Fluid Power Equipment Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 69.98 Billion |

| Market Size (2030) | USD 87.56 Billion |

| Growth Rate (2025 - 2030) | 4.58% CAGR |

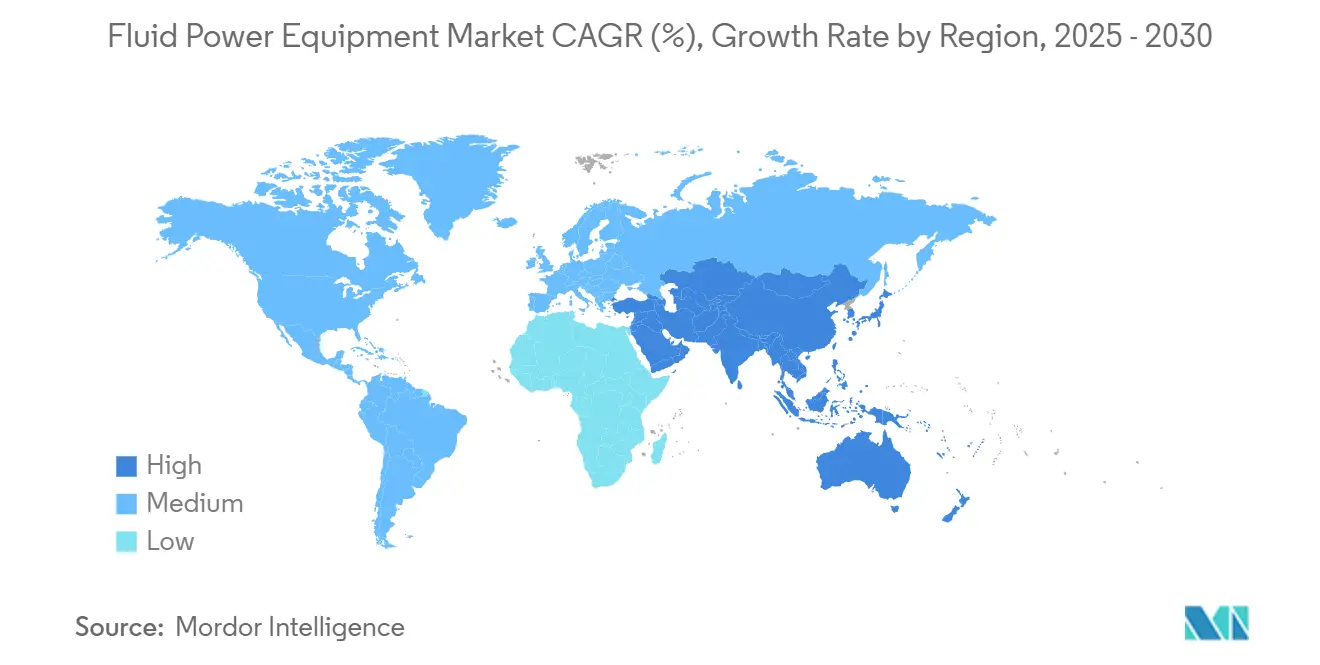

| Fastest Growing Market | Asia Pacific |

| Largest Market | Middle East |

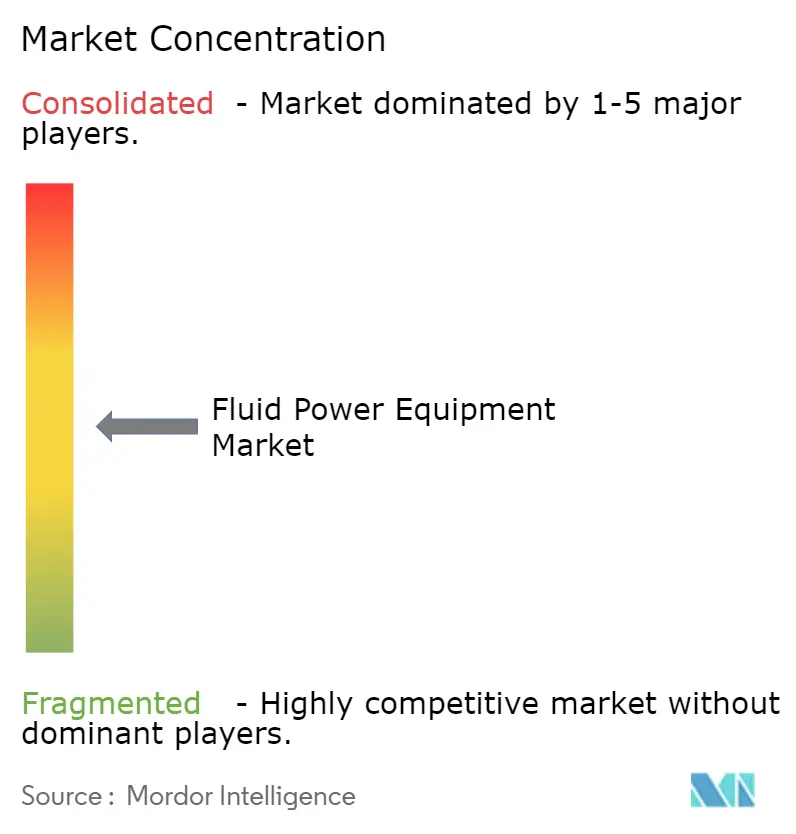

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Fluid Power Equipment Market Analysis by Mordor Intelligence

The fluid power equipment market reached USD 69.98 billion in 2025 and is forecast to expand at a 4.58% CAGR, pushing the fluid power equipment market size to USD 87.56 billion by 2030. This outlook reflects resilient demand from construction, agriculture and smart manufacturing, alongside steady replacement cycles in mature industrial bases. Rising automation, tighter energy‐efficiency norms and broader electrification in off-highway machinery are sustaining component sales. Large vendors are protecting margins through cost discipline, higher value-added digital offerings and selective acquisitions. Meanwhile, aftermarket services are growing faster than original-equipment shipments as users extend asset lifetimes and adopt predictive maintenance.

Key Report Takeaways

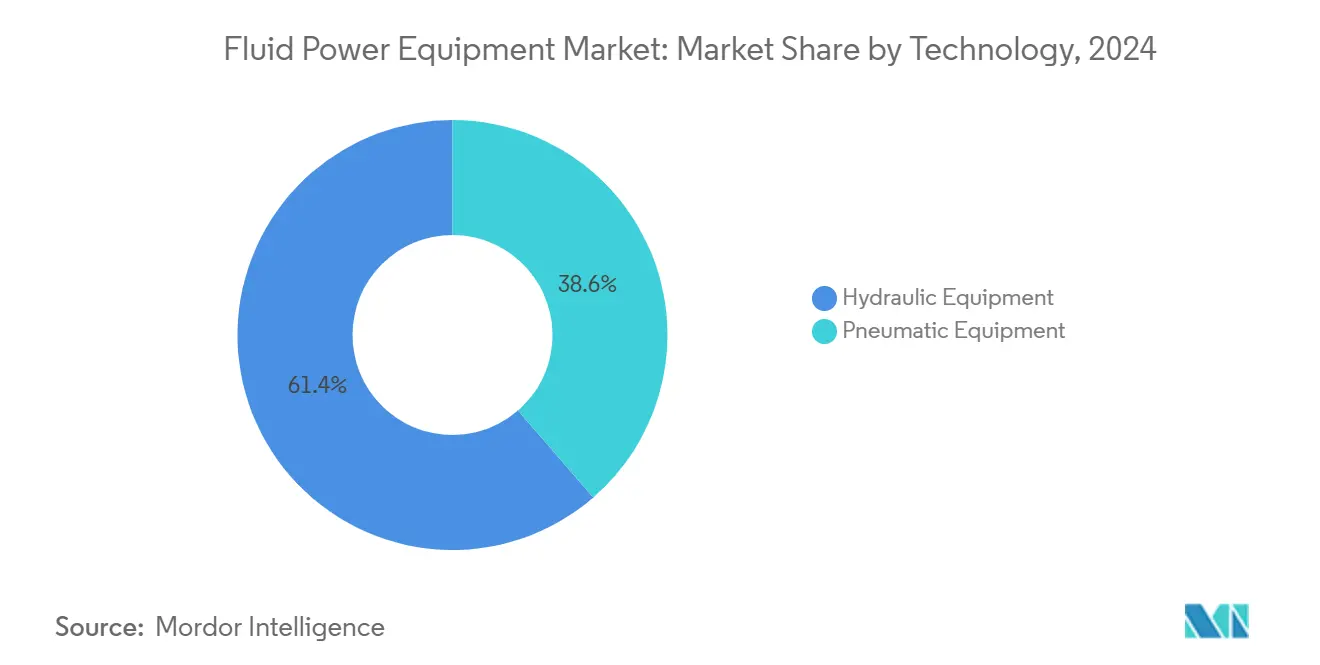

- By technology, hydraulic equipment accounted for 61.37% of 2024 revenue, while pneumatic equipment is projected to post the highest 4.89% CAGR to 2030.

- By product type, pumps led with 27.68% 2024 revenue, whereas accumulators and filters are expected to log a 5.78% CAGR through 2030.

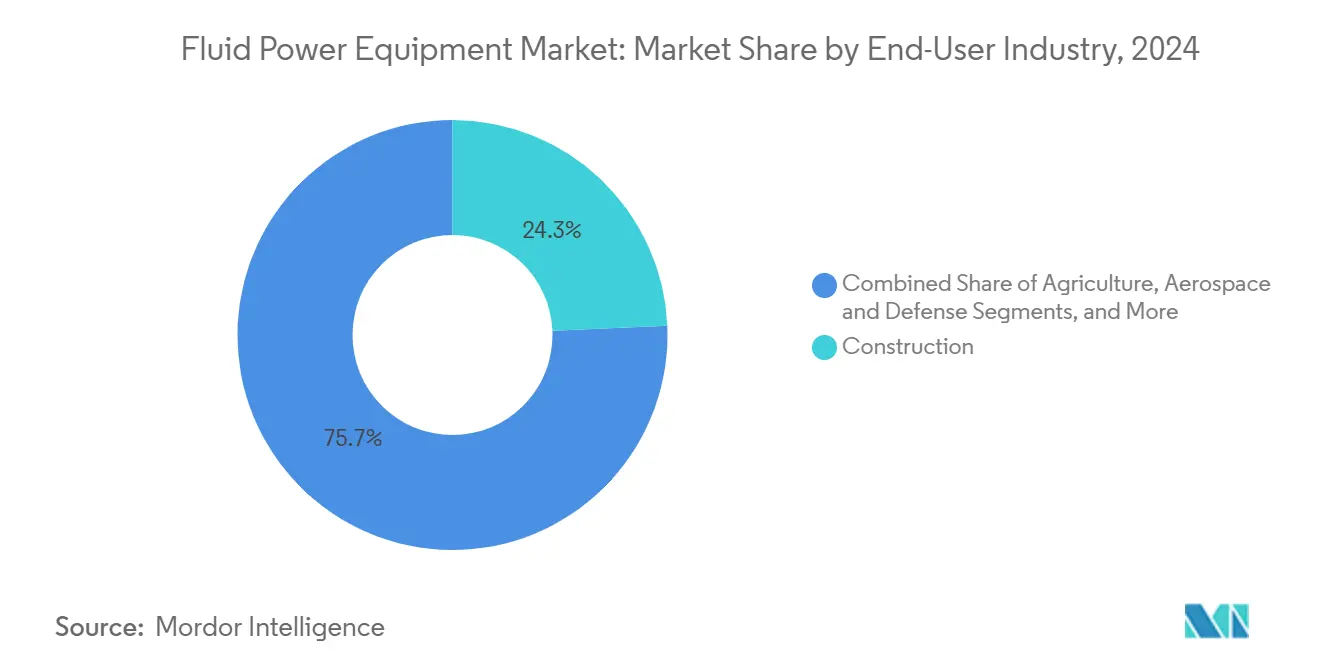

- By end-user industry, construction held 24.32% share in 2024, but agriculture is on track for the fastest 5.56% CAGR to 2030.

- By distribution channel, OEM routes retained 65.73% 2024 share, while the aftermarket is forecast to expand at a 5.87% CAGR.

- By geography, Asia Pacific represented 34.42% 2024 revenue, and the Middle East is anticipated to grow at a 5.71% CAGR to 2030.

Global Fluid Power Equipment Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy efficiency and environmental considerations | +1.2% | Global – early gains in Europe and North America | Medium term (2-4 years) |

| Advances in industrial automation | +1.5% | Asia Pacific core, spill-over to North America and Europe | Short term (≤ 2 years) |

| Technical improvements in sealing and material science | +0.8% | Global | Long term (≥ 4 years) |

| Growing investments in off-highway electrification | +1.0% | North America and EU, expanding to Asia Pacific | Medium term (2-4 years) |

| Rising demand from smart manufacturing facilities | +1.3% | Asia Pacific and North America | Short term (≤ 2 years) |

| Hydrogen-ready pneumatics for clean-room operations | +0.4% | Europe and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Energy Efficiency and Environmental Considerations

Regulations such as CARB Tier 5 and forthcoming EPA 2027 rules are accelerating the adoption of high-efficiency pumps, motors and valves in mobile and stationary equipment.[1]Association of Equipment Manufacturers, “Regulatory Issues,” aem.org Variable-speed drives paired with IE5 synchronous reluctance motors are cutting pump electricity use by up to 60 % in municipal water utilities. Digital hydraulic valves managed through pulse-width modulation are eliminating throttling losses, raising hydrostatic transmission efficiency by 15-36 %. Parker Hannifin aims to lower its operational carbon footprint 50 % by 2030, a target that underpins demand for its energy-optimized components. Combined, these forces lift the fluid power equipment market by driving retrofit and replacement activity across core applications.

Advances in Industrial Automation

Industry 4.0 architectures allow fluid power components to communicate operating parameters in real time, facilitating adaptive control and remote diagnostics. SMC Corporation’s OPC UA-enabled pneumatics cut unscheduled downtime 20-30 % in electronics assembly lines.[2]Qingkai Fan et al., “Review of Research on Hydrostatic Transmission Systems and Control Strategies,” MDPI, pmc.ncbi.nlm.nih.gov Machine-learning algorithms now adjust pump displacement and working pressures dynamically, improving energy utilization by 36 % in hydrostatic transmissions. Hybrid electro-hydraulic actuation is gaining traction in collaborative robots and automated guided vehicles, enlarging addressable demand for the fluid power equipment market.

Technical Improvements in Sealing and Material Science

Ceramic matrix composites and silicon-carbide inserts enable cylinders, pumps and valves to withstand higher pressures and temperatures in renewable energy installations). Thermoplastic composite pipe is lowering total-cost-of-ownership for subsea hydrogen and carbon-capture networks by eliminating corrosion and permitting longer continuous runs). New elastomer compounds paired with micro-textured surfaces slash leakage, a primary cause of energy loss in hydraulic systems, thereby further expanding the fluid power equipment market.

Growing Investments in Off-Highway Electrification

Construction and agricultural OEMs are integrating hybrid hydraulics with onboard battery packs to meet zero-emission job-site mandates. Demonstrations at Bauma 2025 confirmed that energy-recovery circuits using accumulators cut fuel or electricity consumption 15.8 % on slewing motions. Constant-pressure networks replace classic throttle control, trimming total system energy losses up to 60 % on telehandlers. These upgrades translate into escalating demand for advanced pumps, motors and smart valves, lending positive momentum to the fluid power equipment market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyclical capital expenditure in heavy industries | -1.8% | Global, pronounced in North America and Europe | Short term (≤ 2 years) |

| Price volatility of raw materials | -0.9% | Global | Medium term (2-4 years) |

| Leakage-driven energy losses in hydraulic systems | -0.6% | Global | Long term (≥ 4 years) |

| Supply chain fragmentation for precision components | -0.7% | Global, acute in Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyclical Capital Expenditure in Heavy Industries

North American diversified industrial revenue at Parker Hannifin fell 5.8 % organically in Q2 2025 as transportation and off-highway customers delayed new hydraulic equipment orders. Construction machinery OEMs are stretching rebuild cycles amid higher interest rates and uncertain infrastructure outlays, dampening near-term fluid power component uptake. Similar caution is visible in mining and primary metal segments, both large consumers of high-pressure pumps and motors. These swings limit consistent growth for the fluid power equipment market until macro-investment sentiment stabilizes.

Price Volatility of Raw Materials

Steel, copper and specialty alloy prices hold at elevated levels, pushing material inputs to as much as 50 % of finished-component cost in precision manifolds and fittings. Air-Way Manufacturing reports longer lead times and freight surcharges, requiring greater buffer inventories that strain working capital. While large vendors pass on surcharges through index-linked contracts, smaller suppliers struggle to maintain margins, prompting selective price increases and redesigns to reduce metal weight. Material cost uncertainty therefore tempers capacity additions within the fluid power equipment market.

Segment Analysis

By Technology: Hydraulic Equipment Sustains Scale While Pneumatics Outpaces on Growth

Hydraulic solutions accounted for 61.37% of 2024 revenue, underpinning the largest slice of the fluid power equipment market share thanks to unmatched power density in excavators, presses and drilling rigs. Vendors are pairing variable-displacement pumps with digital controllers, improving metering accuracy and lowering fuel burn. Pneumatics, although smaller, is set to register a 4.89% CAGR to 2030 on the strength of lightweight end-effectors in electronics assembly and life-science packaging. The fluid power equipment market size expansion in pneumatics is further supported by smart sensors that transmit cycle counts and leak-rate alerts to edge gateways. Hybrid architectures are also emerging: low-flow pneumatics handles positioning, while hydraulics delivers peak force, creating incremental revenue opportunities across both lines.

Continuous R&D in high-switch-frequency digital valves is narrowing performance gaps between the two technologies. Field tests show discrete-flow hydraulic circuits trimming energy losses 20 % relative to proportional control, an upgrade gaining favor in material-handling forklifts. On the pneumatic side, vacuum-ejector designs with integrated pressure feedback now reduce compressed-air consumption up to 50 %, cutting factory operating costs. Together these advances keep the fluid power equipment market on a modernization trajectory that balances traditional strengths with digital agility.

By Product Type: Pumps Dominate, Accumulators and Filters Advance Fastest

Pumps represented 27.68% of 2024 sales, affirming their role as the heart of every circuit and a cornerstone of the broader fluid power equipment market. Demand spans utility water management, steel mills and forestry harvesters. Electronic pressure compensation, bi-directional telematics and condition-monitoring probes all raise pump bill-of-materials content, enlarging supplier value capture. In contrast, accumulators and filters, while smaller today, are forecast to grow 5.78% annually to 2030. Their surge stems from energy-recovery mandates and stricter contamination codes in semiconductor fabs and food plants, respectively.

Filters are shifting toward high-separation microglass media that deliver lower differential pressure, prolonging element life and reducing motor load. Accumulator designs now incorporate bladder materials rated for 20,000 charge cycles, meeting duty profiles of hybrid cranes and agricultural sprayers. Margins in these categories trend above corporate averages, reinforcing why vendors allocate R&D aimed at total-system optimization and lifecycle monitoring. The mix shift positions the fluid power equipment market size for better profitability even as headline growth remains moderate.

By End-User Industry: Construction Retains Scale, Agriculture Leads Growth Curve

Construction captured 24.32% of 2024 revenue, buoyed by residential high-rise activity in India and highway network upgrades in the United States. Excavators require high-flow pumps and swing motors that generate reliable volume for original-equipment suppliers. Conversely, agriculture is projected to expand 5.56% annually as precision farming proliferates in Brazil, China and Europe. Variable-rate seeders, autonomous tractors and smart irrigation units rely on low-leak hydraulic manifolds and compact pneumatic dosing valves.

Material-handling and logistics continue to adopt automated guided vehicles powered by electro-hydraulic steering actuators, reinforcing demand diversity within the fluid power equipment market. Oil and gas remains material, but decarbonization policies are redirecting capital toward hydrogen, carbon-capture and offshore wind, where specialized fluid power modules manage blade pitch and subsea actuation. Such cross-vertical opportunities cushion the market against cyclical dips in any one sector.

Note: Segment shares of all individual segments available upon report purchase

By Distribution Channel: OEM Networks Command Volume, Aftermarket Accelerates on Services

OEM routes controlled 65.73% of 2024 shipments, underpinned by tight integration between component specifications and machine design. Long-running partnerships help minimize warranty risk and streamline assembly. The aftermarket, though smaller, is on course for a 5.87% CAGR through 2030 as plant operators pursue uptime via predictive maintenance. Cloud ordering portals and AI-driven stocking algorithms enable distributors to ship repair kits within 24 hours, shrinking downtime costs.

Applied Industrial Technologies’ USD 260 million purchase of Hydradyne underscores how service-centric portfolios can capture high-margin retrofit and remanufacturing demand. OEMs are responding by bundling subscription-based monitoring dashboards that alert users to filter clogging or pump cavitation, blurring boundaries between first-fit and replacement sales. These shifts underpin sustained throughput for the fluid power equipment market while lifting average revenue per installed unit.

Geography Analysis

Asia Pacific accounted for a leading 34.42% of 2024 turnover, anchored by China’s electronics clusters, India’s highway build-out and Southeast Asia’s packaging export hubs. Regional governments continue to promote industrial automation grants that favor both hydraulic presses and pneumatic pick-and-place systems, supporting consistent growth in the fluid power equipment market. China’s accelerated shift to electric vehicles is stimulating demand for battery manufacturing conveyors and cooling pumps.[3] International Energy Agency, “Global Overview – Renewables 2024 – Analysis,” iea.org India’s Production-Linked Incentive schemes for mobile phone assembly call for dozens of new clean-room facilities, each equipped with hydrogen-tolerant pneumatic valves, further lifting volumes.

The Middle East is the fastest-growing territory, projected at a 5.71% CAGR through 2030. Saudi Arabia’s Vision 2030 and the UAE’s Operation 300 Bn strategies funnel investment into solar desalination, green hydrogen electrolysers and advanced logistics, all reliant on robust fluid power control. Harsh ambient temperatures demand specialty seals and high-thermal-stability fluids, creating premium niches for global component vendors. Turkey, acting as a bridge to European supply chains, is expanding automotive stamping capacity that employs high-tonnage hydraulic presses, propelling incremental orders.

North America and Europe display slower near-term momentum due to softer capital expenditure, yet they remain vital innovation hubs for the fluid power equipment market. Parker Hannifin’s North American industrial sales slipped, but aerospace aftermarket demand and medical equipment orders offset part of the decline. The European transition to Tier 5 off-road standards is sparking retrofits of hydraulic excavators and agricultural sprayers with low-emission pumps, counterbalancing weaker new-machine builds. These mature regions will likely regain traction once macro uncertainty eases, aided by legislated energy-efficiency upgrades across brownfield factories.

Competitive Landscape

The fluid power equipment market exhibits moderate concentration, with the top five suppliers controlling roughly 45 % of global revenue. Parker Hannifin, Bosch Rexroth and Danfoss leverage vertical integration, global service footprints and digital control platforms to retain share. Bosch Rexroth’s January 2025 purchase of HydraForce adds cartridge valve depth and broadens mobile hydraulics coverage.[4]Bosch Rexroth, “HydraForce Acquisition,” boschrexroth.com Parker improved segment operating margins to 25.6 % in fiscal Q2 2025 through continuous-improvement programs and cost synergies from past acquisitions.

Secondary consolidators focus on value-added distribution and niche technology. Applied Industrial Technologies expanded its hydraulics MRO footprint via Hydradyne, positioning for subscription-based condition monitoring. Ingersoll Rand spent USD 47 million on Lead Fluid and Termomeccanica Industrial Compressor to secure life-science and renewable-gas opportunities. Such bolt-ons provide access to fast-growing adjacencies and cross-sell potential without major integration risk.

White-space competition is mounting from startups offering machine-learning-driven digital valves and compact hydraulic transformers that reclaim braking energy in mobile machinery. Established players respond with open-protocol software, cloud diagnostic portals and service-as-a-subscription programs. The resulting technology race should push overall performance benchmarks higher, supporting replacement demand and enlarging total addressable value for the fluid power equipment market.

Fluid Power Equipment Industry Leaders

-

Bosch Rexroth AG

-

Parker-Hannifin Corporation

-

Danfoss A/S

-

SMC Corporation

-

Eaton Corporation plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Enerpac Tool Group posted 5.1 % organic sales growth in Q2 FY2025 on strong hydraulic tools demand.

- February 2025: IDEX Corporation recorded a 31.6 % adjusted EBITDA margin in its Fluid and Metering Technologies segment despite flat sales.

- January 2025: DXP Enterprises completed seven acquisitions in FY2024, lifting total sales to USD 1.802 billion.

- January 2025: Bosch Rexroth completed the acquisition of HydraForce Inc., expanding cartridge valve and mobile hydraulics capabilities.

Global Fluid Power Equipment Market Report Scope

Fluid power is a term describing hydraulics and pneumatics technologies. Fluid Power Equipment comprises equipment that uses a fluid (liquid or gas) to transmit power from one location to another. The fluid is a liquid (usually oil) with hydraulics, whereas pneumatics uses gas (usually compressed air).

For both the hydraulic and pneumatic categories, the study only considers revenue accrued from the sales of equipment used in the production of end products. It does not reflect the revenues of finished goods.

The fluid power equipment market in which hydraulic equipment market is segmented by product type (pumps, motors, valves, cylinders, accumulators & filters), end-user vertical (construction, agriculture, material handling, oil and gas, aerospace and defense, machine tools, hydraulic tools) and geography (North America, Europe, Asia-Pacific, rest of the World). The pneumatic equipment market is segmented by product type (valves, actuators, FRLs, fittings), end-user vertical (food processing and packaging, automotive, material handling and assembly, chemicals/plastics/oil, semiconductor, and electronics, metalworking, paper and printing, life sciences) and geography (North America, Europe, Asia-Pacific, rest of the World). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Hydraulic Equipment |

| Pneumatic Equipment |

| Pumps |

| Motors |

| Valves |

| Cylinders |

| Accumulators and Filters |

| Construction |

| Agriculture |

| Material Handling and Logistics |

| Oil and Gas |

| Aerospace and Defense |

| Machine Tools |

| Food Processing and Packaging |

| Other End-User Industries |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Southeast Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Technology | Hydraulic Equipment | |

| Pneumatic Equipment | ||

| By Product Type | Pumps | |

| Motors | ||

| Valves | ||

| Cylinders | ||

| Accumulators and Filters | ||

| By End-User Industry | Construction | |

| Agriculture | ||

| Material Handling and Logistics | ||

| Oil and Gas | ||

| Aerospace and Defense | ||

| Machine Tools | ||

| Food Processing and Packaging | ||

| Other End-User Industries | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Southeast Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the fluid power equipment market in 2025?

It stood at USD 69.98 billion in 2025 and is projected to reach USD 87.56 billion by 2030.

What is the expected CAGR for the fluid power equipment market to 2030?

The forecast compound annual growth rate is 4.58 % over the 2025-2030 period.

Which technology commands the largest share of revenue?

Hydraulic equipment led with 61.37 % of 2024 sales thanks to unrivaled power density.

Which end-user segment is forecast to grow the fastest?

Agriculture is projected to expand at a 5.56 % CAGR as precision farming gains traction.

Which region is the fastest-growing market?

The Middle East is expected to post a 5.71 % CAGR through 2030, led by renewable energy projects.

Who are the leading suppliers in the fluid power equipment market?

Parker Hannifin, Bosch Rexroth and Danfoss head the market, collectively holding a mid-20 % share.

Page last updated on: