Fitness Rings Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

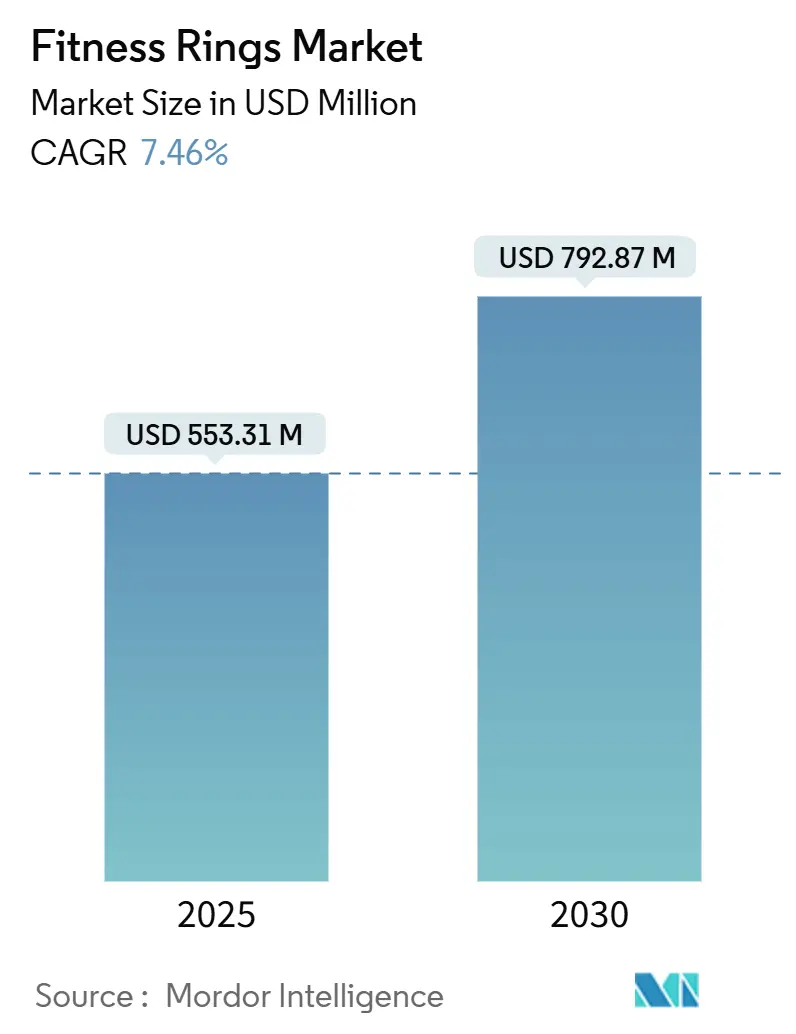

| Market Size (2025) | USD 553.31 Million |

| Market Size (2030) | USD 792.87 Million |

| Growth Rate (2025 - 2030) | 7.46% CAGR |

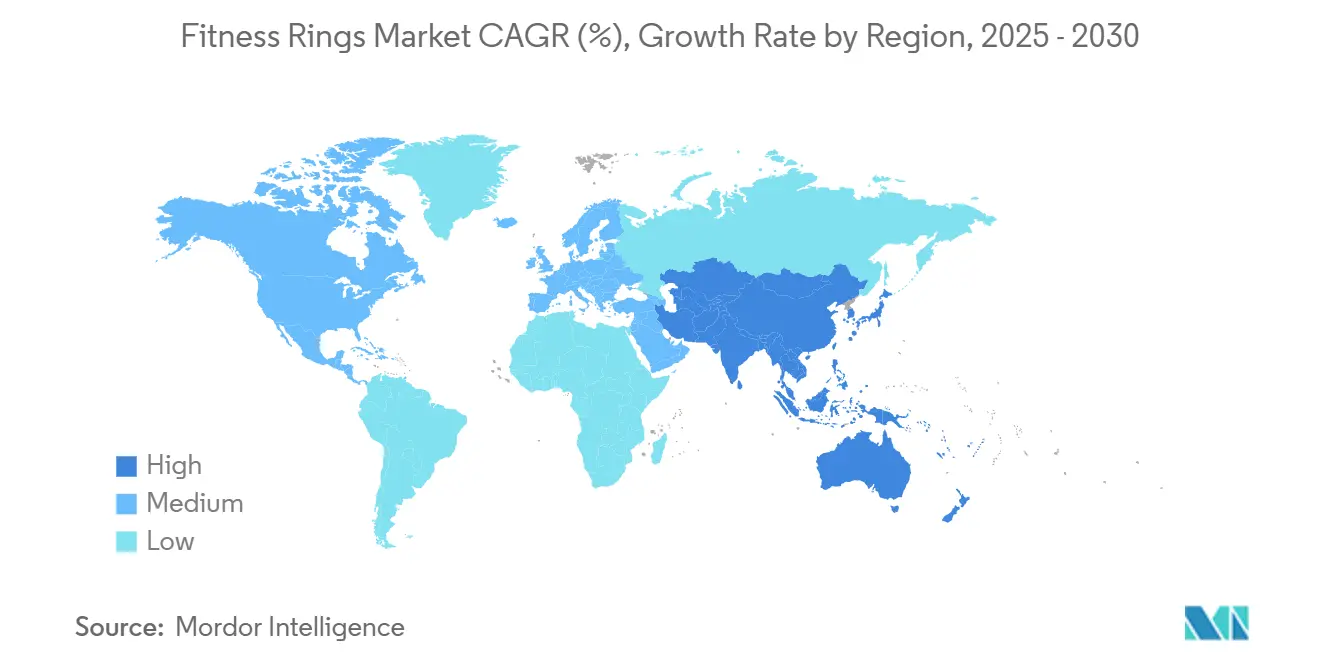

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

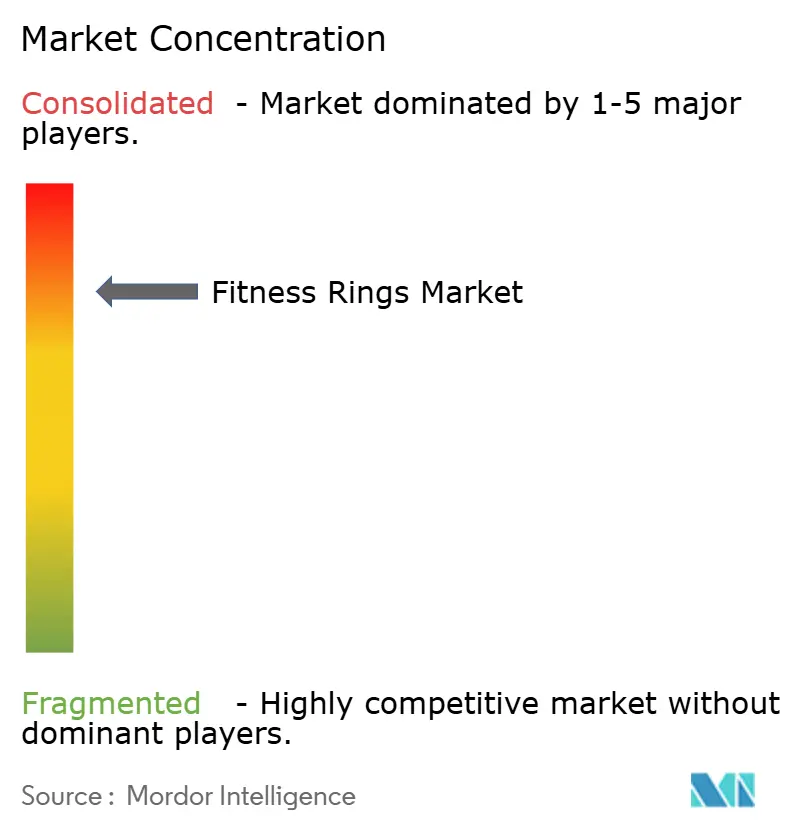

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Fitness Rings Market Analysis by Mordor Intelligence

The fitness rings market size is USD 553.31 million in 2025 and is projected to reach USD 792.87 million in 2030, advancing at a 7.46% CAGR. Rapid sensor miniaturization, the widening adoption of corporate wellness, and entry by major consumer electronics brands are redefining form factor expectations in wearables. Vendors that combine high-accuracy biometrics, AI-generated guidance, and seamless ecosystem integration are capturing premium price points, while ultra-low-cost Chinese models expand the reachable customer base. Tiered pricing, hybrid Bluetooth-NFC architectures, and subscription analytics are growing lifetime value per user, yet battery-life constraints and privacy concerns remain gating factors. Competitive intensity is rising as Samsung, Oura, Ultrahuman, Movano, and Sky Labs scale differentiated go-to-market strategies aimed at achieving clinical validation, luxury positioning, or mass-market penetration below USD 100.

Key Report Takeaways

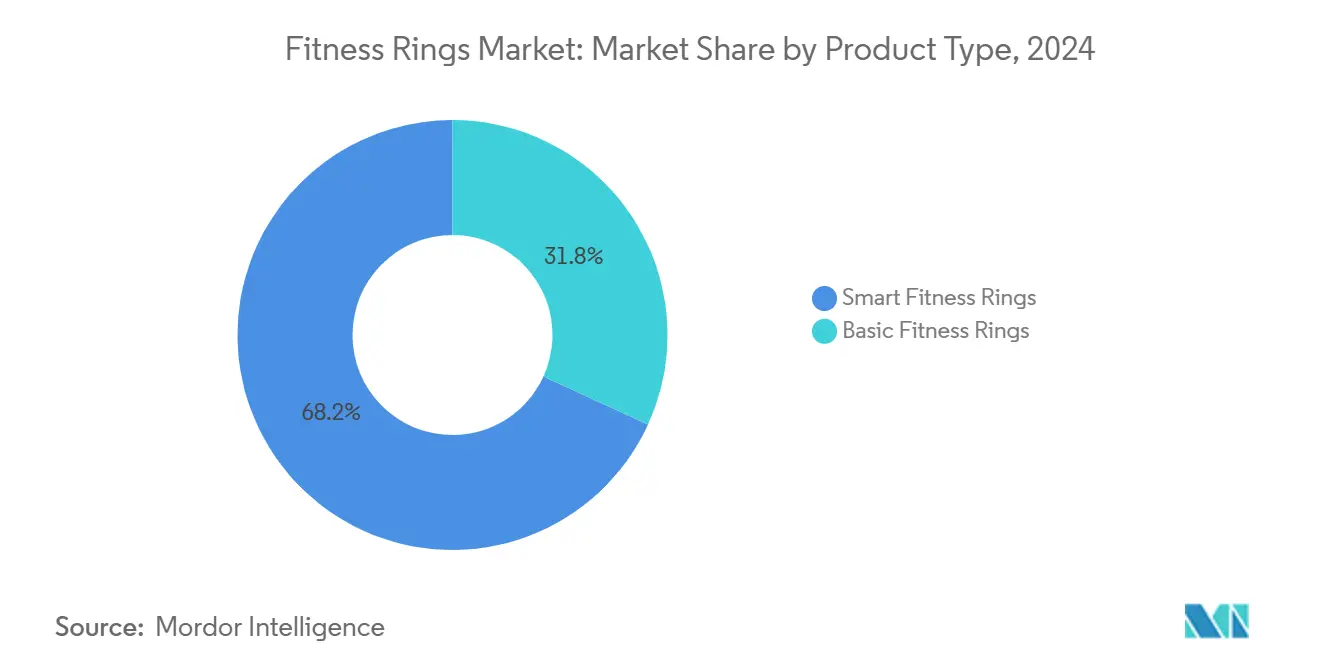

- By product type, smart fitness rings led with 68.17% of the 2024 fitness rings market share, and are forecast to expand at a 8.71% CAGR through 2030.

- By technology, Bluetooth-enabled models held 72.53% of the 2024 fitness rings market share, whereas NFC-enabled variants are projected to grow at a 9.26% CAGR to 2030.

- By application, health and wellness monitoring accounted for 64.44% of the fitness ring market size in 2024, and contactless payment use cases are expected to advance at an 8.22% CAGR through 2030.

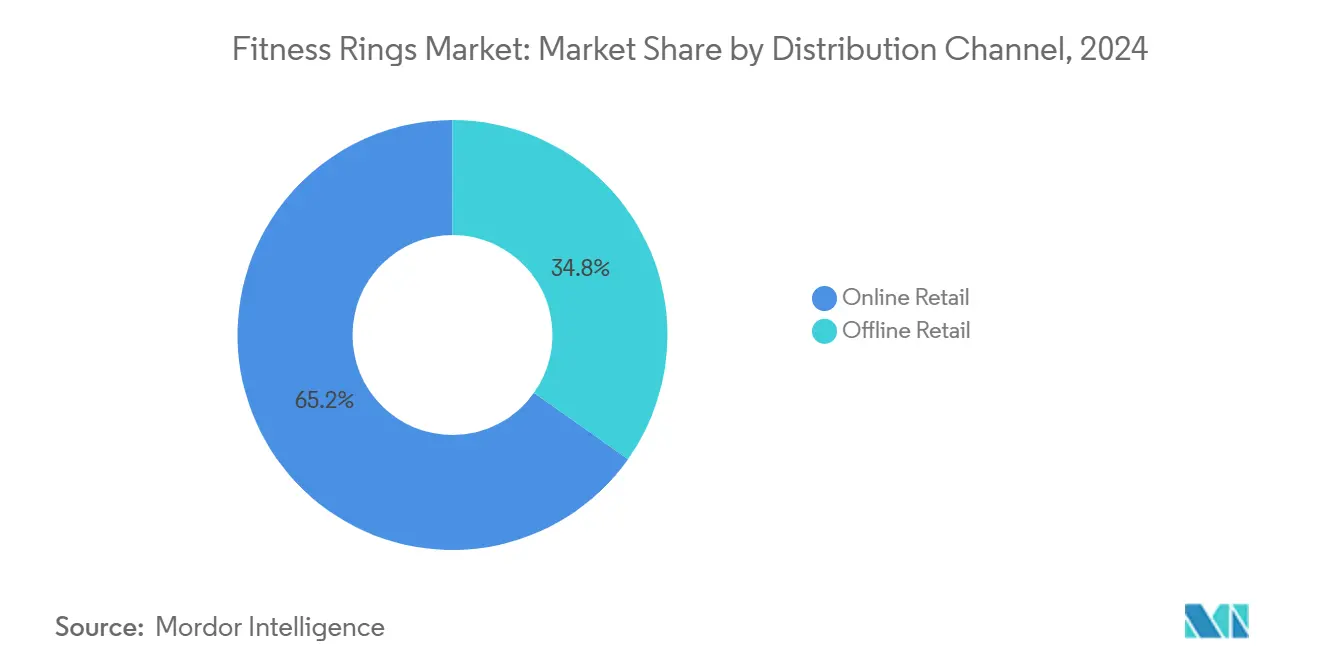

- By distribution channel, online retail captured 65.19% of sales in 2024; offline retail is the fastest-growing channel at a 9.75% CAGR, as in-store sizing removes conversion friction.

- By end user, individual consumers contributed 58.36% of the 2024 fitness rings market share, whereas corporate wellness programs are projected to record the highest growth rate of 10.02% from 2024 to 2030.

- By geography, North America commanded 39.01% of the 2024 revenue, while the Asia-Pacific region showed the fastest 8.01% CAGR to 2030.

Global Fitness Rings Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding Retail Availability of Smart Rings | +1.2% | Global, led by North America and Western Europe | Short term (≤ 2 years) |

| Rapid Miniaturization of Biometric Sensors | +1.5% | Global, with Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Growing Corporate Wellness Adoption of Rings | +1.3% | North America and Europe, spillover to Asia-Pacific | Medium term (2-4 years) |

| Rising Demand for Discreet Sleep-Tracking Wearables | +1.1% | Global, especially North America and Europe | Short term (≤ 2 years) |

| AI-Enabled Personalized Health Insights | +1.4% | Global, strongest in North America | Medium term (2-4 years) |

| Increasing Women’s-Health-Focused Ring Features | +0.9% | Global, notable in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Retail Availability Of Smart Rings

Mobile-carrier stores and consumer-electronics chains now stock smart rings beside flagship phones, giving shoppers hands-on sizing and immediate purchase options that online channels cannot replicate.[1]Victoria Song, “This Might Be the Year of the Smart Ring,” The Verge, theverge.com Staff-assisted fitting reduces returns that previously stemmed from incorrect ring sizes and lifts conversion during smartphone upgrade cycles. Financial institutions are also introducing battery-free payment rings through loyalty programs, exposing mainstream consumers to this form factor at checkout counters. This offline push compresses the adoption curve by validating the product category for shoppers who remain skeptical of buying health gadgets sight unseen. Vendors benefit from impulse purchases and carrier financing plans that lower upfront costs, supporting volume growth and accelerating global shelf presence.

Rapid Miniaturization Of Biometric Sensors

New photoplethysmography stacks and flexible printed circuits enable rings to match wrist-device accuracy for heart rate, SpO₂, and heart-rate variability, while maintaining a slim profile.[2]Jae-Lim Lee, “Sky Labs to Debut Smart Ring Monitoring Blood Pressure This Year,” Korea JoongAng Daily, koreajoongangdaily.joins.com Regulatory milestones, such as continuous blood pressure approval in South Korea and FDA-cleared pulse oximetry in the United States, confirm clinical-grade precision. Shrinking sensor modules free internal space for larger batteries or dual Bluetooth-NFC chipsets without enlarging the casing, broadening use cases from wellness scoring to reimbursable remote monitoring. Asian contract manufacturers scale production rapidly, driving down component costs and making advanced sensing affordable. These engineering gains re-position rings as credible medical devices rather than mere fitness accessories.

Growing Corporate Wellness Adoption Of Rings

Employers deploy rings in voluntary wellness programs because the discreet jewelry-style form avoids on-screen distractions that accompany smartwatches.[3]James Stables, “Wearables News Round-Up: Migraine Tech, Apple Smart Ring, Google LLMs,” Wareable PULSE, wareable.substack.com Passive overnight data collection feeds readiness scores used by human resources teams to shape fatigue management initiatives and benchmark program ROI. Sports organizations, including several NBA franchises, adopt rings to monitor recovery and modulate training loads, providing high-visibility proof points for enterprise buyers. Partnerships with Medicare Advantage plans show that payer-provider collaborations can underwrite hardware costs in exchange for continuous biometric data. High employee compliance, compared to badge-style trackers, strengthens the business case, prompting wellness budgets to shift from stipends toward subsidized ring rollouts.

AI-Enabled Personalized Health Insights

Ring vendors now embed large language model engines that translate raw biometrics into conversational guidance, elevating value beyond simple dashboards. Virtual assistants cross-reference individual sleep patterns, heart rate variability, temperature shifts, and mood logs against peer baselines and medical literature to recommend actionable lifestyle adjustments. Subscription tiers monetize these premium insights, and early metrics indicate higher retention among users who receive AI-generated coaching. As sensor hardware becomes commoditized, differentiation shifts to algorithm accuracy and evidence-based recommendations. Vendors without proprietary AI pipelines risk being viewed as basic data collectors rather than holistic health partners.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-Privacy and Cyber-Security Concerns | -0.8% | Global, heightened in Europe and North America | Short term (≤ 2 years) |

| Limited Battery Life Versus Wrist Wearables | -0.6% | Global | Medium term (2-4 years) |

| High Average Selling Prices Restrict Mass Adoption | -0.7% | Global, most acute in emerging markets | Short term (≤ 2 years) |

| Fragmented Regulatory Pathways Delay Medical-Device Claims | -0.5% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy And Cyber-Security Concerns

Continuous streams of heart-rate variability, sleep cycles, and body temperature data create sensitive profiles that could be misused if breached, prompting 60% of UAE respondents to hesitate before making wearable purchases. Many ring companies operate outside HIPAA-defined covered-entity status, leaving regulatory gray zones that amplify consumer skepticism. European GDPR rules impose strict consent and data-handling requirements that raise compliance costs for small vendors. Enterprises evaluating B2B deployments require ISO 27001 certifications and transparent retention policies prior to procurement. Vendors that fail to demonstrate robust encryption and breach-response protocols risk sales slowdowns in privacy-sensitive regions.

Limited Battery Life Versus Wrist Wearables

Smart rings typically deliver seven days of runtime, limited by the small lithium-polymer cells that power continuous PPG sensing and Bluetooth connectivity. Users accustomed to multi-week basic trackers find weekly charging inconvenient, especially when proprietary docks are misplaced during travel. Quick-charge cases and power-management integrated circuits provide incremental gains but do not eliminate the ritual. Battery-free NFC payment rings demonstrate an alternate architecture but sacrifice biometric sensing, splitting consumer choices. Solid-state batteries and energy-harvesting chips could potentially double runtime after 2027; however, near-term adoption will continue to be restrained by current chemistry limitations.

Segment Analysis

By Product Type: Smart Rings Accelerate Premium Adoption

Smart rings accounted for 68.17% of 2024 revenue and are advancing at an 8.71% CAGR, driven by consumer demand for integrated AI analytics, app ecosystems, and multi-device synchronization. High-grade titanium builds, FDA-cleared sensors, and subscription-based coaching justify price bands ranging from USD 300 to USD 500, positioning these devices at the center of an emerging holistic health stack. Basic rings, priced below USD 100, appeal to cost-conscious buyers but struggle to match accuracy under heavy motion or under clinical scrutiny.

Market leaders bundle menstrual-cycle intelligence, recovery readiness, and stress tracking, transforming rings from step-count curiosities into 24-hour health companions that sit comfortably beneath gloves and weight-training grips. Luxury editions clad in gold or platinum extend addressable demographics to fashion-focused users. Conversely, ultra-low-cost Chinese entrants squeeze margins while expanding their geographic reach in price-sensitive economies. When smart and basic shipments are combined, the fitness rings market size at the product level is projected to reach USD 239.56 million by 2030, with smart variants maintaining a dominant fitness rings market share as medical-grade approvals accumulate.

By Technology: Hybrid Bluetooth-NFC Architectures Broaden Use Cases

Bluetooth Low Energy remains foundational, powering real-time health data sync and firmware updates, and anchoring 72.53% of 2024 shipments. NFC-only rings, once a niche product, are now scaling with the enthusiasm for contactless payments, posting a 9.26% CAGR through 2030. Consumer surveys indicate high favorability for finger-tap transactions that eliminate the need for phone retrieval.

Banks subsidize NFC hardware to grow card volumes, incentivizing adoption in loyalty ecosystems. Meanwhile, dual-radio designs emerge, combining Bluetooth biometrics and passive NFC payments into a single device, blurring historic segmentation boundaries. Suppliers of secure-element chips and antenna micro-modules enable this convergence without enlarging housings. As hybrid adoption rises, the technology-level fitness rings market size expands, while the fitness rings market share of pure-Bluetooth variants gradually erodes, although they retain primacy for clinical data streams that require larger on-device memory and battery capacity.

By Application: Health Monitoring Remains Core While Payments Climb

Biometric health monitoring generated 64.44% of 2024 revenue thanks to consumer appetite for readiness scores that dictate training loads and sleep-rest calendars. Clinical trials leverage ring accuracy for long-COVID and chronic-disease research, underscoring data credibility. FDA-cleared pulse oximetry and continuous blood pressure monitoring rings signal a shift toward reimbursable remote patient monitoring programs, thereby enlarging the total addressable volume.

Payments, advancing at an 8.22% CAGR, ride on global tap-to-pay infrastructure and bank-financed hardware bundles. Athlete-recovery analytics gain traction in professional sports and collegiate programs, reinforcing performance credentials. Nascent smart-home gesture control and mixed-reality input applications hint at future diversification, yet current revenue contribution remains marginal. Collectively, these vectors keep the overall fitness rings market resilient against single-use saturation.

By Distribution Channel: Online Dominance Eases As In-Store Sizing Scales

Direct-to-consumer websites commanded 65.19% of sales in 2024, driven by early tech adopters and subscription upsell opportunities. Free return sizing kits mitigate fit anxiety but extend fulfillment cycles. Offline retail, currently at 34.81%, is growing at the fastest rate of 9.75% CAGR, as shelf presence enhances category awareness among mainstream shoppers.

Electronics chains, mobile-carrier shops, and luxury jewelers offer instant sizing and experiential demos that shrink hesitation and trigger impulse buys. In-store financing further softens price resistance. Vendor analytics indicate that multi-channel customers exhibit higher long-term app engagement and lower churn. As the fitness rings market matures, balanced channel strategies will temper acquisition costs while preserving data ownership.

By End User: Enterprises Drive Next-Wave Growth

Individual consumers still account for 58.36% of demand, yet price sensitivity and subscription fatigue limit velocity. Employers view rings as low-friction wellness tools that operate without screen distractions, and hence, corporate wellness programs are projected to clock a 10.02% CAGR through 2030. Enterprise dashboards standardize program performance metrics using aggregated readiness scores and sleep-quality trends, facilitating value-based contracting with insurers.

Healthcare-provider adoption grows where devices obtain medical device clearances, unlocking reimbursement codes for hypertension and sleep apnea monitoring. As reimbursement spreads, provider budgets will help scale penetration beyond lifestyle users, cementing rings in chronic-care pathways. These dynamics reinforce diversified revenue streams, spreading the growth of the fitness rings market size across both consumer and institutional purchasers.

Geography Analysis

North America accounted for 39.01% of 2024 revenue, driven by high discretionary income and an entrenched quantified-self culture. Early OEM launches, subscription absorption, and expansive carrier networks sustain demand.

The Asia-Pacific region, led by China, India, Japan, and South Korea, is expected to accelerate at an 8.01% CAGR, driven by the introduction of aggressively priced local brands and robust manufacturing ecosystems.

Clinical-grade approvals in South Korea and Japan foster hospital partnerships, while India’s smartphone uptake widens consumer exposure. Europe captures a roughly 28% share, balancing digital health enthusiasm with the stringent costs of GDPR compliance that challenge smaller vendors. Middle East markets, led by the United Arab Emirates and Israel, reward premium finishes and payment-first designs, while Africa and South America remain nascent, constrained by disposable-income disparities yet showing urban pockets of early demand.

Competitive Landscape

Market concentration is moderate. Oura retains a nearly 40% smart-ring share, driven by 2.5 million cumulative units and a subscription engine that generates over 20% of its revenue. Samsung leverages its Galaxy ecosystem lock-in and expansive retail channels, pressuring incumbents on brand recognition and research and development budgets.

Ultrahuman differentiates with metabolic biomarker integration and luxury plating, while Movano and Sky Labs chase FDA-based clinical credibility. Chinese challengers, such as Colmi and Xiaomi, flood the entry-level tiers at sub-USD 100, growing unit volume but compressing margins. Intellectual property filings increased eightfold between 2013 and 2023, with patents clustering around miniaturized PPG stacks, secure element payments, and AI-adaptive coaching algorithms. Strategic focus areas now hinge on extending battery life, securing data pipelines, and winning institutional deals that amortize hardware subsidies across subscription lifecycles.

Fitness Rings Industry Leaders

Oura Health Oy

Samsung Electronics Co., Ltd.

Ultrahuman Healthcare Private Limited

Motiv Inc.

RingConn Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: Isracard launched a battery-free payment ring priced at NIS 280 (USD 82) for Cashback Plus cardholders, enabling passive NFC transactions up to NIS 300.

- January 2025: Circular Ring 2 also introduced an 8-day battery life and rounded titanium design aimed at medical-grade B2B health-tracking deployments.

- January 2025: Circular launched Ring 2 featuring an FDA-approved ECG sensor for atrial fibrillation, tachycardia, and bradycardia detection.

- January 2025: Movano Health announced EvieAI, a virtual wellness assistant that personalizes guidance by cross-referencing Evie Ring biometrics with more than 100,000 medical journals.

Global Fitness Rings Market Report Scope

The fitness rings market report is segmented by Product Type (Basic Fitness Rings, Smart Fitness Rings), Technology (Bluetooth-Enabled Rings, NFC-Enabled Rings), Application (Health and Wellness Monitoring, Contactless Payments, Sports and Athlete Recovery, Smart Home and Device Control), Distribution Channel (Online Retail, Offline Retail), End User (Individual Consumers, Corporate Wellness Programs, Healthcare Providers), and Geography (North America, Europe, Asia-Pacific, Middle East, Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

| Basic Fitness Rings |

| Smart Fitness Rings |

| Bluetooth-Enabled Rings |

| NFC-Enabled Rings |

| Health and Wellness Monitoring |

| Contactless Payments |

| Sports and Athlete Recovery |

| Smart Home and Device Control |

| Online Retail |

| Offline Retail |

| Individual Consumers |

| Corporate Wellness Programs |

| Healthcare Providers |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product Type | Basic Fitness Rings | ||

| Smart Fitness Rings | |||

| By Technology | Bluetooth-Enabled Rings | ||

| NFC-Enabled Rings | |||

| By Application | Health and Wellness Monitoring | ||

| Contactless Payments | |||

| Sports and Athlete Recovery | |||

| Smart Home and Device Control | |||

| By Distribution Channel | Online Retail | ||

| Offline Retail | |||

| By End User | Individual Consumers | ||

| Corporate Wellness Programs | |||

| Healthcare Providers | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the fitness rings market in 2025 and how fast is it growing?

The market stands at USD 553.31 million in 2025 and is forecast to reach USD 792.87 million by 2030, reflecting a 7.46% CAGR.

Which product type generates most revenue today?

Smart rings hold 68.17% of 2024 revenue thanks to AI analytics and ecosystem integration.

What drives enterprise demand for rings versus watches?

Employers prefer rings because they collect passive data without on-screen distractions, boosting compliance in wellness programs.

How are ring vendors addressing battery-life concerns?

Solutions include dual power-efficient chipsets, quick-charge docks, and research into solid-state batteries that could double runtime after 2027.

Why are NFC-only rings gaining traction?

They enable battery-free contactless payments, appealing to banks that subsidize hardware to lift card transaction volume.

Which region is forecast to grow fastest by 2030?

Asia-Pacific leads with an 8.01% CAGR, driven by aggressive pricing from Chinese manufacturers and rising health awareness.