Fraud Detection And Prevention (FDP) Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

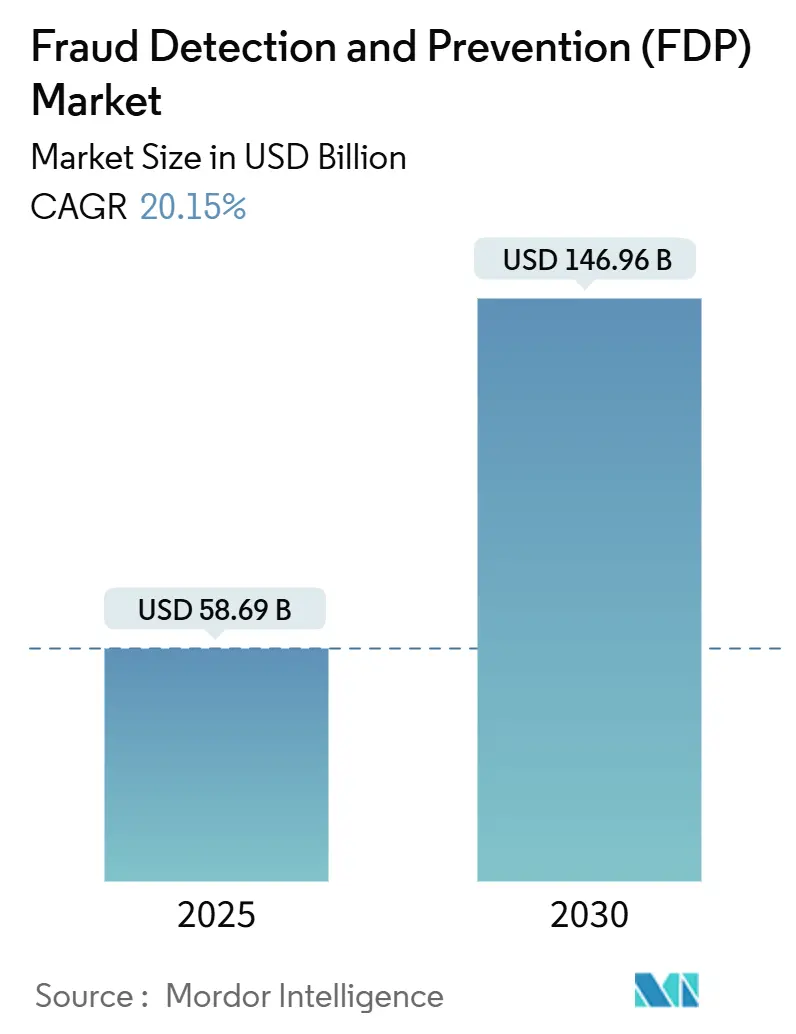

| Market Size (2025) | USD 58.69 Billion |

| Market Size (2030) | USD 146.96 Billion |

| Growth Rate (2025 - 2030) | 20.15% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fraud Detection And Prevention (FDP) Market Analysis by Mordor Intelligence

The fraud detection and prevention market reached USD 58.69 billion in 2025 and is set to climb to USD 146.96 billion by 2030, translating into a 20.15% CAGR. This steep trajectory mirrors the surge in deepfake scams, synthetic identities, and other AI-enabled threats that overwhelm legacy rule engines and elevate demand for adaptive machine-learning defenses. Regulatory momentum, notably the European PSD3 and PSR package that tightens Strong Customer Authentication (SCA) from 2026, accelerates technology refresh cycles as banks look to align security, compliance, and customer experience in real time. Fraud detection and prevention market in various countries is fueled by mobile-first payment habits and laws such as the Philippines’ Anti-Financial Account Scamming Act that mandates automated, real-time monitoring. Intensifying supply-chain fraud, evidenced by triple-digit spikes in counterfeit component scams, further underscores because organizations now treat security as a revenue-protection lever, not merely a compliance cost.

Key Report Takeaways

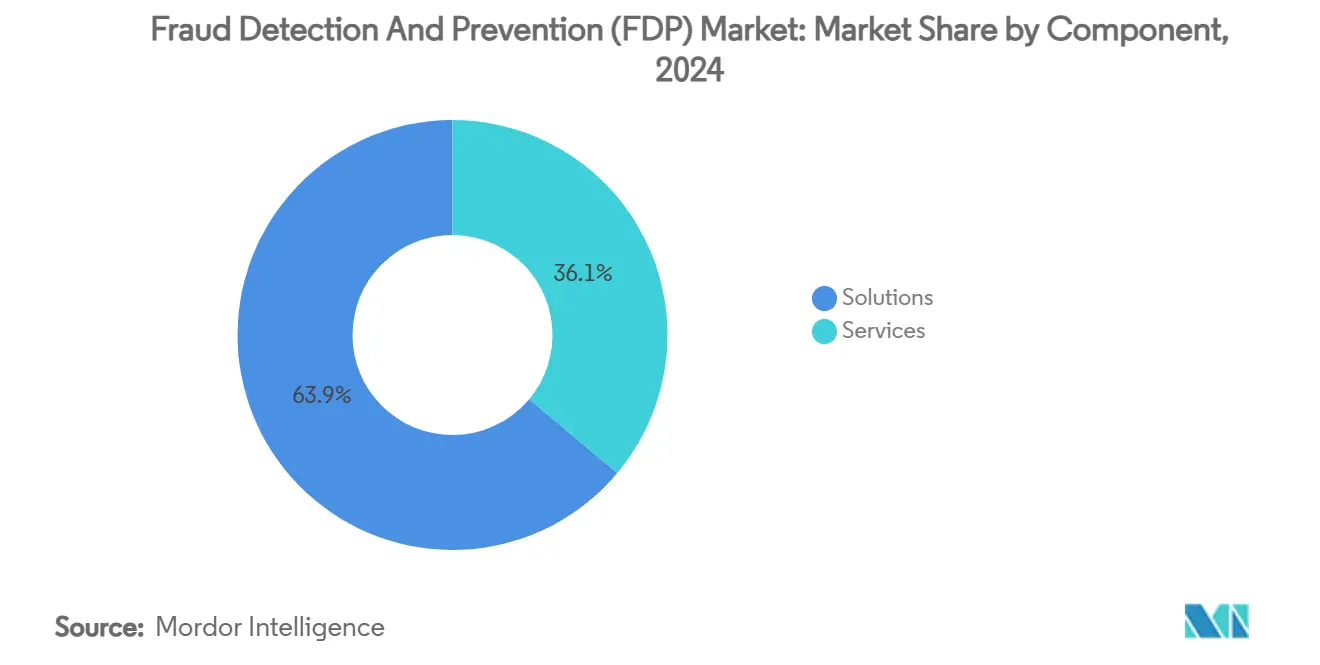

- By component, solutions led with 63.9% revenue share in 2024, while services are forecast to rise at a 21.5% CAGR through 2030.

- By deployment mode, on-premises captured 56.1% of the fraud detection and prevention market share in 2024; cloud deployments are projected to expand at a 22.7% CAGR to 2030.

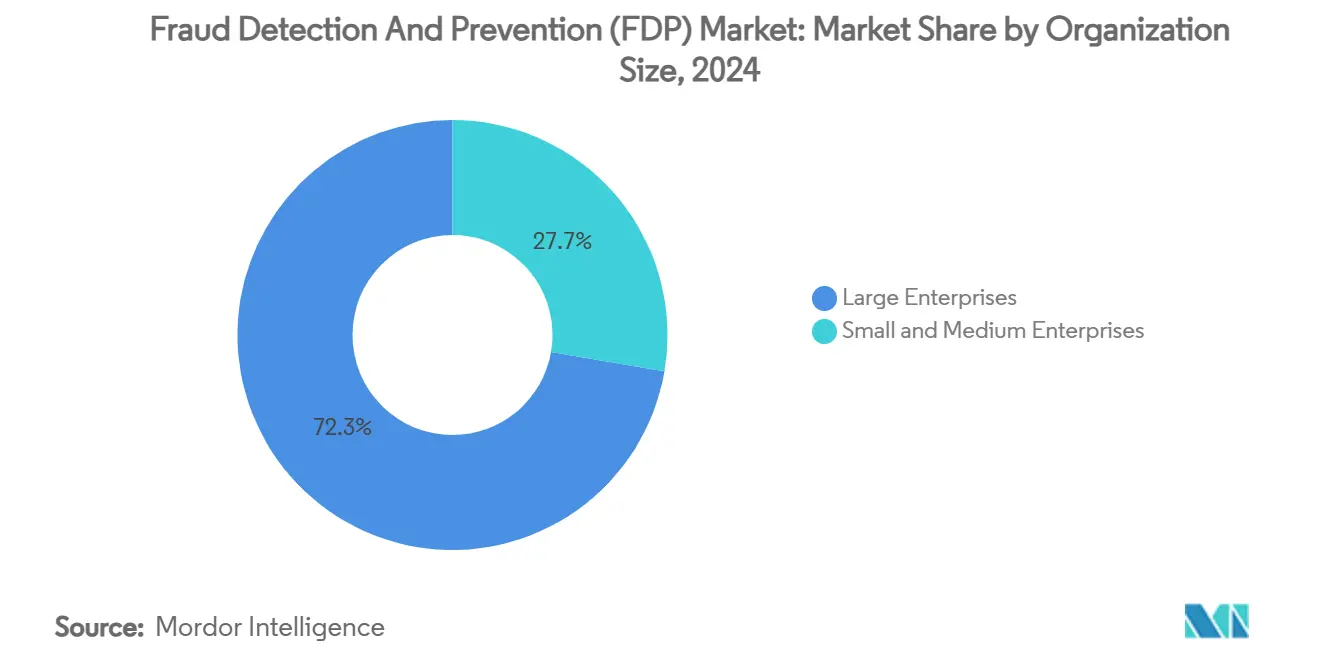

- By organization size, large enterprises controlled 72.3% of the 2024 market, whereas SMEs are advancing at a 21.9% CAGR through 2030.

- By end-user industry, the BFSI segment held 32.6% revenue share in 2024, and retail & e-commerce is poised for the fastest 20.4% CAGR to 2030.

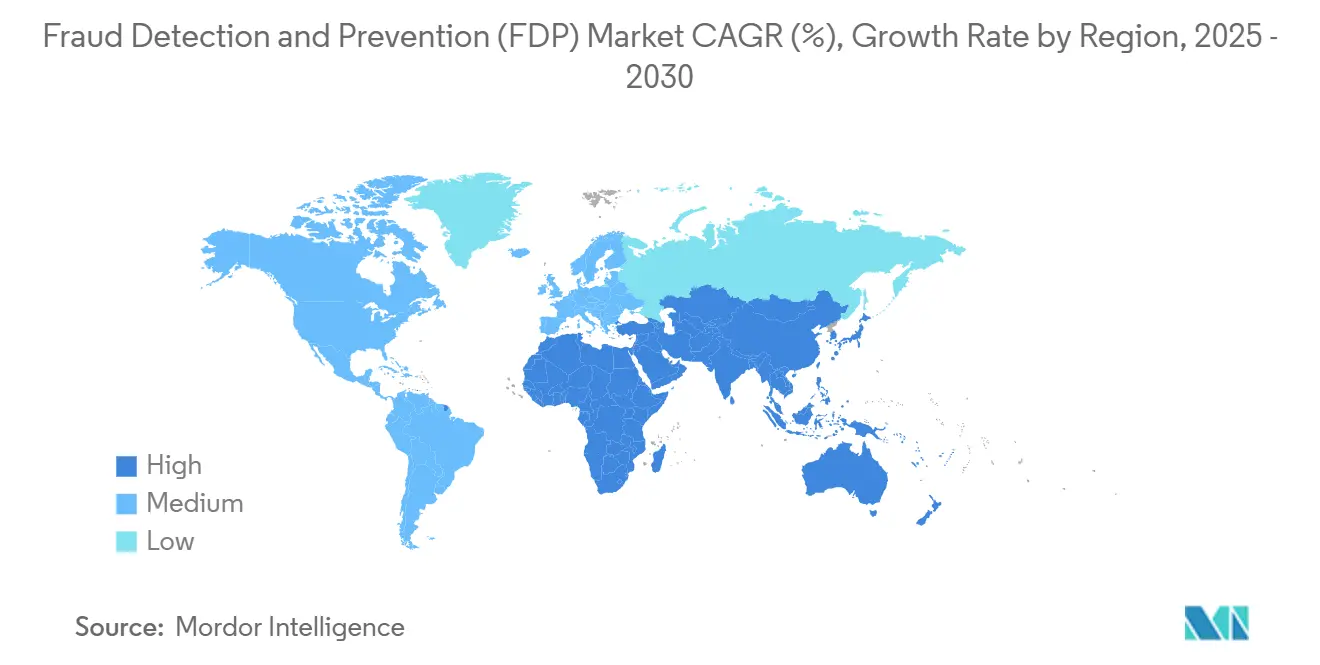

- Regionally, North America retained 27.5% share of the 2024 fraud detection and prevention market size, while Asia-Pacific is the quickest-growing region at 20.1% CAGR through 2030.

Global Fraud Detection And Prevention (FDP) Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising digital payments and e-commerce volumes | +4.2% | Global, with Asia-Pacific leading adoption | Medium term (2-4 years) |

| Stringent regulatory compliance pressures | +3.8% | Europe and North America primarily | Short term (≤ 2 years) |

| AI/ML-enabled analytics improving detection accuracy | +5.1% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Tokenization and 3-D Secure 2.3 boosting adoption | +2.3% | Europe and North America | Medium term (2-4 years) |

| Open Banking/instant-payment rails creating new fraud vectors | +2.8% | Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Generative-AI deepfake fraud escalation | +3.4% | Global, with financial centers most affected | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Digital Payments and E-commerce Volumes

Mobile wallets, QR codes, and contactless cards now dominate checkout flows, expanding attack surfaces that legacy systems cannot parse effectively. Real-time analysis of device fingerprinting and behavioral biometrics has therefore become mandatory to distinguish legitimate customers from bots or scripted card-testing attacks.[1]Ping Identity, "From Friction to Trust: Rethinking Seamless Fraud Prevention," pingidentity.comE-commerce fraud losses reached USD 48 billion in 2023, with card-not-present (CNP) transactions as the chief culprit, pushing merchants toward cloud-based risk engines that score transactions in milliseconds. Retail platforms increasingly embed these engines directly in payment gateways to preserve checkout speed while reducing chargeback exposure. As digital-first consumers continue to displace in-store traffic, demand for scalable detection that adapts to novel payment formats—such as buy-now-pay-later and instant-credit lines—intensifies across every major geography.

Stringent Regulatory Compliance Pressures

Europe’s PSD3 and PSR overhaul expands SCA beyond two-factor credentials to include mandatory payee name verification and real-time fraud data sharing among financial institutions. Vendors that deliver single platforms covering authentication, analytics, and reporting gain an edge as banks consolidate point products to rein in compliance overhead. The global nature of cross-border commerce compels US banks and PSPs to meet European SCA benchmarks when serving EU clients, effectively exporting stricter standards worldwide. Similar momentum appears in Asia-Pacific, where regulators in Singapore and Australia link operating licences to monitored fraud thresholds. Compliance thus compresses deployment timelines, pushing even risk-averse institutions toward cloud infrastructures that offer rapid rule and model updates without lengthy change-control cycles.

AI/ML-Enabled Analytics Improving Detection Accuracy

Machine-learning pipelines now drive fraud decisions in milliseconds, training on billions of transactions to predict risk at the user, device, and network levels. JPMorgan Chase reports detection speeds 300 times faster than legacy rules and USD 200 million in yearly operating savings after switching to behavior-based AI models. Techniques such as ensemble learning and graph neural networks surface hidden mule networks and triangulate suspicious device clusters. Explainable AI overlays provide regulators with feature-importance narratives, satisfying audit needs without slowing response times. Together, these advances contribute 5.1 percentage points to forecast CAGR, making adaptive analytics the single largest engine of long-term growth for the fraud detection and prevention market.

Generative-AI Deepfake Fraud Escalation

Open-source voice-cloning and synthetic-identity toolkits have slashed the cost and skill required to execute high-value social-engineering scams. Financial institutions now face “fraud-as-a-service” models that rent AI bots capable of bypassing call-center voice verification or forging realistic photo IDs. Countermeasures center on liveness detection, multi-factor biometrics, and continuous authentication streams that assess micro-expressions or background audio cues. Vendors such as Thales layer facial recognition, voice analysis, and behavioral biometrics to differentiate genuine users from deepfake imposters.[2]Rob Eijbergen, “Deepfake Fraud: How Thales Combats Synthetic Biometric Attacks,” Thales Group, thalesgroup.com As attacks proliferate, enterprises acknowledge a sustained arms race in which the ability to update detection models daily becomes a competitive necessity.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High false-positive rates hurting customer experience | -2.1% | Global, particularly affecting digital-first institutions | Medium term (2-4 years) |

| Integration complexity with legacy systems | -1.8% | North America and Europe with established banking infrastructure | Long term (≥ 4 years) |

| Lack of labelled data sets for AI model training | -1.4% | Global, more pronounced in emerging markets | Long term (≥ 4 years) |

| Data-sharing limits under privacy regulations | -1.2% | Europe under GDPR, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High False-Positive Rates Hurting Customer Experience

Overly sensitive rule sets can tag legitimate spend as suspicious, triggering manual reviews that stall instant-payment expectations. Customer surveys show that two consecutively declined genuine transactions triple the likelihood of switching banks within a year. Modern AI engines reduce noise by profiling individual spending rhythms, seasonal travel patterns, and device preferences, cutting false-positive counts by up to half without sacrificing catch rates. [3]Cognizant, "AI Machine Learning Fraud Detection," cognizant.comYet the shift to real-time settlement compresses decision windows to mere seconds, leaving no room for human intervention. Institutions therefore calibrate risk thresholds more carefully, accepting marginally higher fraud loss on low-ticket items to protect overall conversion and satisfaction metrics.

Integration Complexity with Legacy Systems

Mainframe-based core banking platforms often lack standardized APIs or possess fragmented data schemas that hamper real-time analytics. Projects to bolt modern detection layers onto these cores can overrun budgets and stretch beyond 18 months, during which institutions must keep parallel stacks live for regulatory continuity. Data quality shortfalls—missing fields, inconsistent time stamps, duplicate customer accounts—undercut model accuracy and inflate feature-engineering workloads. While containerized, cloud-native fraud engines promise faster rollouts, many large banks opt for hybrid architectures that keep sensitive records on-premises yet stream tokenized feeds to the cloud for model training. Competitively, this integration drag opens space for digital-only challengers that deploy plug-and-play fraud defenses in weeks, eroding incumbents’ share in certain product niches.

Segment Analysis

By Component: Solutions Lead While Services Accelerate

Solutions hold 63.9% of the fraud detection and prevention market size, underscoring the foundational role of analytics engines, authentication modules, and investigator dashboards. Vendors refine rule libraries with adaptive machine learning, letting financial institutions ingest terabytes of behavioral data per day and respond to fresh attack signatures in near real time. Solutions revenue also reflects regulatory reporting modules that convert detection data into audit-ready formats, allowing risk officers to satisfy PSD3, GDPR, or OCC exams without separate tooling.

Services, although smaller, are expanding at 21.5% CAGR as boards delegate 24/7 monitoring to managed-security specialists that provide calibrated models, curated global threat feeds, and post-incident forensics. Talent shortages in data science and cyber-ops elevate the appeal of outcome-based contracts that guarantee detection-rate SLAs. In parallel, consulting wraps around solution deployments to re-engineer KYC flows, optimize alert triage, and streamline dispute resolution. This convergence of technology and expertise is expected to lift services to almost one-third of 2030 revenue, reinforcing their strategic position within the broader fraud detection and prevention market.

By Deployment Mode: Cloud Transformation Accelerates

On-premises installations retained 56.1% of 2024 revenue as tier-one banks leveraged sunk infrastructure and met data-residency statutes by processing PII in their own data centers. These firms favor hybrid patterns that shift model training to the cloud yet keep production scoring nodes in private clusters to minimize latency. Under such architectures, anti-fraud latency remains below 10 milliseconds even at holiday peak volumes.

Cloud-native platforms, however, outpace all others at a 22.7% CAGR and will narrow the share gap rapidly. Subscription pricing aligns license fees with transaction growth, letting mid-tier lenders and fintechs avoid capital outlays. Leading vendors now pre-package continuous deployment toolchains that refresh detection models multiple times per week, shortening exposure windows to novel frauds. Advanced encryption and confidential-compute zones address lingering sovereignty worries, while certifications like ISO 27001 and SOC 2 reassure auditors. These advantages collectively establish cloud as the future default for the fraud detection and prevention market.

By Organization Size: SME Adoption Surges Despite Enterprise Dominance

Large enterprises accounted for 72.3% of 2024 revenue, reflecting hefty transaction volumes, complex fraud surfaces, and multi-jurisdictional compliance burdens. Their strategy typically layers behavioral analytics over transaction screening, device intel, and consortium data, with dedicated threat-hunting teams tuning thresholds daily. The resulting defense-in-depth stance solidifies enterprise spending clout and continues to anchor vendor road-maps around scale and configurability.

SMEs, while smaller in absolute dollars, are growing the fastest at 21.9% CAGR because cloud delivery removes the need for in-house data-science talent or six-figure licence commitments. Plug-and-play APIs from vendors like PayPal’s Braintree inject AI models directly into payment workflows, flagging suspect orders before authorization completes. Many mid-size merchants now join risk-sharing consortiums that pool anonymized signals across tens of thousands of peers, giving them big-bank visibility without owning the data lake. As a result, SMEs will uplift the total fraud detection and prevention market by broadening its customer base beyond the traditional banking segment.

By End-User Industry: BFSI Leads While Retail Accelerates

The BFSI vertical generated 32.6% of total revenue in 2024, underpinned by stringent supervisory expectations and direct monetary exposure. Banks confront layered threats—synthetic IDs at account opening, mule networks in P2P transfers, and voice-cloned requests in call centers—necessitating multi-factor, real-time defenses. Investment also targets cross-border money-laundering patterns, aligning with FATF guidelines and bolstering risk-based AML scoring for high-risk corridors.

Retail and e-commerce, posting a 20.4% CAGR, capitalizes on soaring online volumes and the sticky reputational harm of chargebacks. Merchants integrate AI fraud engines inside checkout pages, using device telemetry, e-mail tenure, and historic basket data to achieve sub-second approvals. Tokenized wallets and 3-D Secure 2.3 protocols reduce friction on low-risk traffic but escalate screening for atypical geographies or order values. Similar momentum surfaces in public-sector grants disbursement, healthcare claim adjudication, and smart-grid utilities, each leveraging the same underlying analytics core adapted to domain-specific data fields. Collectively, these sectors expand the addressable fraud detection and prevention market by diversifying use cases beyond traditional financial transactions.

Geography Analysis

North America generated the largest regional slice at 27.5% of 2024 revenue, supported by early cloud adoption, sophisticated threat intelligence sharing, and sizeable technology budgets. Federal agencies such as the US Treasury recovered USD 1 billion in check fraud during fiscal 2024 after deploying AI-driven anomaly detection, signaling public-sector validation that further stimulates private-sector uptake. US card networks likewise advocate AI-based pre-authorization scoring to curb CNP chargebacks, embedding fraud logic directly in payment rails. Canadian banks collaborate in a joint consortium to combat emerging real-time rail fraud, demonstrating regional co-operation on signals exchange.

Europe follows with rapid regulatory expansion as PSD3 and PSR introduce mandatory payee-name matching and real-time risk feeds. GDPR constraints drive innovation in privacy-preserving federated learning, allowing banks to train cross-bank models without raw-data transfers. Telecom operators must filter spoofed calls and malware SMS under new eIDAS updates, broadening the fraud detection and prevention market into telco infrastructure. Nations such as Spain impose EUR 2 million (USD 2.35 million) fines on carriers that fail to implement these measures, embedding security requirements deep in operational licences.

Asia-Pacific records the fastest 20.1% CAGR, led by high mobile payment penetration and fragmented compliance terrain that forces vendors to offer configurable policy engines. The Philippines’ Anti-Financial Account Scamming Act compels fraud systems scaled to institution size, while India’s RBI mandates AI-powered transaction monitoring for UPI instant payments. Mainland China pilots AI corruption analytics on welfare distributions, proving applicability beyond fintech into public-fund oversight. Together, these dynamics amplify regional demand for flexible, real-time solutions, elevating APAC’s weighting in the global fraud detection and prevention market.

Competitive Landscape

The vendor matrix remains moderately fragmented, with top providers jointly controlling under half of global revenue. Technology differentiation pivots on model explainability, consortium data breadth, and deployment agility rather than features parity. IBM, Oracle, and Microsoft embed fraud micro-services inside broader cloud stacks, leveraging cross-product synergies to lock in enterprise accounts. Specialist players—FICO, Feedzai, and Sift—push detection accuracy by pairing graph analytics with network-wide behavioral signatures.

M&A momentum intensified through 2024-2025. Worldpay acquired AI-native Ravelin to enrich e-commerce risk scoring pipelines, targeting rapid merchant onboarding and lower chargeback ratios. Chainalysis bought Alterya to inject real-time KYC fraud control into its blockchain monitoring suite, bridging fiat and crypto compliance. Vendor alliances proliferate: Oscilar links with SentiLink, Socure, and Jumio to knit onboarding identity checks with post-login behavioral surveillance, presenting banks with single-API access across the customer life cycle.

Managed-service models gain ground as customers seek turnkey operations and curated threat feeds. Vendors now staff 24/7 SOCs that triage alerts, deliver weekly tuning, and supply executive dashboards summarizing prevented loss. Cloud-first design has become table stakes; laggards still reliant on static rules experience churn toward next-gen competitors. Over the forecast horizon, strategic partnerships and AI-talent acquisitions will remain the primary levers for market-share gains within the fraud detection and prevention market.

Fraud Detection And Prevention (FDP) Industry Leaders

-

SAP SE

-

IBM Corporation

-

SAS Institute Inc.

-

ACI Worldwide Inc.

-

Fiserv Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Worldpay acquired Ravelin to bolster AI-based e-commerce fraud prevention and accelerate merchant growth.

- February 2025: Oscilar partnered with SentiLink to integrate digital-identity scoring with real-time transaction risk management, targeting false-positive reduction.

- January 2025: Chainalysis purchased Alterya, adding proactive fraud protection during KYC and live payments.

- January 2025: LexisNexis Risk Solutions bought IDVerse to fortify defenses against deepfakes via advanced biometric liveness tests.

- December 2024: Oscilar and Jumio announced an alliance marrying AI risk scoring with document verification in digital onboarding.

Global Fraud Detection And Prevention (FDP) Market Report Scope

The fraud detection and prevention market is defined by the revenue generated from the sale of fraud detection and prevention solutions offered by different market players. The market trends are evaluated by analyzing the investment track in fraud solutions.

The fraud detection and prevention market is segmented by solution (fraud analytics, authentication, reporting, visualization, governance, risk, and compliance (GRC) solutions), by scale of end user (small-sale, medium-scale, large-scale), type of fraud (internal, external), end-user industry (BFSI, retail, IT and telecom, healthcare, energy and power, manufacturing, and other end-user industries), and geography (North America, Europe, Asia-Pacific, Latin America, Middle East & Africa). The market size and forecasts are provided in terms of value (USD) for all the above segments.

| Solutions | Fraud Analytics |

| Authentication | |

| Reporting | |

| Visualization | |

| Others | |

| Services |

| Cloud |

| On-premises |

| Small and Medium Enterprises |

| Large Enterprises |

| BFSI |

| Retail and E-commerce |

| IT and Telecom |

| Healthcare |

| Energy and Utilities |

| Manufacturing |

| Government and Public Sector |

| Others |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| By Component | Solutions | Fraud Analytics | |

| Authentication | |||

| Reporting | |||

| Visualization | |||

| Others | |||

| Services | |||

| By Deployment Mode | Cloud | ||

| On-premises | |||

| By Organization Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-user Industry | BFSI | ||

| Retail and E-commerce | |||

| IT and Telecom | |||

| Healthcare | |||

| Energy and Utilities | |||

| Manufacturing | |||

| Government and Public Sector | |||

| Others | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| India | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the fraud detection and prevention market?

The market is valued at USD 58.69 billion in 2025 and is on track to hit USD 146.96 billion by 2030.

Which region is growing the fastest?

Asia-Pacific is projected to grow at a 20.1% CAGR, outpacing all other regions due to rapid mobile payment adoption and new regulatory mandates.

Why are services outpacing solutions in growth?

Organizations face talent shortages and complex threat landscapes, so they turn to managed-security services that provide 24/7 monitoring and expert model tuning, producing a 21.5% CAGR for the services segment.

Which industry leads adoption?

Banking, Financial Services, and Insurance holds the largest share at 32.6% because of direct monetary exposure and stringent compliance obligations.

How are deepfakes affecting fraud prevention strategies?

Generative-AI tools enable voice cloning and synthetic IDs, prompting institutions to deploy liveness detection, multi-factor biometrics, and explainable AI models capable of real-time adaptation.

Page last updated on: