Defense Aircraft Materials Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

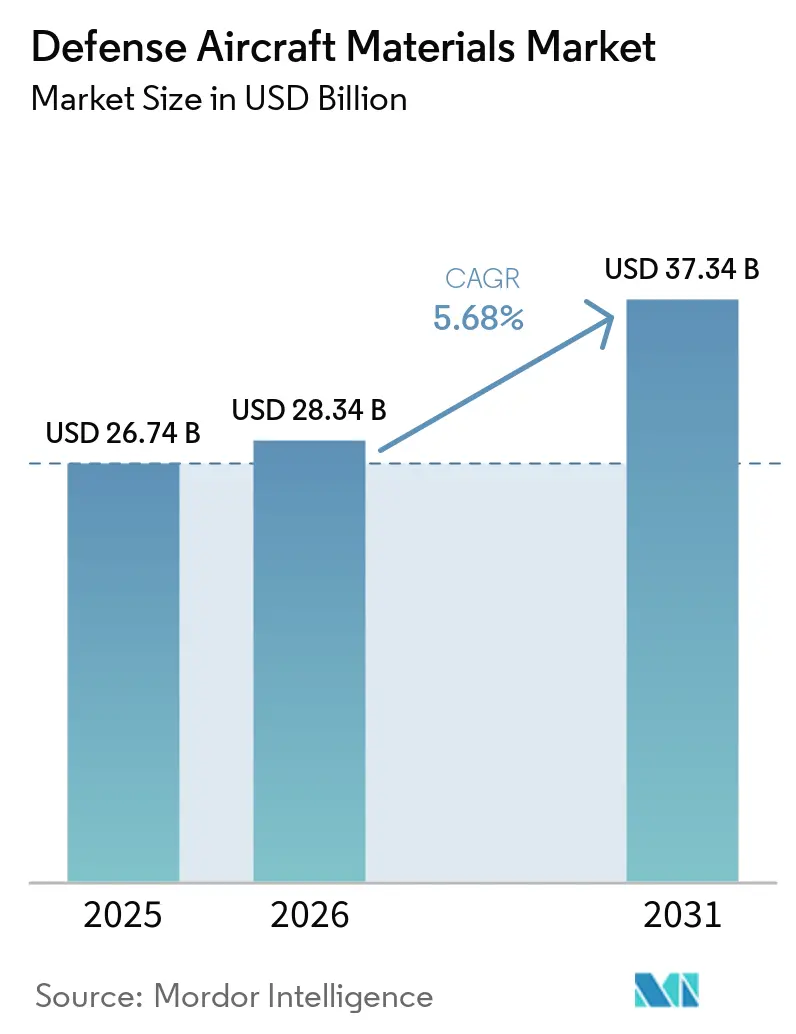

| Market Size (2026) | USD 28.34 Billion |

| Market Size (2031) | USD 37.34 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

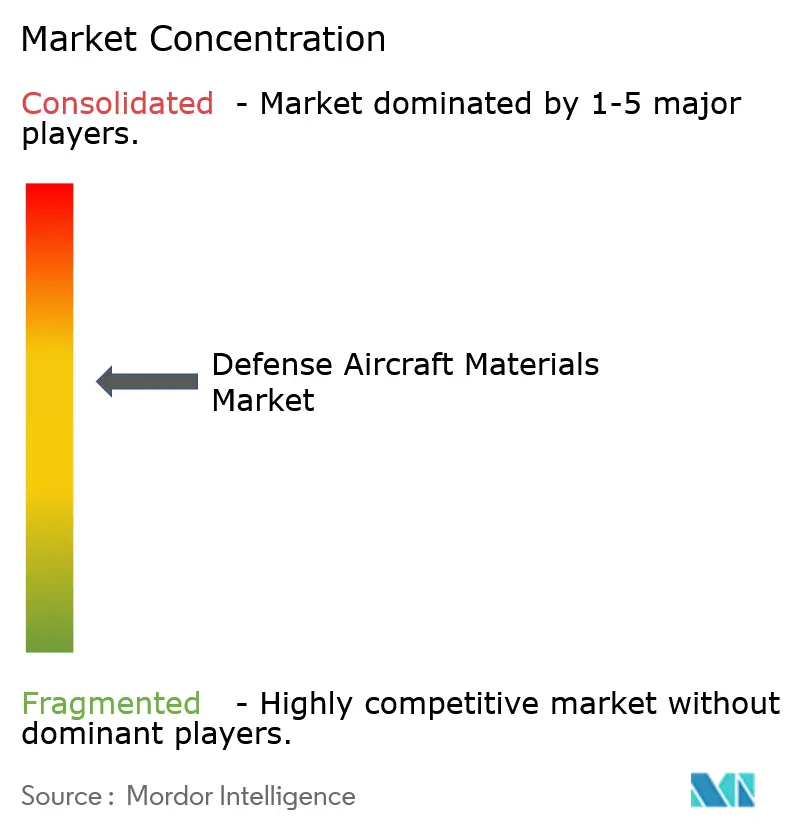

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Defense Aircraft Materials Market Analysis by Mordor Intelligence

The defense aircraft materials market size is expected to grow from USD 26.74 billion in 2025 to USD 28.34 billion in 2026 and is forecasted to reach USD 37.34 billion by 2031 at a 5.68% CAGR over 2026-2031. The consistent procurement of F-35, Rafale, and KF-21 airframes, along with depot-level engine overhauls, underpins baseline demand, even as supply chains adjust to reduced reliance on Russian titanium sponge. Original Equipment Manufacturers (OEMs) are increasingly adopting vertical integration and additive manufacturing to reduce lead times. Concurrently, air forces are allocating higher sustainment budgets toward landing-gear and turbine-disk replacements, benefiting suppliers of nickel-based super-alloys. Price fluctuations in titanium and Inconel, driven by sanctions and export controls, are prompting prime contractors to secure multi-year contracts, transferring cost risks to downstream suppliers. In the Asia-Pacific region, programs such as India’s Tejas and South Korea’s KF-21 are accelerating the localization of forging capacities, reshaping global sourcing strategies. Additionally, the demand for lightweight materials continues to drive the use of titanium and aluminum-lithium alloys in both new production and retrofit projects, thereby mitigating some of the pressure from the substitution of composite materials and supporting the growth of the defense aircraft materials market through 2031.

Key Report Takeaways

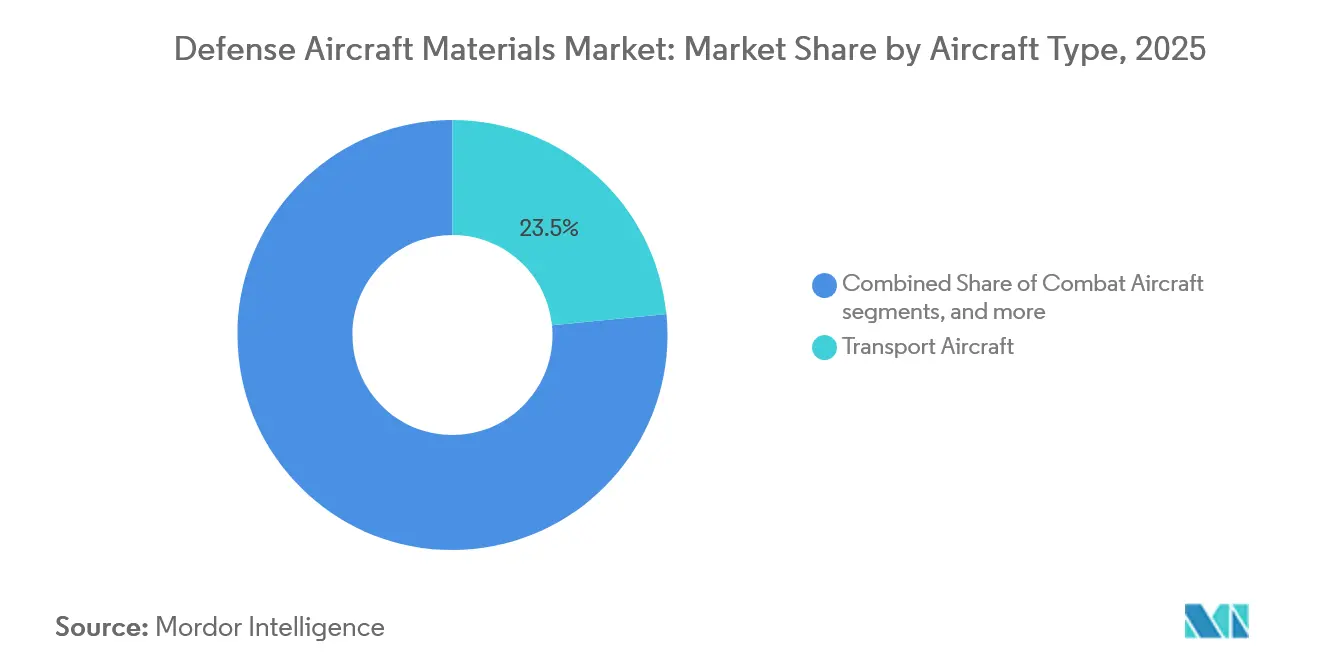

- By aircraft type, transport aircraft led the defense aircraft materials market, accounting for 23.45% of the market share in 2025; multi-role platforms are forecast to expand at a 5.76% CAGR through 2031.

- By material type, aluminum alloys accounted for 37.95% of the defense aircraft materials market in 2025, while titanium alloys are projected to have the highest CAGR of 5.83% through 2031.

- By component, airframe structures accounted for 33.64% of the revenue in 2025; engine systems are projected to advance at a 5.25% CAGR through 2031.

- By end-user phase, linefit applications accounted for 69.05% of the defense aircraft materials market in 2025, whereas retrofit activity is projected to post a 5.05% CAGR through 2031.

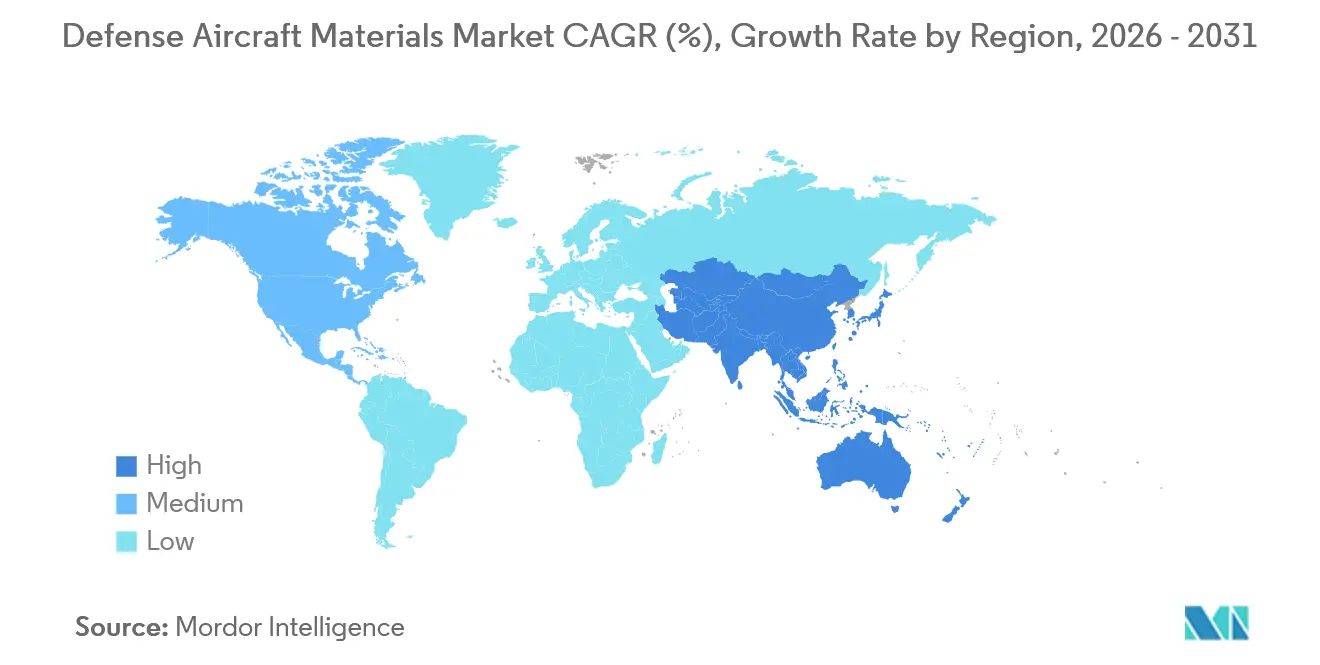

- By geography, North America accounted for 33.69% of the revenue in 2025; the Asia-Pacific region is projected to record the fastest regional CAGR of 5.96% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Defense Aircraft Materials Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Defense modernization budgets rising | +1.20% | Global, with concentration in North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Lightweight-materials imperative for fuel savings | +0.90% | Global, led by North America and Europe for legacy fleet upgrades | Long term (≥ 4 years) |

| Expanding global MRO demand for aging fleets | +1.10% | North America, Europe, Middle East | Short term (≤ 2 years) |

| On-shoring and recycling to mitigate strategic-metal risk | +0.70% | North America, Europe, Asia-Pacific (India, South Korea, Japan) | Long term (≥ 4 years) |

| Certified metal additive manufacturing adoption | +0.60% | North America, Europe | Medium term (2-4 years) |

| OEM single-aisle production ramp-ups through 2030 | +0.80% | Global, anchored by North America OEM hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Defense Modernization Budgets Rising

Pentagon's aircraft expenditures increased by 8% in fiscal 2025, allocating USD 52 billion for F-35 Block 4 upgrades, which require new titanium bulkheads and aluminum wing spars. European NATO members increased defense spending by 6% in 2025, funding Eurofighter Typhoon life-extension contracts that led to a 15% rise in aluminum-plate consumption compared to 2024. India allocated USD 28 billion for fiscal 2025-26 capital purchases, including 83 Tejas Mk1A fighters that utilize locally forged aluminum-lithium extrusions. South Korea budgeted USD 3.2 billion for KF-21 serial production, sourcing titanium forgings from domestic presses to avoid potential delays in obtaining export licenses. China’s official 2025 defense budget increased by 7.2%, with analysts estimating an additional 30% embedded in military-civil programs to accelerate J-20 production. These developments collectively expand the defense aircraft materials market as both new production and overhaul activities intensify.

Lightweight-Materials Imperative for Fuel Savings

NATO air forces spend over USD 10 billion annually on aviation fuel, prompting procurement teams to prioritize aluminum-lithium and titanium alloys that reduce airframe weight by 8-12%.[1]National Academies of Sciences, Engineering, and Medicine, “Lightweighting Technologies for Military Vehicles and Aircraft,” nasem.edu The KC-46 tanker features aluminum 7085 frames, which reduce aircraft weight by 1,320 pounds (600 kg) and achieve a 4% lifetime fuel savings. Ti-6Al-4V accounts for 15% of the F-35’s structural mass, concentrated in engine pylons and wing-root fittings, where its 40% strength advantage over steel justifies its higher cost. Airbus employs an aluminum-lithium alloy, 2195, in the A400M cargo panels, which reduces structural weight by 10% and extends the range by 200 nautical miles. Sikorsky’s CH-53K integrates titanium rotor heads, cutting 450 kg from empty weight and enabling an additional 1,800 kg payload. These material specifications drive investments in forging and extrusion processes, supporting long-term growth in the defense aircraft materials market.

Expanding Global MRO Demand for Aging Fleets

The average age of US tactical aircraft reached 29 years in 2025, resulting in a USD 9.4 billion depot-maintenance expenditure that included replacing corroded aluminum spars and fatigued titanium trunnions. Germany allocated EUR 400 million (USD 467.08 million) for Tornado overhauls, focusing on aluminum skin and titanium engine-mount upgrades through 2030. Middle Eastern operators face corrosion rates 40% higher than those in temperate regions, resulting in increased demand for aluminum fairings and titanium fasteners. India committed USD 1.2 billion to deep overhauls of MiG-29 and Jaguar fleets, replacing steel brackets with titanium inserts. Even the relatively new F-35 program has a USD 1.3 trillion lifetime sustainment budget, which includes frequent replacement of nickel turbine blades and titanium disks. Increased flight hours and delayed retirements are driving aftermarket growth in the defense aircraft materials market.

Certified Metal Additive Manufacturing Adoption

In 2024, the FAA approved GE Aerospace’s laser-sintered F110 engine sump cover, reducing procurement lead times from 18 months to 6 months. Honeywell introduced titanium brackets that are 30% lighter than machined parts, consolidating four components into a single printed piece. Materialise achieved EN 9100 certification in 2024, enabling direct delivery of aluminum hydraulic manifolds to Airbus and eliminating 12-week tooling cycles. The US Air Force printed over 50,000 metal parts in 2025, achieving 40% unit-cost savings and enabling on-site spare part production at forward bases. NASA’s 2024 qualification framework standardized fatigue-test protocols, addressing a significant barrier to adoption. Although certified additive manufacturing accounts for less than 2% of total component mass, it enhances supply chain resilience and mitigates supply disruptions in the defense aircraft materials market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in titanium and super-alloy prices | -0.80% | Global, acute in Europe and Asia-Pacific dependent on Russian supply | Short term (≤ 2 years) |

| Substitution threat from composites | -0.50% | Global, led by North America OEM adoption | Long term (≥ 4 years) |

| Export-controlled titanium-sponge shortfalls | -0.60% | Europe, Asia-Pacific, North America (secondary) | Medium term (2-4 years) |

| REACH/PFAS bans raising coating costs | -0.40% | Europe, with spillover to North America and Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Titanium and Super-Alloy Prices

Titanium sponge prices surged by 45% between January 2024 and December 2025 due to sanctions that disrupted VSMPO-AVISMA’s 35% share of the global aerospace supply.[2]Reuters, “Titanium Prices Surge Amid Russian Export Restrictions,” reuters.com While Boeing and Airbus reopened US sponge production facilities, costs remain 30% higher than Russian supply, leading to increased billet prices and extended lead times of up to 26 weeks. Nickel-based Inconel and Hastelloy spot prices rose by 28% in 2025, driven by Indonesian ore-export taxes and Chinese restrictions on rare earths, further tightening turbine-disk supply. Original Equipment Manufacturers (OEMs) have passed these risks downstream through fixed-price contracts, compressing the margins of tier-two suppliers and moderating growth in the defense aircraft materials market.

Substitution Threat from Composites

Carbon-fiber composites now constitute 25% of the F-35’s structural mass, replacing aluminum in wing skins and fuselage panels. Boeing’s 787 production model, adapted for military derivatives, eliminated 40,000 aluminum rivets per airframe. Airbus extended composite usage to the A400M’s outer wing box, reducing structural weight by 800 kg. However, composites are unsuitable for high-temperature zones such as engine pylons (600 °C) or areas subject to landing-gear impact loads, ensuring continued demand for titanium and steel in these applications. Additionally, the complexity of repairs and susceptibility to high-humidity coating degradation limit the complete substitution of metallic hard points, sustaining demand for metallic parts in the defense aircraft materials market and mitigating risks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Multi-Role Platforms Drive Metallic Complexity

Multi-role fighters are projected to grow at a 5.76% CAGR, surpassing the overall defense aircraft materials market. This growth is driven by air forces consolidating their fleets around twin-engine platforms that require high-strength titanium bulkheads and aluminum spars designed for 9 g maneuvers.[3]U.S. Air Force, “Depot Maintenance Operations Report FY2024,” af.mil Transport aircraft are expected to account for 23.45% of revenue in 2025, supported by sustainment programs for C-130J and A400M, which consume significant volumes of aluminum extrusions and titanium landing-gear forgings. Combat-air-superiority fighters, despite smaller procurement runs, incorporate dense titanium and super-alloy content in engine bays and weapons pylons. Trainers and rotorcraft contribute steady but lower-value demand, with aluminum-lithium fuselages and titanium rotor-head assemblies driving aftermarket orders. Harsh operational environments, such as desert dust and maritime salt spray, accelerate corrosion, reducing replacement cycles and boosting aftermarket demand.

Fixed-wing platforms dominate volume concentration due to their larger structures compared to rotorcraft. Multi-role designs also integrate more metallic components than single-mission predecessors, ensuring a sustained demand for titanium and aluminum components. This trend supports continued growth in the defense aircraft materials market, even as composite materials gain traction.

By Material Type: Titanium Gains as Aluminum Holds Volume

Aluminum alloys are expected to remain dominant, accounting for 37.95% of revenue in 2025, due to their widespread use in fuselage frames and wing ribs where cost efficiency is critical. Titanium alloys, however, are projected to grow at a 5.83% CAGR through 2031, driven by applications in compressor blades, landing gear, and pylons, where weight reduction directly enhances combat radius. Super-alloys and refractory metals, while niche, are indispensable for turbine-inlet temperatures exceeding 1,100 °C, securing their role in engine components.

High-strength steels continue to be used in landing-gear trunnions and arresting hooks, which require exceptional toughness. Aluminum-lithium alloys, offering a 10% weight reduction over traditional aluminum at moderate cost premiums, are expanding their presence in retrofit programs. The material mix positions titanium as the value leader and aluminum as the volume anchor, ensuring resilience in the defense aircraft materials market.

By Component: Engine Systems Accelerate Amid Sustainment Pressures

Airframe structures are expected to contribute 33.64% of revenue in 2025, while engine systems are projected to grow at a 5.25% CAGR. This growth is driven by depot overhauls for F135 and F110 engines, which require nickel turbine disks and titanium compressor blades to be replaced on 3,000-hour cycles.

Landing-gear assemblies maintain consistent demand due to high sortie rates, while avionics housings grow in line with radar-upgrade programs, which require precision-machined aluminum enclosures. Incremental gains in interiors are driven by VIP conversions adopting aluminum-lithium seat frames. Regulatory changes, such as bans on hexavalent chromium and PFAS, are prompting the reformulation of coatings and sealants, which increases consumable costs and adds compliance-related premiums across the defense aircraft materials market.

By End-User Phase: Linefit Dominance Reflects New-Build Momentum

Linefit deliveries are expected to account for 69.05% of revenue in 2025, supported by multi-year orders for F-35, Rafale, and KF-21 aircraft, which ensure predictable titanium and aluminum volumes for qualified suppliers. Retrofit growth is projected at a 5.05% CAGR, as budgets prioritize fifth-generation acquisitions.

However, aging fleets of F-16, Tornado, and C-130 aircraft require periodic wing-life extensions and landing-gear replacements, sustaining a USD 2 billion retrofit segment by 2031. The defense aircraft materials market balances steady linefit pipelines with aftermarket opportunities driven by fleet aging.

Geography Analysis

North America is expected to account for 33.69% of the revenue in 2025, driven by USD 52 billion in Pentagon aircraft expenditures and a domestic metals industry that produces 40,000 tons of aerospace-grade aluminum and 8,000 tons of titanium annually. The Asia-Pacific region is projected to grow at the fastest rate, with a 5.96% CAGR, fueled by China’s J-20 production reaching 80 units per year, India’s Atmanirbhar Bharat sourcing mandates, and South Korea’s KF-21 program securing local bulkhead and spar production. Europe, although trailing in market share, benefits from FCAS and Tempest programs, which aim to localize the procurement of super-alloys and titanium within the region, channeling orders to companies such as Safran and Airbus Aerostructures (Airbus SE).

Regional supply chains are undergoing significant changes. US sponge restarts and Polish forging capacity expansions reduce trans-Atlantic dependencies, while Asian governments subsidize forging facilities to enhance strategic autonomy. In the Middle East, aftermarket demand for F-15SA and Rafale fleets remains strong, although limited domestic forging capacity restricts the capture of value. South America remains a niche market, anchored by Brazil’s KC-390 program and driven by offset requirements for local content. Overall, shifting production hubs are redistributing growth, while absolute volume increases across all regions reinforce the global diversification of the defense aircraft materials market.

Competitive Landscape

The top five suppliers, Howmet, GKN, Safran, VSMPO-AVISMA, and Airbus Aerostructures (Airbus SE), control approximately 40% of global titanium-forging and aluminum-extrusion capacity, indicating moderate market concentration. Howmet’s 2026 Indiana isothermal press is expected to reduce waste by 30% and shorten lead times by eight months, showcasing the impact of capital investments. Safran and GKN’s 2025 joint venture aims to establish a EUR 300 million (USD 350.38 million) French forging hub, targeting 70% European content for FCAS components. ATI’s Utah sponge restart and Hanwha’s upstream titanium smelter highlight national strategies to secure defense programs against potential sanctions. Certified additive manufacturing is emerging as a growth area, with GE Aerospace’s FAA-approved printed compressor blade demonstrating the potential for on-demand spares that bypass traditional forging processes.

Competitive intensity is increasing as European and US primes compete for limited non-Russian sponge supplies, while Indian and South Korean entrants leverage subsidized capital to undercut Western costs by 20%. Patent activity is focused on titanium aluminide isothermal forging, with Howmet filing 12 patents in 2024-25 alone. The defense aircraft materials market is characterized by a balance between established incumbents and emerging regional players amid a fragmented supply chain.

Defense Aircraft Materials Industry Leaders

Howmet Aerospace Inc.

Safran S.A.

PJSC VSMPO-AVISMA Corporation

Airbus Aerostructures (Airbus SE)

GKN Aerospace Services Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Aerovironment secured a USD 20 million contract for Ceramics Advanced Materials and Processes (CAMP) from the Air Force Research Laboratory (AFRL) Materials and Manufacturing Directorate. The contract aims to advance next-generation ceramic and ceramic matrix composite materials (CMCs) for aerospace and defense applications under extreme conditions, supporting the U.S. Air and Space Forces. Over the 39 months, Aerovironment's materials experts will collaborate with AFRL scientists and engineers at Wright-Patterson Air Force Base in Dayton, Ohio. The focus will be on accelerating development, deploying advanced capabilities more quickly, and enhancing mission readiness while reducing lifecycle costs. The project will utilize advanced additive manufacturing, three-dimensional (3D) printing, and sensor integration techniques to develop lightweight, thermally resilient structures, including high-speed aerodynamic vehicles, turbine engines, rocket propulsion systems, transparent armor, thermal-protection tiles, and nozzle extensions.

- June 2025: AeroVironment, Inc., a global leader in defense technology innovation, was awarded a USD 20 million contract from the Air Force Research Laboratory (AFRL) Materials and Manufacturing Directorate. The contract, titled Ceramics Advanced Materials and Processes (CAMP), aims to enhance next-generation ceramic and ceramic matrix composite materials (CMCs) for demanding aerospace and defense applications, bolstering support for the US Air and Space Forces.

- March 2025: Korea Aerospace Industries (KAI) and Hanwha Aerospace secured contracts exceeding KRW 3 trillion (approximately USD 2.2 billion) to manufacture additional KF-21 fighter aircraft and General Electric F414 engines for the Republic of Korea Air Force (RoKAF). The new agreement, awarded by the Defense Acquisition Program Administration (DAPA), allocates KRW 2.39 trillion (approximately USD 1.75 billion) to KAI, with the contract set to extend through December 2028. Hanwha Aerospace's contract, valued at KRW 623.2 billion (approximately USD 456 million), includes the licensed production of 40 additional F414 engines and related spare parts.

Global Defense Aircraft Materials Market Report Scope

The defense aircraft materials market comprises materials forged, cast, extruded, machined, or additively manufactured from aluminum, titanium, steel, and nickel-based alloy components that form the primary structures, engine elements, landing-gear assemblies, and ancillary fittings of military and government-operated aircraft. The study of defense aircraft materials market covers the production, installation, maintenance, repair, and overhaul of these components across combat, transport, trainer, and mission-support fixed-wing aircraft and rotorcraft. The market also captures component-level replacement cycles occurring during depot overhauls of engines, landing gear, and structural sub-assemblies.

The defense aircraft materials market is segmented by aircraft type, material type, component, end-user phase, and geography. By aircraft type, the market is segmented into fixed-wing aircraft and rotorcraft. By material type, the market is segmented into aluminum alloys, titanium alloys, high-strength steels, super-alloys, and other specialty metals. By component, the market is segmented into airframe structures, engine systems, avionics and electronics housings, landing gear and braking systems, interiors and seating, and coatings, sealants, and consumables. By the end-user phase, the market is segmented into linefit (OEM production) and retrofit (maintenance, repair, and overhaul). By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. The market sizing and forecasts have been provided in value (USD billion) for all the above segments.

| Fixed-Wing Aircraft | Combat Aircraft |

| Multi-role Aircraft | |

| Training Aircraft | |

| Transport Aircraft | |

| Other Aircraft | |

| Rotorcraft | Multi-Mission Helicopter |

| Transport Helicopter | |

| Other Helicopter |

| Aluminum Alloys |

| High-Strength Steels |

| Titanium Alloys |

| Composite Materials |

| Super-alloys and Refractory Metals |

| Specialty Polymers and Adhesives |

| Airframe Structures |

| Engine Systems |

| Avionics and Electronics Housings |

| Landing Gear and Braking Systems |

| Interior and Seating |

| Coatings, Sealants and Consumables |

| Linefit |

| Retrofit |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest OF Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Aircraft Type | Fixed-Wing Aircraft | Combat Aircraft | |

| Multi-role Aircraft | |||

| Training Aircraft | |||

| Transport Aircraft | |||

| Other Aircraft | |||

| Rotorcraft | Multi-Mission Helicopter | ||

| Transport Helicopter | |||

| Other Helicopter | |||

| By Material Type | Aluminum Alloys | ||

| High-Strength Steels | |||

| Titanium Alloys | |||

| Composite Materials | |||

| Super-alloys and Refractory Metals | |||

| Specialty Polymers and Adhesives | |||

| By Component | Airframe Structures | ||

| Engine Systems | |||

| Avionics and Electronics Housings | |||

| Landing Gear and Braking Systems | |||

| Interior and Seating | |||

| Coatings, Sealants and Consumables | |||

| By End-User Phase | Linefit | ||

| Retrofit | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest OF Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the defense aircraft materials market?

It stands at USD 28.34 billion in 2026 and is projected to reach USD 37.34 billion by 2031, reflecting a 5.68% CAGR.

Which material contributes the largest revenue share today?

Aluminum alloys lead with 37.95% share, thanks to their widespread use in fuselage frames, wing ribs, and control-surface structures.

Why are titanium alloys growing faster than other metals?

They deliver a 40% weight advantage over steel and tolerate 600 °C engine-pylon heat, driving a 5.83% CAGR through 2031.

How do sanctions on Russian titanium affect supply chains?

Sanctions removed 35% of global aerospace-grade sponge capacity, lifting prices 45% and stretching billet lead times to 26 weeks.

What role does additive manufacturing play in metallic-parts production?

FAA-certified printed titanium engine components now trim lead times from 18 months to 6 months and cut costs by about 40%, though they still account for under 2% of total component mass.

Which region is expected to post the fastest growth to 2031?

Asia-Pacific, at a 5.96% CAGR, fueled by China’s J-20 ramp-up, India’s Tejas and AMCA programs, and South Korea’s KF-21 serial production.

Page last updated on: