Market Overview

| Study Period | 2019 - 2030 |

|---|---|

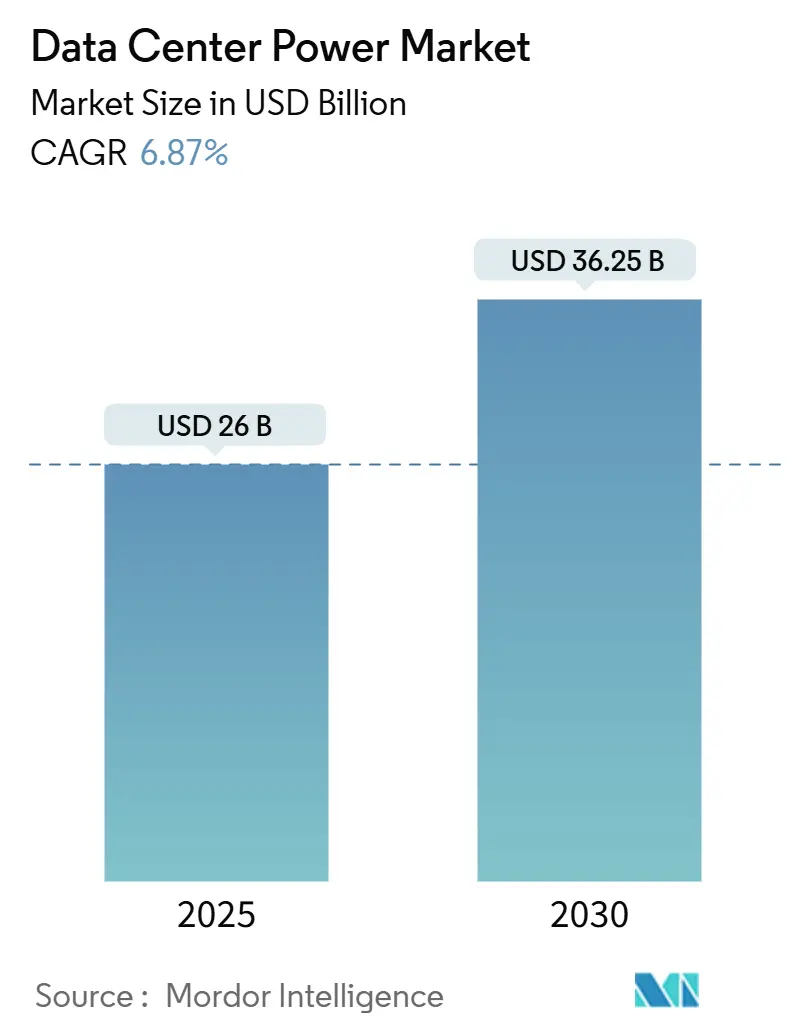

| Market Size (2025) | USD 26 Billion |

| Market Size (2030) | USD 36.25 Billion |

| Growth Rate (2025 - 2030) | 6.87% CAGR |

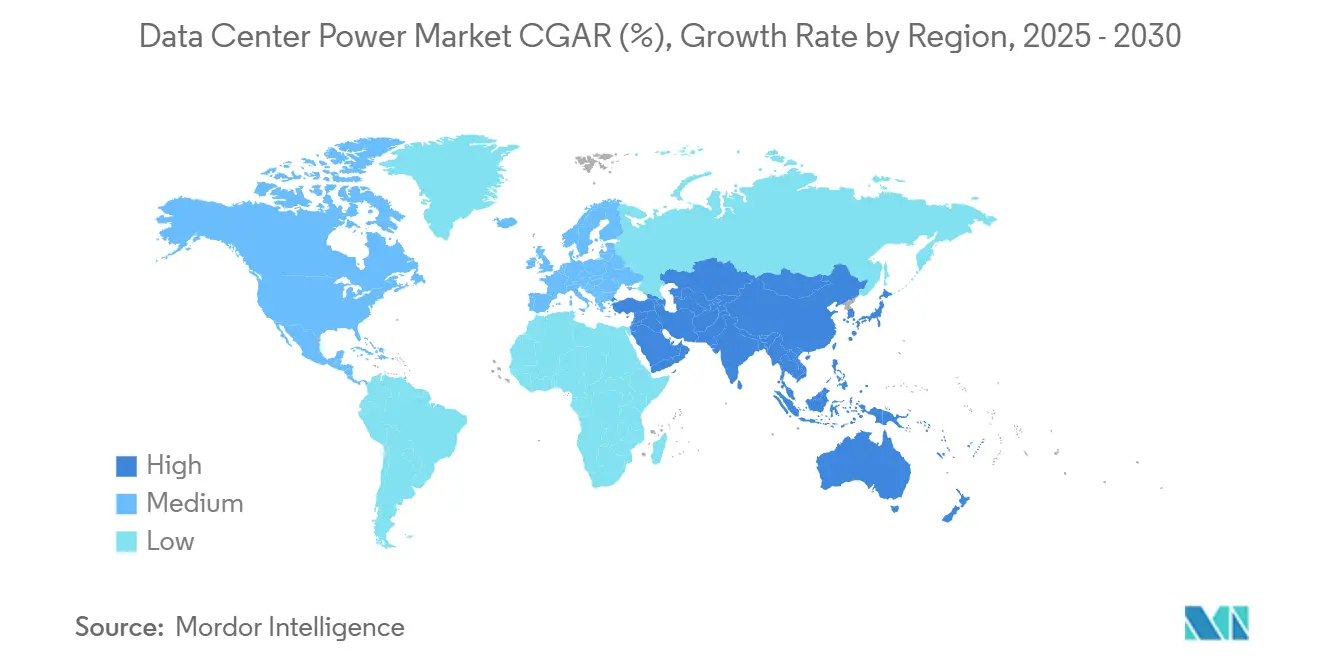

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Data Center Power Market Analysis by Mordor Intelligence

The data center power market size is expected to be valued at USD 24.56 billion in 2025 and is projected to advance at a 7.25% CAGR, reaching USD 34.86 billion by 2030. Growing deployment of artificial intelligence, aggressive hyperscale capacity additions, and stricter reliability mandates are reshaping electrical infrastructure priorities and fueling expansion in the data center power market. High-density AI workloads consume three times more electricity than conventional CPUs, pushing operators toward higher-voltage distribution, liquid cooling, and grid-interactive power trains. Consolidation among equipment suppliers is strengthening as utilities, regulators, and cloud providers align on large-scale projects that require multi-gigawatt interconnections. With more operators repurposing retired coal plants for campus-style facilities, the data center power market is transitioning from passive energy consumption to active grid participation, unlocking new revenue streams through ancillary services.

Key Report Takeaways

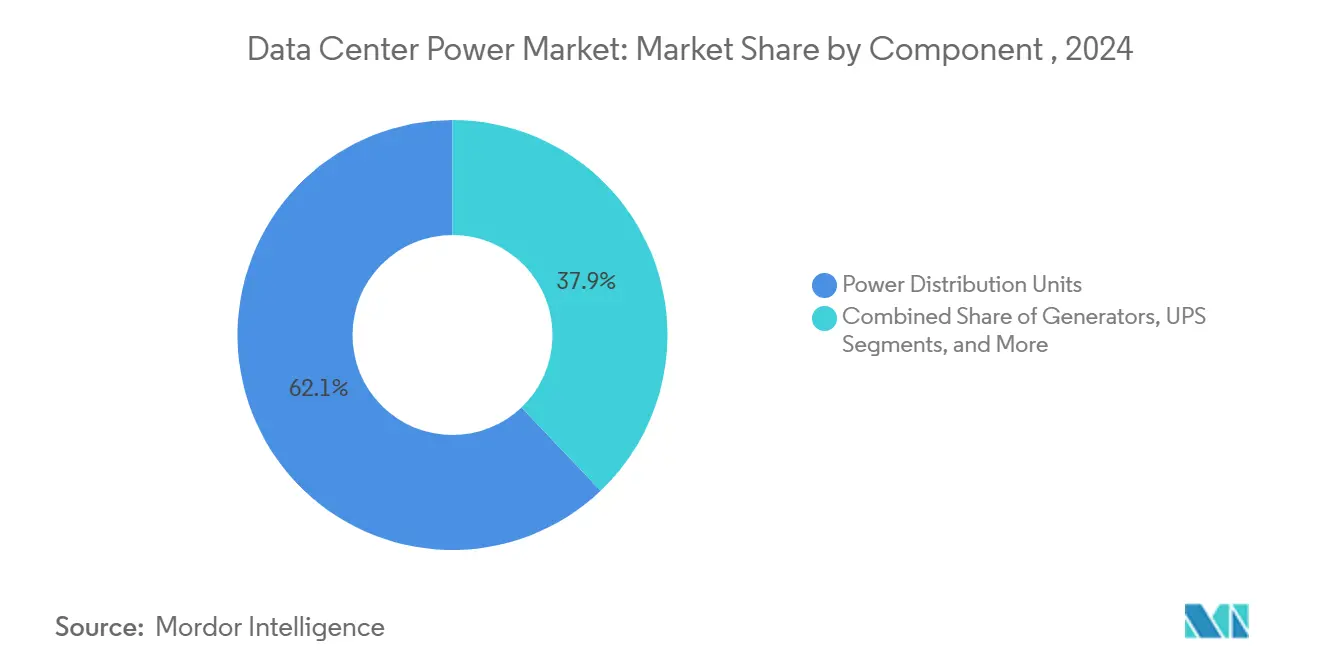

- By component, UPS systems led with 62.1% of the data center power market share in 2024, while power distribution units are expanding at the fastest 7.5% CAGR through 2030.

- By data center type, colocation providers held 43.8% revenue share in 2024; hyperscale operators are projected to register the highest 8.7% CAGR over 2025-2030.

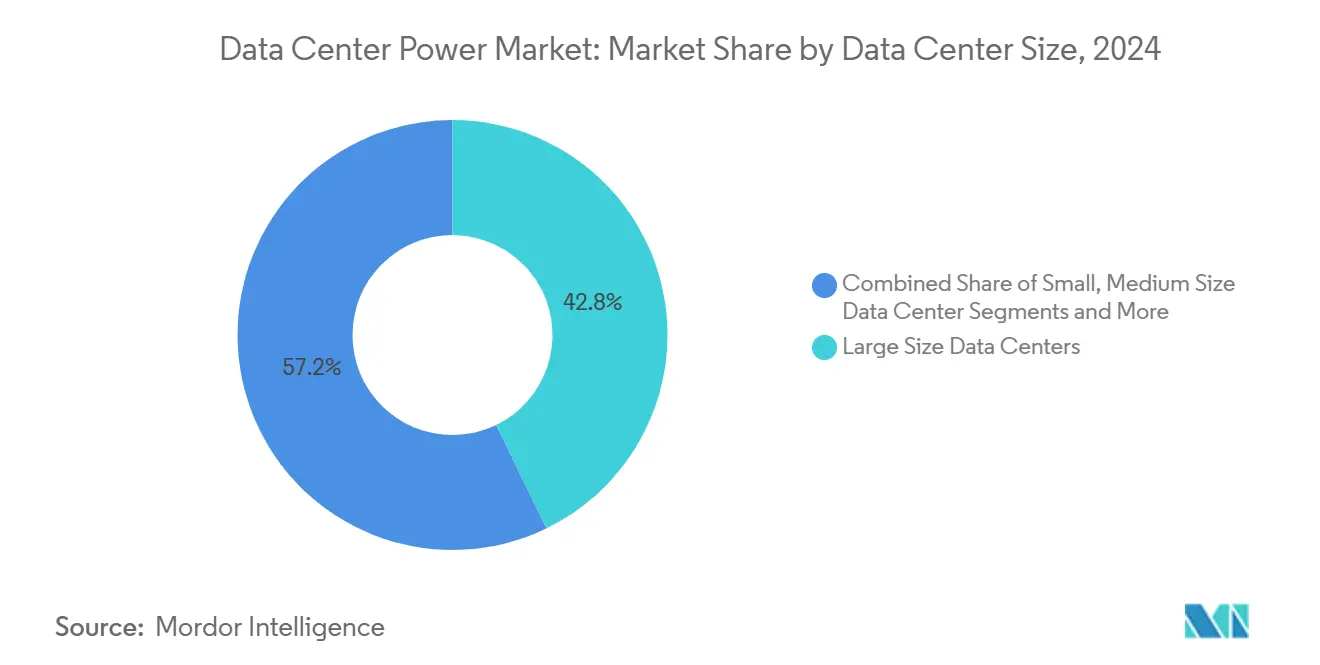

- By facility size, large-scale installations commanded 42.8% of the data center power market size in 2024; mega-scale sites are forecast to grow at a 7.3% CAGR.

- By tier classification, Tier III dominated with a 63.1% share of the data center power market size in 2024, whereas Tier IV is on track for an 8.9% CAGR.

- By geography, Europe accounted for 34.18% revenue share in 2024, and Asia-Pacific is set to expand at a 9.2% CAGR to 2030.

Global Data Center Power Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperscale & cloud computing expansion | +2.1% | North America, Asia-Pacific | Medium term (2-4 years) |

| AI-driven high-density workloads | +1.8% | North America, Europe | Short term (≤ 2 years) |

| Stricter uptime & redundancy standards | +1.2% | Europe, North America | Long term (≥ 4 years) |

| Sustainability & energy-efficiency mandates | +0.9% | Europe, Asia-Pacific | Long term (≥ 4 years) |

| Grid-interactive revenue streams | +0.7% | North America, Europe | Medium term (2-4 years) |

| Coal-plant site repurposing for campuses | +0.4% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Understand The Key Trends Shaping This Market

Download PDF

Hyperscale & Cloud Computing Expansion

Hyperscale operators are commissioning campuses that equal the electricity demand of medium-sized cities. Meta’s 2 GW development and the 5.6 GW Wonder Valley site illustrate the scale now required to sustain cloud growth. Orders for modular, factory-integrated power trains are rising sharply, and Schneider Electric disclosed that data centers made up 24% of its incoming orders in 2025. Structured agreements tying utility interconnections to phased capacity releases are becoming common, improving risk allocation among utilities, landlords, and cloud tenants. The data center power market benefits directly because every incremental megawatt of IT load drives proportional investment in switchgear, UPS, and medium-voltage systems.

AI-Driven High-Density Workloads

AI accelerators raise rack densities from 5-10 kW to 50-100 kW, forcing a move to 48 V DC distribution, higher phase counts, and liquid cooling. Vertiv’s 360AI platform supports 100 kW per rack with integrated busway, coolant distribution, and leak-detection controls. Persistent thermal loads increase the duty cycle of UPS equipment, making efficiency curves at partial load a critical selection metric. International Energy Agency projections indicate AI could consume 1.5% of global electricity by 2029, reinforcing the urgency for energy-proportional power systems that dynamically throttle in sync with GPU utilization. Vendors that marry power and cooling into a compact, prefabricated block are capturing share as operators seek predictable deployment timelines.

Stricter Uptime & Redundancy Standards

Downtime now incurs multimillion-dollar losses and regulatory fines, prompting investment in Tier IV architectures with 99.995% availability targets. Schneider Electric and NVIDIA published reference designs that embed dual-cord feeds, static transfer switches, and predictive analytics across redundant distribution paths.[1]Schneider Electric, “Schneider Electric Collaborates with NVIDIA on Designs for AI Data Centers,”se.com The EU Digital Operational Resilience Act prescribes continuous availability for financial data, amplifying demand for fault-tolerant power trains that remain serviceable while online. Operators are integrating branch-circuit monitoring with AI-driven maintenance alerts, enabling proactive component swaps. Cost-benefit analyses highlight that the incremental capital premium of Tier IV is offset within one outage event, accelerating adoption across AI training clusters and critical transaction platforms.

Sustainability & Energy-Efficiency Mandates

Regulators target improved power usage effectiveness, renewable integration, and transparent reporting. The EU Energy Efficiency Directive demands annual disclosure of energy and water use, driving uptake of high-efficiency UPS platforms and intelligent power distribution units. China’s policy capping PUE at 1.5 by 2025 accelerates retrofit cycles for legacy sites. Eaton’s Data Centers as a Grid model allows UPS fleets to deliver ancillary services, turning idle capacity into revenue. Operators signing renewable power purchase agreements increasingly specify synchronous battery storage to mitigate volatility. [2]Eaton, “Data Centers as a Grid,”eaton.comGrid-interactive power trains thus grow from optional feature sets into baseline requirements, pulling development roadmaps toward advanced bidirectional inverters and aggregated control software.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High CAPEX of electrical infrastructure | -1.4% | Global, emerging markets | Short term (≤ 2 years) |

| Transformer/switchgear supply bottlenecks | -1.1% | North America, Europe | Medium term (2-4 years) |

| Carbon-intensity regulations & reporting | -0.8% | Europe, North America | Medium term (2-4 years) |

| Local opposition to sub-station expansion | -0.6% | Dense urban zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High CAPEX of Electrical Infrastructure

End-to-end cost for AI-ready campuses approaches USD 38 million per MW, with liquid cooling inflating power-train expenditures by 15-20× compared with air-based designs. Smaller colocation players find it challenging to secure financing for customized medium-voltage gear, long-lead transformers, and specialized batteries. Equipment-as-a-service contracts are emerging, yet lenders remain cautious because secondary-market values for bespoke switchgear are limited. Budget restrictions slow expansion in emerging economies, tempering the otherwise robust trajectory of the data center power market. Financing gaps also spur joint-venture models where landlords and utilities co-invest, diluting returns but enabling project viability.

Transformer/Switchgear Supply Bottlenecks

Lead times for large transformers stretched from quarters to 2-4 years, and unit prices jumped 80% versus 2020 levels, according to the National Infrastructure Advisory Council. Medium-voltage switchgear experiences similar shortages, forcing operators to reserve capacity years before groundbreaking.[3]National Infrastructure Advisory Council, “Transformer Supply Chain Report,” cisa.govMajor suppliers responded by expanding factories; Schneider Electric allocated USD 140 million to Tennessee to boost custom switchgear output. Still, backlogs persist, pressuring schedules and compressing contingency windows. Incumbent vendors with vertical integration and established utility contracts win a disproportionate share as customers prioritize supply assurance. These delays inject friction into the data center power market growth curve even as long-term demand remains intact.

Segment Analysis

By Component: UPS Systems Lead Amid PDU Innovation

UPS platforms retained 62.1% of the data center power market share in 2024, underscoring their role as the last defense against grid instability. Lithium-ion adoption continues, but valve-regulated lead-acid remains prevalent due to cost advantage in lower-density halls. Intelligent switch-mode rectifiers trim conversion losses, improving overall facility energy profiles. In parallel, power distribution units record 7.5% CAGR because operators now embed branch-circuit monitoring, temperature sensing, and secure firmware. Generators stay indispensable, yet the narrative shifts as hydrogen-ready gensets enter pilot use. Switchgear upgrades align with higher voltages demanded by AI racks, and battery energy storage systems gain favor for peak-shaving and revenue stacking.

Ecosystem dynamics shift as UPS vendors add grid services modules, enabling frequency regulation without undermining ride-through performance. Vertiv’s grid-interactive firmware dispatches reserve capacity during non-critical intervals. Delta’s Smart PDU I-Type consolidates metering and remote-upgrade functions into a 42 mm chassis aimed at dense AI enclosures. Services revenue rises because commissioning high-density halls requires thermal mapping, harmonic studies, and ongoing firmware validation. Consequently, operators outsource lifecycle support, driving predictable, annuity-style income streams for integrators and enriching the data center power market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Data Center Type: Hyperscaler Drive Growth

Colocation facilities held a 43.8% share of the data center power market size in 2024, thanks to shared infrastructure economics and rapid time-to-market. Yet hyperscalers post an 8.7% CAGR, propelled by Apple, Microsoft, and Google's strategies to self-build AI hosting zones. Enterprise campuses persist for compliance-sensitive industries, and edge nodes proliferate near population clusters to lower latency. Hyperscalers design proprietary power topologies, integrating on-site substations and battery farms, while colocation players counter with flexible power densities and interconnect fabrics.

Competitive tension fosters innovation: CoreSite advertises liquid-to-chip cooling and 48 V busway as standard in next-gen halls, whereas cloud majors refine modular blocks for 15 MW increments. Pay-as-you-grow contracts appear in both camps, decoupling capital allocation from immediate occupancy. Edge operators deploy standardized micro power modules to keep pace with 5G rollouts. These intertwined strategies collectively elevate equipment volumes flowing into the data center power market.

By Data Center Size: Mega-Scale Facilities Accelerate

Large-scale halls captured 42.8% of the data center power market size in 2024, benefiting from balanced capital efficiency. Mega-scale projects topping 100 MW rise at 7.3% CAGR as hyperscalers consolidate capacity into fewer, but denser, sites to optimize land, cooling, and tax incentives. Small-and-medium sites maintain relevance in metropolitan zones where latency trumps scale, and microgrid-enabled campuses surface where grid queue delays hinder large interconnections.

Mega campuses negotiate directly with utilities for dedicated 230 kV feeds and often co-locate energy storage to smooth load profiles. Conversely, smaller sites explore flywheel UPS and gas turbine hybrids to circumvent transformer shortages. Grid planners now model the collective impact of clustered facilities, escalating the importance of dynamic voltage control and fault-ride-through technologies. The clear segmentation of size categories refines vendor roadmaps and enables targeted go-to-market campaigns across the data center power market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Tier Level: Tier IV Gains Momentum

Tier III dominated with a 63.1% share in 2024, balancing cost and resilience. Tier IV now advances at an 8.9% CAGR, fueled by AI training platforms and financial exchanges that cannot absorb even seconds of downtime. Tier I and II remain viable for archival storage or disaster-recovery outposts in cost-sensitive geographies. Operators upgrading to Tier IV deploy dual utility feeds, concurrently maintainable switchgear, and active-active UPS architectures.

Regulators tie operational licenses for digital banking and healthcare platforms to documented Tier compliance, turning certifications into prerequisites rather than differentiators. Vendors respond with pre-validated blueprints layering redundant power paths, predictive battery analytics, and automated transfer logic. These systemic improvements reinforce long-term service contracts, embedding recurring revenue into the data center power market.

Geography Analysis

Europe led with 34.18% revenue share in 2024, driven by binding energy-efficiency legislation, stringent reporting rules, and aggressive renewable goals. Operators retrofit legacy facilities with high-efficiency UPS and battery storage to satisfy the Energy Efficiency Directive. Coal-plant conversions such as Sines DC repurpose existing grid interconnections and seawater intake lines, accelerating deployment while curbing environmental impact. Vendors supply grid-interactive UPS that help stabilize wind-heavy regional grids, strengthening the continent’s leadership in sustainable design. Corporate buyers prefer European sites because renewable guarantees of origin support net-zero pledges, sustaining equipment demand across the data center power market.

Asia-Pacific delivers the fastest 9.2% CAGR as governments fund cloud corridors and subsidize land, fiber, and electricity. Regional capacity totaled 12,206 MW of live IT load with 14,338 MW in construction as of H2 2024. Microsoft pledged multi-billion-dollar plans in India and Japan, highlighting the scale of expansion. China enforces a national PUE cap that accelerates high-efficiency power component orders. India’s Digital Personal Data Protection Act drives domestic hosting and stimulates new campuses near renewable clusters. Southeast Asian nations offer tax breaks to attract hyperscalers, further widening procurement pipelines for switchgear, UPS, and smart PDUs.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

The market is moderately concentrated, with system integrators controlling critical supply chains. Schneider Electric fortified its portfolio through a USD 850 million acquisition of Motivair and unveiled digital twin capabilities using NVIDIA Omniverse for grid-to-chip simulations. Vertiv advances hybrid cooling and grid-interactive UPS, signing multi-year supply frameworks with Compass Datacenters. ABB and Eaton leverage utility-scale credentials and embedded install bases to defend their share. These incumbents bundle power, cooling, and software into unified offers, creating high switching costs and reinforcing their grip on the data center power market.

Supply bottlenecks advantage established manufacturers. Schneider Electric earmarked USD 700 million to add U.S. capacity for medium-voltage assemblies, signaling a commitment amid transformer shortages. Eaton secured a USD 20 million switchgear contract for NY CREATES, illustrating how deep product lines and local support win complex projects. FlexGen exemplifies a specialist entrant focusing on battery energy storage; its modular BESS compresses deployment cycles for grid-interactive campuses. Success factors now extend beyond kilovolt-ampere ratings to include lifecycle services, software analytics, and financing, compelling all players to broaden capabilities.

White-space opportunities emerge in coal-plant repurposing, microgrid orchestration, and energy-as-a-service models. Vendors with utility partnerships and adaptable control platforms are positioned to capture these niches. Disrupters such as Bloom Energy and Generac enter through on-site generation and fuel cell solutions. Competition therefore hinges on balancing scale manufacturing with tailored engineering, a dynamic that keeps the data center power market vibrant despite rising barriers to entry.

Data Center Power Industry Leaders

-

Schneider Electric SE

-

Vertiv Holdings Co.

-

ABB Ltd

-

Eaton Corporation plc

-

Legrand SA

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- March 2025: Schneider Electric introduced ETAP-powered digital twin models running on NVIDIA Omniverse to simulate AI factory power flows from grid to chip level, improving planning accuracy for high-density halls.

- February 2025: Schneider Electric opened new data center and microgrid laboratories at its Massachusetts R&D hub, featuring a 6,000 sq ft PDU test floor for AI-grade voltage systems.

- February 2025: The Federal Energy Regulatory Commission directed PJM to reassess tariffs for AI-enabled data centers co-located at generation sites to safeguard reliability and consumer costs.

- January 2025: Eaton won a USD 20 million order to supply switchgear and its Brightlayer monitoring system to the NY CREATES NanoFab Reflection research facility.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the data center power market as all electrical infrastructure, namely uninterruptible power supply systems, diesel and gas generators, power distribution units, switchgear, remote power panels, transfer switches, and battery or flywheel energy storage systems, deployed inside colocation, hyperscale, enterprise, edge, and modular facilities to deliver conditioned, redundant electricity up to the IT rack.

Scope exclusion: Facility shell, chillers, CRAH/CRAC cooling, and on-site renewable generation are outside this sizing.

Segmentation Overview

- By Component

- Electrical Solutions

- UPS Systems

- Generators

- Diesel Generators

- Gas Generators

- Hydrogen Fuel-cell Generators

- Power Distribution Units

- Switchgear

- Transfer Switches

- Remote Power Panels

- Energy-storage Systems

- Service

- Installation and Commissioning

- Maintenance and Support

- Training and Consulting

- Electrical Solutions

- By Data Center Type

- Hyperscaler/Cloud Service Providers

- Colocation Providers

- Enterprise and Edge Data Center

- By Data Center Size

- Small Size Data Centers

- Medium Size Data Centers

- Large Size Data Centers

- Massive Size Data Centers

- Mega Size Data Centers

- By Tier Level

- Tier I and II

- Tier III

- Tier IV

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- United Arab Emirates

- Saudi Arabia

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts conducted interviews with power system engineers at colocation operators across North America, Europe, and APAC, procurement heads at hyperscalers, and regional distributors covering Latin America and the GCC. These discussions clarified live ASP movements, redundancy preferences (N+1 versus 2 N), and emerging demand for 415 V busways, ensuring model assumptions mirrored on-ground realities.

Desk Research

We began by mapping publicly available indicators such as regional hyperscale megawatt additions from the Uptime Institute, monthly utility-scale diesel gen set shipments from the US International Trade Commission, and country-level UPS export statistics on UN Comtrade, which gave us baselines for volume and average selling price trends. Annual outage cost surveys from the Ponemon Institute, patent filings on lithium-ion UPS chemistries accessed through Questel, and capacity pipeline announcements in Digital Realty and Equinix 10-Ks helped trace technology shifts toward 2 N designs and lithium batteries. Company presentations, investor transcripts, and trade association briefings (for example, AFCOM State of the Data Center) then contextualized PUE improvement targets and rack density road maps.

Internal access to Dow Jones Factiva and D&B Hoovers allowed our team to triangulate revenue splits for leading OEMs, feeding a reliable component mix. The desk research sources named here are illustrative; many additional open-source and paid references informed our validation.

The desk research sources named here are illustrative; many additional open-source and paid references informed our validation.

Market-Sizing & Forecasting

We reconstruct 2025 spending through a top-down "IT load x power density x cost per kW" pool, built from country data center megawatt additions reported by utilities and planning authorities, and corroborated with selective bottom-up roll-ups of OEM revenues and channel checks. Key variables like average rack density (kW/rack), regional PUE, lithium-ion UPS share, hyperscale capex announcements, and generator fuel switch ratios drive scenario inputs. A multivariate regression model, refreshed each quarter, projects their influence out to 2030. Where bottom-up totals undershoot, gap filling uses sampled ASP x volume from distributor surveys before iterative alignment with the top-down baseline.

Data Validation & Update Cycle

Every draft dataset passes a three-layer review: automated variance flags, peer analyst cross-checks, and senior review sign-off. We revisit sources annually and mid-cycle whenever a material event, large M&A, fuel price shock, or grid outage regulation alters assumptions. A final pre-publication sweep means clients receive our newest view each time they log in.

Why Our Data Center Power Baseline Commands Reliability

Published values differ because firms choose dissimilar component baskets, convert currencies on varying dates, or apply divergent rack density trajectories.

Key gap drivers include differing inclusion of installation services, one-time fuel treatment costs, and whether battery replacements are capitalized or expensed.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 24.56 B | Mordor Intelligence | - |

| USD 15.97 B | Global Consultancy A | Excludes lithium-ion UPS retrofit spend and bases density on 8 kW/rack average |

| USD 22.93 B | Trade Journal B | Treats service contracts as recurring OPEX, then annualizes to CAPEX, inflating outer year totals |

In short, the disciplined alignment of scope, the twin track modeling we apply, and our yearly refresh cadence give decision makers a transparent, repeatable baseline they can trust.

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What is the current value of the data center power market?

The data center power market stands at USD 24.56 billion in 2025 with expectations to reach USD 34.86 billion by 2030.

Which component segment is growing the fastest?

Power distribution units are expanding at a 7.5% CAGR as operators adopt intelligent, grid-interactive monitoring.

Why are hyperscale operators important to market growth?

Hyperscalers contribute 60% of incremental capacity, adding mega-scale campuses that drive large orders for switchgear, UPS, and on-site substations.

How do AI workloads influence power infrastructure design?

AI racks draw 3-4× more electricity than traditional servers, pushing facilities toward 48 V DC distribution, liquid cooling, and higher-capacity UPS systems.

What regions present the strongest growth outlook?

Asia-Pacific posts the highest 9.2% CAGR to 2030, supported by massive digital investments across China, India, and Southeast Asia.

Page last updated on: