| Study Period | 2019 - 2030 |

| Market Size (2025) | USD 5.78 Billion |

| Market Size (2030) | USD 7.53 Billion |

| CAGR (2025 - 2030) | 5.43 % |

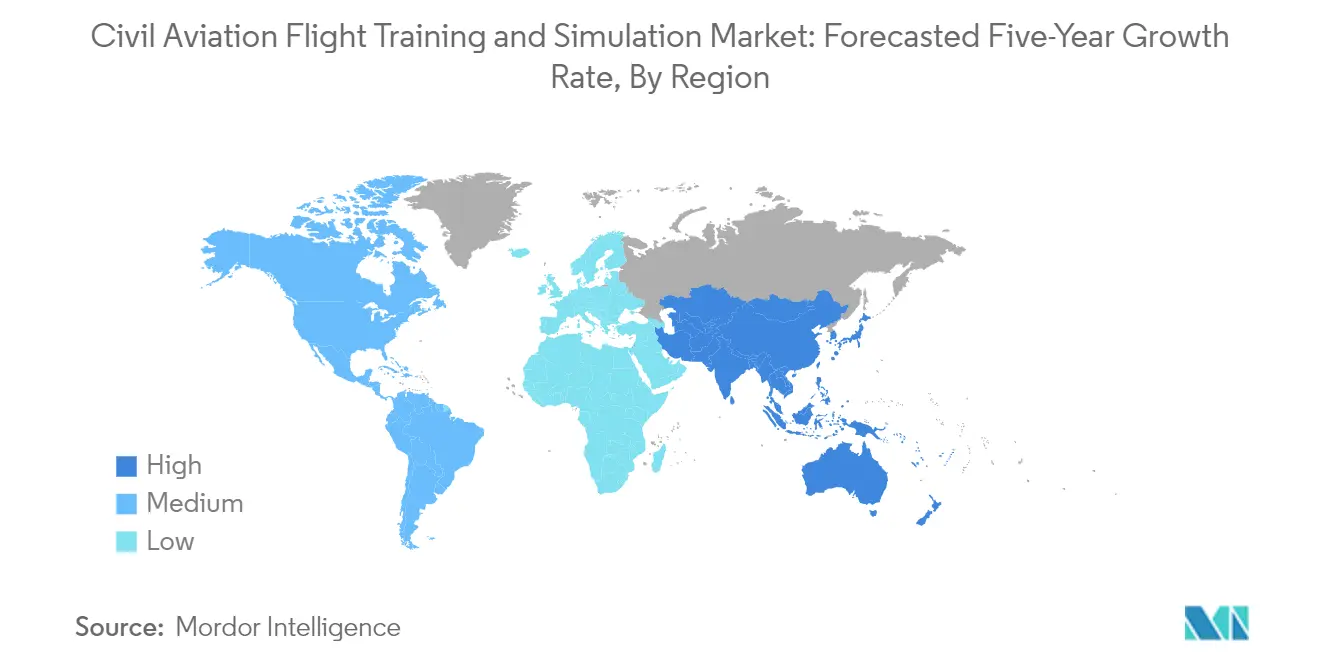

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

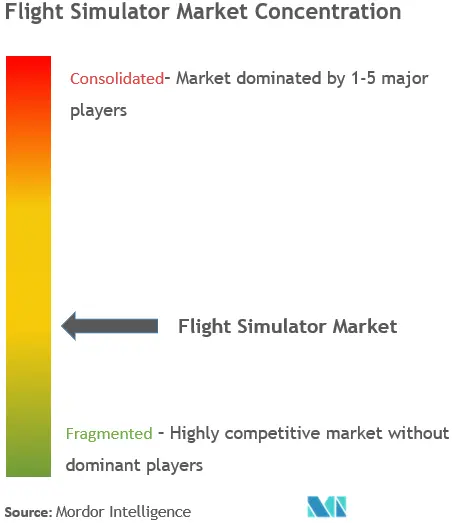

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Civil Aviation Flight Training And Simulation Market Analysis

The Civil Aviation Flight Training And Simulation Market size is estimated at USD 5.78 billion in 2025, and is expected to reach USD 7.53 billion by 2030, at a CAGR of 5.43% during the forecast period (2025-2030).

The civil aviation flight training and simulation industry is experiencing significant transformation driven by technological advancement and increasing air traffic demands. According to Boeing's 2022 Pilot & Technician Outlook, the industry will require 602,000 new civil aviation pilots over the next 20 years to maintain operational capacity. This substantial demand has catalyzed investments in advanced aviation training infrastructure, with major airlines and training providers expanding their capabilities through strategic partnerships and facility developments. The integration of artificial intelligence, virtual reality, and data analytics in aviation training programs has become increasingly prevalent, enabling more efficient and comprehensive pilot training programs.

The industry is witnessing a surge in strategic collaborations between airlines, training providers, and simulator manufacturers to enhance training capabilities. In February 2023, Gen2Fly Flybiz entered into a significant agreement with Avion to supply eight Airbus A320 full flight simulators, demonstrating the industry's commitment to expanding training infrastructure. Similarly, Emirates Airlines announced a USD 135 million investment in a new pilot training center in 2023, which will increase their training capacity by 54% annually through the addition of six new full flight simulator bays. These developments reflect the industry's proactive approach to addressing future pilot training demands.

Major aircraft manufacturers are actively contributing to the evolution of flight training methodologies. In 2022, Airbus and Boeing collectively delivered 1,156 commercial aircraft (676 and 480 respectively), necessitating comprehensive commercial aviation training solutions for airline operators. The industry has responded with innovative approaches to flight simulation, including the integration of advanced simulation technologies and the development of specialized training programs. Boeing's introduction of its 737 Max flight simulator to the Shanghai training center in April 2023 exemplifies the industry's commitment to providing localized, state-of-the-art training facilities.

The market is experiencing a significant shift toward digital transformation and sustainable practices in training operations. Training providers are increasingly incorporating sustainable aviation fuel (SAF) awareness and electric aircraft operations into their programs. Advanced features such as graphical flight deck simulation and interactive representation provisions have been integrated into new aviation simulation systems, enabling more diverse and realistic training scenarios. The industry's focus on technological innovation is further evidenced by the development of high-fidelity virtual reality simulators and immersive tools, which are helping reduce training costs while maintaining high safety standards.

Civil Aviation Flight Training And Simulation Market Trends

Airline Expansion Plans Driving Demand for Pilots

The global aviation industry is experiencing unprecedented growth in air passenger traffic, creating an urgent demand for qualified pilots worldwide. According to the International Air Transport Association (IATA), global air passenger traffic reached 3.11 billion in 2022, demonstrating the robust recovery and expansion of the aviation sector. This surge in passenger numbers has prompted airlines to significantly expand their fleets, with Boeing's 2022 Pilot & Technician Outlook projecting a requirement for 602,000 new civil aviation pilots by 2041. The expansion is further evidenced by major aircraft orders, such as American Airlines' March 2024 contract with Boeing for 85 737-10s and 85 A321neos, highlighting the industry's commitment to fleet modernization and growth.

The increasing fleet size has created a critical need for enhanced pilot training infrastructure and capabilities. Airlines are responding by investing heavily in training facilities and simulators, as demonstrated by United Airlines' February 2024 opening of a new 150,000-square-foot building at its Flight Training Center in Denver, equipped with 12 cutting-edge full-motion flight simulators. The pilot shortage is particularly acute in the United States, where the Bureau of Labor Statistics reported 105,500 commercial airline pilots in 2023, with projections indicating a growing gap between supply and demand. Airlines are implementing various strategies to address this shortage, including establishing their own training academies, creating partnerships with professional training institutions, and developing comprehensive pilot training programs to build a sustainable pipeline of qualified aviators.

Understand The Key Trends Shaping This Market

Download PDF

Growing Adoption of Programs Like Multi-Crew Pilot License (MPL)

The aviation industry is witnessing a significant shift towards more efficient and technology-driven training methodologies, particularly through the adoption of Multi-Crew Pilot License (MPL) programs. These programs represent a modern approach to pilot training, utilizing advanced simulator technologies to produce highly competent pilots in a more time-efficient and cost-effective manner. The MPL program's structure emphasizes competency-based training and assessment (CBTA), as evidenced by recent developments such as the February 2024 inauguration of Embraer and CAE's E-Jets E2 full flight simulator in Singapore, which incorporates CAE's CBTA courseware and interactive classroom instruction utilizing advanced simulation technology.

The MPL program's effectiveness is enhanced by the latest advancements in simulation technology, including full-flight simulators (FFS) that can replicate precise flight parameters and provide more than 180-degree views with satellite-quality visuals. These simulators have evolved from the traditional A through D grading system to a more comprehensive seven-level international standard, with Type 7 (formerly Level D) representing the highest certification level for commercial pilot training. The integration of sophisticated features such as virtual reality (VR) and spatial orientation exercises in modern simulators has made MPL programs increasingly attractive to airlines and training institutions. This technological evolution, combined with the program's focus on airline-specific training from the outset, has led to growing industry acceptance and adoption of MPL as a viable pathway for developing the next generation of commercial pilots.

Segment Analysis: Simulator Type

Full Flight Simulator (FFS) Segment in Civil Aviation Flight Training and Simulation Market

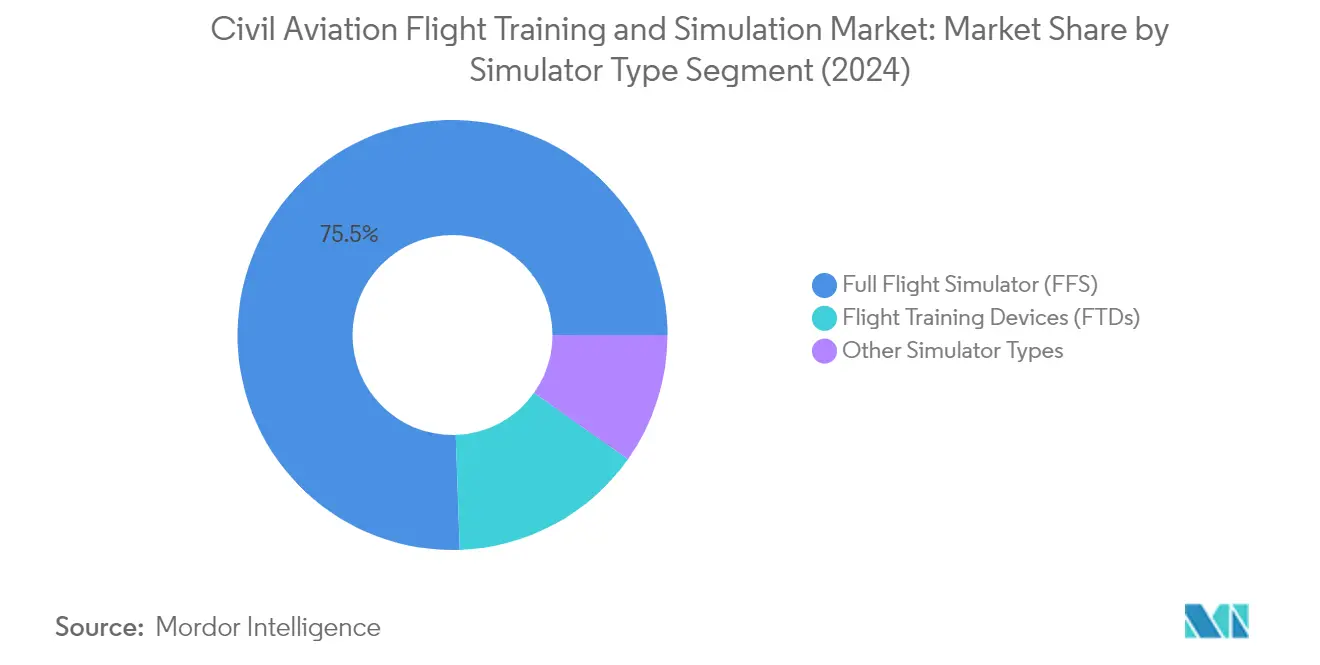

Full Flight Simulators (FFS) dominate the civil aviation flight training and simulation market, commanding approximately 76% market share in 2024. This significant market position is attributed to the growing adoption of advanced full flight simulator technologies by airlines and training academies worldwide. FFS systems provide the most realistic and comprehensive training experience, replicating actual aircraft cockpits with high-fidelity motion systems and sophisticated visual displays. These simulators are particularly valuable for commercial pilot training as they can simulate various weather conditions, emergency scenarios, and complex flight situations without any real-world risks. The increasing focus on pilot safety and proficiency, coupled with stringent regulatory requirements for pilot training, continues to drive the demand for full flight simulator systems across major aviation markets.

Flight Training Devices (FTD) Segment in Civil Aviation Flight Training and Simulation Market

Flight Training Devices (FTDs) represent a rapidly evolving segment in the civil aviation flight training and simulation market. These devices are gaining significant traction due to their cost-effectiveness and versatility in providing essential training capabilities. FTDs offer a more accessible alternative to full flight simulators while maintaining sufficient fidelity for procedural training and basic flight operations. The segment is witnessing increased adoption among flight schools and smaller training organizations that require reliable training solutions without the substantial investment associated with full flight simulators. Modern FTDs incorporate advanced features such as high-definition visual systems, realistic cockpit layouts, and sophisticated software that can simulate various aircraft types and flight conditions, making them increasingly attractive for both initial and recurrent pilot training programs.

Remaining Segments in Simulator Type

Other simulator types in the market include Basic Aviation Training Devices (BATDs), Advanced Aviation Training Devices (AATDs), and various specialized training solutions. These systems play a crucial complementary role in the overall pilot training ecosystem by providing specific training capabilities for different stages of pilot development. While these simulators may not offer the same level of sophistication as FFS or FTDs, they serve essential functions in areas such as basic instrument training, procedure practice, and familiarization with fundamental flight concepts. The continued evolution of these alternative simulator types, particularly with the integration of new technologies like virtual reality and augmented reality, ensures their relevance in comprehensive pilot training programs.

Segment Analysis: Aircraft Type

Fixed-Wing Segment in Civil Aviation Flight Training and Simulation Market

The fixed-wing segment continues to dominate the civil aviation flight training and simulation market, commanding approximately 76% market share in 2024. This significant market position is primarily driven by the increasing demand for commercial aircraft pilots worldwide, particularly in regions experiencing rapid aviation sector growth like Asia-Pacific and the Middle East. The segment's dominance is further reinforced by the extensive fleet expansion plans of major airlines globally, with many carriers placing substantial orders for narrow-body and wide-body aircraft. Additionally, the growing adoption of advanced aircraft simulation technologies for fixed-wing aircraft training, including full flight simulators (FFS) and flight training devices (FTD), has strengthened this segment's market position. The implementation of stringent safety regulations and the increasing emphasis on pilot proficiency have also contributed to the sustained growth of fixed-wing training and simulation solutions.

Rotary-Wing Segment in Civil Aviation Flight Training and Simulation Market

The rotary-wing segment is experiencing robust growth in the civil aviation flight training and simulation market, driven by increasing demand for helicopter pilots across various civilian applications including emergency medical services, offshore operations, and corporate transport. The segment is witnessing significant technological advancements in simulation capabilities, with manufacturers developing more sophisticated and realistic helicopter simulation systems that accurately replicate complex maneuvers and emergency procedures. The adoption of advanced virtual reality and augmented reality technologies in rotary-wing training programs has enhanced the quality and effectiveness of pilot training. Furthermore, the growing emphasis on safety regulations and the need for specialized training in challenging environments has led to increased investments in helicopter simulation facilities worldwide. The segment is also benefiting from the expansion of helicopter operations in emerging markets and the rising demand for skilled rotary-wing pilots in the commercial sector.

Segment Analysis: Training Type

Simulator Segment in Civil Aviation Flight Training and Simulation Market

The simulator segment dominates the civil aviation flight training and simulation market, accounting for approximately 54% of the total market value in 2024. This significant market share can be attributed to the increasing adoption of advanced simulators by airlines and training organizations to provide comprehensive pilot simulation in a safe and controlled environment. The segment's dominance is further strengthened by the growing emphasis on simulation-based training to enhance pilot proficiency across various scenarios and emergency situations. Modern flight simulators incorporate cutting-edge technologies such as high-fidelity visual systems, motion platforms, and realistic cockpit simulation environments, making them indispensable tools for pilot training. Additionally, the cost-effectiveness of simulator training compared to actual aircraft training, coupled with the ability to replicate diverse weather conditions and emergency scenarios, has made simulators the preferred choice for airlines and training institutions worldwide.

Growth Trajectory of Simulator Segment in Civil Aviation Flight Training Market

The simulator segment is projected to exhibit the strongest growth trajectory in the civil aviation flight training and simulation market, with an expected growth rate of approximately 5% during the forecast period 2024-2029. This robust growth is driven by several factors, including the increasing adoption of advanced simulators to train pilots in various scenarios and rising spending from Original Equipment Manufacturers (OEMs) on the design and development of simulators. The growth is further fueled by technological advancements in simulation systems, including improved visual fidelity, enhanced motion systems, and more realistic flight dynamics modeling. The integration of artificial intelligence and virtual reality technologies in flight simulators is also contributing to the segment's growth, enabling more immersive and effective training experiences. Additionally, the growing focus on safety regulations and the need for standardized training protocols across the aviation industry continue to drive the demand for sophisticated simulation systems.

Civil Aviation Flight Training And Simulation Market Geography Segment Analysis

Civil Aviation Flight Training and Simulation Market in North America

North America represents a dominant force in the global civil aviation flight simulation and aviation training market, driven by the presence of major simulator manufacturers, numerous flight training academies, and a robust commercial aviation sector. The United States and Canada form the key markets in this region, with both countries demonstrating strong infrastructure for pilot training programs. The region benefits from advanced technological adoption in flight simulation, established regulatory frameworks, and continuous investments in upgrading training facilities.

Civil Aviation Flight Training and Simulation Market in United States

The United States maintains its position as the largest market within North America, commanding approximately 91% of the regional market share in 2024. The country's dominance is attributed to its well-flourished aviation industry, hosting the world's largest aircraft fleet and extensive network of airports. The presence of major flight schools, advanced training centers, and partnerships between airlines and training providers further strengthens the market. The country has also implemented various regulatory measures and pilot training programs to address the growing demand for commercial pilots, while continuously upgrading its simulation technology infrastructure.

Civil Aviation Flight Training and Simulation Market in Canada

Canada emerges as the fastest-growing market in North America, with a projected growth rate of approximately 6% from 2024 to 2029. The country's aviation training sector is experiencing significant expansion driven by increasing demand for commercial pilots and substantial investments in training infrastructure. Canadian flight training institutions are actively adopting advanced aviation simulation technologies and forming strategic partnerships with international aviation organizations. The country's focus on sustainable aviation practices and implementation of innovative training methodologies continues to attract aspiring pilots from across the globe.

Civil Aviation Flight Training and Simulation Market in Europe

Europe represents a significant market for civil aviation flight training and simulation, characterized by its strong presence of aviation industry players and advanced training infrastructure. The region encompasses key markets including the United Kingdom, Germany, France, and Italy, each contributing significantly to the overall market landscape. European countries have been at the forefront of adopting innovative training methodologies and implementing stringent safety standards in pilot training programs.

Civil Aviation Flight Training and Simulation Market in United Kingdom

The United Kingdom stands as the largest market within Europe, holding approximately 38% of the regional market share in 2024. The country's prominent position is supported by its comprehensive network of flight training academies and advanced simulation facilities. The UK's aviation training sector benefits from strong regulatory oversight, established relationships with major airlines, and continuous investments in modernizing training infrastructure. The presence of major aviation industry players and their commitment to pilot training excellence further reinforces the UK's market leadership.

Civil Aviation Flight Training and Simulation Market in France

France emerges as the fastest-growing market in Europe, with a projected growth rate of approximately 6% from 2024 to 2029. The country's aviation training sector is witnessing substantial development through strategic initiatives and technological advancements in simulation training. French aviation academies are increasingly adopting state-of-the-art training methodologies and forming partnerships with international aviation organizations. The country's strong aerospace industry foundation and commitment to innovation in pilot training continue to drive market growth.

Civil Aviation Flight Training and Simulation Market in Asia-Pacific

The Asia-Pacific region represents a rapidly evolving market in the global civil aviation flight training and simulation landscape, encompassing key markets such as China, India, Japan, and South Korea. The region's aviation training sector is experiencing significant transformation driven by increasing air traffic, expanding airline fleets, and growing demand for trained pilots. Each country in the region is developing its unique strengths in aviation training while addressing the challenges of infrastructure development and technological adoption.

Civil Aviation Flight Training and Simulation Market in China

China maintains its position as the largest market in the Asia-Pacific region, demonstrating strong growth in civil aviation training infrastructure. The country's aviation training sector benefits from substantial investments in flight simulation technology, partnerships with international training providers, and growing domestic demand for commercial pilots. Chinese aviation academies are increasingly focusing on developing comprehensive training programs while adopting advanced simulation technologies to enhance training effectiveness.

Civil Aviation Flight Training and Simulation Market in India

India emerges as the fastest-growing market in the Asia-Pacific region, showing remarkable progress in developing its aviation training capabilities. The country's aviation training sector is witnessing significant expansion through the establishment of new training centers and adoption of advanced simulation technologies. Indian aviation authorities are actively implementing regulatory reforms and fostering partnerships with international training providers to enhance the quality of pilot training programs.

Civil Aviation Flight Training and Simulation Market in Latin America

The Latin American market for civil aviation flight training and simulation demonstrates steady growth potential, with Brazil emerging as both the largest and fastest-growing market in the region. The region's aviation training sector is characterized by increasing investments in training infrastructure and growing adoption of advanced simulation technologies. Latin American countries are focusing on modernizing their training facilities and forming international partnerships to enhance their training capabilities. The region's aviation academies are actively working to address the growing demand for commercial pilots while implementing innovative training methodologies.

Civil Aviation Flight Training and Simulation Market in Middle East & Africa

The Middle East & Africa region presents significant opportunities in the civil aviation flight training and simulation market, with the United Arab Emirates leading as the largest market and Saudi Arabia showing the fastest growth. The region's aviation training sector benefits from substantial investments in state-of-the-art training facilities and strong support from government initiatives. Middle Eastern carriers are actively expanding their training capabilities through partnerships with international training providers and investments in advanced simulation technologies. The region's focus on becoming a global aviation hub continues to drive developments in pilot training infrastructure and capabilities.

Get Analysis on Important Geographic Markets

Download PDF

Civil Aviation Flight Training And Simulation Industry Overview

Top Companies in Civil Aviation Flight Training and Simulation Market

The civil aviation flight simulation and aviation training market is characterized by continuous product innovation across both aircraft and simulator segments. Companies are heavily investing in developing advanced aviation simulation technologies incorporating artificial intelligence, virtual reality, and data analytics to enhance training effectiveness. Operational agility is demonstrated through flexible training programs and customizable simulation solutions that adapt to varying customer requirements. Strategic partnerships between training providers and airlines have become increasingly common to ensure standardized training delivery and cost optimization. Market leaders are expanding their geographical presence through new training centers and simulator deployments while also focusing on sustainability initiatives like electric aircraft development and sustainable aviation fuel integration. The industry shows a strong emphasis on digital transformation with the implementation of e-learning platforms, virtual classrooms, and data-driven training systems to improve accessibility and training outcomes.

Consolidated Market Led By Global Players

The civil aviation flight training and simulation market exhibits a high degree of consolidation with a few global players dominating the landscape. Companies like CAE Inc., Boeing, and Airbus maintain significant market presence through their comprehensive training solutions and extensive network of training centers. The simulator segment shows particularly strong consolidation with CAE Inc. holding a dominant position, while the aircraft training segment is more distributed among specialized manufacturers like Pilatus Aircraft and Diamond Aircraft. The market structure reflects a mix of large aerospace conglomerates that offer end-to-end aviation solutions and specialized training providers focused on specific market segments.

The industry has witnessed strategic mergers and acquisitions aimed at expanding capabilities and market reach. Major players are acquiring smaller, specialized companies to enhance their technological capabilities, particularly in areas like virtual reality and artificial intelligence-based training solutions. Regional expansion strategies often involve partnerships with local training providers or airlines to establish presence in high-growth markets. The market also sees collaboration between aircraft manufacturers and simulation providers to develop integrated training solutions that align with new aircraft technologies and regulatory requirements.

Innovation and Adaptability Drive Market Success

For incumbent companies to maintain and expand their market share, continuous investment in technological innovation and training methodology advancement is crucial. Success factors include developing comprehensive training ecosystems that integrate various learning platforms, maintaining strong relationships with regulatory authorities, and ensuring training programs adapt to evolving industry needs. Companies must also focus on sustainability initiatives and cost-effective training solutions to address growing industry concerns about environmental impact and operational efficiency. The ability to offer standardized yet customizable training programs across global markets while maintaining consistent quality standards remains a key differentiator.

New entrants and smaller players can gain market share by focusing on specialized market segments or innovative training technologies. Success strategies include developing niche expertise in specific aircraft types or training methodologies, leveraging partnerships with established players for market access, and investing in digital solutions that offer cost advantages. The industry's high regulatory requirements and significant capital investments create substantial entry barriers, making strategic partnerships and focused market approaches essential for new competitors. Future success will increasingly depend on the ability to integrate emerging technologies, adapt to changing regulatory landscapes, and address the industry's growing emphasis on sustainable practices and cost efficiency. Additionally, the incorporation of aviation training equipment and flight training device innovations will be pivotal in enhancing training effectiveness and operational efficiency.

Civil Aviation Flight Training And Simulation Market Leaders

-

CAE Inc.

-

TRU Simulation + Training Inc. (Textron Inc.)

-

The Boeing Company

-

FlightSafety International Inc.

-

L3Harris Technologies, Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competiters?

Download PDF

Civil Aviation Flight Training And Simulation Market News

May 2024: The International Flight Training Center (IFTC) awarded HAVELSAN a contract to deliver an Airbus A320 NEO/CEO Full-Flight Simulator (FFS) with three engine options.

March 2024: Exail was awarded a contract by Fosen High School in Norway to deliver a new B737 Flight and Maintenance Training Device to provide a realistic and immersive experience for its students undergoing B737 maintenance and flight training programs.

Flight Simulator Market Report - Table of Contents

1. INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET DYNAMICS

- 4.1 Market Drivers

- 4.2 Market Restraints

-

4.3 Porter's Five Forces Analysis

- 4.3.1 Threat of New Entrants

- 4.3.2 Bargaining Power of Buyers/Consumers

- 4.3.3 Bargaining Power of Suppliers

- 4.3.4 Threat of Substitute Products

- 4.3.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

-

5.1 By Simulator Type

- 5.1.1 Full Flight Simulator (FFS)

- 5.1.2 Flight Training Devices (FDS)

- 5.1.3 Other Training Types

-

5.2 By Aircraft Type

- 5.2.1 Fixed-wing

- 5.2.2 Rotary-wing

-

5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.2 Europe

- 5.3.2.1 United Kingdom

- 5.3.2.2 Germany

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 South Korea

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 Latin America

- 5.3.4.1 Brazil

- 5.3.4.2 Rest of Latin America

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East and Africa

6. COMPETITIVE LANDSCAPE

- 6.1 Vendor Market Share

-

6.2 Company Profiles

- 6.2.1 CAE Inc.

- 6.2.2 FlightSafety International Inc.

- 6.2.3 L3 Harris Technologies Inc.

- 6.2.4 TRU Simulation + Training Inc. (Textron Inc.)

- 6.2.5 The Boeing Company

- 6.2.6 Frasca International Inc.

- 6.2.7 ALSIM EMEA

- 6.2.8 RTX Corporation

- 6.2.9 Airbus SE

- 6.2.10 Simcom Aviation Training

- 6.2.11 Pureflight Aviation Training

- 6.2.12 FAAC Inc.

- 6.2.13 Avion Group

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

You Can Purchase Parts Of This Report. Check Out Prices For Specific Sections

Get Price Break-up Now

Civil Aviation Flight Training And Simulation Industry Segmentation

Civil aviation flight training and simulation is designed to train aircraft pilots and crew members by simulating flight conditions. Simulation-based training encompasses using essential equipment or computers to model a real-world scenario. During training, the pilot understands and learns how to perform specific tasks or activities in various circumstances. Simulation is also helpful for reviewing and training pilots with new modifications to existing craft. Simulation software in the market delivers a robust virtual environment for analyzing, testing, and optimizing processes, systems, and operations.

The flight simulator market is segmented by simulator type, aircraft type, and geography. By simulator type, the market is segmented into full flight simulators (FFS), flight training devices (FTDs), and other training types. By aircraft type, the market is segmented into fixed-wing and rotary-wing. The report also covers the market sizes and forecasts for the aircraft flight recorder market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| By Simulator Type | Full Flight Simulator (FFS) | ||

| Flight Training Devices (FDS) | |||

| Other Training Types | |||

| By Aircraft Type | Fixed-wing | ||

| Rotary-wing | |||

| Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Latin America | Brazil | ||

| Rest of Latin America | |||

| Middle East and Africa | United Arab Emirates | ||

| Saudi Arabia | |||

| Rest of Middle East and Africa | |||

Need A Different Region or Segment?

Customize Now

Flight Simulator Market Research FAQs

How big is the Civil Aviation Flight Training And Simulation Market?

The Civil Aviation Flight Training And Simulation Market size is expected to reach USD 5.78 billion in 2025 and grow at a CAGR of 5.43% to reach USD 7.53 billion by 2030.

What is the current Civil Aviation Flight Training And Simulation Market size?

In 2025, the Civil Aviation Flight Training And Simulation Market size is expected to reach USD 5.78 billion.

Who are the key players in Civil Aviation Flight Training And Simulation Market?

CAE Inc., TRU Simulation + Training Inc. (Textron Inc.), The Boeing Company, FlightSafety International Inc. and L3Harris Technologies, Inc. are the major companies operating in the Civil Aviation Flight Training And Simulation Market.

Which is the fastest growing region in Civil Aviation Flight Training And Simulation Market?

Asia Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Civil Aviation Flight Training And Simulation Market?

In 2025, the North America accounts for the largest market share in Civil Aviation Flight Training And Simulation Market.

What years does this Civil Aviation Flight Training And Simulation Market cover, and what was the market size in 2024?

In 2024, the Civil Aviation Flight Training And Simulation Market size was estimated at USD 5.47 billion. The report covers the Civil Aviation Flight Training And Simulation Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Civil Aviation Flight Training And Simulation Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Our Best Selling Reports

Civil Aviation Flight Training And Simulation Market Research

Mordor Intelligence provides comprehensive insights into the civil aviation flight training and simulation industry. With decades of expertise in aviation training analysis, we cover the full range of flight simulation technologies. This includes full flight simulators, cockpit simulation systems, and advanced flight training devices. Our report, available as an easy-to-download PDF, offers a detailed analysis of aircraft simulation technologies and commercial pilot training methodologies used globally.

Our in-depth analysis benefits stakeholders across the aviation education sector. This includes providers of commercial aviation training and manufacturers of aviation training equipment. The report examines various aspects of pilot training systems, such as FSTDs (Flight Simulation Training Devices) and their applications in flight crew training. Stakeholders gain valuable insights into aviation simulation trends, commercial flight training developments, and technological advancements in the flight simulator market. This information enables informed decision-making for strategic planning and investment opportunities in the flight training system industry.