| Study Period | 2019 - 2030 |

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

| CAGR | 7.04 % |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Europe |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order |

DC Distribution Network Market Analysis

The DC Distribution Network Market is expected to register a CAGR of 7.04% during the forecast period.

The DC distribution network industry is experiencing significant transformation driven by the global shift towards renewable energy integration and distributed power generation. The dramatic decline in costs of key technologies has been a major catalyst, with solar PV panels and lithium-ion batteries seeing price reductions of nearly 90% over the past decade. This cost reduction has made DC distribution networks increasingly viable for both commercial and residential applications. The integration of renewable energy sources with DC distribution networks has become particularly attractive as it eliminates the need for multiple conversion stages, thereby improving overall system efficiency and reliability.

The data center industry has emerged as a key driver of DC distribution network adoption, with infrastructure deployment reaching unprecedented levels. As of January 2022, the United States led global data center deployment with 2,751 facilities, followed by Germany with 484 and the United Kingdom with 458 facilities. The industry is witnessing a paradigm shift towards DC power distribution due to its inherent advantages in reducing power conversion stages, improving energy efficiency, and providing better compatibility with renewable energy sources and energy storage systems. Major technology companies are increasingly adopting DC distribution systems in their new data center projects to optimize power delivery and reduce operational costs.

The electric vehicle charging infrastructure sector is witnessing rapid expansion and technological advancement, creating new opportunities for DC distribution networks. The market is experiencing significant momentum in fast-charging infrastructure development, with companies introducing innovative DC microgrid architectures for charging stations. These systems are particularly advantageous as they allow operators to share centralized power sources across multiple charging points, optimizing infrastructure utilization and reducing installation costs. The integration of solar PV systems with DC charging infrastructure is becoming increasingly common, creating self-sufficient charging stations that reduce grid dependency.

The industry is witnessing significant technological innovations and strategic partnerships aimed at advancing DC distribution network capabilities. Companies are developing new hardware solutions specifically designed for DC distribution systems, including servers, air conditioning units, and building controls. In the residential sector, Australia has demonstrated remarkable progress in distributed energy integration, with installed rooftop solar capacity reaching 25.3 GW in 2021. This growth is accompanied by increasing adoption of battery storage systems and smart DC distribution technologies that enable better energy management and grid integration.

DC Distribution Network Market Trends

Growing Electric Vehicle Adoption and DC Fast Charging Infrastructure

The rapid expansion of electric vehicles globally has created significant demand for efficient charging infrastructure, particularly DC fast charging solutions. A key technical advantage driving DC distribution network adoption is that electric vehicles only accept DC power for charging their batteries. High-powered DC charging stations have demonstrated the ability to charge approximately 80% of a typical EV's battery capacity in under 10 minutes, compared to several hours required for AC charging. This dramatic reduction in charging time is achieved by bypassing the AC-DC conversion process and delivering DC power directly to the vehicle's battery system.

The fundamental compatibility between EVs and DC power systems has led governments across major markets to emphasize DC distribution networks in their charging infrastructure planning. Technical standards and incentive programs specifically targeting fast-DC charging equipment have been implemented across the United States, China, and the European Union. These policy frameworks recognize that DC distribution networks eliminate multiple power conversion steps in the charging process, improving overall system efficiency while reducing equipment costs and spatial requirements at charging stations. The elimination of AC-DC conversion stages also results in lower power losses and reduced maintenance requirements for charging infrastructure operators.

Understand The Key Trends Shaping This Market

Download PDF

Rising Renewable Energy Integration and Distributed Generation

The increasing deployment of distributed renewable energy sources, particularly solar photovoltaic (PV) systems, is driving demand for DC distribution networks that can efficiently manage variable power generation. Solar PV systems inherently generate DC power, making DC distribution networks an ideal choice for minimizing conversion losses and maximizing system efficiency. The integration of DC distribution systems allows direct utilization of solar-generated DC power for various applications, eliminating the need for multiple conversion stages that typically result in 5-15% power losses in traditional AC systems.

The technical advantages of DC distribution networks become particularly evident in applications combining renewable generation with energy storage systems. These networks enable seamless integration of solar PV, battery storage, and DC loads while maintaining high system efficiency and power quality. For instance, in commercial and industrial applications, DC distribution networks allow direct coupling of rooftop solar installations with battery storage systems and DC-powered equipment such as LED lighting, HVAC systems, and electric vehicle charging stations. This direct DC power utilization approach not only improves overall system efficiency but also reduces the complexity and maintenance requirements of power distribution infrastructure.

Data Center Power Optimization and Energy Efficiency

Data centers represent a primary driver for DC distribution network adoption due to their inherent compatibility with DC-powered IT equipment and the potential for significant energy efficiency improvements. According to industry estimates, traditional AC distribution systems in data centers lose approximately 50% of power through conversion processes and heat management. DC distribution networks can substantially reduce these losses by eliminating multiple conversion stages and simplifying power delivery to servers and cooling systems. The implementation of DC distribution systems has demonstrated the ability to reduce copper usage by up to 40% compared to equivalent AC systems, while also requiring approximately 25% less floor space.

The technical benefits of DC distribution networks extend beyond energy efficiency to include improved power quality and reliability in data center operations. DC systems inherently eliminate power quality issues such as harmonics and phase load balancing that are common in AC distribution systems, reducing the need for power conditioning equipment. Furthermore, DC distribution networks facilitate easier integration of renewable energy sources and energy storage systems, supporting data centers' increasing focus on sustainability and carbon reduction goals. The simplified power distribution architecture of DC systems, with fewer components and potential points of failure, also contributes to improved system reliability and reduced maintenance requirements.

Energy Storage Systems Integration

The growing deployment of energy storage systems (ESS) across various applications has emerged as a significant driver for DC distribution networks. Battery energy storage systems naturally operate on DC power, making DC distribution networks the most efficient solution for integrating these systems with both power sources and loads. The elimination of multiple conversion stages in DC distribution systems not only improves overall system efficiency but also reduces the complexity and cost of energy storage installations. This technical advantage becomes particularly important as battery storage systems are increasingly deployed for applications ranging from renewable energy integration to grid stability services.

The compatibility between DC distribution networks and energy storage systems extends to both utility-scale and distributed applications. In commercial and industrial settings, DC distribution networks enable direct coupling of battery storage systems with on-site renewable generation and DC loads, maximizing system efficiency and operational flexibility. The ability to maintain power quality and manage variable renewable generation through integrated energy storage becomes more effective with DC distribution networks, as they eliminate the power quality issues typically associated with AC systems. This technical synergy between DC distribution networks and energy storage systems has become particularly important in applications such as microgrids and backup power systems, where efficient energy storage integration is crucial for system reliability and performance.

Segment Analysis: Voltage

Low and Medium Voltage Segment in DC Distribution Network Market

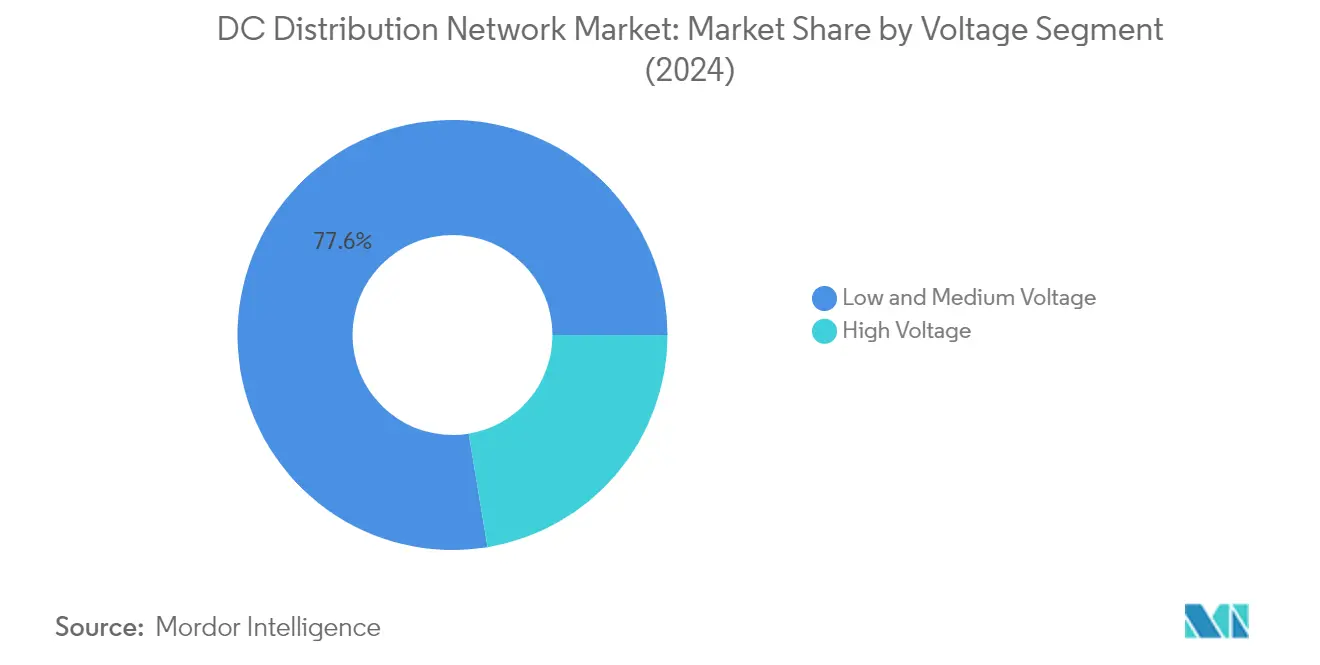

The Low and Medium Voltage segment dominates the DC distribution network market, accounting for approximately 78% of the total market share in 2024. This segment operates within voltage levels up to 750V DC, which can be used directly without further voltage reduction. The significant market share can be attributed to its widespread application across various sectors, including EV charging equipment, data centers, telecommunication infrastructure, lighting systems, and electronic devices. The segment's dominance is further strengthened by the increasing adoption of renewable power systems, particularly solar photovoltaic installations, as they are more easily interfaced with DC grids compared to AC grids. Additionally, the segment benefits from the growing deployment of battery energy storage systems and the expanding electric vehicle charging infrastructure globally.

Low and Medium Voltage Segment in DC Distribution Network Market

The Low and Medium Voltage segment is also projected to be the fastest-growing segment in the DC distribution network market from 2024 to 2029. This growth is primarily driven by the rapid expansion of data center infrastructure globally, with major investments flowing into regions like North America and Asia-Pacific. The segment's growth is further accelerated by the increasing adoption of electric vehicles and the corresponding need for charging infrastructure. The integration of renewable energy sources, particularly solar PV systems, with DC distribution networks is another key factor propelling the segment's growth. Additionally, the declining costs of battery energy storage systems and the growing trend toward distributed power generation are expected to provide significant momentum to the segment's expansion during the forecast period.

Segment Analysis: End User

Commercial and Industrial Segment in DC Distribution Network Market

The Commercial and Industrial (C&I) segment dominates the DC distribution network market, accounting for approximately 66% of the total market share in 2024. This segment's prominence is primarily driven by its widespread application in commercial facilities, including data centers, telecom sites, and hospitals. The segment has shown particularly strong growth potential, especially in the data center sector where companies like Comcast and Verizon are already operating their facilities on DC power. The adoption of DC distribution networks in this segment is fueled by several advantages, including reduced power conversion losses, decreased copper usage (up to 40% less in marine applications), and lower cooling requirements. Additionally, DC distribution systems require approximately 25% less floor space, which increases available space for server racks and cooling equipment, while their simpler design with fewer components reduces the probability of system failure.

Residential Segment in DC Distribution Network Market

The residential segment has emerged as a significant market for DC distribution networks, driven by the declining costs of renewable energy installation and generation. This segment has gained traction as most home appliances, such as CFLs, LEDs, refrigerators, televisions, fans, air conditioners, laptops, and other electronics, are inherently DC loads. The integration of residential solar PV systems and energy storage solutions has further catalyzed the adoption of DC distribution networks in homes. The segment's growth is particularly notable in regions with high rooftop solar PV penetration, such as North America and Europe, where government incentives and favorable policies continue to drive residential solar installations. The residential DC distribution systems typically operate at various DC voltages, including 120V, 230V, 325V, and 380V/400V, offering optimized solutions for different household power requirements.

DC Distribution Network Market Geography Segment Analysis

DC Distribution Network Market in North America

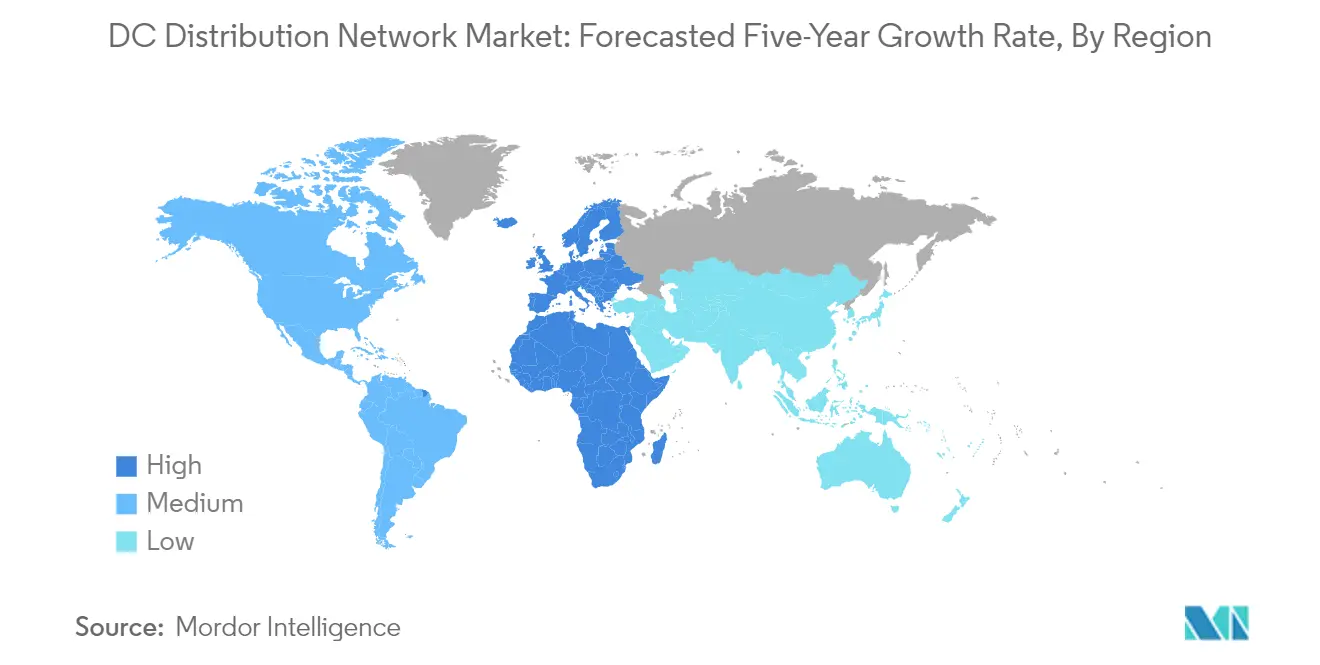

North America represents a dominant force in the global DC distribution network market, commanding approximately 25% of the market share in 2024. The region's leadership position is driven by its highly industrialized economy and the highest per capita power consumption globally. The market is characterized by robust growth in energy storage installations and increasing deployment of distributed renewable energy systems across the United States, Canada, and Mexico. The region's strong focus on data center infrastructure, coupled with the rapid adoption of electric vehicles and charging networks, continues to drive market expansion. Additionally, the presence of major technology companies and their increasing investments in DC-powered facilities has strengthened the market position. The region's advanced regulatory framework and supportive government policies for renewable energy integration and distributed power generation have created a favorable environment for market growth. Furthermore, the increasing focus on grid modernization and the development of smart cities has created additional opportunities for DC distribution network deployments.

DC Distribution Network Market in Europe

Europe has demonstrated remarkable growth in the DC distribution network market, achieving approximately 6% annual growth from 2019 to 2024. The region's market expansion is underpinned by its position as one of the largest renewable energy markets globally, with a strong focus on distributed power generation and energy storage solutions. The European market is characterized by advanced technological adoption and innovative DC distribution projects across various sectors, including commercial buildings, data centers, and industrial facilities. The region's commitment to carbon neutrality and sustainable energy practices has driven significant investments in DC infrastructure. The market has particularly benefited from the growing adoption of renewable energy systems in countries like Germany, France, and the United Kingdom. The presence of major industry players and research institutions has fostered continuous innovation in DC distribution technologies. Furthermore, the region's robust standardization efforts and regulatory framework have created a stable environment for market development, while the increasing focus on energy efficiency and grid modernization continues to drive market growth.

DC Distribution Network Market in Asia-Pacific

The Asia-Pacific DC distribution network market is positioned for substantial growth, with projections indicating approximately 9% annual growth from 2024 to 2029. The region's market dynamics are driven by rapidly increasing electricity demand and the growing need for efficient electrical infrastructure. The market is characterized by significant investments in renewable energy integration, particularly in countries like India, Japan, and Australia. The region's rapid industrialization and urbanization have created substantial opportunities for DC distribution network deployments, especially in new infrastructure developments. The market has been particularly active in the development of smart cities and modern industrial facilities that leverage DC distribution systems. The increasing focus on energy efficiency and the adoption of distributed energy resources have created favorable conditions for market expansion. Additionally, the region's growing data center industry and the rapid adoption of electric vehicles have emerged as key drivers for DC distribution network implementations. The market is further supported by government initiatives promoting clean energy adoption and grid modernization across various countries in the region.

DC Distribution Network Market in China

China represents a crucial market in the global DC distribution networks market, driven by its position as the global leader in renewable energy deployment and electric vehicle adoption. The market is characterized by significant investments in grid modernization and the development of smart cities. The country's commitment to achieving carbon neutrality has accelerated the adoption of DC distribution networks, particularly in commercial and industrial applications. The market benefits from strong domestic manufacturing capabilities and a robust supply chain for DC distribution equipment. The country's focus on technological innovation and research in power distribution systems has led to the development of advanced DC distribution solutions. Additionally, the rapid expansion of data center infrastructure and the growing adoption of distributed energy resources have created substantial opportunities for market growth. The presence of numerous domestic manufacturers and suppliers has fostered competitive pricing and technological advancement in the sector.

DC Distribution Network Market in Rest of the World

The Rest of the World market, encompassing regions such as South America and the Middle East & Africa, demonstrates significant potential in the DC distribution network sector. These regions are characterized by rapidly growing electricity demand and substantial untapped potential for renewable energy integration. The market is driven by improving economic conditions and increasing investments in power infrastructure modernization. The adoption of DC distribution networks is particularly relevant in remote and off-grid applications, where traditional AC distribution may not be economically viable. The market benefits from increasing awareness of energy efficiency and the growing focus on sustainable development. The oil-led economies in the Middle East are diversifying their energy infrastructure, creating new opportunities for DC distribution network deployments. Additionally, the growing focus on industrial development and the expansion of data center infrastructure in these regions are creating new avenues for market growth.

Get Analysis on Important Geographic Markets

Download PDF

DC Distribution Network Industry Overview

Top Companies in DC Distribution Network Market

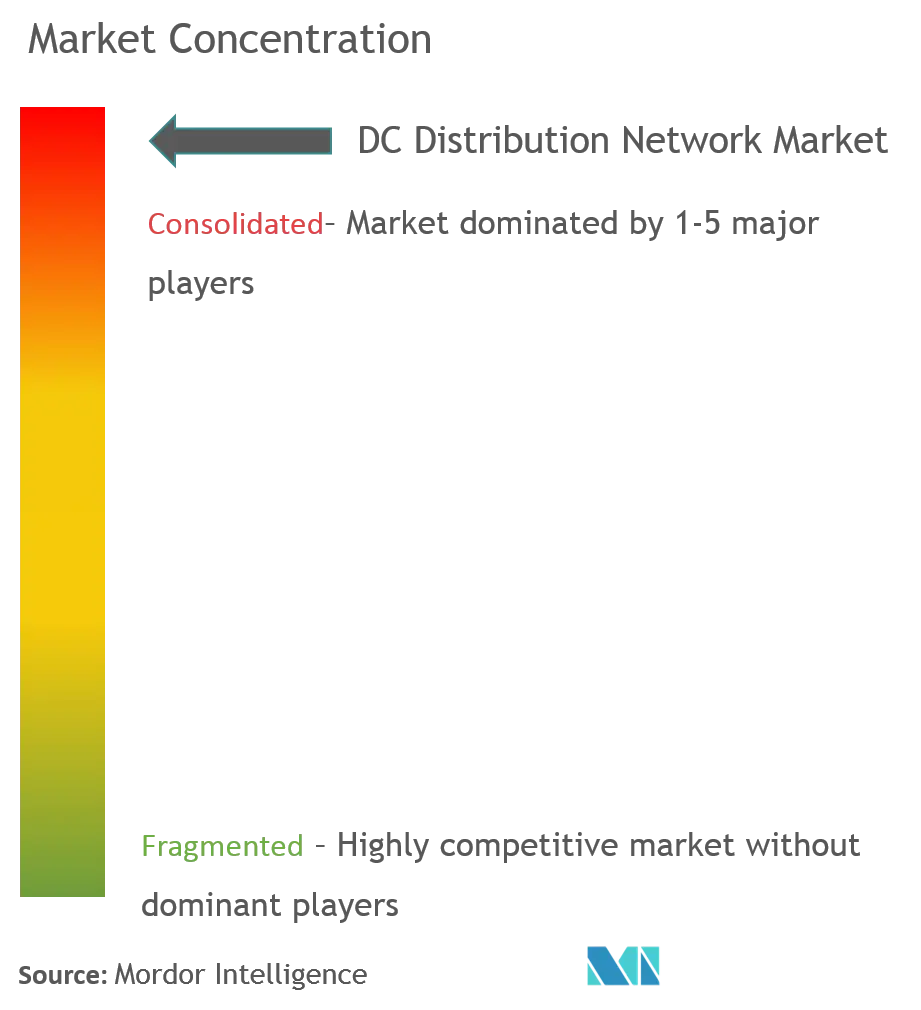

The DC distribution network market features prominent players like ABB, Siemens, Vertiv Group, Eaton Corporation, and Secheron SA, leading the industry through continuous innovation and strategic expansion. Companies are focusing on developing advanced power conversion technologies and smart distribution network solutions while expanding their product portfolios through research and development initiatives. The industry witnesses active collaboration between established players and technology startups to enhance capabilities in areas like power electronics and control systems. Market leaders are increasingly emphasizing sustainable solutions and energy efficiency improvements in their product offerings while simultaneously expanding their geographical presence through strategic partnerships and distribution agreements. These companies are also investing in manufacturing facilities and innovation centers across key regions to strengthen their market position and better serve local demand.

Consolidated Market with Strong Global Players

The DC market demonstrates a relatively consolidated structure dominated by large multinational conglomerates with diverse product portfolios and strong technological capabilities. These established players leverage their extensive research and development capabilities, global manufacturing footprint, and well-established distribution networks to maintain their market positions. The market has witnessed significant merger and acquisition activities, with companies like Schneider Electric acquiring DC Systems BV and Eaton Corporation acquiring Power Distribution Inc. to strengthen their technological capabilities and market presence. Regional players, particularly in Asia-Pacific, are increasingly gaining prominence by focusing on specific market segments and developing cost-effective solutions.

The competitive landscape is characterized by a mix of integrated solution providers and specialized manufacturers, with the former holding a stronger position due to their ability to offer comprehensive DC distribution solutions. Chinese domestic manufacturers are emerging as significant players, particularly in the Asia-Pacific region, by offering competitive pricing and locally adapted solutions. The market witnesses strategic partnerships between equipment manufacturers and technology providers to enhance product offerings and expand market reach, while companies are also focusing on developing region-specific solutions to address local market requirements and regulations.

Innovation and Adaptability Drive Market Success

Success in the DC distribution network market increasingly depends on companies' ability to innovate and adapt to evolving technological requirements, particularly in emerging applications like data centers, renewable energy integration, and electric vehicle charging infrastructure. Market players need to focus on developing cost-effective solutions while maintaining high reliability and efficiency standards to gain a competitive advantage. Companies must also strengthen their after-sales service capabilities and establish strong relationships with system integrators and engineering firms to enhance their market position. The ability to provide customized solutions for specific industry applications while maintaining standardization for cost efficiency is becoming a crucial factor for success.

Future market leadership will require companies to develop comprehensive product portfolios that address various voltage levels and power requirements while ensuring compatibility with existing infrastructure. Players must also focus on building strong relationships with end-users in key sectors like telecommunications, data centers, and renewable energy to understand evolving requirements and develop appropriate solutions. The increasing emphasis on environmental sustainability and energy efficiency creates opportunities for companies to differentiate themselves through innovative green technologies and solutions. Additionally, success in this market requires companies to maintain strong financial positions to support continuous research and development efforts while building robust supply chains to ensure reliable product delivery.

DC Distribution Network Market Leaders

-

ABB Ltd

-

Siemens AG

-

Vertiv Group Corp.

-

Eaton Corporation PLC

-

Secheron Sa

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

DC Distribution Network Market News

- March 2022: In line with shared commitments to decarbonize, National Grid and Siemens Energy teamed up to undertake an upgrade of a National Grid substation using Siemens Energy-designed fluorinated gas-free Blue DC circuit breakers, which are made of clean air insulation and vacuum switching technology. Scheduled for commissioning in 2023, Siemens Energy's Blue DC circuit breakers will be installed in Massachusetts at the United States substation that serves several Massachusetts communities. The first Siemens Energy Blue circuit breaker installation will be in National Grid's United States electricity network.

- January 2022: Eaton announced a USD 4.9 million award from the United States Department of Energy to reduce the cost and complexity of deploying a direct-current (DC) distribution network for fast electric vehicle charging in the country. Eaton is likely to develop and demonstrate a novel, compact, and turnkey solution for DC fast-charging infrastructure that is likely to reduce costs by 65% through improvements in power conversion and grid interconnection technology, charger integration and modularity, and installation time.

DC Distribution Network Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Scope of the Study

- 1.2 Market Definition

- 1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

- 4.1 Introduction

- 4.2 Market Size and Demand Forecast in USD Billion, till 2028

- 4.3 Recent Trends and Developments

- 4.4 Government Policies and Regulations

-

4.5 Market Dynamics

- 4.5.1 Drivers

- 4.5.2 Restraints

- 4.6 Supply Chain Analysis

-

4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products and Services

- 4.7.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 End User (Qualitative Analysis Only)

- 5.1.1 Remote Cell Towers

- 5.1.2 Commercial Buildings

- 5.1.3 Data Centers

- 5.1.4 Military Applications

- 5.1.5 EV Fast Charging Systems

- 5.1.6 Other End Users

-

5.2 Geography

- 5.2.1 North America

- 5.2.2 Europe

- 5.2.3 Asia-Pacific

- 5.2.4 South America

- 5.2.5 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Strategies Adopted by Leading Players

- 6.3 Market Share Analysis

-

6.4 Company Profiles

- 6.4.1 ABB Ltd.

- 6.4.2 Siemens AG

- 6.4.3 Vertiv Group Corp.

- 6.4.4 Eaton Corporation PLC

- 6.4.5 Robert Bosch GmbH

- 6.4.6 Schneider Electric SE

- 6.4.7 Alpha Technologies Inc.

- 6.4.8 Nextek Power Systems Inc.

- 6.4.9 Secheron Sa

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

**Subject to Availability

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

DC Distribution Network Industry Segmentation

DC distribution network is used for installations that operate at a nominal capacity of less than or equal to 1500 Vdc. In this report on the DC distribution network market (henceforth referred to as the market studied), the market considers the revenue generated from the DC distribution network and systems vendors from the aforementioned voltage range. The after-sales, replacement, repair, and services markets are not part of the market studied.

The DC distribution network market is segmented by end-user (remote Cell Towers, Commercial buildings, data Centers, Military Applications, EV Fast charging systems, and other End Users), and geography (North America, Europe, Asia-pacific, South America, and Middle-East and Africa). The report offers the market size and forecasts for the DC Distribution Network Market in revenue (USD billion) for all the above segments.

| End User (Qualitative Analysis Only) | Remote Cell Towers |

| Commercial Buildings | |

| Data Centers | |

| Military Applications | |

| EV Fast Charging Systems | |

| Other End Users | |

| Geography | North America |

| Europe | |

| Asia-Pacific | |

| South America | |

| Middle-East and Africa |

Need A Different Region or Segment?

Customize Now

DC Distribution Network Market Research FAQs

What is the current DC Distribution Network Market size?

The DC Distribution Network Market is projected to register a CAGR of 7.04% during the forecast period (2025-2030)

Who are the key players in DC Distribution Network Market?

ABB Ltd, Siemens AG, Vertiv Group Corp., Eaton Corporation PLC and Secheron Sa are the major companies operating in the DC Distribution Network Market.

Which is the fastest growing region in DC Distribution Network Market?

Middle East and Africa is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in DC Distribution Network Market?

In 2025, the Europe accounts for the largest market share in DC Distribution Network Market.

What years does this DC Distribution Network Market cover?

The report covers the DC Distribution Network Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the DC Distribution Network Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

DC Distribution Network Market Research

Mordor Intelligence offers unparalleled expertise in analyzing the DC distribution industry. We provide comprehensive insights into the evolving distribution network landscape. Our extensive research covers the entire spectrum of DC market dynamics. This includes detailed analysis of direct current power system implementations and DC distribution network configurations across global markets. The report offers in-depth coverage of size DC metrics and emerging trends in DC size developments. It is available as an easy-to-download report PDF.

Stakeholders in the distribution network sector gain valuable insights through our detailed examination of technological advancements and infrastructure developments. The analysis encompasses crucial aspects of DC distribution systems, including power management solutions and network optimization strategies. Our research methodology ensures thorough coverage of both established and emerging distribution system technologies. This provides actionable intelligence for decision-makers involved in direct current panel implementations and network infrastructure development.