| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 97.23 Billion |

| Market Size (2030) | USD 144.13 Billion |

| CAGR (2025 - 2030) | 8.19 % |

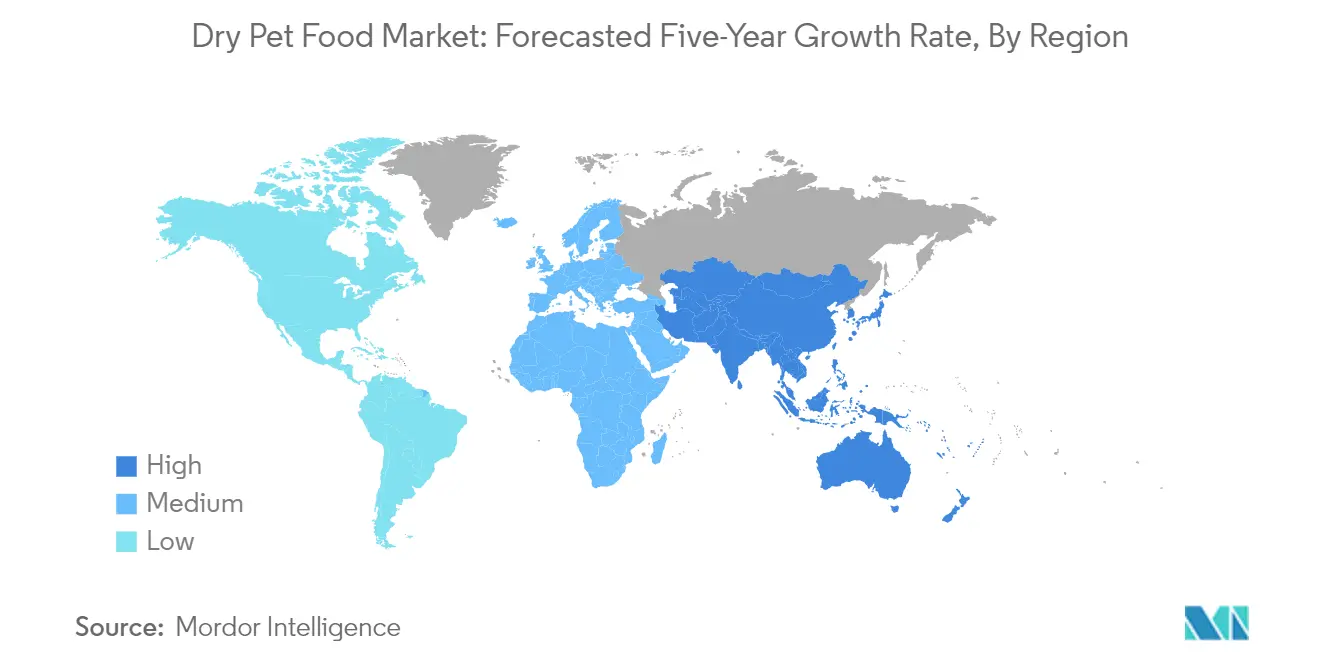

| Fastest Growing Market | Africa |

| Largest Market | North America |

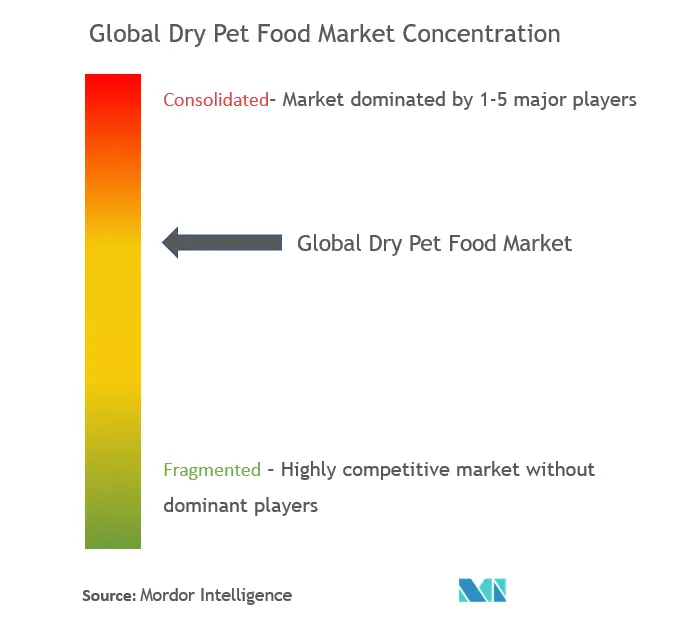

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order |

Dry Pet Food Market Analysis

The Dry Pet Food Market size is estimated at USD 97.23 billion in 2025, and is expected to reach USD 144.13 billion by 2030, at a CAGR of 8.19% during the forecast period (2025-2030).

The pet food industry is experiencing significant transformation driven by changing consumer demographics and lifestyle patterns. Pet ownership has reached unprecedented levels across developed markets, with the European Pet Food Federation (FEDIAF) reporting that 46% of European households owned pets by the end of 2021, representing 90 million households. This surge in pet ownership has been particularly pronounced among millennials and urban professionals, who are increasingly viewing pets as integral family members. The shift towards apartment living and busy urban lifestyles has made dry pet food an attractive option due to its convenience in storage and feeding.

Product quality and ingredient transparency have become paramount considerations in the pet food industry. A comprehensive 2022 survey across major markets, including the United States, United Kingdom, Brazil, Germany, and China, revealed that 79% of pet owners actively read product labels, demonstrating increased consumer consciousness about pet nutrition. This has prompted manufacturers to focus on premium ingredients, natural formulations, and clear labeling practices. The industry has witnessed a notable shift towards incorporating novel proteins, superfoods, and functional ingredients that promote specific health benefits.

Manufacturing processes are undergoing substantial modernization with the integration of advanced technologies. Artificial intelligence and automation are being increasingly deployed in production facilities to enhance quality control, improve efficiency, and ensure product consistency. These technological advancements are enabling manufacturers to maintain stricter quality standards while optimizing production costs. The industry is also witnessing innovations in packaging technology, with a focus on sustainable materials and improved preservation methods that extend shelf life while maintaining nutritional value.

The retail landscape for dry pet food continues to evolve, with traditional and modern channels adapting to changing consumer preferences. According to the American Pet Products Association's (APPA) National Pet Owners Survey 2021-2022, 54% of US households owned dogs, indicating a robust market for specialized pet retail channels. Retailers are responding by expanding their premium product offerings and developing private label brands that compete with established names. The industry is seeing increased collaboration between manufacturers and retailers to create exclusive product lines and enhanced shopping experiences that cater to sophisticated pet owners. This evolution in retail strategies is a significant aspect of pet food sales growth.

Dry Pet Food Market Trends

Increasing Trend of Pet Humanization

Pet humanization has emerged as a transformative force in the global pet food market, with pet owners increasingly viewing themselves as "pet parents" rather than mere owners. This shift in perception has led to a remarkable change in consumer behavior, with pet owners now prioritizing premium, high-quality nutrition for their animal companions. According to the European Pet Food Federation (FEDIAF), this trend is particularly evident in Europe, where 90 million households, representing 46% of total homes, now own companion animals. This has resulted in substantial spending on pet-related products and services, with pet owners increasingly seeking products that mirror human-grade quality and nutritional standards.

The humanization trend has directly influenced product development and marketing strategies across the industry. Major companies are responding by launching premium product lines with high-quality ingredients and specific health benefits. For instance, MARS Petcare's introduction of premium cat food under the IAMS brand in India, featuring specialized variants for both adult cats and kittens, exemplifies this trend. According to the American Pet Products Association, this shift towards premium products is reflected in consumer spending patterns, with dog owners spending an average of USD 287 on food annually, and a significant 41% of dog owners choosing premium dog food in 2020, marking an increase from 37% in the previous year.

Understand The Key Trends Shaping This Market

Download PDF

Growing Trend of E-commerce

The pet food market has witnessed a significant transformation in its distribution channels, with e-commerce emerging as a crucial platform for pet food sales. This shift is characterized by the integration of specialized online pet stores, subscription-based services, and omnichannel retail strategies that combine the convenience of online shopping with personalized customer service. The evolution of e-commerce has particularly benefited the dry pet food manufacturers, as these products are easier to store and ship compared to wet food alternatives, making them ideal for online retail and subscription-based delivery models.

The e-commerce trend has also facilitated greater product customization and consumer education. Online platforms now offer detailed product information, ingredient lists, and nutritional benefits, enabling pet owners to make more informed decisions about their pets' dietary needs. This digital transformation has led to the emergence of direct-to-consumer brands and subscription-based models that offer personalized feeding solutions based on factors such as breed, age, size, and specific health requirements. Major retailers and manufacturers have responded by expanding their online presence and developing specialized e-commerce strategies, including the integration of artificial intelligence for personalized product recommendations and automated reordering systems.

Increasing Concerns Over Pet Allergy and Intolerances

The growing awareness of pet food allergies and intolerances has become a significant driver in the premium pet food market, leading to the development of specialized formulations and alternative protein sources. Pet owners are becoming increasingly vigilant about ingredient selection, particularly regarding common allergens such as corn, wheat, soy, eggs, dairy, and certain protein sources. This heightened awareness has prompted manufacturers to develop grain-free, limited-ingredient, and novel protein formulations to address these concerns, resulting in a broader range of specialized dry pet food products available in the market.

The industry has responded to these concerns by introducing innovative solutions and alternative ingredients. Companies are investing in research and development to create hypoallergenic formulations and incorporate novel protein sources such as insects, plant-based proteins, and unique animal proteins. These alternatives not only address allergy concerns but also cater to pets with specific dietary requirements or sensitivities. The trend has also led to increased transparency in ingredient labeling and the development of products with clean label claims, allowing pet owners to make more informed decisions about their pets' nutrition while avoiding potential allergens that could affect their pets' health and well-being.

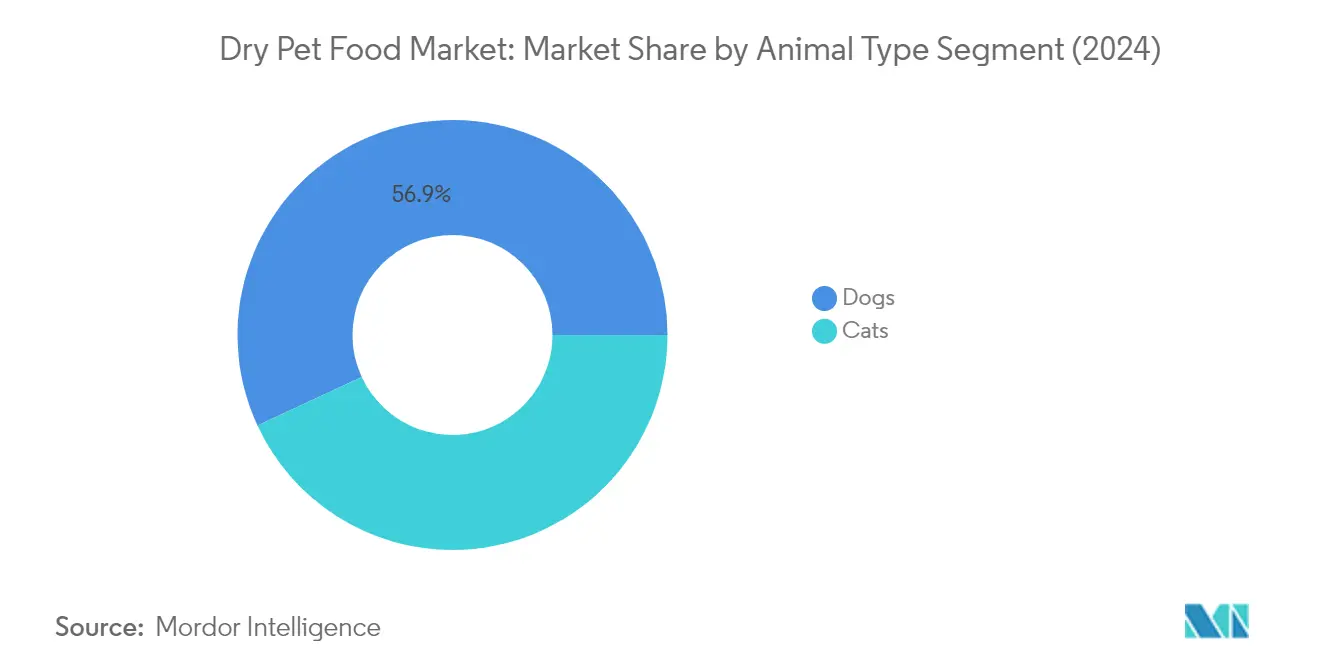

Segment Analysis: Animal Type

Dogs Segment in Dry Pet Food Market

The dogs segment continues to dominate the global dry pet food market, holding approximately 57% of the market share in 2024. This significant market position is driven by the increasing trend of dog ownership across major economies and growing awareness about proper pet nutrition. Pet owners are increasingly seeking premium and specialized custom dry dog food products that cater to different breeds, sizes, and life stages of dogs. The segment's growth is further supported by the rising demand for grain-free options, natural ingredients, and products addressing specific health concerns like weight management and digestive health. Additionally, the expansion of specialized pet retail channels and the growing availability of breed-specific formulations have contributed to maintaining the segment's dominant position in the market.

Cats Segment in Dry Pet Food Market

The cats segment is emerging as the fastest-growing segment in the dry pet food market, projected to grow at approximately 6% during 2024-2029. This accelerated growth is primarily attributed to the increasing preference for cats as pets in urban households, particularly among young professionals and small families. The segment is witnessing significant innovation in product formulations, with manufacturers introducing specialized dry food products that address specific nutritional requirements of indoor cats, different age groups, and various health conditions. The rising trend of premium cat food products, coupled with increasing awareness about feline nutrition and health, is driving the segment's growth. Furthermore, the development of palatability enhancers and the introduction of novel protein sources are creating new opportunities in this segment.

Segment Analysis: Product Type

Kibble Segment in Dry Pet Food Market

Kibble pet food continues to dominate the global dry pet food market, holding approximately 65% of the market share in 2024. This significant market position is attributed to kibble's superior qualities and consumer preferences. Kibble pet food is made from ground ingredients such as meat, grains, legumes, vegetables, and fruits, which are combined, formed into pellets, and cooked through extrusion. The segment's popularity stems from its convenience in storage and transportation, making it particularly appealing to pet owners. Kibble for dogs is notably less messy than wet dog food and can be left out for longer periods without bacterial contamination. For cats, kibble is more economical compared to wet food options and is particularly suitable for proportionate meal servings. Additionally, chewing hard kibble aids in preventing plaque and tartar buildup in pets' teeth, making it a preferred choice among veterinarians and pet owners focused on dental health.

Other Product Types Segment in Dry Pet Food Market

The Other Product Types segment, which includes crunchy bites, dehydrated pet food, freeze-dried diets, biscuits, and other treats, is projected to grow at approximately 6% CAGR from 2024 to 2029. This accelerated growth is driven by increasing consumer demand for premium and specialized pet food options. Dehydrated and freeze-dried foods are gaining significant traction as they retain more nutrients compared to higher-temperature-processed foods. These formats offer unique advantages such as being either completely raw or gently cooked, making them an attractive option for pet owners seeking more natural feeding alternatives. The segment's growth is further bolstered by the rising popularity of dental treats, particularly as more than 80% of dogs develop periodontal disease by the age of three. The increasing focus on pet dental health, combined with the growing trend of pet humanization, has made these specialized products one of the most sought-after categories in the market.

Segment Analysis: Ingredient Type

Protein Segment in Dry Pet Food Market

The protein segment continues to dominate the global dry pet food market, holding approximately 72% of the market share in 2024. This substantial market position is driven by the increasing awareness among pet owners about the importance of high-quality protein in their pets' diets. The segment's growth is particularly strong in premium and super-premium dry pet food categories, where manufacturers are incorporating novel protein sources like salmon, insect protein, and other animal-derived proteins. Pet food companies are also focusing on developing protein-rich formulations that cater to specific breed requirements and life stages of pets. The demand for protein-based dry pet food is further bolstered by the rising trend of pet humanization, where pet owners are increasingly seeking products that mirror human-grade protein quality. Additionally, the segment's growth is supported by innovations in protein processing technologies that help maintain the nutritional integrity of protein sources in dry pet food formulations.

Cereal and Cereal Derivatives Segment in Dry Pet Food Market

The cereal and cereal derivatives segment is experiencing robust growth, projected to expand at approximately 6% CAGR from 2024 to 2029. This growth is primarily driven by the increasing incorporation of wholesome grains and novel cereal derivatives in pet food formulations. Manufacturers are developing innovative grain-inclusive recipes that combine the benefits of traditional cereals with modern nutritional science. The segment is witnessing significant innovation in terms of ingredient processing techniques that enhance the digestibility and nutritional value of cereal-based components. Pet food companies are also responding to the growing demand for ancient grains and alternative cereal sources that offer additional health benefits. The segment's growth is further supported by research indicating the importance of certain grain-based nutrients in pet diets, leading to increased inclusion of specialized cereal derivatives in premium dry pet food formulations. Additionally, the rising trend of sustainable pet food production is driving the use of locally sourced cereal ingredients.

Remaining Segments in Ingredient Type

The other ingredient types segment in the dry pet food market encompasses a diverse range of components including vitamins, minerals, functional additives, and specialty ingredients. This segment plays a crucial role in enhancing the nutritional profile and functionality of dry pet food products. Manufacturers are increasingly incorporating novel ingredients such as antioxidants, probiotics, and natural preservatives to meet the growing demand for functional pet food products. The segment also includes various plant-based ingredients and specialty additives that cater to pets with specific dietary requirements or health conditions. Innovation in this segment is largely driven by advancements in ingredient processing technologies and increasing research into pet nutrition. The development of new functional ingredients and natural additives continues to expand the possibilities for product differentiation and value addition in the dry pet food market.

Segment Analysis: Distribution Channel

Specialized Pet Shops Segment in Dry Pet Food Market

Specialized pet shops continue to dominate the dry pet food market, holding approximately 40% market share in 2024. These shops, which include pet shop chains, independent stores, and veterinary shops, maintain their leadership position due to their deep expertise and personalized customer service. Pet shop chains particularly stand out by offering extensive product selections, professional consultations, and specialized knowledge about pet nutrition. The segment's strength is further enhanced by these shops' ability to provide in-store product demonstrations, samples, and expert nutrition guidance that helps pet owners make informed decisions. Additionally, specialized pet shops often partner with veterinary hospitals and grooming salons, offering comprehensive pet care solutions alongside their dry pet food products. Their ability to stock premium and super-premium brands, along with veterinary diets, makes them the preferred choice for pet owners seeking high-quality dry pet food products.

Online Channel Segment in Dry Pet Food Market

The online channel segment is experiencing remarkable growth, projected to expand at approximately 7% during 2024-2029. This accelerated growth is driven by the increasing adoption of e-commerce platforms among pet owners, particularly millennials who are well-versed in omnichannel retailing. The segment's expansion is further fueled by the convenience of doorstep delivery, competitive pricing, and the availability of a wider product range compared to traditional retail formats. Online retailers are enhancing their service offerings through subscription models, exclusive online-only products, and personalized shopping experiences. The segment is also benefiting from the integration of advanced technologies, such as AI-powered recommendation systems and automated reordering capabilities, which are making the online shopping experience more seamless for pet owners. Moreover, the rise in smartphone usage and internet penetration across various regions is contributing to the segment's robust growth trajectory.

Remaining Segments in Distribution Channel

The supermarkets/hypermarkets and other distribution channels segments continue to play vital roles in the dry pet food market. Supermarkets and hypermarkets leverage their advantage of providing one-stop shopping experiences, offering convenience for customers who prefer to purchase pet food alongside their regular groceries. These retail formats also benefit from their ability to offer competitive prices and frequent promotional activities. The other distribution channels segment, which includes grocery chains, drug stores, and niche specialists, serves specific customer needs and preferences. These channels often cater to local markets and provide essential access points for dry pet food products in areas where specialized pet shops or large retail formats may not be present. Both segments contribute to the market's overall accessibility and provide diverse options for pet owners to purchase dry pet food products.

Dry Pet Food Market Geography Segment Analysis

Dry Pet Food Market in North America

North America represents a mature and sophisticated market for dry pet food products, characterized by high pet ownership rates and increasing pet humanization trends. The region, comprising the United States, Canada, and other North American countries, demonstrates strong consumer awareness regarding pet nutrition and wellness. The pet food market is driven by the growing preference for premium and specialized dry pet food products, with manufacturers focusing on natural ingredients, grain-free options, and breed-specific formulations. The presence of major market players, advanced distribution networks, and robust e-commerce platforms further strengthens the regional market dynamics.

Dry Pet Food Market in United States

The United States dominates the North American dry pet food landscape, holding approximately 80% of the regional market share in 2024. The country's market is characterized by sophisticated consumer preferences and high spending on pet care products. American pet owners increasingly seek premium dry pet food products with specific nutritional benefits, driving innovation in product formulations. The market benefits from extensive retail networks, including specialized pet stores, supermarkets, and growing e-commerce channels. Pet humanization trends, coupled with rising awareness about pet health and nutrition, continue to shape product development and marketing strategies in the country.

Dry Pet Food Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 7% during 2024-2029. The Canadian market demonstrates increasing sophistication in consumer preferences, with pet owners showing strong interest in premium and natural dry pet food products. The country's robust pet care industry, supported by growing pet ownership rates and increasing disposable income, drives market expansion. Canadian consumers particularly value products with transparent ingredient sourcing and sustainable packaging. The market also benefits from strong distribution networks and increasing penetration of e-commerce platforms for pet food purchases.

Dry Pet Food Market in Europe

Europe represents a diverse and mature market for pet food market products, with distinct preferences across different regions. The market encompasses both Western European countries like Germany, the United Kingdom, France, Spain, Italy, and Belgium, as well as other European nations. The region demonstrates a strong emphasis on product quality, ingredient sourcing, and nutritional value. European consumers show an increasing preference for premium products, natural ingredients, and environmentally sustainable packaging solutions. The market benefits from well-established distribution networks and growing e-commerce penetration.

Dry Pet Food Market in Germany

Germany leads the European dry pet food market, commanding approximately 19% of the regional market share in 2024. The German market is characterized by stringent quality standards and sophisticated consumer preferences. Pet owners in Germany demonstrate strong interest in premium and specialized dry pet food products, particularly those with natural ingredients and specific health benefits. The country's robust retail infrastructure, including specialized pet stores and supermarkets, supports market growth. German consumers show an increasing preference for sustainable and environmentally friendly pet food products.

Dry Pet Food Market in Spain

Spain emerges as the fastest-growing market in Europe, with an expected growth rate of approximately 6% during 2024-2029. The Spanish market shows increasing sophistication in consumer preferences and growing awareness about pet nutrition. Pet owners in Spain demonstrate strong interest in premium dry pet food products, particularly those with specific health benefits and natural ingredients. The market benefits from expanding retail networks and growing e-commerce penetration. Spanish consumers increasingly value transparency in ingredient sourcing and manufacturing processes.

Dry Pet Food Market in Asia-Pacific

The Asia-Pacific region represents a dynamic and rapidly evolving market for dry pet food products, encompassing diverse countries with varying market maturity levels. The region includes major markets like China, Japan, and Southeast Asian countries, including Malaysia, the Philippines, Thailand, Indonesia, and Korea. The market is characterized by increasing pet ownership rates, growing urbanization, and rising disposable incomes. Consumer preferences vary significantly across countries, ranging from premium products in developed markets to value-oriented offerings in emerging economies. Japan emerges as the largest market in the region, while Korea demonstrates the fastest growth potential among all countries in the region.

Dry Pet Food Market in Japan

Japan leads the Asia-Pacific dry pet food market, demonstrating sophisticated consumer preferences and a strong emphasis on product quality. The Japanese market is characterized by high demand for premium products, particularly those focusing on specific health benefits and age-appropriate formulations. Japanese consumers show a strong preference for domestic brands and products with clear ingredient sourcing. The market benefits from advanced distribution networks and a strong presence of both local and international manufacturers.

Dry Pet Food Market in Korea

Korea emerges as the fastest-growing market in the Asia-Pacific region, demonstrating rapid evolution in consumer preferences and market sophistication. The Korean market shows increasing premiumization trends, with growing demand for high-quality dry pet food products. Pet owners in Korea demonstrate strong interest in products with specific health benefits and natural ingredients. The market benefits from expanding retail networks and growing e-commerce penetration, particularly among younger pet owners.

Get Analysis on Important Geographic Markets

Download PDF

Dry Pet Food Industry Overview

Top Companies in Dry Pet Food Market

The global dry pet food market is characterized by intense innovation and strategic expansion activities among major players like Mars Inc., Nestlé Purina, Colgate-Palmolive, and J.M. Smucker Company. Companies are focusing on developing premium and specialized formulas that are grain-free, organic, promote oral health, and address specific dietary needs of pets. Operational agility is demonstrated through investments in manufacturing facilities and supply chain optimization to meet growing demand. Strategic moves include partnerships with veterinary services, research institutions, and e-commerce platforms to strengthen market presence. Companies are expanding their geographical footprint through new manufacturing facilities, particularly in emerging markets like India and Brazil, while also investing in sustainable production practices and innovative packaging solutions to meet evolving consumer preferences. Notably, leading pet food manufacturers like Mars Inc. are spearheading these initiatives.

Consolidated Market Led By Global Conglomerates

The dry pet food market exhibits a moderately consolidated structure dominated by multinational conglomerates with diverse product portfolios and extensive distribution networks. These major players leverage their established brand reputation, research capabilities, and financial resources to maintain market leadership. The market is characterized by a mix of global leaders and regional specialists, with local players focusing on specific geographical regions or product niches. The presence of numerous small and medium-sized enterprises creates a competitive environment in regional markets, though they often struggle to match the scale and reach of global leaders.

Merger and acquisition activities have been significant in shaping the market landscape, with larger companies acquiring smaller, innovative brands to expand their product offerings and market reach. Notable acquisitions include General Mills' purchase of Blue Buffalo and J.M. Smucker's acquisition of Big Heart Pet Brands, demonstrating the industry's consolidation trend. Companies are also forming strategic partnerships with veterinary service providers and research institutions to strengthen their market position and enhance product development capabilities. Among these, leading pet food manufacturers are particularly active in mergers and acquisitions to consolidate their market position.

Innovation and Distribution Key to Success

Success in the dry pet food market increasingly depends on companies' ability to innovate across product formulations, manufacturing processes, and distribution channels. Incumbents must focus on premium product development, sustainable packaging solutions, and strengthening their e-commerce presence to maintain market share. Companies need to invest in research and development to create specialized products addressing specific health concerns and dietary requirements while also expanding their distribution networks through both traditional and digital channels. Building strong relationships with veterinarians and pet care professionals has become crucial for product validation and market penetration.

For contenders looking to gain ground, focusing on niche markets and developing innovative, specialized products presents significant opportunities. Success factors include establishing strong local distribution networks, leveraging e-commerce platforms, and building brand credibility through transparency in ingredient sourcing and manufacturing processes. The regulatory environment, particularly regarding pet food safety and labeling requirements, continues to influence market dynamics and necessitates ongoing compliance investments. Companies must also address the growing consumer emphasis on sustainability and ethical sourcing practices while maintaining competitive pricing strategies to succeed in this evolving market landscape. Key players such as cat food manufacturers and dry food manufacturers are at the forefront of these innovations, ensuring they meet consumer demands effectively.

Dry Pet Food Market Leaders

-

Mars Inc

-

Nestle SA Purina

-

Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.)

-

The J.M. Smucker Company

-

Blue Buffalo Company Ltd

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Dry Pet Food Market News

- February 2023: Mars Petcare, part of Mars Incorporated announced that it has completed its acquisition of Champion Petfoods a pioneer in the fast-growing premium pet food space, and its two premier brands, ORIJEN and ACANA. This acquisition enhances Mars Petcare's global portfolio, bolstering its offerings in pet nutrition products and health services.

- July 2022: Nestle acquired the pet food company Purina Petcare India. This will transfer the entire assets and liabilities to the company, including the employees.

- May 2022: MARS Petcare launched premium cat food in India under the IAMS brand. This brand offers four dry variants in India, specially designed to ensure a healthy, natural defense for both adult cats and kittens.

Dry Pet Food Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Overview

-

4.2 Market Drivers

- 4.2.1 Increasing Trend of Pet Humanization

- 4.2.2 Growing Trend of E-Commerce

- 4.2.3 Increasing Concern over Pet Allergies and Intolerances

-

4.3 Market Restraints

- 4.3.1 High Cost of Dry Pet Food

- 4.3.2 Limited Availability of High Quality Ingredients

-

4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 Animal Type

- 5.1.1 Dogs

- 5.1.2 Cats

- 5.1.3 Other Animals

-

5.2 Product Type

- 5.2.1 Kibble

- 5.2.2 Other Product Types

-

5.3 Ingredient Type

- 5.3.1 Protein

- 5.3.1.1 Animal-derived

- 5.3.1.2 Plant-derived

- 5.3.2 Cereals and Cereal Derivatives

- 5.3.3 Other Ingredient Types

-

5.4 Distribution Channel

- 5.4.1 Specialized Pet Shops

- 5.4.2 Online Channels

- 5.4.3 Supermarkets/Hypermarkets

- 5.4.4 Other Distribution Channels

-

5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East & Africa

- 5.5.5.1 South Africa

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Rest of Middle East & Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

-

6.3 Company Profiles

- 6.3.1 Mars Inc.

- 6.3.2 Nestle Purina Petcare Company

- 6.3.3 The JM Smucker Company

- 6.3.4 Colgate-Palmolive Company (Hill's Pet Nutrition Inc.)

- 6.3.5 General Mills Blue Buffalo Pet Products Inc.

- 6.3.6 Clearlake Capital Group L.P. (Wellness Pet Company Inc.)

- 6.3.7 Schell & Kampeter Inc. (Diamond Pet Foods)

- 6.3.8 Alltech Inc.

- 6.3.9 Archer Daniels Midland

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Dry Pet Food Industry Segmentation

Pet foods are usually intended to provide complete and balanced nutrition to the pet but are primarily used as functional products. A dry diet, a biscuit diet, or a kibble diet is a processed pet food diet.

The Dry Pet Food Market is segmented by Animal Type, Product Type, Ingredient Type, Distribution Channel, and Geography. The Animal Types are further segmented into Dogs and Cats. Product Types are further segmented into Kibble and Other Dry Pet Food. The Ingredient Types are further segmented into Protein, Cereal and Cereal Derivatives, and Other Ingredient Types. The Distribution Channels are further segmented into Specialized Pet Stores, Supermarkets/Hypermarkets, Online Channels, and Other Distribution Channels. The report is further segmented by Geography into North America, Europe, Asia-Pacific, South America, and Middle East & Africa. The report offers the market size for all the above segments in terms of value (USD).

| Animal Type | Dogs | ||

| Cats | |||

| Other Animals | |||

| Product Type | Kibble | ||

| Other Product Types | |||

| Ingredient Type | Protein | Animal-derived | |

| Plant-derived | |||

| Cereals and Cereal Derivatives | |||

| Other Ingredient Types | |||

| Distribution Channel | Specialized Pet Shops | ||

| Online Channels | |||

| Supermarkets/Hypermarkets | |||

| Other Distribution Channels | |||

| Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Rest of North America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Spain | |||

| Rest of Europe | |||

| Asia-Pacific | India | ||

| China | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East & Africa | South Africa | ||

| United Arab Emirates | |||

| Saudi Arabia | |||

| Rest of Middle East & Africa | |||

Need A Different Region or Segment?

Customize Now

Dry Pet Food Market Research Faqs

How big is the Dry Pet Food Market?

The Dry Pet Food Market size is expected to reach USD 97.23 billion in 2025 and grow at a CAGR of 8.19% to reach USD 144.13 billion by 2030.

What is the current Dry Pet Food Market size?

In 2025, the Dry Pet Food Market size is expected to reach USD 97.23 billion.

Who are the key players in Dry Pet Food Market?

Mars Inc, Nestle SA Purina, Colgate-Palmolive Company (Hill's Pet Nutrition, Inc.), The J.M. Smucker Company and Blue Buffalo Company Ltd are the major companies operating in the Dry Pet Food Market.

Which is the fastest growing region in Dry Pet Food Market?

Africa is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Dry Pet Food Market?

In 2025, the North America accounts for the largest market share in Dry Pet Food Market.

What years does this Dry Pet Food Market cover, and what was the market size in 2024?

In 2024, the Dry Pet Food Market size was estimated at USD 89.27 billion. The report covers the Dry Pet Food Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Dry Pet Food Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Dry Pet Food Market Research

Mordor Intelligence provides a comprehensive analysis of the dry pet food market, drawing on decades of expertise in the pet food industry. Our extensive coverage spans the entire ecosystem, from dry pet food manufacturers to leading brands like Mars dog food brands and Mars cat food brands. The report thoroughly examines the dry pet food manufacturing process, including specialized segments such as kibble pet food and dehydrated pet food. It also analyzes the dynamics of pet food sales across global markets.

This detailed industry analysis benefits stakeholders across the value chain, from cat food manufacturers to retailers. It offers actionable insights into opportunities in the premium pet food market. The report examines various sales channels in the pet food market, with a particular focus on regional markets, including the UAE pet food market and Saudi Arabia pet food market. Our insights are available in an easy-to-read report PDF format for download. It features comprehensive data on dry foods manufacturers and emerging trends in the global pet food market, enabling informed decision-making for industry participants.