| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 6.03 Billion |

| Market Size (2030) | USD 8.23 Billion |

| CAGR (2025 - 2030) | 6.41 % |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Flow Control Market Analysis

The Flow Control Market In The Semiconductor Industry is expected to grow from USD 6.03 billion in 2025 to USD 8.23 billion by 2030, at a CAGR of 6.41% during the forecast period (2025-2030).

The semiconductor industry continues to demonstrate robust growth and technological advancement, as evidenced by the Semiconductor Industry Association (SIA) reporting global semiconductor sales reaching USD 580.13 billion in 2022, marking a 4.4% increase from the previous year. This growth trajectory has sparked unprecedented levels of investment in semiconductor manufacturing equipment, with major industry players expanding their production footprint through new fabrication facilities. The industry's evolution is particularly notable in the development of advanced process technologies for artificial intelligence, quantum computing, and sophisticated wireless networks like 5G, driving the need for more precise and efficient semiconductor process control solutions.

The landscape of semiconductor manufacturing is undergoing a significant transformation with major corporations making substantial investments in new production facilities. Intel's announcement of investing over USD 20 billion in two new fabs in Arizona represents a strategic move to enhance domestic semiconductor manufacturing capabilities. Similarly, TSMC's USD 12 billion investment in its Arizona plant, designed to produce 5-nanometer chips by 2024, demonstrates the industry's commitment to expanding advanced manufacturing capabilities. These investments are driving the demand for sophisticated semiconductor process equipment capable of handling increasingly complex manufacturing processes.

The industry is witnessing a geographical diversification of manufacturing capabilities, with several regions developing their semiconductor ecosystems. Samsung's USD 17 billion investment in a new semiconductor manufacturing facility in Texas marks a significant step in expanding the global manufacturing footprint. This trend is complemented by the European Union's initiatives to establish advanced semiconductor manufacturing capabilities, aiming to produce chips with features smaller than 10 nanometers and eventually reaching 2-nanometer technology. These developments are creating new opportunities for semiconductor manufacturing equipment market players to serve diverse market needs.

The technological complexity of semiconductor manufacturing processes continues to evolve, particularly in areas such as plasma etch, chemical vapor deposition (CVD), and atomic layer deposition. These processes require precise control of multiple gas flows, where even minimal deviations can result in process failures. The industry's push toward smaller node sizes and more sophisticated chip designs is driving the development of more advanced semiconductor process control solutions. This trend is particularly evident in the growing adoption of ultra-pure engineered-plastic chemical valves and specialized flow control equipment designed to maintain the stringent cleanliness requirements of semiconductor manufacturing environments.

Flow Control Market Trends

Growing Electronics Industry Driven by IIoT Digitalization

The rapid advancement of the Industrial Internet of Things (IIoT) and widespread digitalization across industries have emerged as significant drivers for the flow control market in the semiconductor industry. The increasing adoption of IIoT technologies has created unprecedented demand for sophisticated semiconductor components, with global semiconductor sales reaching USD 580.13 billion in 2022, marking a 4.4% year-over-year growth according to SIA and WSTS data. This surge in demand is further amplified by the growing integration of advanced technologies like artificial intelligence (AI), machine learning (ML), and IoT applications across various industrial sectors, necessitating more complex and capable semiconductor solutions that require precise control systems for semiconductor processes during manufacturing.

The semiconductor industry has witnessed substantial investments in manufacturing capabilities to meet this growing demand, particularly exemplified by the United States' CHIPS and Science Act of 2022, which allocated USD 52.7 billion to boost domestic semiconductor production and research. This comprehensive initiative includes USD 39 billion for manufacturing incentives, USD 13.2 billion for R&D and workforce development, and USD 500 million for semiconductor supply chain activities. Major manufacturers have responded with significant facility expansions, such as TSMC increasing its investment in Arizona-based factories from USD 12 billion to USD 40 billion. These expansions require sophisticated flow control systems, including advanced vacuum pumps, valves, and mechanical seals, to maintain the ultra-pure manufacturing environments essential for modern equipment used in semiconductor manufacturing.

The integration of IIoT in manufacturing processes has created a self-reinforcing cycle where increased digitalization drives demand for more sophisticated semiconductor components, which in turn enables further industrial automation and IIoT adoption. This trend is evidenced by the growing implementation of smart manufacturing solutions, automated process control systems, and connected devices across industries. The demand for high-performance processors used in data centers, 5G infrastructure, and emerging technologies has prompted logic chip manufacturers and foundries to invest heavily in expanding production capacity for cutting-edge technology, particularly in advanced nodes like 5nm and 7nm, which require increasingly sophisticated equipment for semiconductor processes and control systems for semiconductor processes in their manufacturing processes.

Understand The Key Trends Shaping This Market

Download PDF

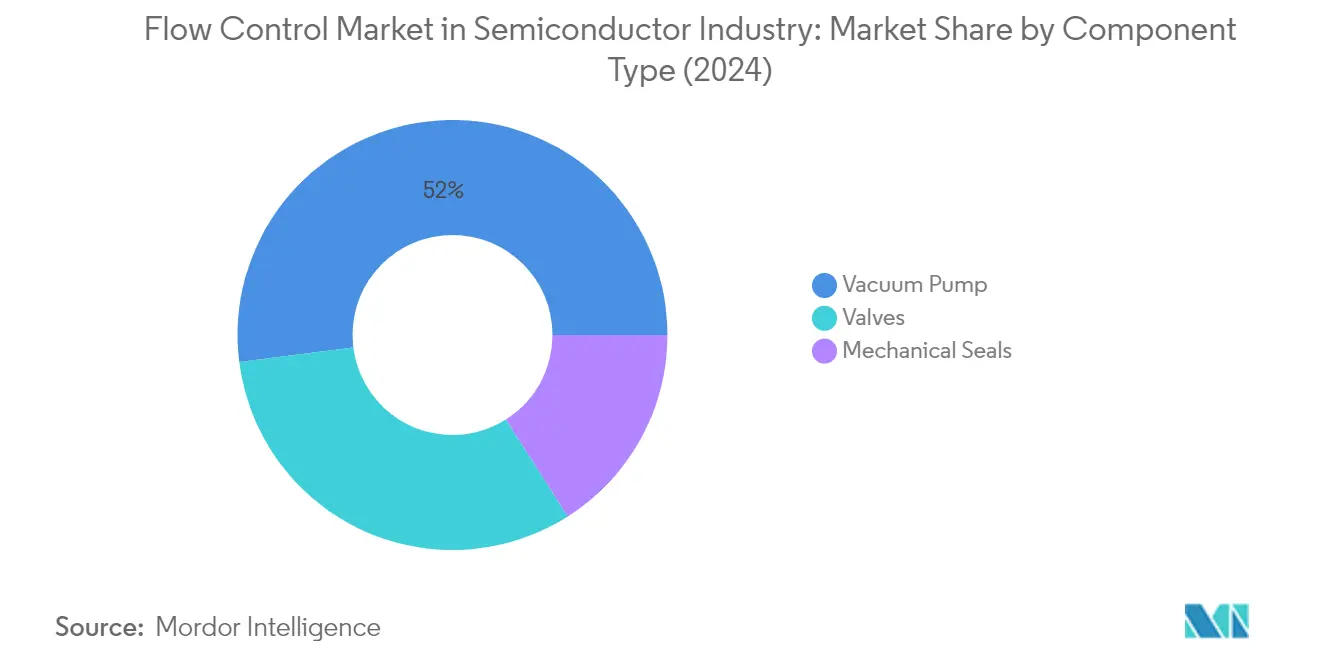

Segment Analysis: By Type of Component

Vacuum Pump Segment in Flow Control Market for Semiconductor Industry

The Vacuum Pump segment dominates the flow control market in the semiconductor industry, holding approximately 52% of the market share in 2024. This significant market position is attributed to the critical role of vacuum pumps in semiconductor process control, where they are essential for creating and maintaining the ultra-clean, low-pressure environments required for wafer processing. Vacuum pumps are extensively used across various applications, including physical vapor deposition, chemical vapor deposition, etching, and ion implantation processes. The segment's dominance is further strengthened by the increasing demand for advanced semiconductor manufacturing equipment that requires more sophisticated vacuum systems, particularly in applications such as atomic layer deposition and plasma processing.

Mechanical Seals Segment in Flow Control Market for Semiconductor Industry

The Mechanical Seals segment is emerging as the fastest-growing segment in the semiconductor industry's flow control market, with a projected growth rate of approximately 7% from 2024 to 2029. This accelerated growth is driven by the increasing emphasis on contamination control and reliability in semiconductor manufacturing processes. The segment's growth is further supported by technological advancements in seal materials and designs, particularly in developing seals that can withstand harsh chemical environments and extreme temperatures. The rising adoption of mechanical seals in critical semiconductor applications, including chemical filtration, chemical transfer, and silicon wafer fabrication, is contributing to this segment's rapid expansion.

Remaining Segments in Flow Control Market by Type of Component

The Valves segment represents a crucial component of the flow control market in the semiconductor industry, playing a vital role in controlling the flow of various gases and chemicals used in semiconductor process equipment. This segment encompasses various valve types, including ball, butterfly, gate, and globe valves, each serving specific applications in chemical supply, wafer manufacturing, and water treatment processes. The segment's significance is underscored by the growing demand for high-purity valves that can maintain the stringent cleanliness requirements of semiconductor manufacturing while providing precise flow control capabilities.

Flow Control Market In The Semiconductor Industry Geography Segment Analysis

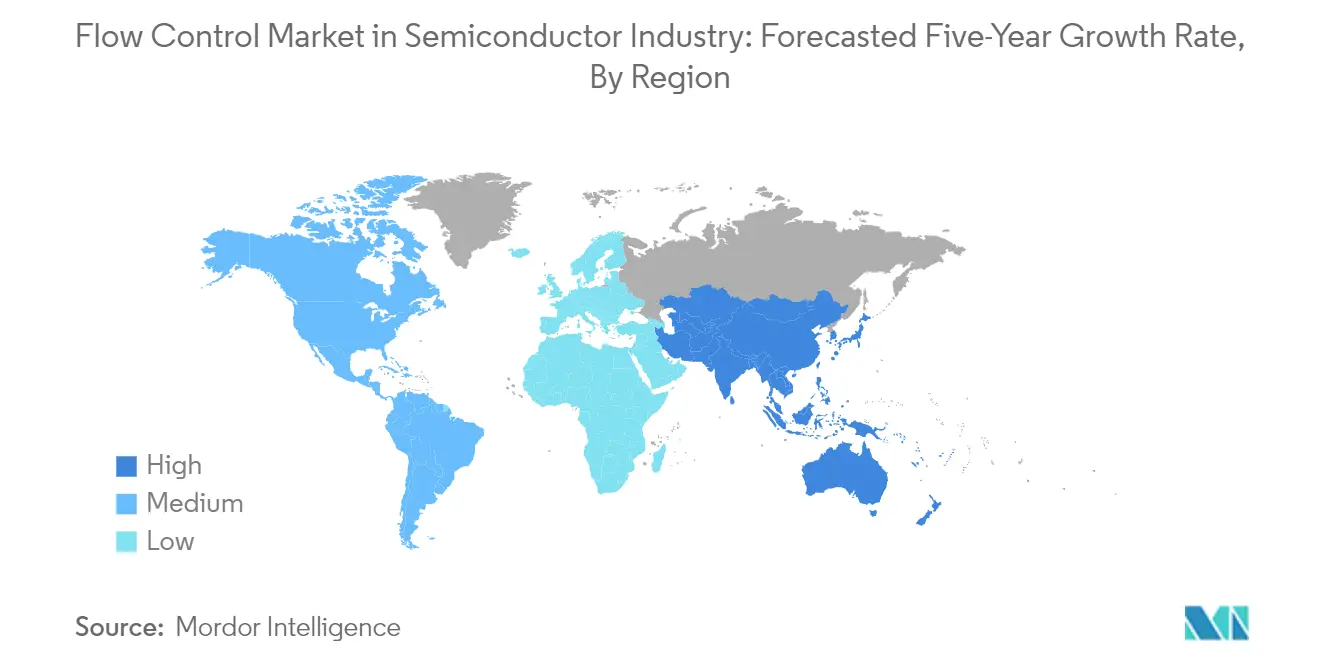

Flow Control Market in the Semiconductor Industry in China

China has established itself as the dominant force in the global semiconductor flow control market, commanding approximately 28% of the market share in 2024. The country's semiconductor industry is experiencing unprecedented growth, projected to expand at nearly 8% annually from 2024 to 2029. This remarkable growth is largely attributed to the country's ambitious semiconductor agenda, supported by substantial government initiatives and investments in domestic IC manufacturing capabilities. The country's focus on developing advanced manufacturing facilities and expanding production capacities has attracted numerous global players to establish their presence in the region. The emphasis on technological self-reliance and the development of domestic semiconductor manufacturing capabilities has led to significant investments in semiconductor manufacturing equipment, including vacuum pumps, valves, and mechanical seals. The growing adoption of advanced semiconductor manufacturing processes and the increasing demand for high-performance chips have further accelerated the need for sophisticated flow control solutions in the country's semiconductor facilities.

Flow Control Market in the Semiconductor Industry in Taiwan

Taiwan continues to maintain its position as a crucial hub in the global semiconductor flow control market, driven by the presence of major semiconductor manufacturers and foundries. The country's semiconductor ecosystem is characterized by a robust supply chain and advanced manufacturing capabilities, particularly in the production of high-performance chips. Taiwan's strength lies in its well-established semiconductor manufacturing infrastructure, supported by significant investments in research and development. The presence of leading semiconductor companies and their continuous focus on expanding production capacities has created substantial demand for advanced flow control solutions. The country's emphasis on developing next-generation semiconductor technologies and maintaining its competitive edge in the global market has led to increased adoption of sophisticated semiconductor process equipment. Taiwan's commitment to maintaining high manufacturing standards and clean room requirements has also driven the demand for high-quality vacuum pumps, valves, and mechanical seals in semiconductor manufacturing processes.

Flow Control Market in the Semiconductor Industry in South Korea

South Korea has emerged as a powerhouse in the semiconductor flow control market, supported by the presence of major memory chip manufacturers and significant government support. The country's semiconductor industry is characterized by its focus on technological innovation and continuous advancement in manufacturing processes. South Korea's strength in memory chip production has created substantial demand for specialized flow control equipment, particularly in advanced manufacturing processes. The country's commitment to maintaining its competitive position in the global semiconductor market has led to significant investments in manufacturing capabilities and advanced technologies. The presence of major semiconductor manufacturers and their focus on expanding production capacities has driven the demand for high-performance flow control solutions. South Korean manufacturers' emphasis on automation and smart manufacturing has further accelerated the adoption of advanced semiconductor manufacturing equipment in semiconductor manufacturing processes.

Flow Control Market in the Semiconductor Industry in Other Countries

The semiconductor flow control market maintains a significant presence across various other regions, including the United States, Japan, and European countries. These regions are characterized by their focus on specialized semiconductor manufacturing and research and development activities. The United States, with its emphasis on advanced chip design and manufacturing, continues to drive innovation in flow control technologies. Japan's semiconductor industry, known for its high-precision manufacturing capabilities, maintains a steady demand for sophisticated flow control solutions. European countries are increasingly focusing on developing their semiconductor manufacturing capabilities, supported by various government initiatives and investments. These regions collectively contribute to the advancement of flow control technologies in semiconductor manufacturing, with each market displaying unique characteristics and requirements based on their specific manufacturing focus and technological capabilities.

Get Analysis on Important Geographic Markets

Download PDF

Flow Control Industry Overview

Top Companies in Flow Control Market in Semiconductor Industry

The leading companies in the flow control semiconductor market demonstrate a strong focus on technological advancement and product innovation, particularly in developing high-performance vacuum pumps, precision valves, and specialized mechanical seals. These organizations are investing substantially in research and development to create solutions that meet the increasingly complex demands of semiconductor manufacturing equipment processes. Companies are pursuing strategic acquisitions and partnerships to expand their geographical presence and strengthen their product portfolios, particularly in key semiconductor manufacturing hubs across Asia, Europe, and North America. Operational agility is evidenced through the establishment of localized manufacturing facilities, robust distribution networks, and enhanced after-sales support services. The market leaders are also emphasizing sustainability initiatives and energy-efficient solutions while maintaining strong quality certifications and compliance with semiconductor industry standards.

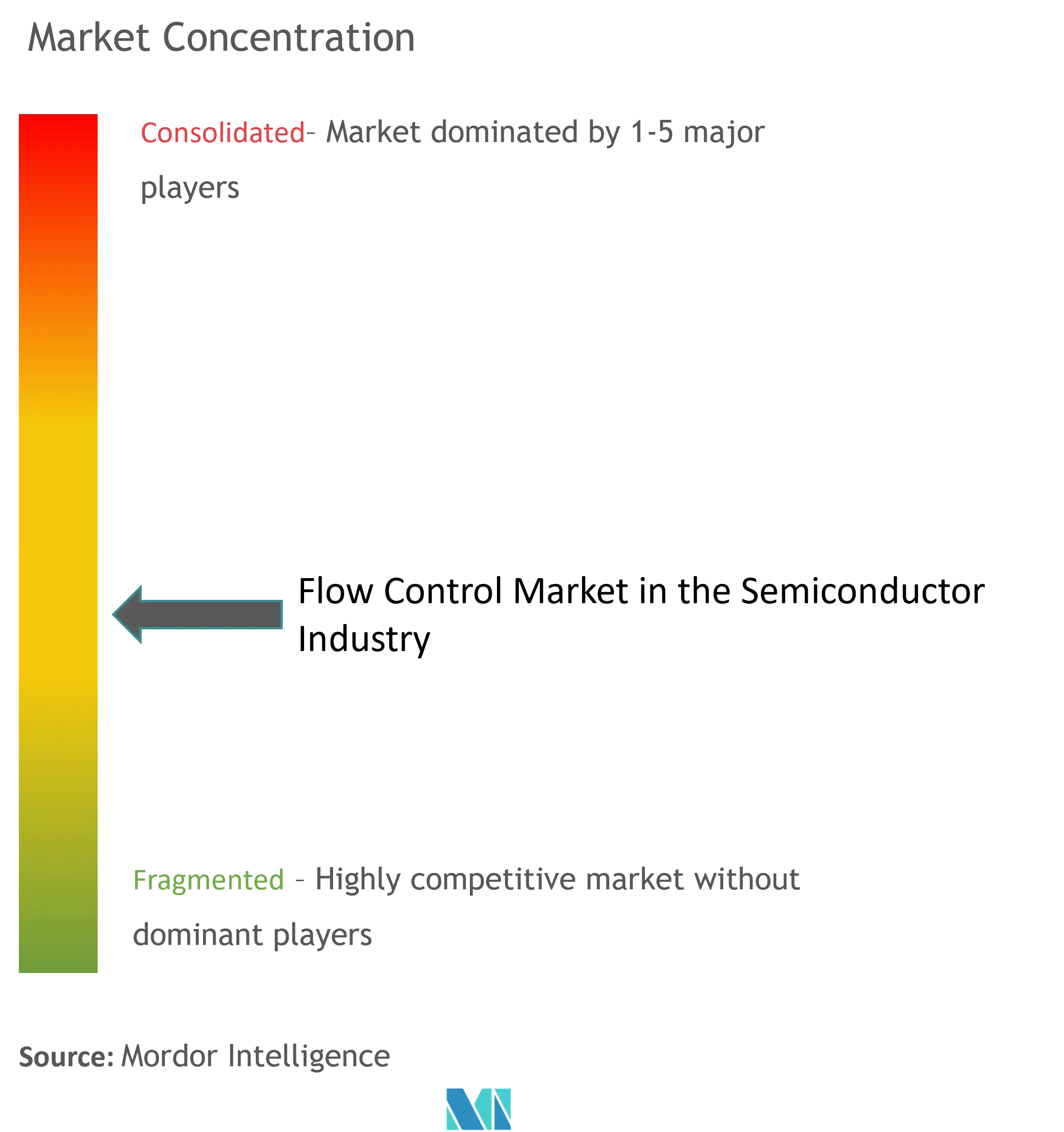

Consolidated Market with Strong Regional Players

The flow control market in the semiconductor industry exhibits a moderately consolidated structure, characterized by the presence of both global conglomerates and specialized regional manufacturers. Global players leverage their extensive research capabilities, established brand reputation, and comprehensive product portfolios to maintain market leadership, while regional specialists excel through their deep understanding of local market requirements and ability to provide customized solutions. The market demonstrates active merger and acquisition activity, with larger companies acquiring specialized manufacturers to enhance their technological capabilities and expand their market reach.

The competitive dynamics are shaped by the presence of diversified industrial groups that offer complete flow control solutions alongside specialized manufacturers focusing on specific product categories such as vacuum pumps, valves, or mechanical seals. Market consolidation is particularly evident in mature markets, where established players are strengthening their positions through vertical integration and strategic partnerships. The industry also witnesses collaboration between flow control equipment manufacturers and semiconductor companies to develop application-specific solutions, creating high entry barriers for new entrants.

Innovation and Customization Drive Market Success

Success in the flow control semiconductor market increasingly depends on companies' ability to provide innovative, highly specialized solutions that address the evolving needs of semiconductor manufacturers. Incumbent companies are focusing on developing advanced materials, improving product performance, and integrating smart technologies to maintain their competitive edge. The ability to offer comprehensive support services, including technical consultation, maintenance, and rapid response to customer requirements, has become crucial for market success. Companies are also investing in digital capabilities and automation solutions to enhance their operational efficiency and customer service delivery.

Market contenders are gaining ground by focusing on niche applications, developing cost-effective alternatives, and establishing strong relationships with regional semiconductor manufacturers. The industry's future competitive landscape will be shaped by factors such as technological advancement in semiconductor process control, increasing demand for energy-efficient solutions, and growing emphasis on supply chain resilience. Companies that can effectively balance product innovation, operational efficiency, and customer service while maintaining competitive pricing structures are likely to succeed in this evolving market environment. The ability to adapt to regulatory changes, particularly regarding environmental standards and safety requirements, will also play a crucial role in determining market success.

Flow Control Market Leaders

-

Pfeiffer Vacuum GmbH

-

Atlas Copco AB

-

Gardner Denver (Ingersoll Rand Inc.)

-

Flowserve Corporation

-

Busch Holding GmbH

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Flow Control Market News

- June 2024: The construction commenced of Edwards Vacuum's dry pump manufacturing facility in Alabama, New York. The company, which manufactures vacuum and abatement equipment for the semiconductor industry, announced plans to invest USD 319 million into the project, with USD 127 million spent on phase one. Edwards Vacuum's 240,000 sq. ft campus would feature manufacturing, warehouse, and administration facilities to expand its production capacity, increase supply, and diversify its production locations.

- February 2024: KITZ Corporation announced plans to establish a new factory building on the premises of its Vietnamese subsidiary, KITZ Corporation of Vietnam Co. Ltd (KCV), to produce high-purity gas-compatible valves for the semiconductor equipment market, supported by the increasing demand in this market. The company plans to establish a new factory building at its Vietnamese plant to expand production capacity, ensure stable supply, and diversify its production locations.

Flow Control Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET INSIGHTS

- 4.1 Market Overview

-

4.2 Industry Analysis - Porter's Five Forces Analysis

- 4.2.1 Bargaining Power of Suppliers

- 4.2.2 Bargaining Power of Buyers

- 4.2.3 Threat of New Entrants

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Assessment of the Impact of COVID-19 on the Market

5. MARKET DYNAMICS

-

5.1 Market Drivers

- 5.1.1 Growth in Electronics Industry Driven by IIoT Digitalization

-

5.2 Market Challenges

- 5.2.1 Increasing Market Consolidation Expected to Create Stiff Competition

6. MAJOR APPLICATIONS OF VACUUM PUMPS AND VALVES IN THE SEMICONDUCTOR INDUSTRY

-

6.1 Vacuum Pumps

- 6.1.1 Physical Vapor Deposition/Sputtering

- 6.1.2 Chemical Vapor Deposition (Plasma/Sub-atmospheric)

- 6.1.3 Diffusion/Low Pressure Chemical Vapor Deposition (LPCVD)

- 6.1.4 Atomic Layer Deposition

- 6.1.5 Dry Stripping and Cleaning

- 6.1.6 Dielectric Etch

- 6.1.7 Conductor and Polysilicon Etch

- 6.1.8 Atomic Layer Etching

- 6.1.9 Ion Implantation

- 6.1.10 Load Lock and Transfer

- 6.1.11 Critical Dimension Scanning Electron Microscope

- 6.1.12 Particle Monitoring in Front Opening Universal Pods

- 6.1.13 Airborne Molecular Contamination

-

6.2 Valves

- 6.2.1 Chemical Supply

- 6.2.2 Polysilicon Process

- 6.2.3 Wafer Manufacturing

- 6.2.4 Chemical Manufacturing

- 6.2.5 Slurry Supply

- 6.2.6 Solvent Supply

- 6.2.7 Water Treatment

- 6.2.8 Lithography

- 6.2.9 Etching

- 6.2.10 CMP

- 6.2.11 Chemical and Slurry Recovery

7. MARKET SEGMENTATION

-

7.1 Type of Component

- 7.1.1 Vacuum

- 7.1.2 Valves

- 7.1.2.1 Ball

- 7.1.2.2 Butterfly

- 7.1.2.3 Gate

- 7.1.2.4 Globe

- 7.1.2.5 Other Valves

- 7.1.3 Mechanical Seals

-

7.2 By Country

- 7.2.1 United States

- 7.2.2 China

- 7.2.3 Taiwan

- 7.2.4 South Korea

- 7.2.5 Japan

- 7.2.6 Rest of the World

8. COMPETITIVE LANDSCAPE

-

8.1 Company Profiles - Vacuum Pumps*

- 8.1.1 Pfeiffer Vacuum GmbH

- 8.1.2 Atlas Copco AB

- 8.1.3 Gardner Denver (ingersoll Rand Inc.)

- 8.1.4 Flowserve Corporation

- 8.1.5 Busch Holding Gmbh

- 8.1.6 Kurt J. Lesker Company

-

8.2 Company Profiles - Valves*

- 8.2.1 Fujikin Incorporation

- 8.2.2 GEMÜ Holding GmbH & Co.KG

- 8.2.3 VAT Vakuumventile AG

- 8.2.4 Swagelok Company

- 8.2.5 Festo SE & Co. KG

- 8.2.6 GCE Group

-

8.3 Company Profiles - Mechanical Seals*

- 8.3.1 DuPont De Nemours Inc.

- 8.3.2 EKK Eagle SC Inc.

- 8.3.3 EnPro Industries Inc.

- 8.3.4 Freudenberg Group

- 8.3.5 AESSEAL PLC

- 8.3.6 Parker-Hannifin Corporation

- 8.3.7 Greene, Tweed & Co. Inc.

9. INVESTMENT AND FUTURE OUTLOOK

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Flow Control Industry Segmentation

Flow controllers are electronic devices that monitor and maintain flow rate variables in process applications. They can be utilized in fluid flow systems with pumps and valves to enable greater control of flow variables. Dry vacuum pumps are essential in the semiconductor manufacturing process. Gases are injected into a chamber to react and produce a layer on the surface of a silicon wafer. The pump's job is to maintain a constant low pressure in the chamber to aid in forming the film.

The global flow control market in the semiconductor industry is segmented by type of component (vacuum, valves (ball, butterfly, gate, globe, and other valves), and mechanical seals) and country. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Type of Component | Vacuum | ||

| Valves | Ball | ||

| Butterfly | |||

| Gate | |||

| Globe | |||

| Other Valves | |||

| Mechanical Seals | |||

| By Country | United States | ||

| China | |||

| Taiwan | |||

| South Korea | |||

| Japan | |||

| Rest of the World | |||

Need A Different Region or Segment?

Customize Now

Flow Control Market Research FAQs

How big is the Flow Control Market In The Semiconductor Industry?

The Flow Control Market In The Semiconductor Industry size is expected to reach USD 6.03 billion in 2025 and grow at a CAGR of 6.41% to reach USD 8.23 billion by 2030.

What is the current Flow Control Market In The Semiconductor Industry size?

In 2025, the Flow Control Market In The Semiconductor Industry size is expected to reach USD 6.03 billion.

Who are the key players in Flow Control Market In The Semiconductor Industry?

Pfeiffer Vacuum GmbH, Atlas Copco AB, Gardner Denver (Ingersoll Rand Inc.), Flowserve Corporation and Busch Holding GmbH are the major companies operating in the Flow Control Market In The Semiconductor Industry.

Which is the fastest growing region in Flow Control Market In The Semiconductor Industry?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Flow Control Market In The Semiconductor Industry?

In 2025, the North America accounts for the largest market share in Flow Control Market In The Semiconductor Industry.

What years does this Flow Control Market In The Semiconductor Industry cover, and what was the market size in 2024?

In 2024, the Flow Control Market In The Semiconductor Industry size was estimated at USD 5.64 billion. The report covers the Flow Control Market In The Semiconductor Industry historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Flow Control Market In The Semiconductor Industry size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Flow Control Market In The Semiconductor Industry Research

Mordor Intelligence offers a comprehensive analysis of the semiconductor manufacturing equipment industry, drawing on our extensive experience in technology sector research. Our detailed report, available as an easy-to-download PDF, provides in-depth insights into developments in semiconductor process equipment and emerging technologies. The analysis covers crucial aspects of semiconductor process control systems, offering stakeholders a thorough understanding of market dynamics and technological advancements.

Our extensive research spans the entire spectrum of the semiconductor manufacturing equipment market. It includes a detailed analysis of key industry trends, technological innovations, and regulatory frameworks. The report provides valuable insights for manufacturers, suppliers, and investors involved in the development and implementation of semiconductor process equipment. Stakeholders benefit from our detailed examination of semiconductor process control technologies, enabling informed decision-making and strategic planning in this rapidly evolving industry. The comprehensive report PDF can be downloaded for immediate access to these crucial insights.