| Study Period | 2021 - 2030 |

| Market Size (2025) | USD 40.10 Billion |

| Market Size (2030) | USD 55.09 Billion |

| CAGR (2025 - 2030) | 6.56 % |

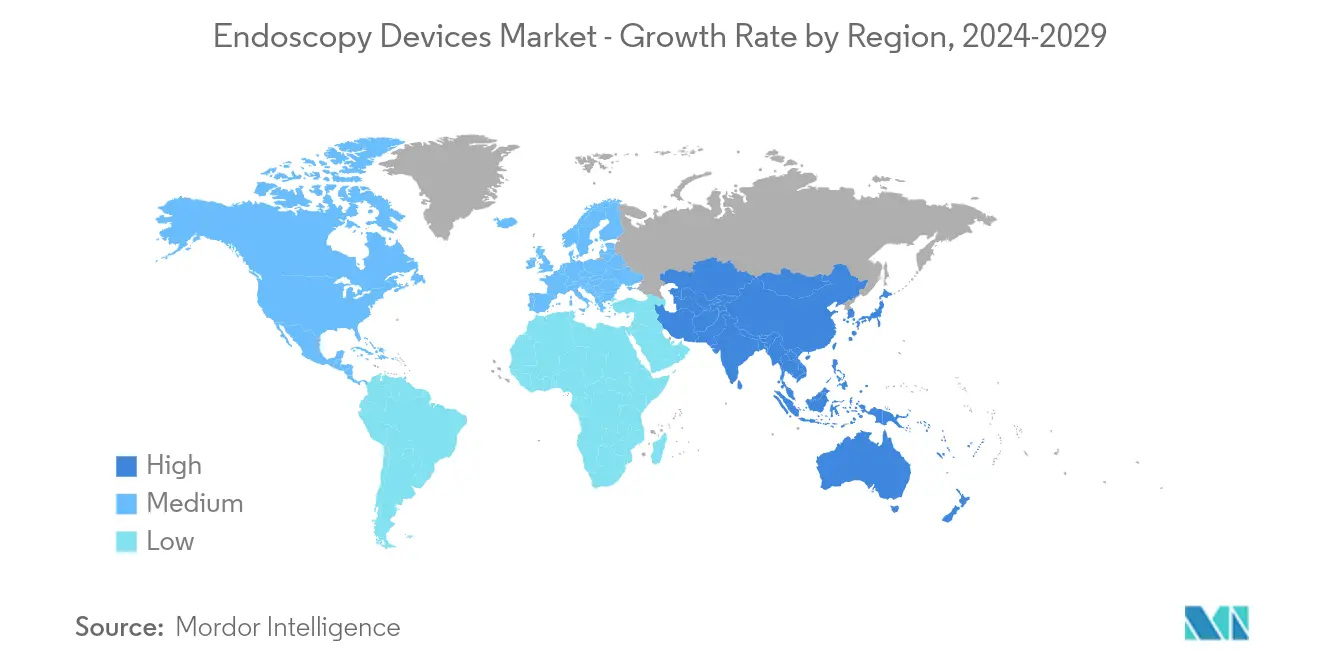

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

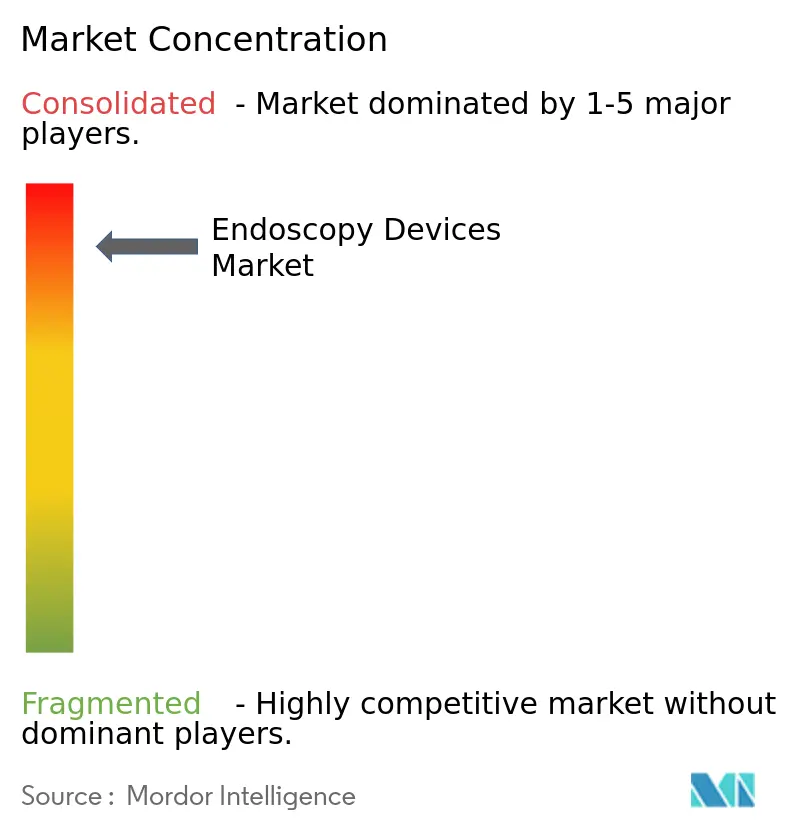

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Endoscopy Devices Market Analysis

The Global Endoscopy Devices Market size is estimated at USD 40.10 billion in 2025, and is expected to reach USD 55.09 billion by 2030, at a CAGR of 6.56% during the forecast period (2025-2030). Key drivers propelling the growth of the endoscopy devices market encompass an uptick in chronic disease cases, a heightened embrace of minimally invasive procedures, and enhanced healthcare access for the general public and other end users. Further, in both developing and developed nations, the demand for minimally invasive surgeries has surged over the past few decades in ambulatory surgery centers, driven by a rise in chronic diseases, including orthopedic, cardiovascular, neurosurgical, urological, and other persistent disorders. Organizations like the American Association of Gynecologic Laparoscopists (AAGL) and the International Society of Gynecologic Endoscopy (ISGE) are partnering with healthcare agencies in South Africa. They aim to raise awareness about the advantages of minimally invasive surgeries (MIS) and enhance their adoption rate, potentially propelling the market's growth in the years ahead.

Additionally, the American Cancer Society estimates that there will be 83,190 diagnoses of bladder cancer in the United States in 2024. The rising prevalence of bladder cancer, which necessitates precise endoscopic evaluations for effective treatment, is anticipated to propel market growth in the country. Technological advancements play a pivotal role in propelling the endoscopy devices market. For instance, in November 2024, Guam Regional Medical City (GRMC) launched an advanced capsule endoscopy service, introducing a cutting-edge, minimally invasive approach to digestive health diagnostics. This initiative marks a pivotal enhancement in gastrointestinal (GI) healthcare for Guam and its neighboring regions, spotlighting the integration of innovative medical technology and heightened patient comfort.

Moreover, government initiatives and support for endoscopic procedures are set to boost the endoscopy devices market share for various key players during the forecast period. For instance, in 2023, the Tasmanian Government allocated extra funds for public endoscopy services and unveiled the Statewide Endoscopy Services Four-Year Plan for 2023–2027. According to this plan, which was published by the Department of Health Tasmania, statewide endoscopies provided by private entities to public patients rose by 9.5% in the 2023–2024 period. This uptick underscores bolstered collaboration with the private sector and effective use of state resources to tackle the public waitlist for endoscopies.

In summary, the market is expanding due to the rising prevalence of chronic diseases and a growing demand for minimally invasive procedures. However, challenges persist. A shortage of skilled technicians and the risk of infections in endoscopes may hinder the market's growth during the forecast period.

Endoscopy Devices Market Insights and Trends

The Flexible Endoscope Segment is Expected to Show Growth as per this Market Forecast

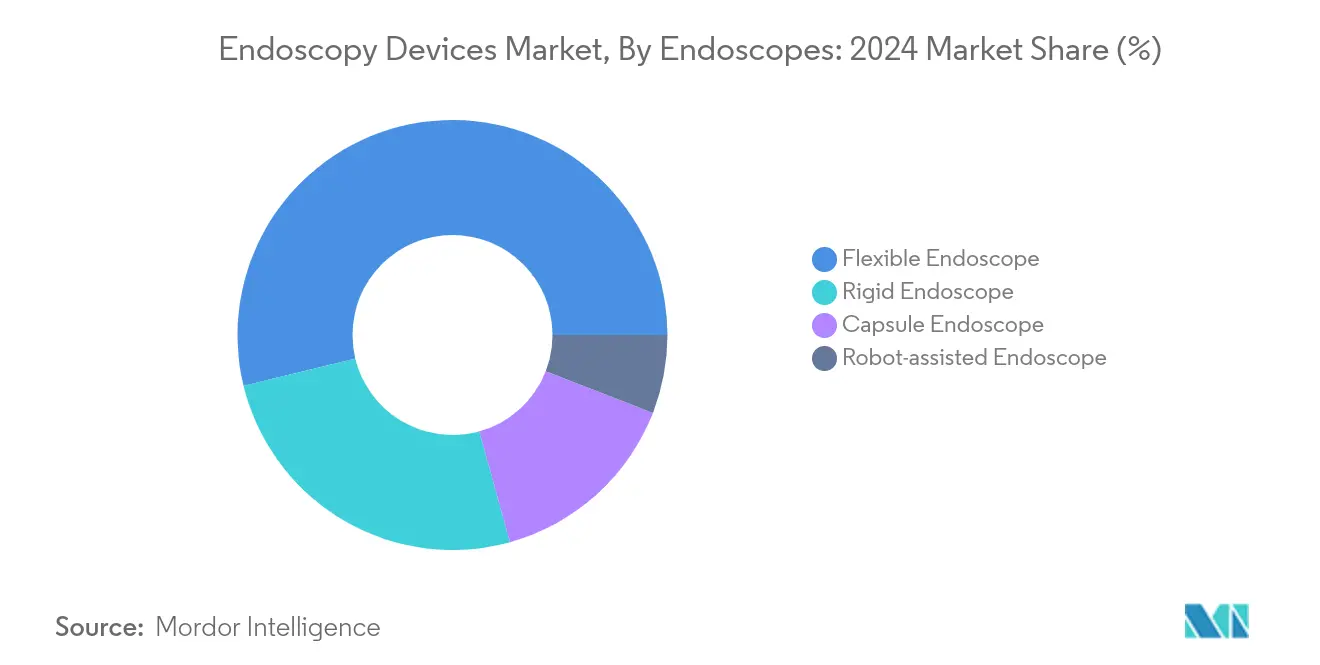

The flexible endoscope under the endoscopes segment is expected to have the major endoscopy devices market share with a CAGR of 5.86% over the forecast period (2024-2029). Market research estimates that the flexible endoscopes segment is expected to have a market value of USD 7.42 billion in 2024 and is likely to reach a market value of USD 9.87 billion by 2029.

Flexible endoscopes are optical instruments that transmit light and relay images to the observer. These instruments utilize flexible transparent fibers. The segment is projected to expand during the forecast period, driven by the advantages of flexible endoscopes over alternatives, a surge in product launches, and their growing adoption.

Key players and market leaders are continuously involved in various strategic activities related to the flexible endoscope, which ultimately accentuates segment growth over the forecast period. For instance, in September 2024, Olympus Australia, a global MedTech company unveiled "Sapphire." This marks Olympus's inaugural flexible endoscope sterilization facility. Situated in Melbourne, Australia, Sapphire is integrated into the newly introduced Olympus On-Demand solution. This solution is accessible to Australian healthcare facilities and aims to mitigate the risks, costs, and complexities tied to managing endoscopy services. Similarly, in February 2023, Boston Scientific Corporation secured the United States Food and Drug Administration 510(k) clearance for its LithoVue Elite Single-Use Digital Flexible Ureteroscope System. This system stands out as the first ureteroscope capable of real-time intrarenal pressure monitoring during procedures. Thus, considering the strategic activities related to the manufacturing of endoscopes, their demand is likely to increase, leading to flexible endoscope segment growth over the forecast period.

Understand The Key Trends Shaping This Market

Download PDF

The Gastroenterology Segment is Expected to Show a Significant Growth Rate in the Forecast Period

By application, the gastroenterology segment is expected to have a notable growth rate with a market size of USD 8.25 billion in 2024, and the industry analysis indicates that it is expected to grow to 10.61 billion in 2029 with a CAGR of 5.16% over the forecast period. Global growth in the gastroenterology segment is primarily fueled by the rising incidence of gastrointestinal diseases across young, adult, and elderly populations. Additionally, gastroesophageal reflux disease stands out as a widely recognized organic gastrointestinal disorder. As the burden of these diseases escalates and the geriatric population expands, the demand for gastrointestinal endoscopy surges.

The endoscopy devices market is segmented by type of device and application. The type of device segment is further segmented into endoscopes, endoscopic operative devices, and visualization equipment. The endoscopes are further segmented into rigid endoscopes, flexible endoscopes, capsule endoscopes, and robot-assisted endoscopes. The endoscopic operative devices are further segmented into irrigation/suction systems, access devices, wound protectors, insufflation devices, operative manual instruments, and other endoscopic operative devices. The visualization equipment is further segmented into an endoscopic camera, SD visualization system, and HD visualization system. The application segment is further segmented into gastroenterology, pulmonology, orthopedic surgery, cardiology, ENT surgery, gynecology, neurology, and other applications. Segmenting the market type of device and application enables stakeholders to grasp market dynamics and pinpoint key growth opportunities.

North America is Expected to Dominate the Endoscopy Devices Market During the Forecast Period

By geography, the North American region is likely to hold a major share with an estimated market size of USD 14.43 billion in 2024, expected to reach USD 19.72 billion by 2029, with a CAGR of 6.45%. In North America, the endoscopy devices industry is fueled by a growing geriatric population, the high burden of cardiovascular diseases, colorectal and stomach cancer, increasing adoption of minimally invasive surgeries, technological innovations, approvals, product launches, and partnerships by market players .

The increasing use of endoscopy devices in minimally invasive surgeries is set to boost market growth in countries such as the United States, Canada, and Mexico. The rise in cardiovascular diseases like heart failure and coronary artery disease, along with the increasing geriatric population, is one of the critical factors expected to fuel the market growth.

For instance, as per the October 2024 data updated by the Centers for Disease Control and Prevention (CDC), approximately 5% of adults aged 20 and older are affected by coronary artery disease, translating to about 1 in every 20 individuals in the United States. As per the same source, in the United States, approximately 805,000 individuals experience a heart attack annually. Of these, 605,000 are encountering their first heart attack, while 200,000 are individuals with a history of prior heart attacks. Hence, owing to the high prevalence of cardiac diseases, the demand for endoscopy devices is expected to rise, leading to market growth in the region.

Furthermore, growing government initiatives related to endoscopic procedures in the region are expected to drive market growth. For instance, in August 2024, under the Your Health plan, the Ontario government gave access to publicly funded surgeries and procedures. Annually, the province planned to add around 60,000 gastrointestinal (GI) endoscopy procedures at community surgical and diagnostic centres. The government is not only expanding the number of surgeries and procedures at community surgical and diagnostic centers but is also ensuring these centers are seamlessly integrated into the broader public health system. Hence, the high prevalence of chronic disease cases and government support for endoscopic procedures are likely to boost the market's growth over the forecast period in North America.

By geography, the global market is segmented into North America (United States, Canada, Mexico), Europe (Germany, United Kingdom, France, Italy, Spain, Rest of Europe), Asia-Pacific (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific), Middle East and Africa (GCC, South Africa, Rest of Middle East and Africa), and South America (Brazil, Argentina, Rest of South America). China, Japan, and India lead the Asia-Pacific region in both the swift development of advanced endoscopy devices and the surging market demand for them. The APAC region prioritizes establishing response systems and advanced endoscopy equipment for tackling various chronic diseases.

Endoscopy Devices Industry Overview

The market is semi-consolidated in nature and consists of global and local players. The competitive landscape includes an analysis of a few international as well as local companies that hold market shares. Key players in the endoscopy devices market research include Boston Scientific Corporation, CONMED Corporation, Cook Group Incorporated, Richard Wolf GmbH, Johnson & Johnson, Fujifilm Holdings Corporation, Medtronic PLC, Olympus Corporation, Karl Storz SE & Co. KG, Stryker Corporation, Hoya Corporation, Smith & Nephew PLC. Few of the key players currently hold a significant position in terms of market share. Key players focus on various technological advancements in their portfolio and are enhancing endoscopy procedures, which is anticipated to drive market growth during the forecast period.

For instance, in January 2024, Olympus Corporation (Tokyo, Japan) unveiled its cutting-edge innovations, ranging from advanced imaging technologies to pioneering medical procedures, that are set to redefine the landscape of healthcare. Olympus launched the VISERA ELITE III surgical visualization platform. This cutting-edge platform offers a versatile and forward-compatible solution, integrating multiple observation modes tailored to the evolving landscape of endoscopic surgery. Hence, owing to the incorporation of advanced platforms that can help in endoscopy, is poised to drive market growth during the forecast period.

Endoscopy Devices Market Leaders

-

Johnson & Johnson

-

Medtronic

-

Olympus

-

Boston Scientific

-

Cook Medical

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Endoscopy Devices Market News

- September 2024: Olympus Latin America unveiled the EVIS X1 endoscopy system in Brazil, marking the debut of Olympus' most advanced endoscopy technology to date. Supporting the launch, two events showcased virtual lectures by Dr. Yoji Takeuchi, focusing on colorectal cancer and the pivotal role of Olympus technology in its detection and treatment. Attendees also got to experience hands-on demonstrations of the EVIS X1 system.

- September 2024: Inovus Medical unveiled its suite of second-generation modules for the groundbreaking LapAR laparoscopic simulator. These new modules, an evolution of the successful first-generation platform, mark a notable leap in surgical education, boasting improved haptic feedback, heightened anatomical realism, and greater scalability and usability.

- September 2024: Olympus Corporation unveiled its latest innovation; the CH-S700-08-LB, a state-of-the-art 4K camera head tailored for endoscopic procedures in urology and gynecology. This advanced camera head seamlessly integrates with the VISERA ELITE III video system center, designed specifically for surgical endoscopy. Following its European debut, the CH-S700-08-LB is poised for launches in Japan, Hong Kong, and Singapore, with rollouts commencing in September 2024: contingent on each nation's regulatory approvals. The product's technical development was spearheaded by Sony Olympus Medical Solutions Corporation, a collaborative venture between Olympus and Sony Corporation.

- December 2023: Fujifilm India teamed up with GVN Hospital in Trichy to launch an innovative mobile endoscopy unit, dubbed the Endo Bus. The unit aims to transform the early detection landscape for gastrointestinal (GI) cancer throughout India.

Endoscopy Devices Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Growing Preference for Minimally-invasive Surgeries

- 4.2.2 Increasing Adoption of Endoscopy for Treatment and Diagnosis

- 4.2.3 Technological Advancements Leading to Enhanced Applications

-

4.3 Market Restraints

- 4.3.1 Lack of Skilled Technicians

- 4.3.2 Infections Caused by Some Endoscopes

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION (Market Size by Value in USD Billion)

-

5.1 By Type of Device

- 5.1.1 By Endoscopes

- 5.1.1.1 Rigid Endoscope

- 5.1.1.2 Flexible Endoscope

- 5.1.1.3 Capsule Endoscope

- 5.1.1.4 Robot-assisted Endoscope

- 5.1.2 By Endoscopic Operative Device

- 5.1.2.1 Irrigation/suction System

- 5.1.2.2 Access Device

- 5.1.2.3 Wound Protector

- 5.1.2.4 Insufflation Device

- 5.1.2.5 Operative Manual Instrument

- 5.1.2.6 Other Endoscopic Operative Devices

- 5.1.3 By Visualization Equipment

- 5.1.3.1 Endoscopic Camera

- 5.1.3.2 SD Visualization System

- 5.1.3.3 HD Visualization System

-

5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

6. COMPETITIVE LANDSCAPE

-

6.1 Company Profiles

- 6.1.1 Boston Scientific Corporation

- 6.1.2 CONMED Corporation

- 6.1.3 Cook Group Incorporated

- 6.1.4 Richard Wolf GmbH

- 6.1.5 Johnson & Johnson

- 6.1.6 Fujifilm Holdings Corporation

- 6.1.7 Medtronic PLC

- 6.1.8 Olympus Corporation

- 6.1.9 Karl Storz SE & Co. KG

- 6.1.10 Stryker Corporation

- 6.1.11 Hoya Corporation

- 6.1.12 Smith & Nephew PLC

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Competitive Landscape covers- Business Overview, Financials, Products and Strategies and Recent Developments

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Endoscopy Devices Industry Segmentation

As per the scope of the report, endoscopes are minimally invasive devices and can be inserted into natural openings of the body to observe an internal organ or a tissue in detail. Endoscopic surgeries are performed for imaging procedures and minor surgeries.

The endoscopy devices market is segmented by type of device, application, and geography. By type of device, the market is segmented into endoscopes, endoscopic operative devices, and visualization equipment. By application, the market is segmented into gastroenterology, pulmonology, orthopedic surgery, cardiology, ENT surgery, gynecology, neurology, and other applications. By geography, the market is further segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers the market sizes and forecasts in value (USD Billion) for the above segments.

| By Type of Device | By Endoscopes | Rigid Endoscope | |

| Flexible Endoscope | |||

| Capsule Endoscope | |||

| Robot-assisted Endoscope | |||

| By Endoscopic Operative Device | Irrigation/suction System | ||

| Access Device | |||

| Wound Protector | |||

| Insufflation Device | |||

| Operative Manual Instrument | |||

| Other Endoscopic Operative Devices | |||

| By Visualization Equipment | Endoscopic Camera | ||

| SD Visualization System | |||

| HD Visualization System | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| Australia | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | GCC | ||

| South Africa | |||

| Rest of Middle East and Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Need A Different Region or Segment?

Customize Now

Endoscopy Devices Market Research FAQs

What devices are used in Endoscopy?

Key devices used in endoscopy are endoscopes, gastroscopes, colonoscopes, electrosurgical devices, bronchoscopes, insufflators, etc.

What are the segments of the endoscopy market?

This endoscopy devices report is segmented by type of device, application, and geography.

What are the different types of endoscopic equipment?

Laryngoscope, Encephaloscope, Esophagoscope, Thoracoscope, Hysteroscope, etc., among others, are types of endoscopic equipment.

Who are the major players in the endoscopy devices market?

The major market players are Boston Scientific Corporation, Medtronic PLC, Olympus Corporation, Cook Group Incorporated, and Johnson & Johnson.

What are the challenges faced by the endoscopy devices market?

In many developing and under-developed countries, companies face endoscopy devices market size growth constraints, primarily due to a shortage of skilled technicians to operate these devices, despite investments in innovative technologies.