Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 9.17 Billion |

| Market Size (2030) | USD 12.34 Billion |

| Growth Rate (2025 - 2030) | 6.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players_Market_Players.webp)

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Computed Tomography (CT) Market Analysis by Mordor Intelligence

The Computed Tomography (CT) market size reached USD 9.17 billion in 2025 and is on track to rise to USD 12.34 billion by 2030, expanding at a 6.12% CAGR. Continued gains come from accelerating adoption of photon-counting detectors, artificial-intelligence–enabled workflow orchestration, and higher scan volumes for oncology, cardiology, and full-body preventive imaging. The CT scanner market also benefits from a growing geriatric population that demands minimally invasive diagnostics, while mobile stroke units and rural outreach programs broaden geographic reach. Competitive rivalry intensifies as GE HealthCare, Siemens Healthineers, and Philips shorten product cycles, embed cloud connectivity, and form strategic alliances that fuse hardware with software. Supply-chain fragility around semiconductor components and persistent radiologic-technologist shortages temper momentum but simultaneously spark investment in automation and remote‐operation capabilities that extend CT market access.

Key Report Takeaways

- By technology, mid-slice systems led with 38.56% of CT market share in 2024, whereas high-slice configurations are advancing at a 6.89% CAGR to 2030.

- By product type, stationary scanners accounted for 62.67% of CT market size in 2024, while portable and mobile units record the strongest growth trajectory.

- By application, oncology held 31.82% share of the CT market in 2024, whereas dental and maxillofacial imaging is growing at a 7.11% CAGR through 2030.

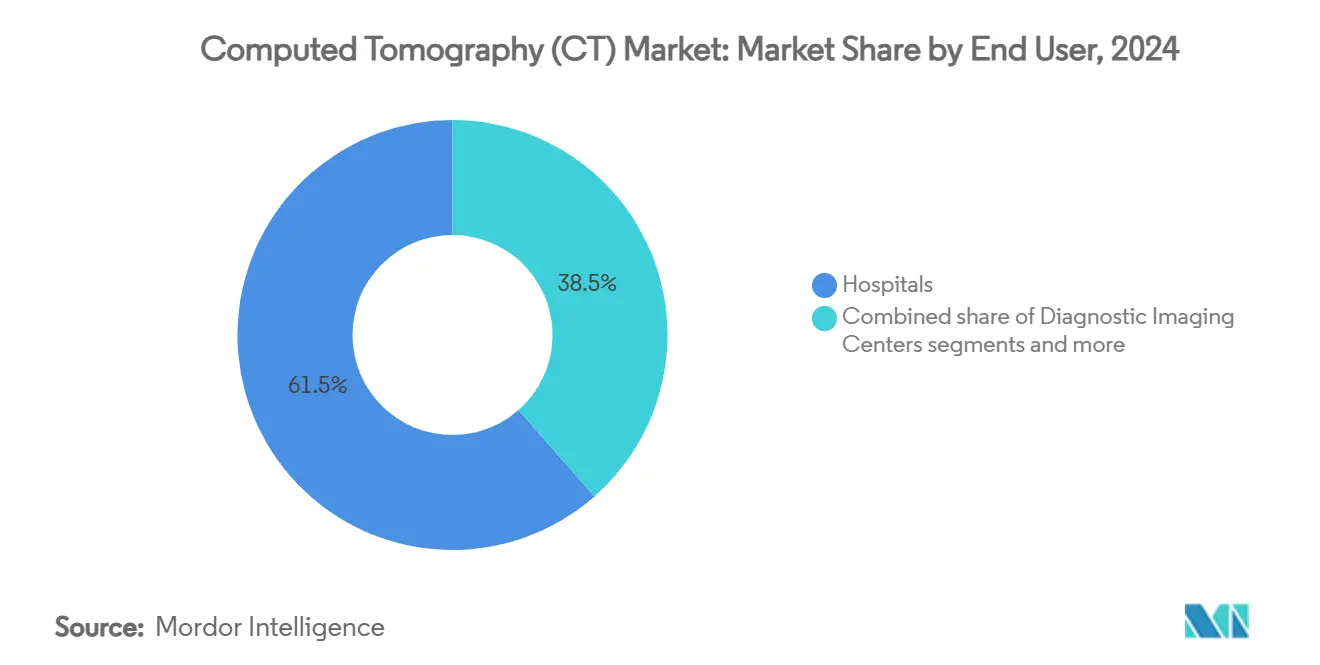

- By end-user, hospitals controlled 61.48% share of the CT market in 2024, yet ambulatory surgical centers post a 7.34% CAGR to 2030.

- By device architecture, spiral systems represented 68.82% share of CT market size in 2024, and ring-gantry systems show the fastest 7.58% CAGR outlook.

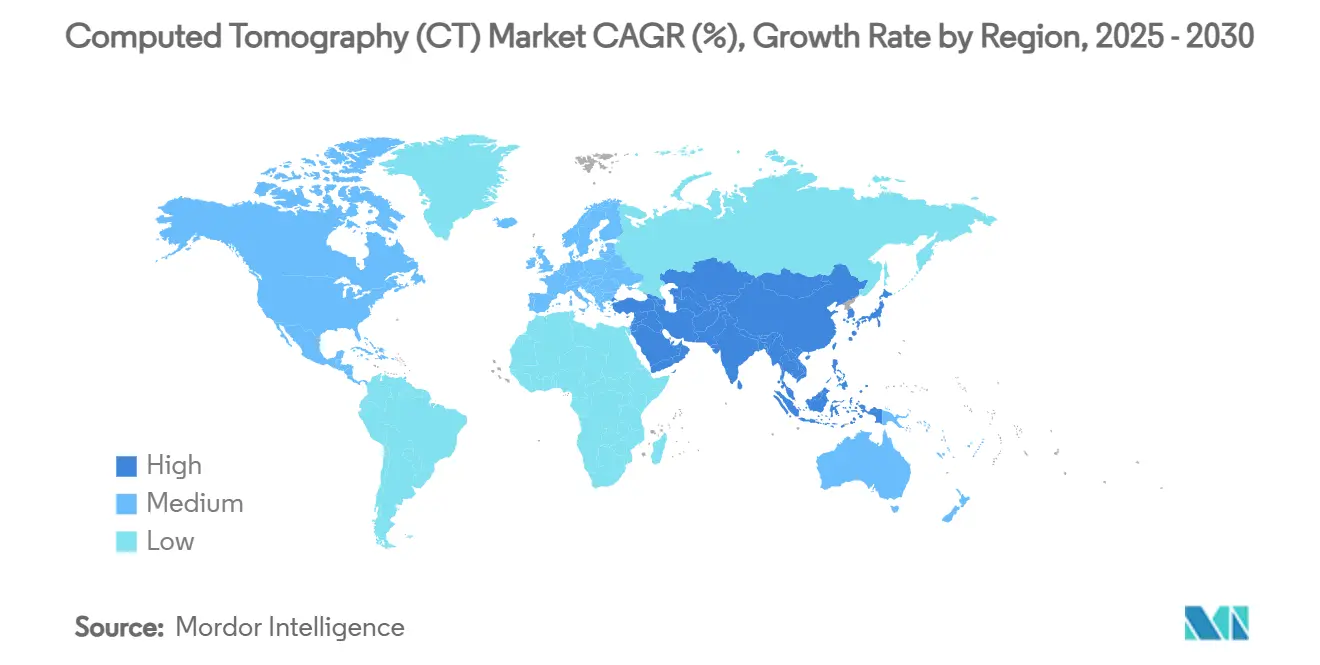

- By geography, North America commanded 42.23% of CT market share in 2024, while Asia-Pacific demonstrates a 7.82% CAGR to 2030.

Global Computed Tomography (CT) Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging chronic-disease burden | +1.2% | Global, with highest impact in North America & Europe | Long term (≥ 4 years) |

| Rapid detector & spectral-CT innovations | +1.8% | North America & EU leading, APAC adoption following | Medium term (2-4 years) |

| Growing demand for minimally-invasive diagnostics | +1.0% | Global, with accelerated adoption in APAC | Medium term (2-4 years) |

| Expanding geriatric population base | +0.9% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Eco-sustainability mandates driving low-dose CT investment | +0.6% | EU & North America primarily | Short term (≤ 2 years) |

| Cardiac CT angiography guideline adoption | +0.7% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Chronic-Disease Burden

Rising prevalence of cardiovascular disease, projected to cause more than 23 million deaths by 2030, is sharply elevating demand for cardiothoracic imaging. CT scans already account for 25.87% of imaging volume in pharmaceutical trials, underscoring their central role in oncology and cardiovascular drug evaluation. Low-dose lung-cancer screening programs are scaling across multiple regions and demonstrate mortality reductions near 25% in high-risk cohorts. Health systems integrate AI triage that cuts inter-reader variability by 42.5% and shortens report turnaround by 63%, enabling higher throughput without sacrificing quality. Emerging economies, supported by infrastructure upgrades, are rapidly widening CT market penetration to address previously unmet diagnostic needs.

Rapid Detector & Spectral-CT Innovations

Photon-counting detectors such as Siemens Healthineers’ Naeotom Alpha class reach spatial-resolution ratings of 134.7 HU/mm while lowering radiation dose, redefining image clarity for vascular studies[1]Source: Cassling Editorial Team, “Naeotom Alpha Class of Photon-Counting CT Scanners Cleared by FDA,” cassling.com . Spectral imaging adds material decomposition and quantitative iodine mapping that assist oncologic staging and cardiology plaque analysis. Mobile stroke units equipped with high-performance scanners accelerate thrombolysis by shrinking door-to-needle times. Capital allocation follows technology leadership, as Siemens commits USD 350 million exclusively for CT advancement within its broader med-tech program.

Growing Demand for Minimally-Invasive Diagnostics

CT-guided interventions lower surgical morbidity and shorten patient recovery, driving higher elective use in outpatient centers. Imaging services are projected to move from 40% to 46% of procedures in outpatient venues within three years, reflecting cost sensitivity and convenience. Compact cone-beam platforms now produce brain images comparable to multidetector systems while offering smaller footprints and lower operating costs. Preventive full-body scanning constitutes a fast-growing consumer segment that advances at double-digit rates, signaling a broader wellness orientation. AI modules that extract bone-mineral density from routine abdominal scans illustrate how single exposures yield multiple diagnostic insights.

Expanding Geriatric Population Base

Population aging is expected to lift CT utilization by up to 59% by 2055, coinciding with persistent shortages of radiologists and technologists. Coronary CT angiography usage rose 67% over five years for dizziness and headache indications, signaling broader clinical acceptance[2]ACR Bulletin. "Radiology Workforce Shortage and Growing Demand Something Has to Give." July 3, 2024. www.acr.org. . AI workflows eliminate roughly 40% of manual steps, helping facilities handle higher case loads amid staffing gaps. Portable C-arm and head CT devices deliver imaging at the bedside, an advantage for frail elderly or rural residents who face transport risks. Asia-Pacific hospital expansion further accelerates demand as governments channel capital toward senior-care infrastructure.

Restraint Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & maintenance cost | -1.5% | Global, most severe in price-sensitive emerging markets | Long term (≥ 4 years) |

| Radiation-dose concerns and tightening regulation | -0.8% | EU & North America primarily, expanding globally | Medium term (2-4 years) |

| Reimbursement pressure in price-sensitive nations | -1.2% | APAC & Latin America primarily | Medium term (2-4 years) |

| Shortage of CT-trained radiologic technologists | -0.9% | North America & EU, emerging in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Maintenance Cost

Capital outlays for premium scanners can exceed USD 2 million per unit and the supply-chain burden equals up to 20% of manufacturing revenue, compressing margins for vendors. Semiconductor vulnerabilities, highlighted by disruptions to high-purity quartz mining, threaten downstream component availability that keeps CT market production on schedule. Providers mitigate cost barriers by lengthening asset life cycles, leveraging cloud-hosted reconstruction engines, and adopting vendor financing that aligns payments with scan volumes. Smaller centers, facing elevated contract-labor expenses, must balance technology upgrades against financial sustainability.

Radiation-Dose Concerns and Tightening Regulation

Vacancy rates for technologists climbed from 8.7% in 2021 to 17.7% in 2023 and reached 18.1% in 2024. More than 1,400 open radiologist positions in the United States strain interpretation capacity. AI-guided positioning, protocol selection, and automatic dose adjustment reduce operator involvement and accelerate scan completion. Remote scanner operation pilots demonstrate that technologists can supervise devices across multiple sites from a centralized hub, although regulatory frameworks are still evolving.

Segment Analysis

By Technology: Mid-Slice Systems Anchor Installed Base

The CT market size for mid-slice platforms stood at USD 3.54 billion in 2024, reflecting 38.56% of global installations. This cohort balances throughput and affordability for routine diagnostics, yet demand is shifting toward high-slice scanners that deliver sub-second cardiac imaging and sub-millimeter isotropic resolution. High-slice models now grow at 6.89% CAGR as cardiology, oncology, and trauma specialists prioritize spectral decomposition and whole-organ perfusion. Photon-counting detectors further elevate the premium tier by enhancing contrast-to-noise ratios while trimming radiation dose, a proposition valued by pediatric and serial-follow-up protocols. Manufacturers leverage modular gantry designs that allow in-field upgrades from 128-slice to 256-slice, protecting capital budgets. Clinical evidence underscores diagnostic superiority: vessel sharpness scores of 134.7 HU/mm versus 100.9 HU/mm for energy-integrating predecessors. Health systems consolidate procurement around fewer, more capable units, reinforcing high-slice momentum within the CT market.

At the opposite end, low-slice scanners preserve relevance in emergency and point-of-care deployments where quick setup, minimal shielding, and favorable pricing outweigh resolution demands. Rural hospitals adopt 16-slice units mounted on mobile trailers for trauma triage, expanding CT market access without expensive room construction. Convergence between cone-beam and multidetector domains blurs boundaries as algorithms correct cone-beam artifacts, widening their clinical scope.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Product Type: Mobile Solutions Gain Momentum

Stationary scanners accounted for 62.67% of Computed Tomography (CT) market share in 2024, anchored within hospitals and diagnostic centers that need high uptime and integration with RIS/PACS networks. Vendors differentiate through AI-reconstruction engines that shorten scan-to-view times and through iterative dose-reduction software that aligns with upcoming radiation-reporting mandates. However, mobile and portable devices represent the fastest-growing category as emergency-medicine teams deploy them in ambulances and field clinics. ARPA-H’s USD 12 million grant to develop rugged mobile platforms validates institutional confidence in transportable solutions.

Revenue opportunity escalates when mobile stroke units demonstrate 30-minute reductions in time to thrombolysis, translating to improved patient outcomes and lower long-term neuro-rehabilitation expenses. ICU adoption is high, with 97% of physicians reporting portable head CT utility to avoid transporting unstable patients. Manufacturing collaborations such as GE HealthCare and Kalbe’s facility expansion in Southeast Asia shorten lead times and localize service, supporting mobile-segment expansion.

By Application: Oncology Leadership with Dental Surge

Oncology remains the largest revenue contributor, with a 31.82% share of Computed Tomography (CT) market size in 2024. Low-dose protocols and spectral mapping refine tumor delineation, while AI contouring accelerates radiation-therapy planning for head-and-neck and lung cases. Population-based lung-cancer screening programs reinforce baseline imaging volumes and require scanners capable of sub-low-dose operation without compromising nodule detectability. Cardiology follows closely, boosted by the Medicare payment jump for coronary CT angiography to USD 357, which doubles prior reimbursement and fortifies outpatient uptake.

Dental and maxillofacial indications exhibit the highest 7.11% CAGR as cone-beam CT becomes routine for implant planning and orthognathic assessment. Dental clinics appreciate compact footprints and plug-and-play installation that bypass costly lead shielding. Traumatology and emergency medicine continue to rely on ultra-fast gantry rotation and extended coverage to survey polytrauma patients within seconds. Musculoskeletal sub-segments benefit from photon-counting clarity that distinguishes cortical bone micro-architecture from adjacent soft tissue.

By End-User: Ambulatory Centers Accelerate Growth

Hospitals controlled 61.48% of Computed Tomography (CT) market share in 2024, leveraging 24/7 staffing and multidisciplinary teams that manage complex cases. Integration with enterprise data lakes enables AI triage that aligns resource allocation to acuity, though staffing shortfalls trigger workflow bottlenecks. Diagnostic imaging centers sustain volume through convenient scheduling and transparent pricing, capturing elective referrals. Ambulatory surgical centers, buoyed by relaxed certificate-of-need regulations, exhibit a 7.34% CAGR as insurers push procedures toward lower-cost venues.

Dental offices and oral-surgery suites embrace in-office cone-beam units that improve patient engagement through same-day diagnostics. Veterinary hospitals begin adopting dedicated scanners for advanced orthopedic and oncologic care in companion animals, hinting at a nascent yet specialized Computed Tomography (CT) market niche. Academic institutions expand high-slice capacity to support imaging trials valued at USD 1.23 billion in 2024, positioning themselves to attract grant funding and pharmaceutical partnerships.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Device Architecture: Spiral Systems Maintain Dominance

Spiral or helical systems maintained 68.82% share of Computed Tomography (CT) market size in 2024, validated by decades of clinical familiarity and steady improvements in iterative reconstruction that halves noise while trimming dose. Their continuous table motion suits angiography, trauma, and multiphase organ exams. Ring-gantry systems, growing at 7.58% CAGR, find favor in radiation-therapy suites and specialized cardiology labs that exploit stationary patient tables for motion-free acquisitions. Vendors deploy ring-gantry photon-counting designs that allow ultra-high-resolution inner-ear imaging and coronary plaque characterization in sub-second sequences.

C-arm and O-arm configurations dominate intra-operative imaging, especially in spinal and orthopedic surgery where real-time guidance enhances screw placement accuracy. Flat-panel detector CT devices combine high dynamic range with compact geometry, serving image-guided interventions in hybrid ORs lacking space for full-size scanners. Architecture diversification signals that manufacturers tailor gantry mechanics to setting-specific constraints, thereby expanding total CT market addressability.

Geography Analysis

North America held 42.23% of Computed Tomography (CT) market share in 2024, anchored by extensive modality fleets, robust reimbursement, and rapid adoption of photon-counting systems. Medicare’s doubled payment for coronary CT angiography incentivizes outpatient service expansion. Strategic alliances such as GE HealthCare’s seven-year deal with Sutter Health pair capital investment with workforce-development programs that aim to ease technologist shortages. The region prepares for compulsory radiation-dose reporting by 2027, prompting hospitals to upgrade to low-dose software and analytics dashboards. Teleradiology and remote scanner operation trials gain momentum as a mitigation strategy for rural staffing deficits.

Asia-Pacific registers the fastest 7.82% CAGR through 2030, propelled by large-scale government investment in healthcare infrastructure and expansion of point-of-care imaging. Local manufacturing partnerships, including GE HealthCare–Kalbe’s Indonesian plant and Wipro GE’s USD 959 million capacity build-out, shorten supply chains and reduce cost barriers for regional buyers. Population aging and escalating lifestyle-related diseases underpin higher imaging demand, while cloud-enabled AI platforms lower entry hurdles for smaller centers. National cancer-screening mandates across China, Japan, and South Korea stimulate sustained procurement of low-dose CT technology.

Europe retains a robust installed base, propelled by stringent quality standards that favor premium detector technology and eco-friendly workflow solutions. Environmental policies encourage procurement of scanners with intelligent power-saving modes and recyclable component designs. Middle East and Africa undergo rapid modernization with public-private partnerships that fund tertiary hospitals equipped with advanced CT suites; GE HealthCare’s collaboration with Dr. Sulaiman Al-Habib Medical Group exemplifies value-chain localization. South America experiences steady growth led by Brazil’s nationwide telehealth roll-outs, although constrained fiscal space and complex import regulations temper the pace of high-end scanner adoption.

Get Analysis on Important Geographic Markets

Download PDF

Competitive Landscape

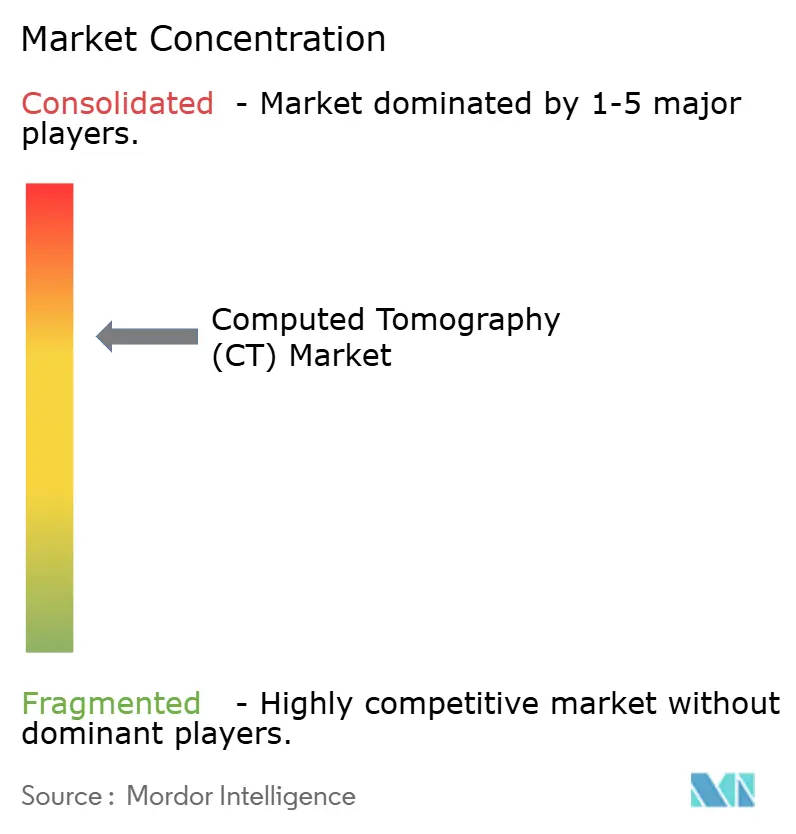

Competitive intensity in the Computed Tomography (CT) market is moderate yet rising as incumbents fuse hardware excellence with AI-driven analytics. GE HealthCare’s Revolution Vibe platform halves cardiac scan times through “Unlimited One-Beat” technology and pairs with NVIDIA to prototype autonomous positioning that reduces labor dependency. Siemens Healthineers leads photon-counting commercialization and channels USD 350 million toward CT R&D, cementing first-mover advantage. Philips focuses on spectral detector integration linked with cloud-based operational dashboards that predict tube replacement and minimize downtime.

Mid-tier players pursue niche leadership: Arineta secures FDA clearance for low-dose dual-organ screening, while NeuroLogica refines mobile platforms for combat casualty care. Acquisition strategy remains active; RadNet committed over USD 54 million to imaging-center and AI start-up purchases in 2024, enhancing vertical integration. AI companies that deliver automated triage and structured reporting become attractive targets, as evidenced by GE HealthCare’s USD 51 million purchase of Intelligent Ultrasound’s clinical AI portfolio.

White-space opportunities include rural imaging networks, cloud-native reconstruction services, and subscription-based detector upgrades. Vendors experiment with outcome-based pricing tied to reduction in repeat scans or faster diagnostic throughput. Market entrants emphasize portability and battery operation to penetrate disaster-relief and battlefield medicine niches. Overall, the Computed Tomography (CT) market values hybrid strategies that blend hardware innovation, software ecosystems, and service-oriented business models to sustain differentiation.

Computed Tomography (CT) Industry Leaders

-

Canon Medical Systems Corporation

-

GE Healthcare

-

Koninklijke Philips NV

-

Siemens Healthineers

-

Fujifilm Holdings Corporation

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- July 2025: Siemens Healthineers unveiled the SOMATOM Pro.Pulse dual-source CT at AOCR 2025, optimized for variable heart rates and equipped with AI-driven scan assistants

- March 2025: Siemens Healthineers received FDA clearance for the Naeotom Alpha.Prime, the first commercial single-source photon-counting CT system

- March 2025: GE HealthCare launched the Revolution Vibe CT with Unlimited One-Beat Cardiac mode, reducing scan time by 50%.

Global Computed Tomography (CT) Market Report Scope

As per the scope of the report, computed tomography (CT) is an imaging process that customizes special X-ray equipment to generate a sequence of exhaustive images or scans of areas inside the body. The Computed Tomography (CT) Market is Segmented by Type (Low Slice, Medium Slice, and High Slice), by Application (Oncology, Neurology, Cardiovascular, Musculoskeletal, and Other Applications), by End User (Hospitals, Diagnostic Centers, and Other End Users), and by Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market size and forecast in value (USD million) for the above segments.

By Technology (Slice Count)

| Low-slice (<64) |

| Mid-slice (64) |

| High-slice (128–256) |

By Product Type

| Stationary CT Scanners |

| Portable / Mobile CT Scanners |

| Consumables and Accessories |

| Software and Services |

By Application

| Oncology | Lung Cancer Screening |

| Head & Neck Oncology | |

| Colorectal Oncology | |

| Other Oncology | |

| Cardiology | Coronary CT Angiography |

| Calcium Scoring | |

| Structural Heart Disease | |

| Neurology | Stroke Assessment |

| Brain Trauma | |

| Vascular | Peripheral Vascular Disease |

| Pulmonary Angiography | |

| Musculoskeletal | Orthopedic Trauma |

| Sports Injuries | |

| Dental & Maxillofacial | |

| Trauma & Emergency | |

| Other Applications |

By End-User

| Hospitals | Public Hospitals |

| Private Hospitals | |

| Diagnostic Imaging Centers | |

| Ambulatory Surgical Centers | |

| Dental Clinics | |

| Veterinary Clinics & Hospitals | |

| Academic & Research Institutes |

By Device Architecture

| Spiral / Helical CT |

| Ring-Gantry CT |

| C-arm CT |

| O-arm CT |

| Flat-Panel Detector CT |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Technology (Slice Count) | Low-slice (<64) | |

| Mid-slice (64) | ||

| High-slice (128–256) | ||

| By Product Type | Stationary CT Scanners | |

| Portable / Mobile CT Scanners | ||

| Consumables and Accessories | ||

| Software and Services | ||

| By Application | Oncology | Lung Cancer Screening |

| Head & Neck Oncology | ||

| Colorectal Oncology | ||

| Other Oncology | ||

| Cardiology | Coronary CT Angiography | |

| Calcium Scoring | ||

| Structural Heart Disease | ||

| Neurology | Stroke Assessment | |

| Brain Trauma | ||

| Vascular | Peripheral Vascular Disease | |

| Pulmonary Angiography | ||

| Musculoskeletal | Orthopedic Trauma | |

| Sports Injuries | ||

| Dental & Maxillofacial | ||

| Trauma & Emergency | ||

| Other Applications | ||

| By End-User | Hospitals | Public Hospitals |

| Private Hospitals | ||

| Diagnostic Imaging Centers | ||

| Ambulatory Surgical Centers | ||

| Dental Clinics | ||

| Veterinary Clinics & Hospitals | ||

| Academic & Research Institutes | ||

| By Device Architecture | Spiral / Helical CT | |

| Ring-Gantry CT | ||

| C-arm CT | ||

| O-arm CT | ||

| Flat-Panel Detector CT | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

What revenue and growth trajectory is projected for the Computed Tomography market through 2030?

The market is expected to rise from USD 9.17 billion in 2025 to USD 12.34 billion by 2030, reflecting a 6.12% CAGR.

Which technology segment drives the majority of current installations?

Mid-slice (64-slice) scanners captured 38.56% of 2024 revenue because they balance clinical capability with capital cost.

Why is photon-counting CT considered a game changer?

Photon-counting detectors achieve 0.2 mm resolution and provide intrinsic spectral data, reclassifying over half of coronary patients to lower-severity categories in early studies.

Which region will post the fastest growth in CT adoption?

Asia-Pacific is forecast to grow at 7.82% CAGR to 2030 due to large-scale infrastructure investments and expanding healthcare access in China and India.

How are sustainability goals influencing CT procurement?

EU and North American hospitals increasingly require energy-efficient scanners, with studies showing automated power-down routines can cut energy use by up to one-third over a scanners life.

Page last updated on: