Market Size of dog food Industry

| Icons | Lable | Value |

|---|---|---|

|

|

Study Period | 2017 - 2029 |

|

|

Market Size (2024) | USD 96.33 Billion |

|

|

Market Size (2029) | USD 156.60 Billion |

|

|

Largest Share by Pet Food Product | Food |

|

|

CAGR (2024 - 2029) | 10.21 % |

|

|

Largest Share by Region | North America |

|

|

Market Concentration | Medium |

Major Players |

||

|

|

||

|

*Disclaimer: Major Players sorted in no particular order |

Dog Food Market Analysis

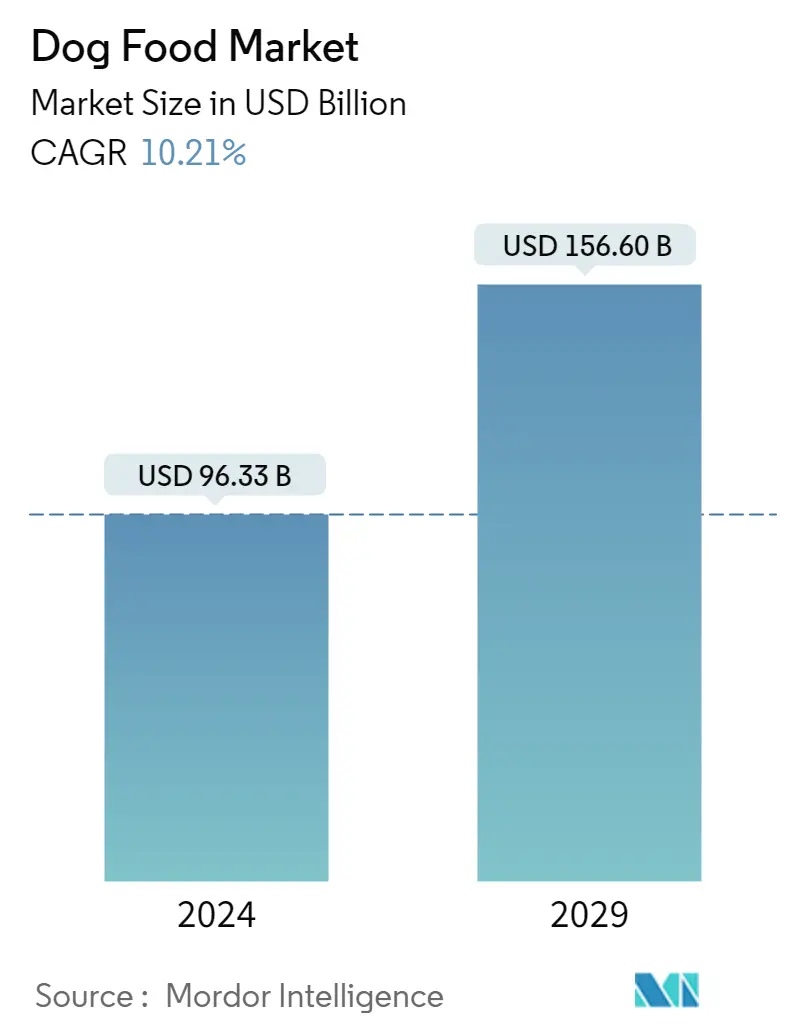

The Dog Food Market size is estimated at USD 96.33 billion in 2024, and is expected to reach USD 156.60 billion by 2029, growing at a CAGR of 10.21% during the forecast period (2024-2029).

96.33 Billion

Market Size in 2024 (USD)

156.60 Billion

Market Size in 2029 (USD)

10.46 %

CAGR (2017-2023)

10.21 %

CAGR (2024-2029)

Largest Market by Product

68.47 %

value share, Food, 2022

The expanding dog population has led to increased demand for pet food options, making it the largest segment as owners prioritize providing essential nutrition for their dogs.

Largest Market by Region

44.98 %

value share, North America, 2022

High dog ownership rates and increased purchasing of dry food such as kibbles and treats formulated with functional ingredients have contributed to the region’s leading position.

Fastest-growing Market by Product

11.58 %

Projected CAGR, Pet Veterinary Diets, 2023-2029

Increasing diseases in dogs, specifically digestive and CKD issues, increased the necessity of these diets to support canine health, thereby promoting market growth.

Fastest-growing Market by Region

12.59 %

Projected CAGR, Africa, 2023-2029

Increasing dog ownership rates and growing consumer spending power on premium and nutritional dog food products are the major factors driving the region’s growth.

Leading Market Player

18.42 %

market share, Mars Incorporated, 2022

Mars, Incorporated is the market leader due to its product launches with a focus on providing cats with specialized nutrition and the expansion of its manufacturing facilities globally.

Food products and treats dominate the global dog food market, with veterinary diets emerging as the major pet food segment

- Globally, dogs are the major pets dominating the pet food market due to the higher consumption of commercial pet food and high population. In 2022, dogs held 48.7% of the global pet food market. The share increased by 67.2% between 2017 and 2022 due to the rising dog population and the growing demand for premium products. For instance, the dog population grew by 13.5% in 2022 compared to 2017. The food segment is the largest segment in the dog food market, valued at USD 54.7 billion in 2022. This is because pet food is a staple purchase for most pet owners regardless of their pet breed size or age.

- Treats were the second-largest product type, amounting to a market value of USD 13.3 billion in 2022. Dogs show a preference for treats over other pets. These treats serve multiple purposes, including training, maintaining dental health, and providing rewards. The dog treats market is projected to witness a CAGR of 9.0% during the forecast period.

- Pet veterinary diets are specifically formulated to address specific health conditions in pets, such as urinary tract diseases, renal failure, and digestive sensitivity. They may also be given to pets as a preventative measure to avoid developing specific health issues. During the forecast period, pet veterinary diets are expected to register the highest CAGR of 9.8%, as there is a growing demand for these specialized products.

- The pet nutraceuticals market increased by 19.7% in 2022 compared to 2017, driven by the growing awareness of healthy diets, particularly due to rising health concerns in dogs.

- The market is driven by the increasing dog population, the specific health needs of dogs, and the growing awareness of health among dog owners. It is projected to witness a CAGR of 8.8% during the forecast period.

North America dominates the market due to increased disposable income and higher pet humanization in the region

- The global dog food market witnessed significant growth. In 2022, North America emerged as the largest region in the global dog food product market, accounting for USD 36.0 billion, which increased by 81.8% between 2017 and 2022. This growth was driven by the increasing dog population by 17.8% in the same period, increasing disposable income, and the rising trend of pet humanization.

- Europe is the second major region for the dog food market. In 2022, it accounted for USD 19.48 billion in 2022, and it is projected to reach 35.57 billion in 2029. It is associated with increasing awareness about pet nutrition, rising demand for grain-free and natural products, adoption of preventive approaches, and increased dog population in the region. For instance, the dog population in 2022 was 97.0 million, which increased by 14.2% since 2017.

- Asia-Pacific is one of the emerging dog food markets. In 2022, it accounted for 17.5% of the global dog food market, which had a significant growth of 61.9% between 2017 and 2022. This is due to the pet owners increasingly opting for commercial pet food products and the higher population in the region. In 2022, it accounted for 29.1% of the global dog population.

- Africa and South America are the fastest-growing regions in the global dog food market, with projected CAGRs of 12.6% and 12.4% during the forecast period, respectively. This growth is associated with the increasing pet humanization, growing pet population, and a large number of pet owners shifting from home-cooked food to commercial pet food.

- The higher usage of commercial products increased the pet population, and the rise in pet humanization trends are factors expected to drive the market with a CAGR of 8.8% during the forecast period.

Dog Food Industry Segmentation

Food, Pet Nutraceuticals/Supplements, Pet Treats, Pet Veterinary Diets are covered as segments by Pet Food Product. Convenience Stores, Online Channel, Specialty Stores, Supermarkets/Hypermarkets are covered as segments by Distribution Channel. Africa, Asia-Pacific, Europe, North America, South America are covered as segments by Region.

- Globally, dogs are the major pets dominating the pet food market due to the higher consumption of commercial pet food and high population. In 2022, dogs held 48.7% of the global pet food market. The share increased by 67.2% between 2017 and 2022 due to the rising dog population and the growing demand for premium products. For instance, the dog population grew by 13.5% in 2022 compared to 2017. The food segment is the largest segment in the dog food market, valued at USD 54.7 billion in 2022. This is because pet food is a staple purchase for most pet owners regardless of their pet breed size or age.

- Treats were the second-largest product type, amounting to a market value of USD 13.3 billion in 2022. Dogs show a preference for treats over other pets. These treats serve multiple purposes, including training, maintaining dental health, and providing rewards. The dog treats market is projected to witness a CAGR of 9.0% during the forecast period.

- Pet veterinary diets are specifically formulated to address specific health conditions in pets, such as urinary tract diseases, renal failure, and digestive sensitivity. They may also be given to pets as a preventative measure to avoid developing specific health issues. During the forecast period, pet veterinary diets are expected to register the highest CAGR of 9.8%, as there is a growing demand for these specialized products.

- The pet nutraceuticals market increased by 19.7% in 2022 compared to 2017, driven by the growing awareness of healthy diets, particularly due to rising health concerns in dogs.

- The market is driven by the increasing dog population, the specific health needs of dogs, and the growing awareness of health among dog owners. It is projected to witness a CAGR of 8.8% during the forecast period.

| Pet Food Product | |||||||||||

| |||||||||||

| |||||||||||

| |||||||||||

|

| Distribution Channel | |

| Convenience Stores | |

| Online Channel | |

| Specialty Stores | |

| Supermarkets/Hypermarkets | |

| Other Channels |

| Region | |||||||||||||||

| |||||||||||||||

| |||||||||||||||

| |||||||||||||||

| |||||||||||||||

|

Dog Food Market Size Summary

The dog food market is experiencing robust growth, driven by the increasing dog population and the rising demand for premium and specialized pet products. Dogs dominate the global pet food market, with a significant share attributed to their higher consumption of commercial pet food. The market is characterized by a strong preference for dog food, treats, and veterinary diets, with the latter witnessing the highest growth due to the growing awareness of specific health needs in dogs. The trend of pet humanization, where pets are treated as family members, is further propelling the market, as pet owners are more inclined to invest in high-quality and health-conscious food options for their dogs.

Regionally, North America leads the market, supported by a high adoption rate of dogs and increasing disposable incomes. Europe follows closely, with a focus on natural and grain-free products, while the Asia-Pacific region is emerging as a significant market due to the growing trend of commercial pet food adoption. The market is also witnessing a shift towards online retailing, enhancing accessibility and convenience for pet owners. The competitive landscape is moderately consolidated, with major players like Colgate-Palmolive Company, General Mills Inc., Mars Incorporated, Nestle (Purina), and The J. M. Smucker Company dominating the market. These companies are actively innovating and expanding their product offerings to cater to the evolving preferences of dog owners.

Dog Food Market Size - Table of Contents

-

1. MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

-

1.1 Pet Food Product

-

1.1.1 Food

-

1.1.1.1 By Sub Product

-

1.1.1.1.1 Dry Pet Food

-

1.1.1.1.1.1 By Sub Dry Pet Food

-

1.1.1.1.1.1.1 Kibbles

-

1.1.1.1.1.1.2 Other Dry Pet Food

-

-

-

1.1.1.1.2 Wet Pet Food

-

-

-

1.1.2 Pet Nutraceuticals/Supplements

-

1.1.2.1 By Sub Product

-

1.1.2.1.1 Milk Bioactives

-

1.1.2.1.2 Omega-3 Fatty Acids

-

1.1.2.1.3 Probiotics

-

1.1.2.1.4 Proteins and Peptides

-

1.1.2.1.5 Vitamins and Minerals

-

1.1.2.1.6 Other Nutraceuticals

-

-

-

1.1.3 Pet Treats

-

1.1.3.1 By Sub Product

-

1.1.3.1.1 Crunchy Treats

-

1.1.3.1.2 Dental Treats

-

1.1.3.1.3 Freeze-dried and Jerky Treats

-

1.1.3.1.4 Soft & Chewy Treats

-

1.1.3.1.5 Other Treats

-

-

-

1.1.4 Pet Veterinary Diets

-

1.1.4.1 By Sub Product

-

1.1.4.1.1 Diabetes

-

1.1.4.1.2 Digestive Sensitivity

-

1.1.4.1.3 Oral Care Diets

-

1.1.4.1.4 Renal

-

1.1.4.1.5 Urinary tract disease

-

1.1.4.1.6 Other Veterinary Diets

-

-

-

-

1.2 Distribution Channel

-

1.2.1 Convenience Stores

-

1.2.2 Online Channel

-

1.2.3 Specialty Stores

-

1.2.4 Supermarkets/Hypermarkets

-

1.2.5 Other Channels

-

-

1.3 Region

-

1.3.1 Africa

-

1.3.1.1 By Country

-

1.3.1.1.1 South Africa

-

1.3.1.1.2 Rest of Africa

-

-

-

1.3.2 Asia-Pacific

-

1.3.2.1 By Country

-

1.3.2.1.1 Australia

-

1.3.2.1.2 China

-

1.3.2.1.3 India

-

1.3.2.1.4 Indonesia

-

1.3.2.1.5 Japan

-

1.3.2.1.6 Malaysia

-

1.3.2.1.7 Philippines

-

1.3.2.1.8 Taiwan

-

1.3.2.1.9 Thailand

-

1.3.2.1.10 Vietnam

-

1.3.2.1.11 Rest of Asia-Pacific

-

-

-

1.3.3 Europe

-

1.3.3.1 By Country

-

1.3.3.1.1 France

-

1.3.3.1.2 Germany

-

1.3.3.1.3 Italy

-

1.3.3.1.4 Netherlands

-

1.3.3.1.5 Poland

-

1.3.3.1.6 Russia

-

1.3.3.1.7 Spain

-

1.3.3.1.8 United Kingdom

-

1.3.3.1.9 Rest of Europe

-

-

-

1.3.4 North America

-

1.3.4.1 By Country

-

1.3.4.1.1 Canada

-

1.3.4.1.2 Mexico

-

1.3.4.1.3 United States

-

1.3.4.1.4 Rest of North America

-

-

-

1.3.5 South America

-

1.3.5.1 By Country

-

1.3.5.1.1 Argentina

-

1.3.5.1.2 Brazil

-

1.3.5.1.3 Rest of South America

-

-

-

-

Dog Food Market Size FAQs

How big is the Dog Food Market?

The Dog Food Market size is expected to reach USD 96.33 billion in 2024 and grow at a CAGR of 10.21% to reach USD 156.60 billion by 2029.

What is the current Dog Food Market size?

In 2024, the Dog Food Market size is expected to reach USD 96.33 billion.