turbines in this segment, offering up to 45% efficiency compared to 35% for heavier gas turbines, is further accelerating market growth.

Remaining Segments in Capacity Segmentation

The Less than 30 MW segment plays a crucial role in distributed power generation at remote facilities, serving both industrial and utility applications. These smaller capacity gas turbines are particularly valuable in the petroleum industry, where they are employed in large buildings, complexes, and offices. The segment's significance extends to driving compressors on long-distance natural gas pipelines and maintaining well pressures in refineries and petrochemical plants. The versatility of these smaller units is demonstrated through their application in combined heat and power (CHP) systems, where they can operate on various fuel types, including landfill gas, digester gas, and coal mine methane, making them essential for resource recovery applications.

Segment Analysis: Type

Combined Cycle Segment in Gas Turbine Market

The Combined Cycle segment dominates the global gas turbine market, accounting for approximately 69% of the total market share in 2024. This dominance is primarily attributed to the higher efficiency and environmental benefits offered by combined cycle power plants, which can achieve efficiency rates of 50% to 60% compared to simple open-cycle applications. The segment's leadership position is further strengthened by increasing investments in new large gas-fired combined cycle power generation facilities worldwide. For instance, in 2023, the Czech energy group EPH secured a contract to build a 1.7 GW combined-cycle gas turbine power plant, demonstrating the continued preference for this technology. Additionally, the segment is projected to maintain its strong market position with the highest growth rate of around 4% during 2024-2029, driven by the global shift from coal to natural gas-fired power generation and the increasing need for efficient power generation solutions.

Open Cycle Segment in Gas Turbine Market

The Open Cycle segment represents a significant portion of the gas turbine market, serving specific applications where simplicity and quick start-up capabilities are prioritized over maximum efficiency. Open cycle gas turbines are particularly valuable in industrial applications, including oil and gas operations, where they are used for mechanical drives and on-site power generation. These systems are ideal in locations where gas is cost-effective but have been increasingly complemented by more efficient systems for new projects. The segment maintains its importance in the market due to its lower initial capital costs, smaller footprint requirements, and ability to provide peaking power in capacity-constrained areas. Power utilities often utilize gas turbines in the 5–40 MW size range to provide incremental capacity and grid support, making open cycle systems particularly valuable for emergency power generation and remote industrial applications.

Segment Analysis: End-User Industry

Power Segment in Gas Turbine Market

The power segment dominates the global gas turbine market, accounting for approximately 47% of the total market share in 2024. This segment's prominence is driven by the increasing shift from coal to natural gas-based power generation worldwide, particularly in developing economies. The segment's growth is further supported by the rising electricity demand, aging fleet of power plants requiring replacements, and the need for grid stability amidst increasing renewable energy integration. Several major economies are investing heavily in gas-fired power plants, with significant projects under development. For instance, according to the Energy Information Administration, between 2023 and 2025, around 27.3 gigawatts of natural gas-fired power generation capacity is scheduled to come online in the United States alone. Additionally, the segment is witnessing substantial growth due to the increasing adoption of combined cycle power plants, which offer higher efficiency and lower emissions compared to traditional power generation methods, making it a key driver in the gas turbines market for power industry.

Oil and Gas Segment in Gas Turbine Market

The oil and gas segment represents a significant portion of the gas turbine market, with applications spanning across upstream, midstream, and downstream operations. Gas turbines in this sector are specifically designed for use in power generation for offshore platforms, floating production systems (FPS), gas production, and process facilities. The segment's growth is driven by increasing exploration and production activities, particularly in regions like North America and the Middle East. The development of new LNG terminals and the expansion of existing facilities worldwide are creating additional demand for gas turbines. Moreover, the segment is witnessing technological advancements in terms of efficiency improvements and emissions reduction capabilities, making gas turbines more attractive for oil and gas applications.

Remaining Segments in End-User Industry

Other end-user industries utilizing gas turbines include the chemical and mining sectors, where these machines play crucial roles in providing reliable power supply for various operations. In the chemical industry, gas turbines are essential for providing heat and electricity to drive different processes, while in the mining sector, they are primarily used for on-site power generation in remote locations. These industries particularly value gas turbines for their reliability, efficiency, and ability to operate in harsh environments. The adoption of gas turbines in these sectors is influenced by factors such as increasing industrialization, growing demand for chemicals, and the expansion of mining activities in emerging economies, contributing to the growth of the industrial gas turbine market.

Gas Turbine Market Geography Segment Analysis

Gas Turbine Market in North America

North America represents one of the most mature gas turbine markets globally, characterized by significant investments in power generation infrastructure and a strong focus on transitioning from coal to natural gas-based power generation. The United States and Canada are the primary contributors to the region's gas turbine market size, with both countries showing substantial development in gas-fired power plants and combined cycle power generation facilities. The region's growth is primarily driven by the replacement of aging power infrastructure, increasing natural gas production, and stringent environmental regulations promoting cleaner energy sources.

Gas Turbine Market in the United States

The United States dominates the North American gas turbine market, leveraging its vast natural gas resources and extensive power generation infrastructure. The country has witnessed significant developments in gas-fired power generation, particularly in combined cycle power plants. With approximately 63% share of the North American market in 2024, the U.S. market is driven by factors such as the decommissioning of coal-fired plants, the development of new natural gas power plants, and growing exploration and production of unconventional gas. The country's electricity generation from natural gas reached significant levels, making it the primary energy source for power generation.

Gas Turbine Market in Canada

Canada's gas turbine market is experiencing steady growth with an expected growth rate of approximately 3% from 2024-2029. The country's market is primarily driven by the increasing adoption of natural gas for power generation and the government's focus on reducing greenhouse gas emissions. Canada's strategic initiatives to maximize economic and environmental benefits through large-scale gas power plant development have created significant opportunities for market expansion. The country's abundant natural gas resources and supportive regulatory framework continue to attract investments in gas-based power generation infrastructure.

Gas Turbine Market in Europe

The European gas turbine market is characterized by a strong focus on energy transition and environmental sustainability. The region encompasses major markets including Germany, France, the United Kingdom, and Russia, each contributing significantly to the overall market dynamics. The European market is driven by the increasing shift from coal-based power generation to natural gas, coupled with the need to ensure grid stability amid growing renewable energy integration. The region's commitment to reducing carbon emissions while maintaining energy security has led to substantial investments in gas turbine technology.

Gas Turbine Market in Russia

Russia maintains its position as the largest gas turbine market in Europe, with approximately 44% market share in 2024. The country's market is supported by its vast natural gas reserves and significant power generation capacity. Russia's thermal and electrical plants have maintained the largest installed capacity in the region, with gas-fired power plants having substantial installed capacity. The country's continued investment in power infrastructure and development of new gas-based power plants reinforces its dominant position in the European market.

Gas Turbine Market in Germany

Germany is experiencing rapid growth in its gas turbine market, with an anticipated growth rate of approximately 3% from 2024-2029. The country's market expansion is driven by its ambitious plans to phase out coal and nuclear energy while maintaining grid stability. Germany's commitment to developing new gas power plants and its focus on hydrogen-ready gas turbine technology demonstrates its progressive approach toward energy transition. The government's initiatives to auction off gas power plants and add significant gas-fired power capacity highlight the market's growth potential.

Gas Turbine Market in Asia-Pacific

The Asia-Pacific region represents a dynamic gas turbine market, with diverse countries contributing to its growth trajectory. China, India, Japan, ASEAN countries, and Australia form the key markets in this region, each with distinct characteristics and growth drivers. The region's rapid industrialization, increasing electricity demand, and growing focus on cleaner energy sources have created substantial opportunities for gas turbine deployment. The market is further supported by significant investments in power generation infrastructure and the development of natural gas supply networks.

Gas Turbine Market in China

China leads the Asia-Pacific gas turbine market, demonstrating remarkable market presence and growth potential. The country's commitment to reducing carbon emissions and achieving carbon neutrality by 2060 has accelerated the adoption of gas turbines in power generation. China's strategic focus on developing gas-fired power plants, coupled with its robust industrial sector and growing electricity demand, continues to drive market expansion. The country's initiatives in developing indigenous gas turbine technology and expanding its gas infrastructure further strengthen its market position.

Gas Turbine Market in ASEAN Countries

The ASEAN region represents one of the fastest-growing markets for gas turbines in Asia-Pacific. Countries like Indonesia, Malaysia, Thailand, and the Philippines are witnessing increased adoption of gas turbines, driven by rising power demand and energy infrastructure development. The region's focus on transitioning to cleaner energy sources and modernizing power generation facilities has created significant opportunities for market growth. Government initiatives supporting gas-fired power plants and the development of LNG infrastructure continue to boost market expansion.

Gas Turbine Market in South America

The South American gas turbine market is characterized by significant developments in natural gas infrastructure and power generation capacity. Brazil and Argentina are the key markets in this region, with Brazil emerging as both the largest and fastest-growing market. The region's market is driven by increasing electricity consumption, significant intermittent sources of electricity, and the participation of international companies in facilitating gas turbines. The development of new gas-fired power plants and the modernization of existing facilities continue to shape the market landscape in South America.

Gas Turbine Market in Middle East & Africa

The Middle East & Africa region presents a robust gas turbine market, supported by substantial investments in power generation infrastructure and industrial development. The region encompasses key markets including Saudi Arabia, United Arab Emirates, Egypt, and South Africa, with Saudi Arabia emerging as the largest market and the UAE showing the fastest growth. The region's abundant natural gas resources, coupled with increasing industrialization and urbanization, drive the demand for gas turbines. Government initiatives focusing on energy diversification and the development of gas-fired power plants continue to create significant market opportunities.

Get Analysis on Important Geographic Markets

Download PDF

Gas Turbine Industry Overview

Top Companies in Gas Turbine Market

The gas turbine market is dominated by established players like General Electric, Mitsubishi Heavy Industries, Siemens Energy, Kawasaki Heavy Industries, and Solar Turbines, who have built a strong global presence through decades of operation. These gas turbine companies are heavily investing in research and development to create more efficient and environmentally friendly gas turbine technologies, particularly focusing on hydrogen compatibility and carbon capture integration. The industry shows a clear trend toward strategic collaborations and joint ventures to combine technological expertise and market access, especially in emerging markets. Companies are expanding their service networks and aftermarket support capabilities to provide comprehensive lifecycle solutions. There is also an increasing focus on digitalization and smart technologies to enhance turbine performance monitoring and predictive maintenance capabilities.

Consolidated Market with High Entry Barriers

The gas turbine market exhibits a highly consolidated structure dominated by large multinational conglomerates with integrated manufacturing and service capabilities. These established players possess significant advantages through their extensive intellectual property portfolios, established supply chains, and long-standing customer relationships in key markets. The high capital requirements, complex manufacturing processes, and need for specialized technical expertise create substantial barriers to entry for new players. The market has witnessed strategic acquisitions and partnerships, particularly in emerging economies, as companies seek to strengthen their regional presence and technological capabilities.

The competitive dynamics are characterized by a mix of global leaders and regional specialists, with the latter focusing on specific market segments or geographical regions. Chinese manufacturers like Harbin Electric and Dongfang Electric are increasingly gaining prominence through government support and domestic market advantages. The industry has seen a trend toward vertical integration, with major players expanding their capabilities across the value chain, from component manufacturing to aftermarket services. This consolidation has led to increased market power for dominant players while making it challenging for smaller companies to compete effectively.

Innovation and Sustainability Drive Future Success

Success in the gas turbine world increasingly depends on companies' ability to innovate while meeting stringent environmental regulations and efficiency requirements. Incumbent gas turbine companies must focus on developing next-generation turbine technologies that offer higher efficiency, fuel flexibility, and lower emissions to maintain their market position. The ability to provide comprehensive solutions that integrate renewable energy systems and energy storage capabilities will become crucial. Companies need to strengthen their digital capabilities and service networks while maintaining cost competitiveness through operational excellence and supply chain optimization.

For contenders looking to gain market share, specialization in specific market segments or geographical regions offers a viable strategy. Success factors include developing innovative financing solutions, building strong local partnerships, and offering specialized services that address specific customer needs. The increasing focus on decarbonization presents opportunities for companies that can effectively integrate carbon capture technologies and hydrogen-ready solutions. Regulatory changes supporting clean energy transition and regional content requirements will continue to shape market dynamics, while the concentration of large power generation customers necessitates strong relationship management capabilities and proven track records.

Gas Turbine Market Leaders

-

Siemens AG

-

Mitsubishi Heavy Industries Ltd

-

General Electric Company

-

Kawasaki Heavy Industries Ltd

-

Wartsila Oyj Abp

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Gas Turbine Market News

In February 2022, a consortium formed by the Spanish companies Técnicas Reunidas and TSK was awarded a contract by Comisión Federal de Electricidad (CFE) of Mexico for the design and execution of Valladolid and Mérida combined cycle plants. These plants are expected to have an approximate capacity of 1,000 MW and 500 MW, respectively.

In April 2022, Malaysia's largest gas-based power plant Edra Energy's 2.2 GW combined cycle power plant, commenced operations in Alor Gajah, Malacca, Malaysia. The new plant consists of three generating blocks capable of generating over 745 MW per block, each including a GE 9HA.02 gas turbine, an STF-D650 steam turbine, a W88 generator, and a Heat Recovery Steam Generator (HRSG).

Gas Turbine Market Report - Table of Contents

1. MARKET OVERVIEW

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD billion, till 2027

- 4.3 Recent Trends and Developments

-

4.4 Market Dynamics

- 4.4.1 Drivers

- 4.4.2 Restraints

- 4.5 Supply-Chain Analysis

-

4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Capacity

- 5.1.1 Less than 30 MW

- 5.1.2 31-120 MW

- 5.1.3 Above 120 MW

-

5.2 By Type

- 5.2.1 Combined Cycle

- 5.2.2 Open Cycle

-

5.3 By End-User Industry

- 5.3.1 Power

- 5.3.2 Oil and Gas

- 5.3.3 Other End-user Industries

-

5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.2 North America

- 5.4.3 Europe

- 5.4.4 South America

- 5.4.5 Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

-

6.3 Company Profiles

- 6.3.1 Siemens AG

- 6.3.2 Mitsubishi Heavy Industries Ltd

- 6.3.3 General Electric Company

- 6.3.4 Kawasaki Heavy Industries Ltd

- 6.3.5 Wartsila Oyj Abp

- 6.3.6 IHI Corporation

- 6.3.7 Solar Turbines Incorporated

- 6.3.8 Bharat Heavy Electricals Limited

- 6.3.9 Ansaldo Energia SpA

- *List Not Exhaustive

- 6.4 *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Gas Turbine Industry Segmentation

A gas turbine, also called a combustion turbine, is a continuous-flow internal combustion engine that uses natural gas to generate electricity.

The global gas turbine market is segmented by capacity, type, end-user industry, and geography. By capacity, the market is segmented into less than 30 MW, 31-120 MW, and above 120 MW. By type, the market is segmented into combined and open cycles. By end-user industry, the market is segmented into power, oil and gas, and other end-user Industries. The report also covers the market size and forecasts for the gas turbine market across the major regions. For each segment, the market sizing and forecasts have been done based on revenue (USD billion).

| By Capacity | Less than 30 MW |

| 31-120 MW | |

| Above 120 MW | |

| By Type | Combined Cycle |

| Open Cycle | |

| By End-User Industry | Power |

| Oil and Gas | |

| Other End-user Industries | |

| By Geography | Asia-Pacific |

| North America | |

| Europe | |

| South America | |

| Middle East and Africa |

Need A Different Region or Segment?

Customize Now

Gas Turbine Market Research FAQs

What is the current Gas Turbine Market size?

The Gas Turbine Market is projected to register a CAGR of greater than 4% during the forecast period (2025-2030)

Who are the key players in Gas Turbine Market?

Siemens AG, Mitsubishi Heavy Industries Ltd, General Electric Company, Kawasaki Heavy Industries Ltd and Wartsila Oyj Abp are the major companies operating in the Gas Turbine Market.

Which is the fastest growing region in Gas Turbine Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Gas Turbine Market?

In 2025, the Asia-Pacific accounts for the largest market share in Gas Turbine Market.

What years does this Gas Turbine Market cover?

The report covers the Gas Turbine Market historical market size for years: 2021, 2022, 2023 and 2024. The report also forecasts the Gas Turbine Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Gas Turbine Market Research

Mordor Intelligence offers comprehensive insights into the gas turbine industry through detailed industry analysis and consulting services. Our extensive research covers the global gas turbine market. This includes industrial gas turbine applications, aviation gas turbine developments, and power generation solutions. The report provides in-depth coverage of gas turbine vendors, emerging technologies, and regional market dynamics across Asia Pacific, Europe, and North America.

Stakeholders gain valuable insights through our detailed market forecast and industry trends analysis. These are available in an easy-to-read report PDF format for download. The research encompasses crucial aspects of gas turbine services and technological innovations. It also offers detailed market outlook projections. Our analysis supports strategic decision-making with comprehensive coverage of new industrial gas turbines. It also explores evolving market dynamics in the gas turbines market for power industry, enabling businesses to navigate the complex landscape of turbine technologies and services effectively.